Long-Horizon Investing, Part 4: Real-Life Applications in Retirement

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part three of a five-part series that develops an analytical framework for long-term, retirement-oriented investing. You can read part 1 here, part 2 here and part 3 here. The author would like to thank Joe Tomlinson and Michael Finke for their helpful comments on this article series.

The twin paradox: Another financial fable

Consider the following scenario: At the start of 2022, Bob, a healthy 65-year-old man, decides he is ready to retire. To help him manage his finances in retirement, Bob hires Rule of Thumb Investment Advisors (a.k.a., “ROT IA”). He has $1 million to invest, so ROT builds him a portfolio that is 60% stocks and 40% bonds – the classic “60/40” portfolio. Per the famous “4% rule,” ROT informs Bob that he can safely withdraw $40,000/year (4% of $1 million), adjusted annually for inflation.

A year later, compliments of unusually high inflation contributing to double-digit declines in both stocks and bonds, the value of the portfolio has declined to $796,000.1 ROT rebalances back to 60/40 and, noting the 6.5% inflation rate over the prior year, instructs Bob to withdraw $42,600 ($40k + 6.5%) the following year. At the same time, Bob’s identical twin brother Fred decides he too is ready to ride off into the sunset. By uncanny coincidence, Fred also has $796,000 available to invest. His brother convinces him to hire ROT IA as well. Following their formula, ROT builds a 60/40 portfolio and instructs Fred to withdraw $31,840 (4% of $796,000) plus inflation throughout retirement.

Here is a summary of the situation at this juncture: Bob and Fred are the same age, have the same life expectancy (or at least the same genetics), and hold the same nest egg in the same basket of investments. Yet merely because one of them retired a year earlier, his projected “safe withdrawal rate” in retirement is 34% larger ($42,600 vs. $31,840).2

Does this make any sense?

A goals-based approach to retirement investing

Retirement investing is long-term investing, both pre-retirement and in retirement. Parts 2 and 3 of this series sought to establish the following, regarding all forms of long-term investing:

- In exchange for higher expected return, stocks are always riskier, regardless of horizon.

- The risk-free alternative for a long-horizon goal is a horizon-matched Treasury/TIPS bond.3

- “Cash” (e.g., short-term Treasurys) and “bonds” (e.g., a typical short-to-intermediate-term bond portfolio) grow increasingly risky, especially on an inflation-adjusted basis, as the horizon gets longer, without a compensating increase in expected return.

We are at last prepared to contrast the traditional approach of “ROT IA” with a goals-based retirement investment strategy informed by the above principles.

Goals-based investing starts with establishing goals

This process is familiar, as most advisors already practice goals-based planning. But goals-based investing seeks to move beyond tossing financial assets into a single stock/bond pile, deriving a single “probability of success” for all the goals combined, and calling that a plan. Rather, the object is to match specific goals with designated, covarying assets. By no means does the following describe the only way to approach goals-based investing, but the specific methods illustrate how to apply the general principles.

