Ten stocks have dominated US equity market gains for most of this year. But the rest of the market may be waking up. That’s good news for active managers who seek to tap diversified sources of long-term returns that can withstand challenging macroeconomic conditions.

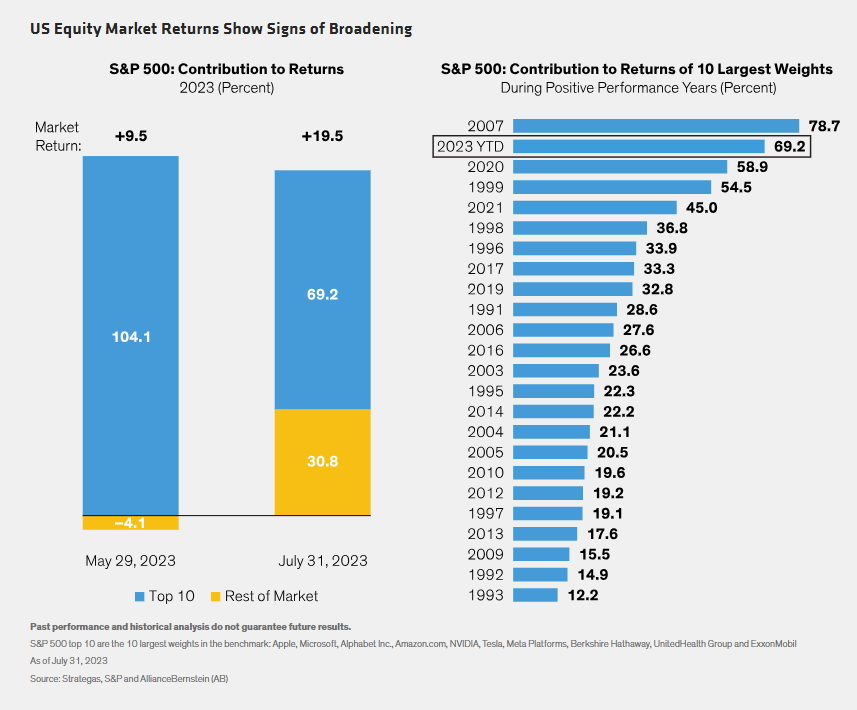

It’s been a dizzying ride for the 10 biggest stocks in the S&P 500 Index. Excitement over artificial intelligence (AI) has attracted investors to mega-cap stocks, particularly those in technology and internet-related industries. In the first five months of 2023, the 10 largest benchmark weights accounted for 104.1% of the S&P 500’s 9.5% gains (Display). At midyear, the market capitalization of Apple and Alphabet had swelled by nearly $1 trillion and $380 billion respectively since end of 2022.

Market Concentration Has Been Extreme

By the end of July, those same 10 stocks contributed 69.2% of market gains of 19.5% on the year. In other words, about 490 issuers that comprise the rest of the market accounted for nearly 31% of the market return.

Even after the recent market broadening, the concentration of returns in such a small number of stocks is extreme from historical perspective. Only in 2007 did the 10 largest stocks contribute more to market returns in a single calendar year over the last three decades.

Finding Growth Beneath the Surface

To be sure, some of the tech titans are good investments when held at appropriate weights and in line with a portfolio’s strategy. Yet investors who hold all the mega-caps at large benchmark weights will be vulnerable to a potentially painful reversal of sentiment. The technology-heavy Nasdaq acknowledged the market concentration risks when it conducted a special rebalancing of benchmark weights in July to curb the influence of the largest stocks.

In the past, episodes of acute market concentration have typically given way to periods of broader market contributions. And beneath the surface of today’s market, we believe investors can find a broad array of companies with relatively attractive valuations and solid growth potential. By tapping into diverse sources of growth, we believe portfolios can be positioned to avoid concentration risk and deliver consistent long-term returns.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein