For the savvy private wealth investor, portfolio diversity is key to success. Investing in infrastructure is one option that can help you both optimize your portfolio and make a positive and meaningful impact on your local community.

Innovative provider of custom indexes becomes a key part of a growing suite of VettaFi index solutions, which now power nearly $19 billion in ETFs and other vehicles.

In this video, Chuck Carnevale, co-founder of FAST Graphs, a.k.a. Mr. Valuation, will guide you through the analysis of consumer staple stocks.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a. Mr. Valuation will analyze the upcoming spin-off of Kellogg into two separate companies and discuss whether it is a good investment opportunity.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a. Mr. Valuation will discuss the compelling investment opportunity in Conagra Brands (CAG).

Dividend Growth Stocks for Current Income and Dividend Growth General Mills (GIS) Consumer staple stocks are blue chips that are considered some of the safest dividend growth stocks you can invest in, especially for dividend growth and dividend growth of income.

Markets are prone to cyclical behavior, which presents risks and opportunities for investors. Here are some basics investors should know about market cycles, recessions, and recoveries.

You’re nearly there! You’re nearing the age when you can finally stop working and enjoy some well-earned rest. But there are a few more steps you should take before officially retiring, which will ensure greater financial stability and peace of mind in your later years.

Dave Wysocki, Vice President of Sales at Harvest ETFs discusses why ETF liquidity is different from stock liquidity.

It’s hard to see your portfolio dip and not panic – especially as you near retirement. Coupled with record inflation, a dip might tempt you to sell your investments to drive cash flow.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs will go over 13 Blue-Chip Consumer Staple Dividend Growth Stocks – a baker’s dozen – 13 of the highest quality blue-chip dividend growth stocks on the planet, all of them in the Consumer Staples Sector.

For example, treasuries, investment grade bonds, corporate debt, and high yield to name a few. And in this case, like equities, they can be bought and sold on a stock exchange.

Over the last several years, we’ve heard plenty of talk about artificial intelligence. There’s even debate about whether AI will ever become sentient and decide to destroy humanity.

A one-time investment in Cummins of $10,000 in 2003 would have turned that $10,000 into $323,000 by August 21st. And more importantly, that $10,000 original investment would have generated $73,634 in income.

If you’re interested in investing in mutual funds or exchange-traded funds (ETFs) – or you already have some in your portfolio – you may be wondering what exactly the difference is between an active and a passive fund.

Chuck Carnevale joins me today to share how to build a profitable dividend income portfolio as well as his secret to driving dividend income with the best dividend stocks 2023 which keep his passive income 2023 flowing into his dividend portfolio.

As the demand for faster, smaller, and more efficient electronic devices grows, so does the need for advanced semiconductor manufacturing techniques. Traditional methods have their limitations, and ASML’s mission revolves around transcending these boundaries.

ETFs have become a popular investment vehicle among many investors and continue to grow in adoption, and so what we’re seeing is that more and more investors are incorporating ETFs into their own portfolios in some way or another.

Recent data and policy developments have fallen firmly in the soft-landing camp, and market performance has reflected this shift. Notwithstanding recent stronger-than-expected economic activity, we continue to believe a downturn is in the pipeline.

ETFs are investments that can hold: bonds, stocks, gold bullion and cryptocurrencies. Canadian ETFs track a wide range of different asset classes via indexes. Most ETFs are tied to index products, including both equity or fixed income funds.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a. Mr. Valuation, will be analyzing cell tower real estate investment trusts (REITs) and helping you determine if they are a good investment.

In this video, Chuck Carnevale, Co-founder of FAST Graphs provides an update on Medifast (MED). Since October 1st, 2021, Medifast has dropped over 52%, resulting in a 28% annualized loss.