Inflexible expenses should be matched with secure income

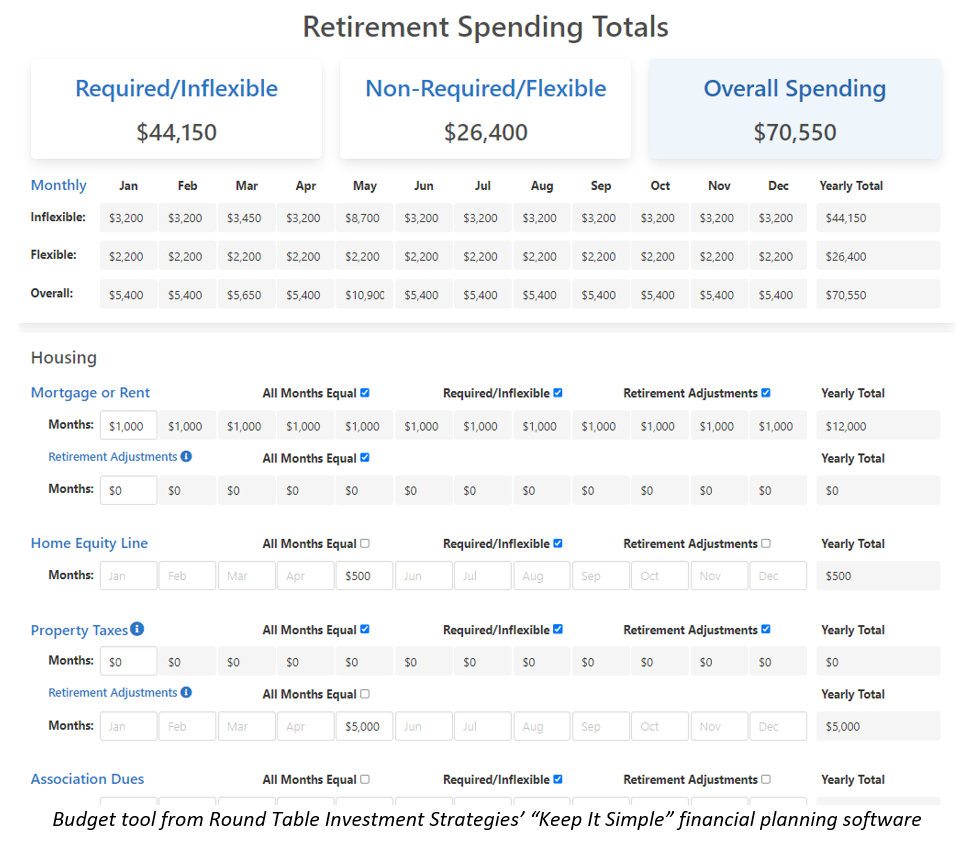

The story at the start of this article also served as the opening gambit to an ongoing blog series about retirement income. Another article in that series explored the process of establishing goals. One of the most important steps in that process is dividing planned annual expenses into “inflexible” and “flexible” spending needs. My firm even developed a web-based budgeting tool to help our clients with this process.

Inflexible expenses will often include things like property taxes, utilities, insurance premiums, and groceries. But as Michael Finke pointed out in his Advisor Perspectives webinar on goals-based planning, even a weekly golf game can be tagged as “inflexible” if a client cannot countenance the prospect of retirement with less than the expected complement of golf. (This is why I prefer the term “inflexible” to “required.”)

The first line of defense in targeting inflexible expenses is Social Security, and potentially other guaranteed income sources.4 But there are two main reasons why supplemental secure (preferably inflation-protected) income may be needed:

- Social Security may not be sufficient to cover someone’s annual budgeted inflexible expenses.

- A person may wish to retire before age 70, but for most retirees (or at least the higher earner of a retiree couple), delaying Social Security claiming to age 70 is one of the best financial decisions available. This creates the need for “bridge” income between retirement and age 70.

