Don’t Look Back The Next Emerging-Market Decade Will Be Different

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBut looking back to assess the future is a questionable strategy. Instead, we think investors should focus on the changing dynamics in EM economies and markets that could reignite returns in the years ahead. Capturing this potential requires specialized research skills because EM companies and markets still march to a different beat than their developed-market (DM) peers.

From Boom to Bust: Two Eras in 20 Years

It’s easy to understand why expectations of EM are anchored to the past. From 2001 to 2010, as historic change swept through the developing world, the MSCI Emerging Markets Index posted supercharged annualized returns of 15.9%, outpacing DM stocks by a wide margin. Yet since 2011, EM equities have advanced by a paltry 0.9% annualized.

The EM bull market of 2001–2010 was fueled by unique circumstances. China joined the World Trade Organization in 2001, increasing its share of world exports and accelerating globalization. As this played out, China made massive investments in fixed assets and real estate, unleashing a commodities supercycle. From 2000–2010, China’s GDP grew by 10.6% on average, boosting global economic activity while enriching commodity-producing EM countries and supporting their currencies. Inside China, a wave of unbridled commercialism reshaped the business landscape in a colossal cultural shift that generated handsome payoffs for astute investors.

Since 2011, the EM tables have turned. Many EM economies suffered a hangover from the boom, caused by uncompetitive currencies and a failure to reform, particularly among commodity-exporting countries. Since 2014, the US dollar strengthened, eroding the competitiveness of EM exports. Commodity prices eased and geopolitical concerns intensified, from US–China trade wars to Russia’s invasion of Ukraine, while the COVID-19 pandemic added new challenges.

