Quarterly Letter

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Grab your coat and get your hat

Leave your worries on the doorstep

Life can be so sweet

On the sunny side of the street”

– Tony Bennett1, On the Sunny Side of the Street

Dear Client,

While US economic data continues to deteriorate along with much of the globe, pockets of growth have developed. We continue to be generally cautious but have expanded the portfolio to include Japan where we see opportunity today. More on that below, but first, a review of Q2 performance for “primary” assets.2

Risky assets were mixed in the second quarter. US equities were up 8.7% during the three-month period. Global equities were up 6.3%. Commodities lost 3.1% during the quarter. Perhaps the equity and commodity divergence is because commodities are more immediately economically sensitive; an interpretation consistent with the global economic slowdown seen across manufacturing, industrial production, and country-level gross domestic production. (Details below.)

Through the end of June, the equity market remained narrow.3 Like the first quarter, the USA MSCI Equal Weighted Index meaningfully trailed the market capitalization weighted index and returned 4.7%. The narrow breadth and its persistence are not signs of a healthy market.

Unlike the first quarter, safe-haven assets were down in the second quarter. Gold was down -2.7%. Long-dated US Treasury bonds returned -2.5%. On the one hand, this action may corroborate the equity market rally. On the other hand, it may be indicating more and longer inflation than previously expected and with that higher-for-longer short-term interest rates.

Of specific note to Grey Owl clients, Japanese equities were up 6.2% during the quarter and are up 14% year-to-date. Over the course of the last few months, we have built a position in Japanese equities on-par with our positions in both US government bonds and precious metals. (More on Japan below.)

Consistent with the defensive posture we have maintained since late 2021, the Grey Owl All-Season4 strategy was essentially flat for the period (down 0.7%).

Economic Growth

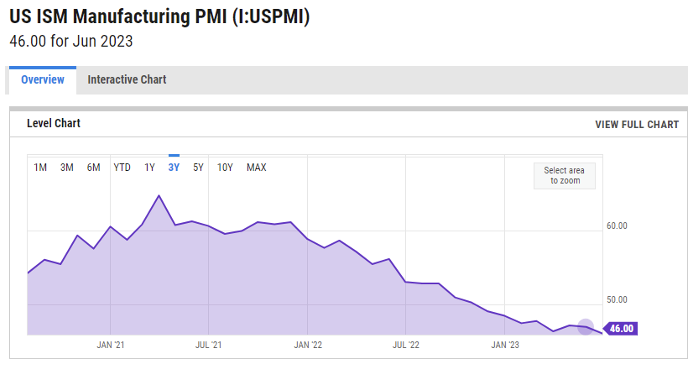

Growth continued to not just decelerate, but contract, during the second quarter as it did in the first quarter. The US ISM Manufacturing Purchasing Manager Index (PMI) summarizes in a single data point the state of the US economy. The PMI is a “diffusion index” which aggregates survey data from decision makers throughout the manufacturing economy. The questions are around the managers’ expectations (e.g. “do you plan to acquire more or less inventory next month compared to this month) and are thus a leading indicator of economic activity.

The PMI has been decelerating since March of 2021. It entered contractionary territory (below 50) in November 2022 and has continued lower and made a new low of 46.00 in June 2023.

Figure 1 – US ISM Manufacturing PMI monthly5

As bad as the PMI and Industrial Production numbers are in the US, they are worse in Europe.

Figure 2 - https://tradingeconomics.com/euro-area/manufacturing-pmi

Back to the US to further the point, Industrial Production has been slowing since early 2022. Growth just went from deceleration to contraction with the June number.

Figure 3 - https://fred.stlouisfed.org/series/INDPRO

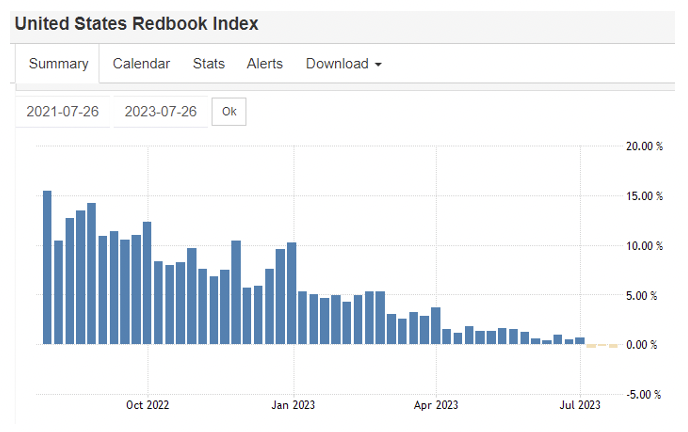

Unfortunately, this is not just a manufacturing slowdown. Retail sales have been decelerating for well over a year and are now contracting. Year-over-year sales have been negative every week in July.

Figure 4 - https://tradingeconomics.com/united-states/redbook-index

Yield Curve

The yield curve is the difference between longer-dated Treasury bonds and short-dated Treasury bonds. The 10-year yield minus the 2-year yield is a common way to view the yield curve. When the difference is negative this indicates that the bond market believes economic contraction is imminent and government-controlled short-term rates are too high.

Inverted (negative) for some time, the curve narrowed modestly following the March regional-banking “crisis” that saw Silicon Valley Bank taken into receivership by the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve provide swap-lines across the banking system attempting to ameliorate liquidity issues. The actions appear to have stopped (or postponed) a contagion (at who knows what expense). Since then, the yield curve spent most of the second quarter further inverting as the flight-to-safety trade dissipated.