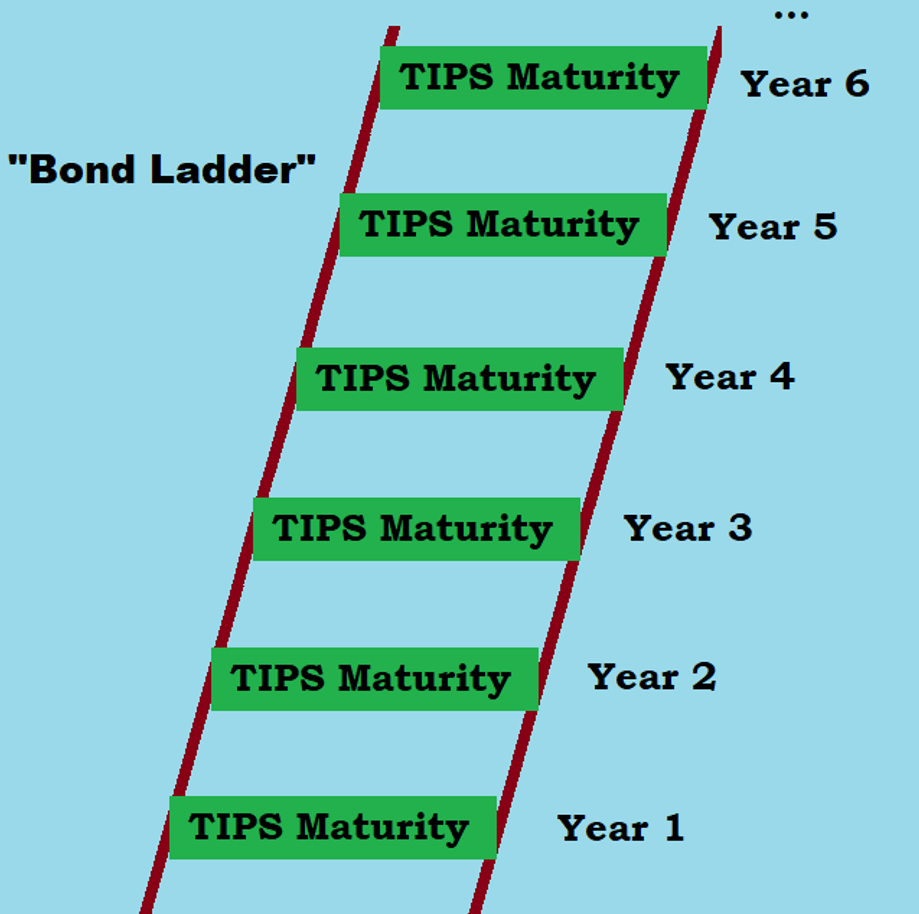

This differs from the single-point-in-time example in Part 3. Whereas I compared that example to reaching a mountaintop, a stream of real income is more like scaling a series of peaks. The straightforward solution is to decompose the series into a sequence of individual goals. The resulting risk-free solution is a “TIPS ladder” – a portfolio of inflation-protected Treasury bonds with maturities corresponding to each year’s “mountaintop.”

I wrote in detail on this topic in an earlier blog post. Notably, coupons for bonds in later years can be applied to the “rungs” for earlier years, thus simplifying a complication that arises from the nonexistence of zero-coupon TIPS. That post also outlines “duration matching” as a solution for missing TIPS maturities, or even as a potentially simpler, if imperfect, alternative for the entire ladder. I’ll return to duration matching when discussing pre-retirement investing in Part 5.5

Counterintuitive corollaries

A TIPS ladder has an analog to another counterintuitive inference from Part 3: As TIPS rates have become “more attractive” (i.e., higher) the past couple years, the dollar amount of TIPS required to meet real income goals – and thus the amount we would recommend to clients – has declined, not risen.

The flipside of that coin is that anyone who already held a TIPS ladder has seen the present dollar value of that ladder decline significantly as rates have risen. This points to one of the most important principles in goals-based investing, a restatement of what the fabled guru said in Part 3’s opening anecdote: In investing, you can have safe income or safe asset value, but not both!

One of our most important educational challenges is helping our clients understand this concept. They must learn to ignore the volatility in the (present) value of a TIPS ladder, knowing that the inflation-protected income for which the ladder is designed is secure.

Observe how wildly this differs from the typical notion of “cash” as the safe investment in retirement. As Part 3 demonstrated, cash can be extremely risky in long-term (real) income terms, just as surely as a long-term TIPS ladder can be very risky in present value terms.

This basic misconception is rampant. For example, when Vanguard designed its target-date funds, it noticed short-term TIPS have a much higher inflation correlation than long-term TIPS, so it decided to include only short-term TIPS in the funds. But insofar as target-date funds are designed to produce income throughout retirement, this is wrong! Short-term TIPS hedge only short-term inflation, but long-term real income requires a long-term inflation hedge.6 Vanguard’s mistake was measuring correlation in present value terms instead of future income terms. (By the way, Dimensional Fund Advisors’ target-date funds get this right, though like all target-date funds they lack the personalization of individualized TIPS ladders.)

What if I outlive my ladder?

A major downside to a TIPS ladder is that the “rungs” are limited by the 30-year maximum TIPS maturity. Longevity protection is another goal to be met in a goals-based plan. Here again, Social Security is the first line of defense, but as an extension of additional secure income beyond the expiration of a TIPS ladder, there exists a tool called longevity insurance, or a deferred-income annuity (DIA). Through the magic of mortality pooling, an insurer can guarantee a stream of income commencing in the future and continuing for the annuitant’s lifetime in exchange for a modest up-front payment today.