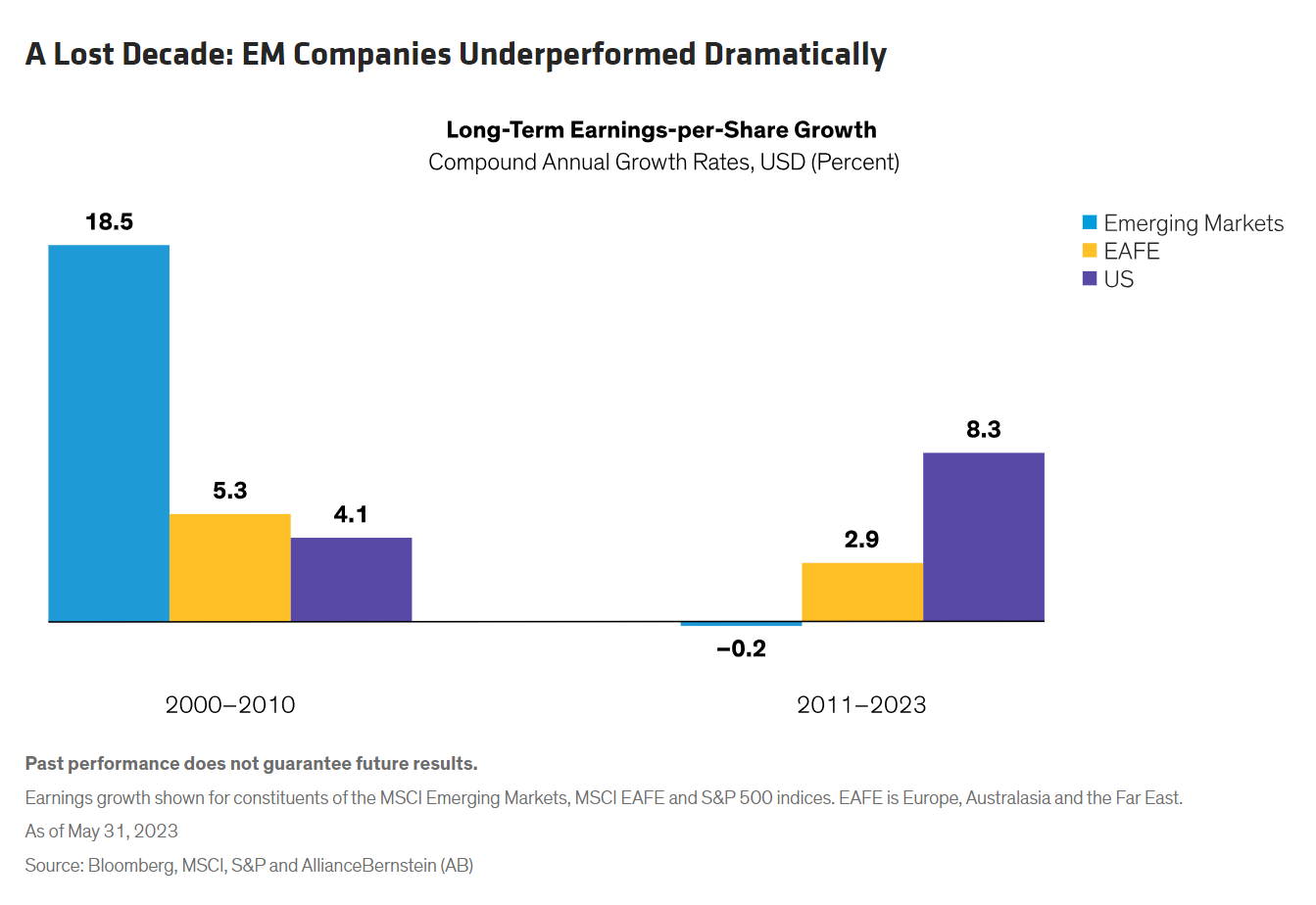

Meanwhile, in China, annual GDP growth slowed to 6.6% from 2011–2022 and is expected to decelerate to about 4.5% in the coming years, according to consensus estimates. Under President Xi Jinping, who came to power in 2013, China began to pursue a more assertive foreign policy and domestic economic reforms. More recently, China’s government has tempered support for entrepreneurialism in favor of a broader agenda focused on social equality. Against this backdrop, EM corporate earnings suffered a lost decade (Display), which suppressed equity returns.