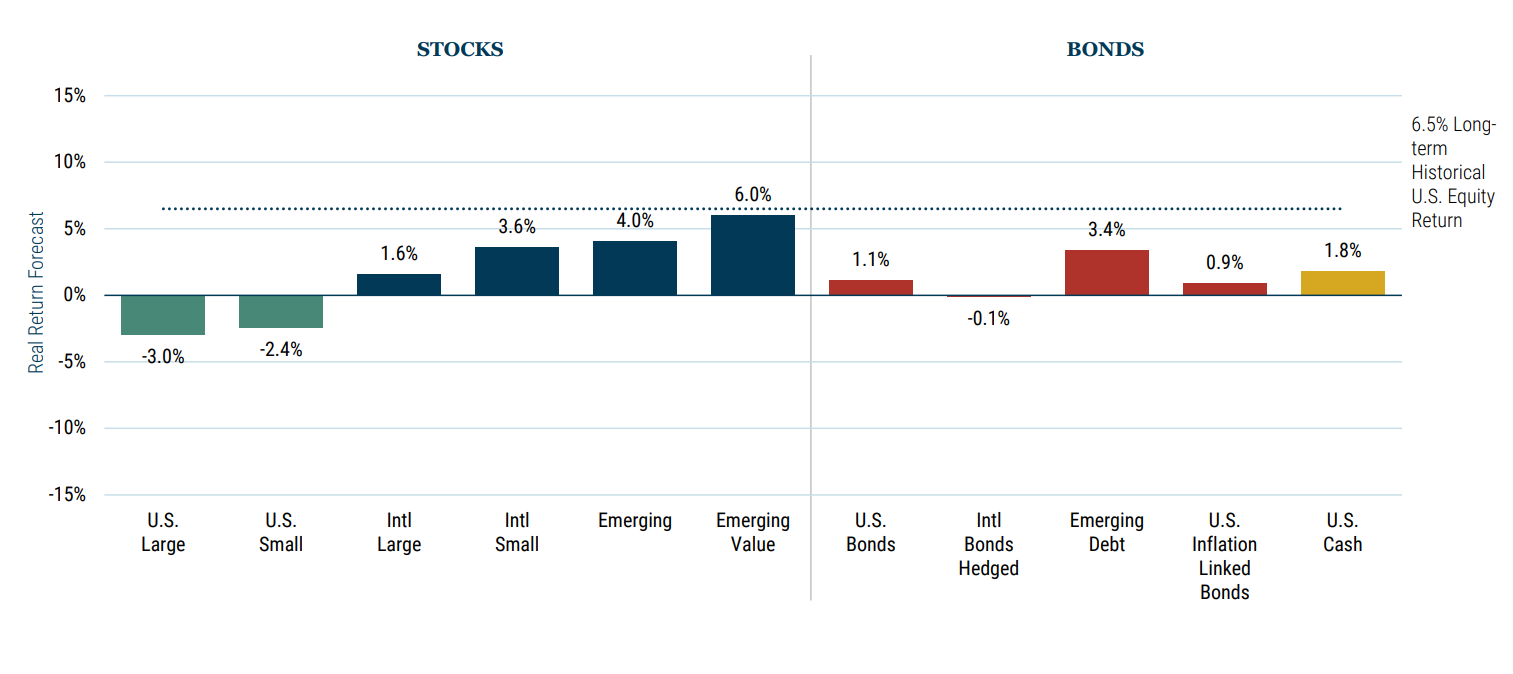

GMO 7-Year Asset Class Forecast: July 2023

Foreign stocks are again competitive with their domestic counterparts. Here are four ways to gain exposure.

It’s been an interesting first half of the year. Markets performed very well in the face of continued Fed tightening, calls for an imminent recession, a regional banking crisis, debt ceiling debate, and drama around an 11th-hour deal to avoid a default on U.S. debt.

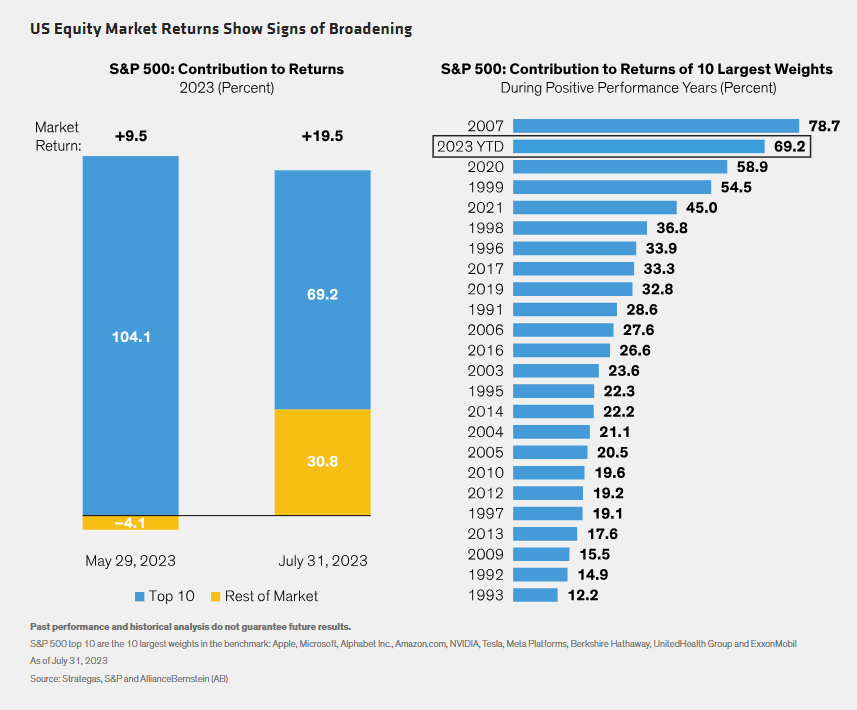

Ten stocks have dominated US equity market gains for most of this year. But the rest of the market may be waking up. That’s good news for active managers who seek to tap diversified sources of long-term returns that can withstand challenging macroeconomic conditions.