A major downside is that true inflation-adjusted annuities do not exist. I have published an article here on Advisor Perspectives calling for the (re)introduction of inflation-linked DIA/SPIA products. (As a side note, an ironic behavioral advantage of an inflation-adjusted annuity versus a TIPS ladder would be the likely lack of transparency into fluctuations in present value. A financial disadvantage would be the introduction of some degree of credit risk.)

Flexible expenses enable higher income on average

As discussed in Part 3, the risk-free asset in a goals-based paradigm is the asset that enables certain achievement of a given goal, no more and no less, for a known price up front. As discussed in Part 2, investments that carry

a risk premium (especially stocks, but also credit bonds and other securities) cannot make this promise, but they do offer the possibility, even the probability, of doing significantly better than the risk-free asset. Indeed, Part 3’s observations about cash excepted, it is reasonable to think of a TIPS ladder as the lowest expected return option – in exchange for its being the safest option – for producing inflation-protected income.

Because Social Security can often cover the lion’s share of inflexible spending needs, it is also commonly the case that a mass-affluent retiree’s TIPS ladder constitutes a mere minority of financial assets. I have no theoretical objection to an investor choosing to lock down even more of their annual budget with secure income, and some of our clients have done so. But when a retiree is willing to allow for flexibility in spending on certain budget items, a traditional stock/bond “total-return portfolio” gives them the ability to spend more (and/or grow their assets more) initially, on average, and under most scenarios in exchange for the willingness to spend less if necessary.

Sometimes I phrase this more expressively:

- If someone professes a willingness to risk spending their last 10 years of life eating cat food7 in exchange for a shot at generational wealth, I’m going to try to talk them out of it.

- But if folks are willing to risk a staycation in exchange for a decent shot at Aruba, I’m not going to try to convince them to lock in Branson instead.

Here again we see the distinction between risk capacity and risk tolerance. If someone’s risk tolerance is represented by the top bullet, I believe more restrictive risk capacity should predominate. But where risk capacity is higher (bullet 2), risk tolerance can dictate when/whether risk will be taken.

The key word though is “flexibility”!

The opening story in this article (and this blog post) illustrates the issues with pretending a risky portfolio can produce risk-free income. On the one hand, there is no way to be certain that any initial withdrawal percentage will be safe. On the other hand, the safer you choose to be, the greater the likelihood of leaving substantially more income potential on the table.

A viable solution is as follows: A TIPS ladder can be viewed as a portfolio whose value covaries with an inflexible spending liability, thereby “immunizing” the liability. Budget flexibility enables us to flip this on its head, allowing the liability to covary with the assets.

The most radical version of this is the opposite of the 4% rule, a “fixed percentage rule” that draws the same percentage of remaining assets each year. However, this may require more flexibility than most folks are willing to tolerate even in their “flexible” expenses! Plenty of middle ground exists. My firm uses a “guardrails” ruleset, which is a modified version of a system developed by Jonathan Guyton and William Klinger. However, in principle, any of the variable spending strategies analyzed by Wade Pfau in his recent article on the topic could serve this purpose.

Notably, the substantial foundation of safety built into a TIPS ladder (plus Social Security) increases the risk capacity of remaining assets. Especially for clients with sizable, guaranteed income (SS, TIPS, pensions, annuities), I may recommend that this total-return income layer be funded with a portfolio with up to 80% stocks. I won’t typically go riskier with this sub-portfolio (or “layer” as we call it), because the volatility dampening feature of bonds can help prevent a guardrails strategy’s year-to-year income from varying more wildly than most clients can stomach.8

Other goals

With the goals-based pattern now well established, the process for meeting other goals is straightforward:

Extraordinary, one-time expenses (e.g., a new car in five years, a child or grandchild’s wedding, a multi-month dream vacation) should ideally be preplanned to the extent possible. Assets can then be set aside to target those expenses. The key phrase is “set aside”: Whenever possible, extra expenses should not be sourced from portfolios designated to meet ongoing expenses. Goals-based dollars should be targeted to one goal each.