What Next? Four Trends Could Revive EM Fortunes

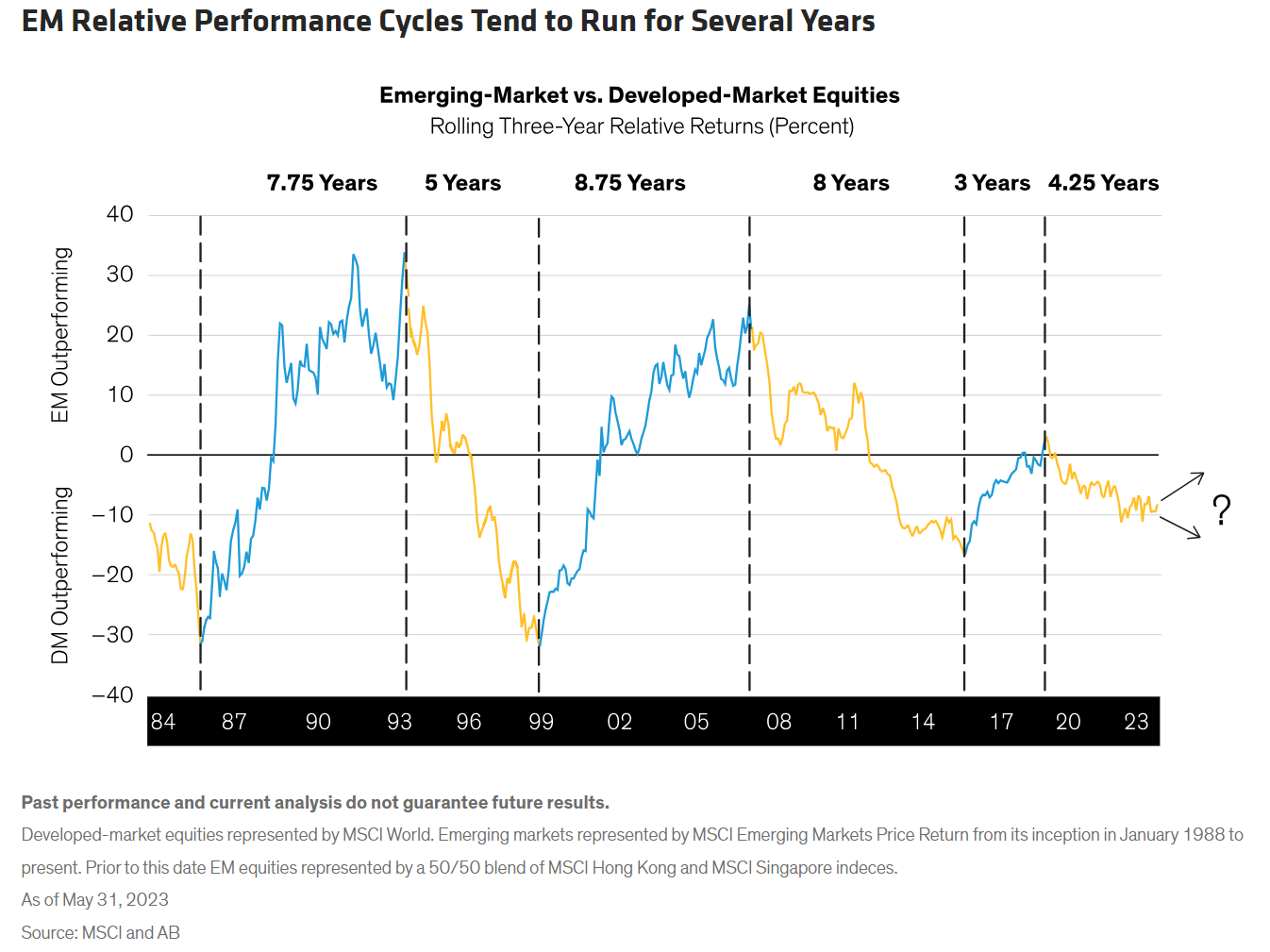

Will the next decade be as bleak for EM investors? We don’t think so. Our research shows that over the last four decades, EM stocks delivered prolonged periods of returns superior to those of DM peers (Display), which could materialize again after a sustained period of underperformance. Still, a potential recovery of EM stocks will be propelled by a very different set of forces. Four key trends will define the next EM era.

1. Innovation Will Be the New Impetus for Growth

Technology and innovation are the new engines for EM growth: they help countries leapfrog into competitive positions, empower consumers with digital capabilities and enable companies to participate in a global innovation bonanza—no matter where they are domiciled.

EM countries are leapfrogging DM countries in many areas. For example, the adoption of electric vehicles (EVs) in China reached 27% in 2021, more than four times the rate in the US. In mobile payments, China is a global trendsetter. Elsewhere in Asia, digital wallets accounted for about 30% of all retail point-of-sale transactions in 2022—about three times the European rate, according to the FIS Global Payments Report.