Figure 3 - www.tradingview.com

The yield curve agrees with the ISM Manufacturing PMI. The US economy is headed for a recession (if not already in one). Since 1950, every time the yield curve has inverted, a recession has followed within two years. 70% of the time it occurred within a year.6 As the graph above shows, the yield curve first inverted in the middle of 2022. The inversion has become increasingly extreme as time has gone on.

Inflation

While indicators of economic growth look directionally similar (just a bit worse) to what we showed in our last few letters, the inflation outlook may be changing. Like growth, inflation had been subsiding. Since peaking in the summer of 2022, we have seen continuous disinflation to the June level of 3% year-over-year as measured by the Consumer Price Index (CPI).

However, since the beginning of May both commodity prices (orange in the chart below) and the 5-Year Breakeven Inflation Rate (blue in the chart below) have been creeping higher.

Figure 4 – www.tradingview.com

Ongoing inflation is corroborated by an indicator conceived of by David Ranson at HCWE & Company. While the spot price of gold is a useful predictor of inflation, it plays multiple roles and often acts as a safe haven investment during periods of panic. Mr. Ranson believes that the price of gold far in the future eliminates that safe haven “noise.” That “forward” price of gold has been accelerating since late 2022.

Figure 5 - www.tradingview.com

Japan

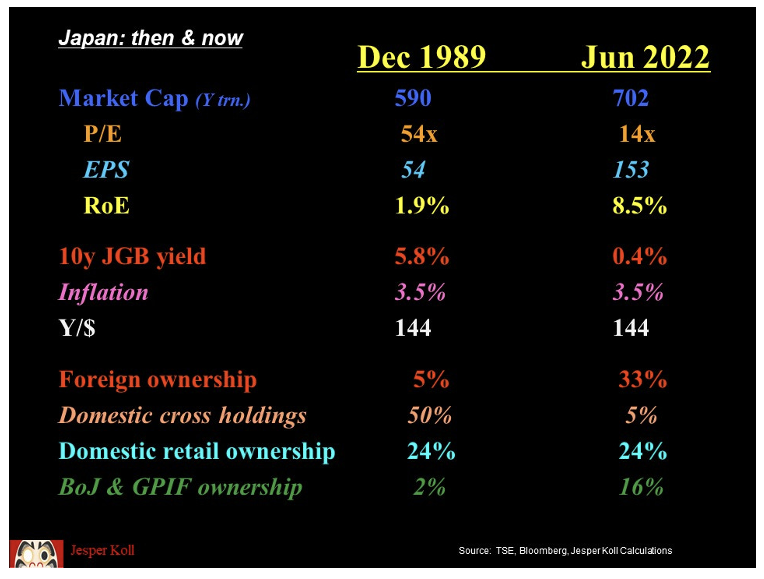

Unlike the US economy, Japan’s economy is accelerating, and valuations are modest. And, Japan’s business sector looks nothing like it did when the Japanese bubble peaked and popped in 1989. The chart below compares key Japanese metrics from 1989 and last summer (very little has changed in a year). Return on equity (investment) is up significantly, valuations are much lower (and reasonable), and incentive-perverting cross-holdings are de minimis.

Figure 6 - Japan Optimist7

While we remain cautious on US equities given the current economic environment, we are happy to invest in Japan where economic fundamentals are accelerating, valuations are reasonable, and price trends are bullish.

A Broader Portfolio

Since the end of 2021, we have positioned the Grey Owl All-Season portfolio for a risk-off environment. With some important modifications that action largely continues, as our “safe haven” positions, particularly our cash allocation, precious metals, and bonds remain large.

What is different this quarter is we believe we have found in the “land of the rising sun” the “sunny side of the street.” We now have a modest allocation to risky assets in the form of Japanese ETFs. Given our inflation outlook, we also plan to opportunistically add additional inflation-oriented securities (beyond precious metals) over the course of the current quarter.

We are acutely aware that markets will shift toward growth and risk-taking long before that becomes obvious in the reported economic data. While equity markets have rallied from oversold levels in late 2022, this move has been very concentrated in the blue-ist of the current blue-chip names. But, we must acknowledge that despite the continuing deterioration in economic data, the market has begun to broaden in the last month or so. We are actively monitoring that development and will adjust accordingly if it persists.

*****

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

Sincerely,

Grey Owl Capital Management

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is a Virginia registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

1 Rest in Peace

2 We refer to US equities, long-dated US Treasury bonds, gold, and commodities as “primary” asset classes borrowing the language of HCWE & Company. The idea is that these four assets best capture two variables that explain a significant amount of asset price movement: global growth (explained by investor risk sentiment) and inflation. This framework is the basis for a permanent portfolio, an “all-season” portfolio, risk-parity, etc. US equities and commodities are “risk” assets, while US Treasury bonds and gold are “haven” assets. The market (or asset class) returns are measured on a total return basis using index exchange traded funds (ETFs): SPY for the S&P 500, ACWI for the MSCI All-Country World Index, GSG for the S&P GSCI Commodity Index, TLT for 20+ Year Treasury Bond index (i.e. “long-dated” US Treasury bonds), and GLD for gold.

3 e must note that there are some indications the market is beginning to broaden. That would be an indication that more equity exposure is warranted. We are watching these indicators closely.

4 Despite the generic and frequent use of the term, we renamed our strategy Grey Owl All-Season after Bridgewater Associates requested we do so claiming it conflicted with a strategy they call All-Weather.

5 https://ycharts.com/indicators/us_pmi

6 ChatGPT

7 H/t to www.hedgeye.com and Andrew McDermott. https://japanoptimist.substack.com/p/japan-reality-check-7-what-has-changed

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All