Here again, the amount of risk taken with these set-aside assets should depend primarily on the amount of flexibility in the expense. If a retiree absolutely can’t live without a new Lexus LS, a five-year Treasury may be in order. If there’s flexibility on make, model, or purchase timing, then credit bonds (maybe even stocks, if a used Camry is okay in the worst case) can be substituted.

An emergency fund is where cash and short-term bonds finally make an appearance as truly low-risk assets. I prefer to think of “emergencies” more expansively as “unplanned expenses.” These come up every year, but because their magnitude and timing are unpredictable, low volatility in present value is a desirable feature. Also, because people are typically prone to underestimating the magnitude and frequency of “unexpected” expenses, I would generally recommend that this sub-portfolio be quite sizable, even if that requires recommending clients lower their planned flexible budgetary spending.

A reverse mortgage is another helpful “buffer asset” than can create a factor of safety for extraordinary expenses. Reverse mortgages can also serve as optional substitutes in the flexible spending category, if/when variable spending rules dictate a reduction in portfolio withdrawals.

A major category of “emergency” expenses is potential long-term care needs. This type of expense seems ideally suited to an insurance-based solution. But long-term-care insurance is so expensive that we usually find clients either can’t afford it or they can afford to cover potential LTC expenses with otherwise unencumbered assets (see next paragraph). I confess that long-term care feels like the greatest unsolved challenge in the field of goals-based retirement investing.9

Assets that are not designated for specific goals have the most risk capacity of all. Again, risk tolerance may dictate otherwise, but I often suggest that these “unencumbered assets” be invested in a 100% equity portfolio, at least initially. One reason is that insofar as these will become legacy assets, it is the risk capacity of the heirs that matters, and we will see in Part 5 how “human capital” increases the risk capacity of financial assets.

Visual illustrations

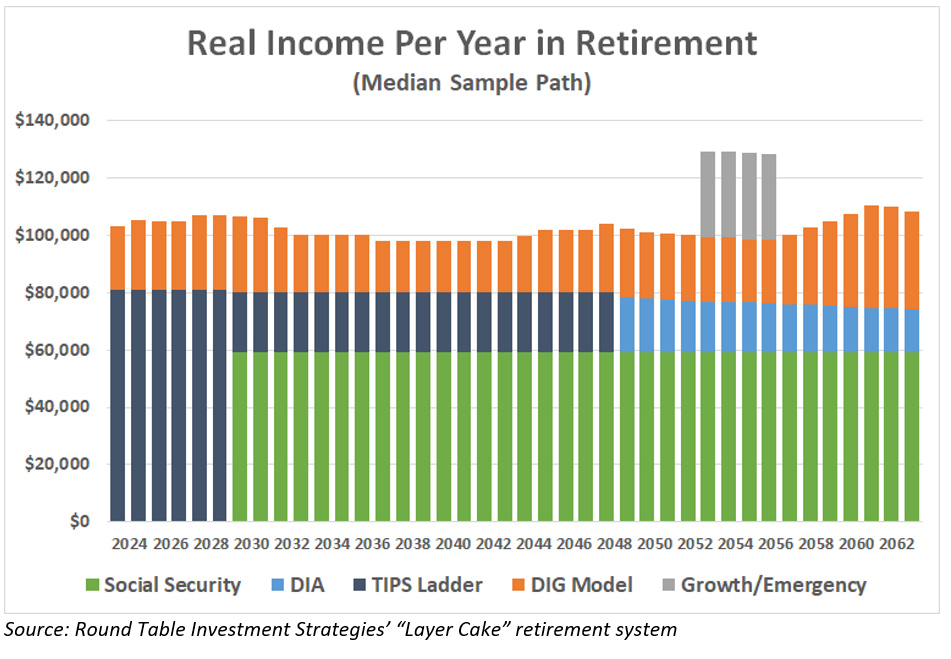

While a goals-based approach divides a retiree’s liabilities (future spending goals/needs) and assets into separate pieces with separate mandates, it can be useful to see how they all stack together. To this end, my company, Round Table Investment Strategies, created an in-house Monte Carlo model to implement our goals-based “Layer Cake” system. This enables us to build outputs like the following:

The above chart shows a “stack” of income arising from the following sources:

- Social Security: This is a 64-year-old couple who will wait to age 70 to collect maximum Social Security of about $60,000 per year, in real dollars.