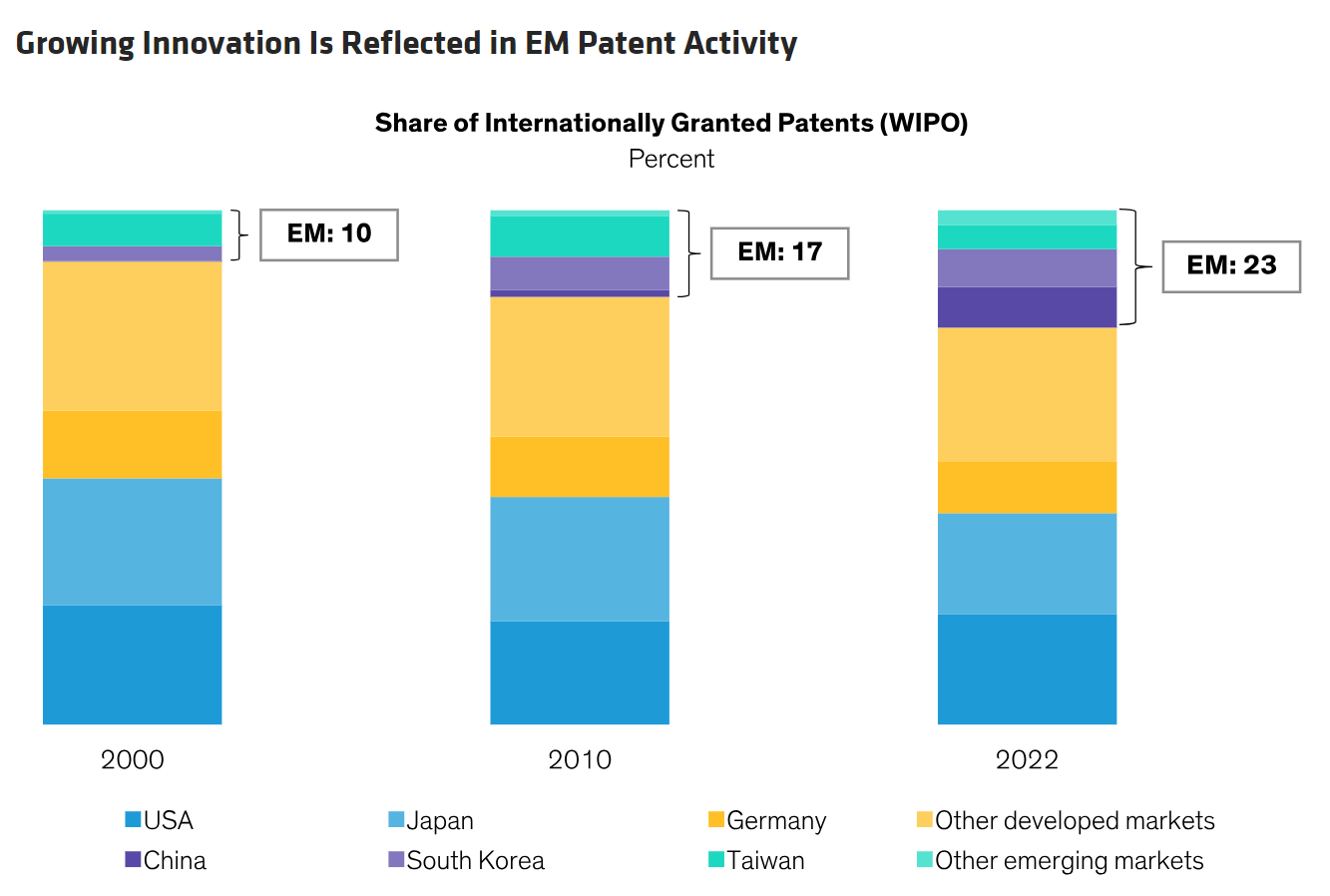

EM companies are active participants in the global technology revolution. Many components that enable AI are manufactured in EM countries. China is home to innovative companies that support global efforts to combat climate change. Developing countries have doubled their share of internationally filed patents since 2000, to 23% (Display).

Innovation helps explain why the MSCI EM index looks so different today than it did 20 years ago. At the end of 2022, six of the 10-largest benchmark holdings were “new economy” stocks, in industries such as technology and e-commerce, compared with only one such company in 2003. But remember—benchmarks are backward looking, as stocks are weighted based on past performance. We expect more changes to the EM benchmark as innovation sweeps through industries such as industrials (automation, EV batteries), healthcare and utilities (renewable energy). To find EM leaders for the next decade, investors must focus on future trends.

2. Reshoring Will Spread Across Developing Countries

Is manufacturing yesterday’s story for EM countries and companies?

Over the past two decades, China cemented its role as factory to the world for countless global companies. But wages in China have risen much faster than wages in other EMs and COVID-19 exposed the risks of heavily concentrating supply chains in one country. As a result, companies are reconfiguring supply chains, and are more willing to pay up and bring manufacturing closer to home to prevent future disruptions.