Chuck Carnevale, a.k.a. Mr. Valuation gives an update on Medical Properties Trust (MPW) in this video.

Effective tax planning means thinking about how tax rates might change.

In this video, Chuck Carnevale, Co-founder of FAST Graphs, the Fundamentals Analyzer Software Tool will analyze the performance and valuation of PayPal (PYPL) stock.

Market volatility is an inevitable part of investing. And, understandably, tumultuous times will likely trigger emotional responses to match.

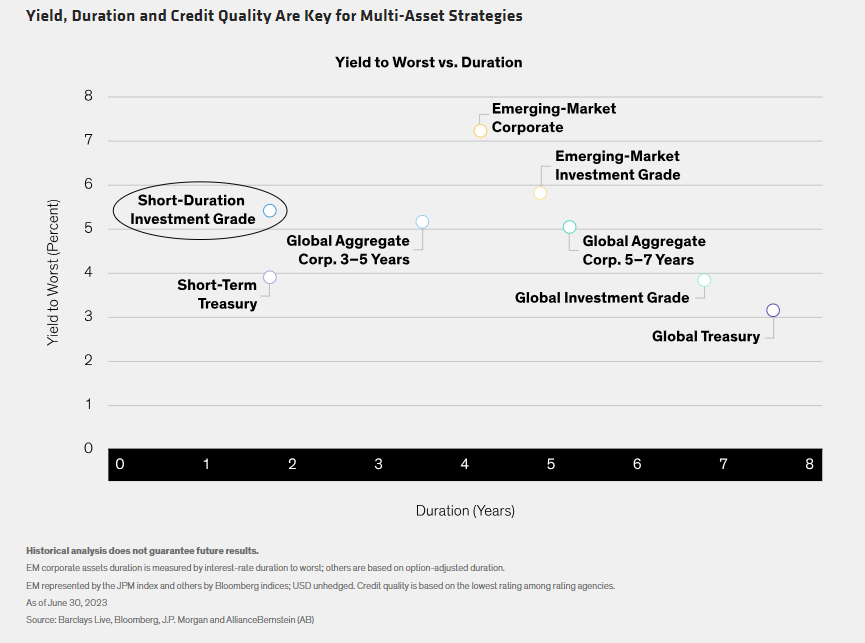

In any environment, multi-asset investors should prudently balance risks across equity, corporate credit and government bonds. But near-term tactical shifts can help take advantage of ever-evolving market conditions in the pursuit of long-term returns.

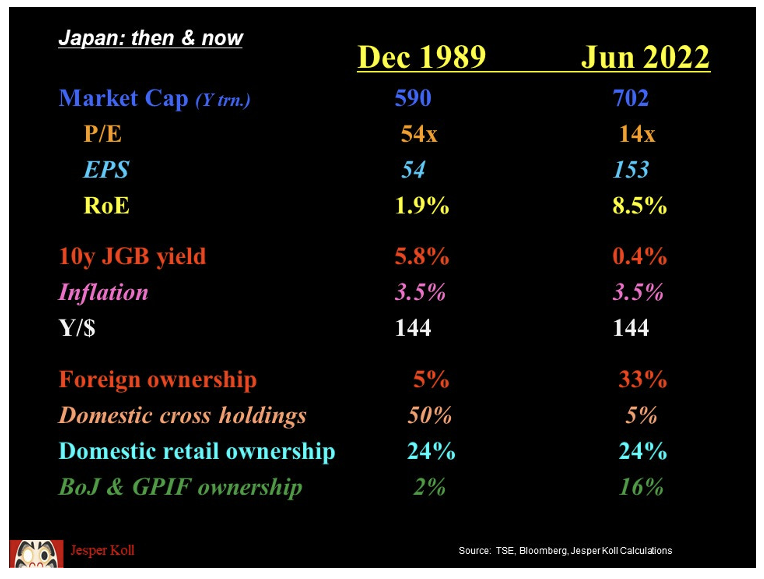

While US economic data continues to deteriorate along with much of the globe, pockets of growth have developed. We continue to be generally cautious but have expanded the portfolio to include Japan where we see opportunity today.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs, a.k.a Mr. Valuation, discusses the differences between investing in growth stocks vs. dividend growth stocks.