- TIPS ladder: Two TIPS ladders are in use. The first produces ~$60,000/year in real income for six years as a Social Security bridge. The other produces ~$21,000/year for 25 years, to bring secure, inflation-adjusted income to ~$81,000/year, the inflexible expense figure derived from the clients’ budgeting process.

- DIA: A deferred-income annuity picks up at age 89. Using breakeven rates to estimate future inflation, we select a nominal income of $32,000/year.

- DIG model: “DIG” stands for “dynamic income and growth,” and it is the total-return guardrails system described above. The orange bars show a median Monte Carlo example of that model responding to market conditions by increasing/decreasing income as necessary. Clients must be made aware that this is just an illustrative example, and their own experience will be different, even if they get an approximately median-level outcome. Non-median outcomes will have wider variance, and these outcomes should be illustrated for clients as well, especially the possibilities to the downside.

- Growth/emergency: In this example, we illustrate four years of LTC expense, pulled from an emergency fund in this couple’s 90s.

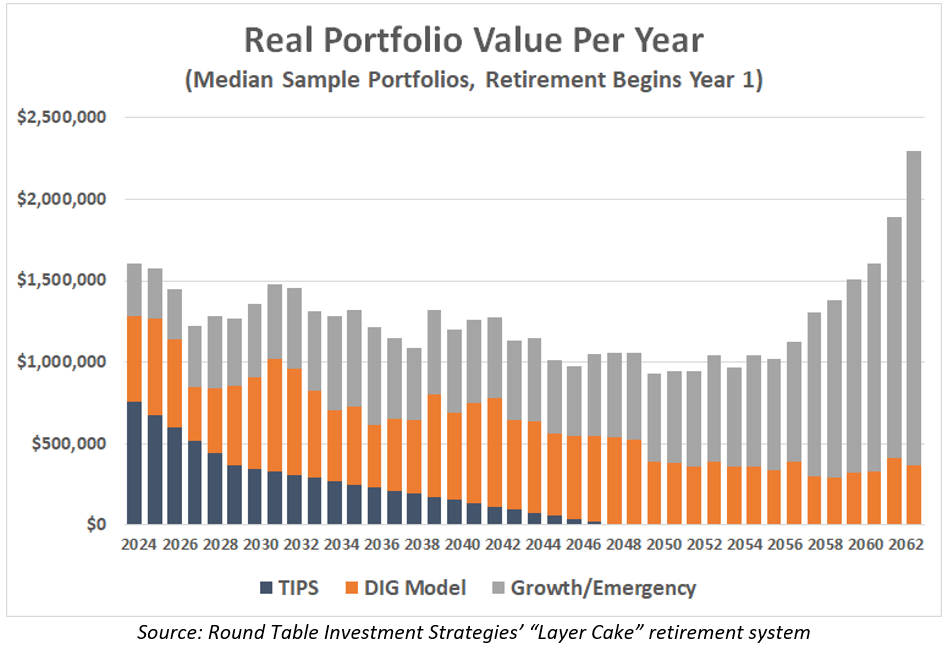

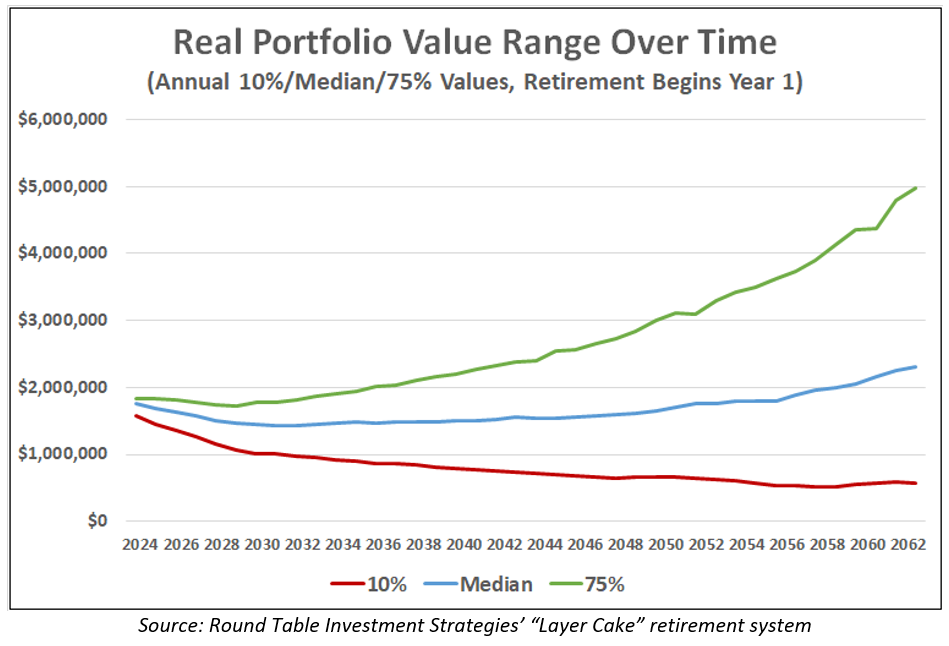

The above chart shows the evolution of each sub-portfolio. In this example, TIPS are over 45% of total assets initially, but they are consumed to zero over 25 years. The “DIG” portfolio balances income and portfolio stability in a median outcome. The non-income portfolios start as 23% of the total, but in many random trials they become the dominant element (especially the growth portfolio) as clients age, due to the equity risk premium and to the fact that the growth portfolio is not tapped for income or expenses.

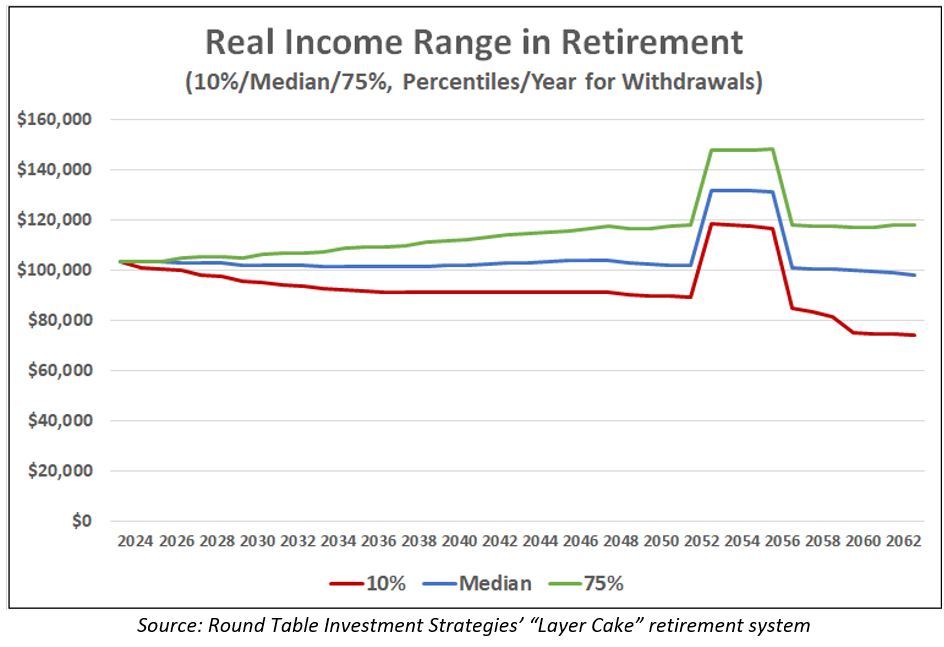

We can also illustrate “good”/ “normal”/ “bad” outcomes; for example, below are 10th, 50th, and 75th percentile outcomes for real income and portfolio totals.10 The flatlining of the red, 10% income line around year 2059 (age 100) illustrates that even a dynamic guardrails rule can eventually see a portfolio go to zero in an extended poor market scenario. (The withdrawal bump in years 30-33 is the modeled LTC expense.)