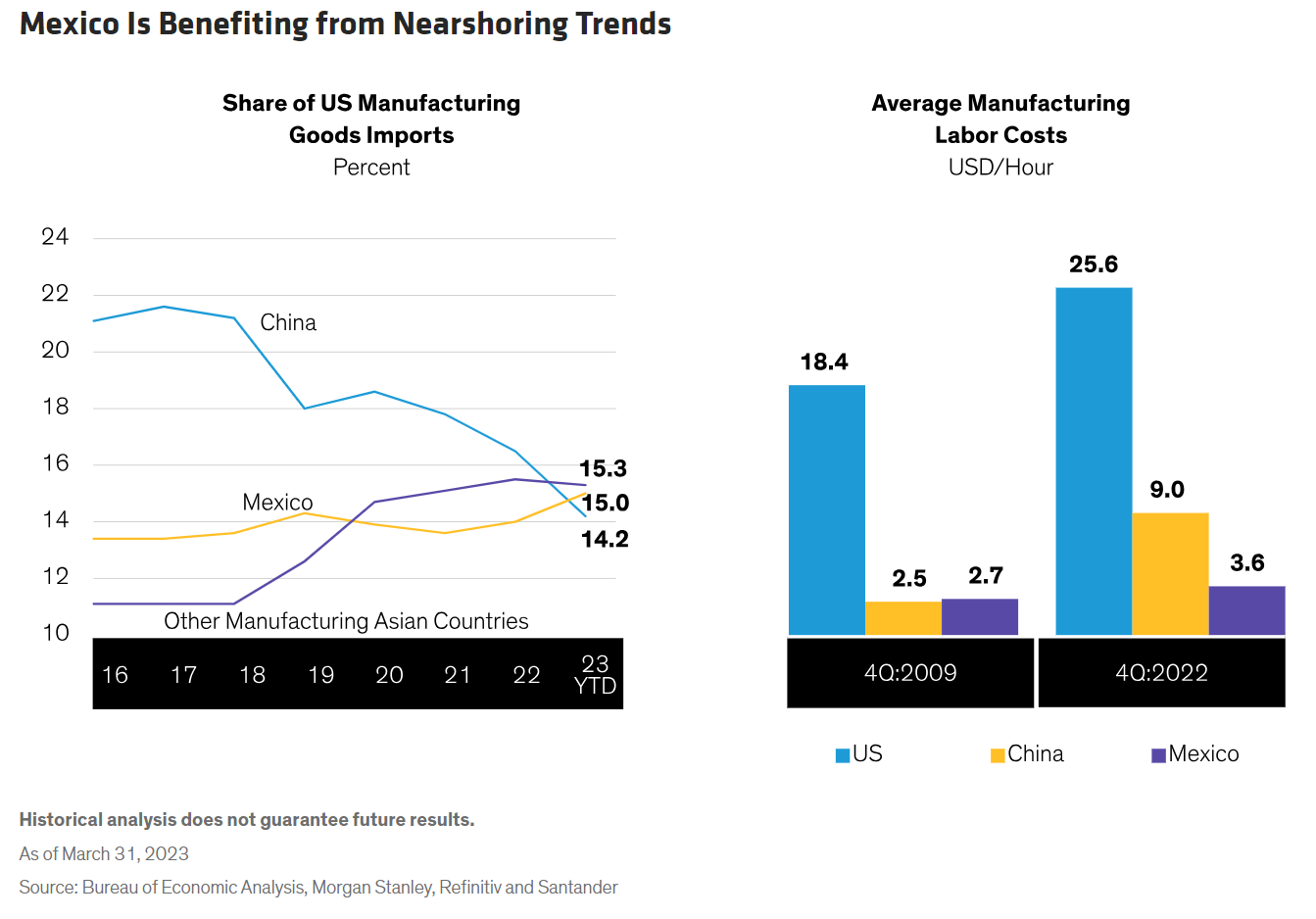

EM countries are essential to the shifting supply chain landscape, in our view. Vietnam’s educated population is rushing to fill jobs in the electronics industry, and the country’s share of electronics exports has surged nearly fivefold, to 5.7%, over the past decade, according to World Trade Organization data. Bangladesh has increased its exports of ready-made garments from US$17.9 billion in 2011 to US$42.6 billion in 2022. Mexico is grabbing the market share of vehicle assembly, particularly in EVs; the country is expected to produce more than 221,000 EVs in 2023, a 179% increase from last year, according to Directorio Automotriz’s Business Intelligence Area. Mexico’s proximity to the US and attractive labor costs have enabled it to overtake China as a key manufacturing hub for the US market (Display). As a result, capital investment in Mexico has been steadily increasing since 2021.

In India, newly crowned the world’s most populous nation, large domestic investment in infrastructure is bolstering manufacturing and attracting foreign investment. Samsung already has operations in India and continues to invest. Taiwan-based Foxconn Electronics, an Apple supplier, is planning a US$200 million facility for producing AirPods in India, marking a big vote of confidence in the country’s manufacturing capabilities.

That investment illustrates how globalization is changing. Investors who can identify the next big reshoring destinations and industries will be able to capture attractive opportunities as the map of global manufacturing is redrawn.

3. China’s Common Prosperity Policy Redefines Growth

As China’s population has become richer in recent years, the government has become more sensitive to a widening socioeconomic gap. In August 2021, President Xi Jinping said that common prosperity, “rather than being egalitarian or having only a few people prosperous,” referred to “affluence shared by everyone.” Xi seeks to increase per-capita income and to reduce inequality across income groups and regions. The agenda covers many areas, from more balanced development to boosting productivity, income and infrastructure.

As part of these efforts, China has taken regulatory action in recent years against certain industries. These moves rattled markets, and for some investors, undermined confidence in investing in China, as regulatory moves are unpredictable.

We think that’s the wrong conclusion. In our view, regulatory uncertainty can be mitigated with a better understanding of the interplay between the government and private sector in China.