As that information presents itself, we may see a fair bit of market choppiness. This is why, even though the market’s monthly moves are fascinating and informative, they are far from instructive for a long-term investor.

Markets posted a strong first quarter, though it was a rollercoaster ride. The path forward will likely stay turbulent, with bank turmoil likely tightening credit conditions and the Fed still wrestling with inflation.

In this video, Chuck Carnevale, Co-Founder of FAST Graphs a.k.a Mr. Valuation will be sharing four growth stocks that he found using our FAST Graphs Premium Preset Screens in our Screening Tool.

The current environment looks favorable for equity market neutral, global macro and insurance-linked securities, according to K2 Advisors. The team offers its mid-year outlook for these and other hedge fund strategies.

After breaking its string of 10 consecutive interest rate hikes in June, the Fed elected to raise the federal funds rate by 25 bps at its July 26, 2023, FOMC meeting.

A professional advisor can craft a tailored, holistic financial plan that supports your needs, goals and intentions for the future.

In this video, Chuck Carnevale, co-founder of FAST Graphs, aka Mr. Valuation, will be sharing with you six incredibly consistent dividend growth stocks that you can invest in today.

Monetary and fiscal indicators continued to tighten significantly in the second quarter pointing towards a material slowdown in the U.S. economy.

Our emerging market debt valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive. In our Quarterly Valuation Update, we provide our Q2 assessment.

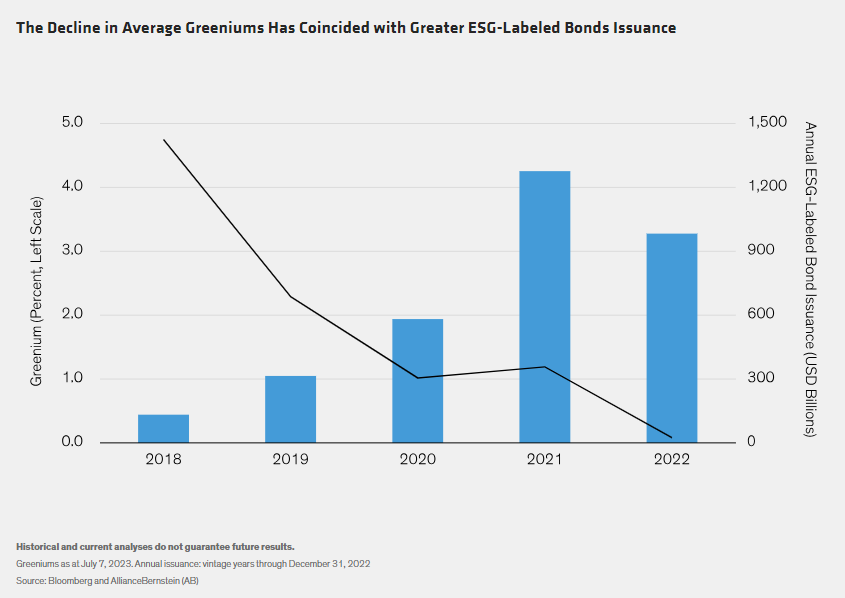

Investors in ESG-labeled bonds expect well-structured issues with strong green or social credentials to command higher prices than the same issuer’s conventional bonds.

To find the best stocks to invest in, there are more than 19,000 stocks to pick from in the US and Canadian markets alone. Consequently, how is the individual self-directed investor able to find the best stocks to meet their goals objectives, and risk tolerances?

This Knowledge Leader aims to provide solutions that can help societies overcome complex challenges. For example, NEC makes biometric identification systems, video analytics systems, and digital government solutions designed to improve the efficiency and transparency of government operations.

The stock market has got to be the weirdest market in existence. It is the only place where people go to buy things and hate it when those things go on sale.

Appealing yields and cautious markets.

Even benchmark-makers are starting to address the supersized influence of heavyweight stocks. Nasdaq’s plan to reconfigure the weights of its constituents should prompt investors to think about the broader concentration risks in US equity markets, particularly in passive portfolios.

The global economy remains in a fragile state. Headline inflation is above-target in almost all major economies, and core inflation is sticky and elevated.

In this video, I will be providing an overview of 26 top-rated companies in the field of artificial intelligence stocks.