Wrapping up and moving on

After the entire design process outlined above, I often find that the total portfolio (i.e., the combination of all sub-portfolios) has a typical 50/50 or 60/40 stock/bond11 ratio. But the distinctions relative to a traditional approach are immense: The kinds of bonds used may be very different, due to the divergence between risk in present value and future-income terms. Where rebalancing occurs, it is within sub-portfolios – for reasons specific to each sub-portfolio’s strategic purpose – rather than globally across all assets. Finally, a natural consequence of this approach is that safe assets are consumed as income over time, resulting in a slowly rising equity position overall. This accords with research conducted by Michael Kitces and Wade Pfau, but without the cognitive dissonance arising from an explicitly rising-risk glidepath.

So ends our overview of goals-based investing in retirement, as informed by the earlier discoveries in this series about long-run investing and different meanings of investment risk. In Part 5, this series will conclude with an investigation of a goals-based approach to investing pre-retirement. The same long-run considerations apply (albeit at even longer horizons), but the techniques will vary somewhat, most notably due to something called “human capital.”

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Here’s the math: First, Bob took out $40,000, leaving $960,000. Using the S&P 500 Index (2022 return = -18.11%) and the Bloomberg Aggregate Bond Index (2022 return = -13.01%) for stock and bond returns, respectively, the 60/40 portfolio returns -16.07%. Assuming another 1% for ROT’s fee means -17.07% return overall. $960,000 * (1 – 17.07%) = $796,128.

2 Since both figures will be adjusted by the same inflation percentage each year, this means Bob’s income is projected to be 34% higher than Fred’s for the rest of their lives. Assuming inflation is generally positive, it also means the differential between their nominal dollar incomes will grow even wider over time. But clearly it also means Bob is at much greater risk of running out of money in retirement, so-called “safe withdrawal rate” notwithstanding. Conversely, it also means Fred is much more likely to pass away with a huge hoard of assets he could have spent.

3 Specifically a zero-coupon Treasury; refer to the nomenclature paragraph in Part 3.

4 But see this article for caveats about future income from Social Security and other “guaranteed” sources.

5 This article series has mostly sidestepped the topic of taxation, but I feel it’s important to point out that a TIPS ladder will ideally be located in an IRA. While so-called “phantom income” taxation is a more sensible policy than it is sometimes made out to be, in the early years of a long-horizon TIPS ladder, a spike in inflation could easily cause taxable income to exceed the cash flow generated by the TIPS ladder, potentially by quite a lot.

6 Here’s a contrived example for effect: Suppose next year, inflation (and with it inflation expectations) jumps to 5% and remains there for 30 years. Someone who rolls short-term TIPS will get one year of inflation protection (in excess of current ~2.5% breakeven rates); from then on, the investor will have to pay every year for the new 5% inflation expectation. Someone who instead bought a 30-year TIPS bond will get 30 years’ worth of protection against the unexpected jump in inflation. And this is just the inflation piece of the equation. Nominal income needs are also best hedged with duration-matched bonds because the price of future income is constantly changing.

7 Is cat food really that much cheaper than people food? I don’t know. Clearly we’re not talking about the premium stuff.

8 As a wonky aside, I am cognizant of Wade Pfau’s assertion that annuitized assets dominate bonds in the context of retirement income (e.g., the “shark fin” chart in the linked article). His point is well taken, and I would advise anyone studying goals-based investing to consider his logic. In the context we are presently considering, though, I believe there is a role for traditional bonds as the volatility dampener, for several reasons. First, as noted, we are now adjusting the goal to match the assets. Second, periodic rebalancing is an intrinsic aspect of variable spending strategies (including in Pfau’s research), and rebalancing is virtually impossible with annuities as the “bond-like” asset. Finally, a flexible spending model may, in poor markets and/or in the long run, result in a total asset base smaller than the remaining present value of the annuity; this means it may not be possible in all cases to draw the strategy’s specified quantity of income.

9 This doesn’t mean LTC planning is hopeless. A helpful resource is chapter 8 of Wade Pfau’s Retirement Planning Guidebook, my favorite retirement planning reference book.

10 The 10/50/75-percentile lines select the given percentage each year independently, resulting in the relatively smooth evolution pictured. I.e., these lines do not illustrate the volatile evolution of portfolio balances or the dynamic nature of DIG model income.

11 Where any annuities are included in the “bond” bucket.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All