Certain types of Chinese companies will benefit from the policy priorities. These include companies that can navigate the commercial and ideological priorities, and businesses aligned with the government’s agenda. Companies that cater to less-wealthy customers may also have an advantage. Instead of forgoing China’s significant return potential, we think investors should develop a strategy that aims to reduce regulatory risk and identify opportunities in a growing economy that is forecast to become the world’s largest by 2035.

4. Green Investments Will Generate Commodity Demand

Alongside common prosperity, China is also pursuing an ambitious green reform agenda. China, the world’s largest CO2 emitter, aims to reach peak carbon emissions before 2030 and is targeting carbon neutrality by 2060. India is also targeting net-zero emissions by 2070.

Achieving these ambitious goals requires massive investments in wind and solar power, EVs, smart power grids and other green technologies. Companies that enable China’s green agenda will benefit from the policy. Many of China’s green enablers are major suppliers around the world and will enjoy an impetus from the global energy transition.

Building climate resilience is, paradoxically, a commodity-intensive endeavor. Copper, nickel, cobalt, lithium and rare earths are essential ingredients in renewable energy equipment and EVs. China is a major supplier of many of these minerals, along with Chile, Argentina, Indonesia and Estonia. Commodity-producing EM countries should enjoy a boost from the energy transition.

Active Investors Can Find Advantages in EM Inefficiencies

Positioning for the potential EM comeback won’t be easy. Investors must be alert to the differences between EM equity markets and their DM peers.

Many EM stock markets are dominated by retail investors, which makes them less efficient than DM markets. Some are dominated by foreign investors, who may be quick to flee in a crisis or when the asset class is out of favor. There’s also less information available about many EM stocks than DM stocks, which makes them more prone to emotional swings.

These issues aren’t new. However, investors might have expected EM market behaviors to converge with DM’s. In fact, we’ve seen the opposite. China A onshore and Saudi Arabian markets are among the more retail-dominated in the world and are becoming a larger part of the broader EM index. As a result, EM markets in aggregate are becoming less efficient, in our view.

Inefficient markets are often illiquid. Yet EM stock markets offer an uncommon combination of liquidity and inefficiency—an attractive combination for stock pickers. When stocks are hit by a market overreaction, active investors can find opportunities in mispriced shares of companies with resilient long-term potential. We believe that EM stocks provide especially fertile ground for active managers because of the equity markets’ behavioral features and the attractive growth potential of a broad spectrum of companies.

What Will It Take to Unleash Return Potential?

EM companies should enjoy strong tailwinds for growth, in our view. Across the developing world, rising incomes, urbanization and government policies aimed at promoting economic growth leads more people into higher income employment. With more income, the middle class begins to spend on products and services that it couldn’t afford previously. Domestic reforms, manufacturing growth through reshoring and technological progress all support sustainable middle-class growth. And the socioeconomic forces that persuade people to pursue a better life are even more powerful today, in a world where easily accessible online information broadens the appeal of premium products and services.

Constraints on EM equity market performance may be starting to ease. Currency dynamics look favorable, China is reopening its economy after pandemic lockdowns and EM growth is poised to widen the gap with DM growth, after the differential narrowed in recent years. In aggregate, developing economies are almost as large as DM economies, yet EM remains underrepresented in global equity indices. The time is right for investors to revisit their EM exposures within global equity al

Sammy Suzuki is Head of Emerging Markets Equities, responsible for overseeing AB’s emerging markets equity business. He is also Co-Chief Investment Officer of Strategic Core Equities. Suzuki was a key architect of the Strategic Core platform and has managed the Emerging Markets portfolio since its inception in 2012, and the Global, International and US portfolios since 2015. He has managed portfolios for nearly two decades. From 2010 to 2012, Suzuki also held the role of director of Fundamental Value Research, where he managed 50 fundamental analysts globally. Prior to managing portfolios, he spent a decade as a research analyst. Suzuki joined AB in 1994 as a research associate, first covering the capital equipment industry, followed by the technology and global automotive industries. Before joining the firm, he was a consultant at Bain & Company. Suzuki holds both a BSE in materials engineering from the School of Engineering and Applied Science, and a BS (magna cum laude) in finance from the Wharton School at the University of Pennsylvania. He is a CFA charterholder and a member of the Board of the CFA Society New York. Location: New York

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All