My Dream Annuity

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The following is an open letter to the annuity industry.

You are looking for ways to expand your reach into the fee-only advisor space, and I am sympathetic. Progress has been slow, fraught as it is with product complexity and the industry’s reputation for lack of transparency and high fees. Yet annuities offer certain benefits that advisors and their clients cannot create with traditional investments.

As a member of a growing faction of goals-based investment planners, I humbly request that you bring to market a product that looks like this.

My dream annuity: Characteristics in brief

My dream annuity has the following characteristics:

- It pays a guaranteed, CPI-adjusted income stream…

…for the lifetime of the annuitant(s)…

…beginning now (SPIA) or at whatever future date we choose (DIA).

- It can be purchased without death benefit, surrender/remainder value, or other add-on that would reduce income…

…but it has a cash value or other method of eliminating conflicts of interest for fee-only advisors.

Motivation and context

Through risk pooling and mortality credits, annuity providers can offer lifetime income guarantees that retirees cannot create for themselves. This is why a deferred income annuity (DIA) is the “optional frosting” on “layer #2” of the layer cake retirement income and investment model developed by my firm, Round Table Investment Strategies.

Social Security, the bedrock of “layer #1” in the layer cake, provides a CPI-adjusted (i.e., inflation-protected) stream of income for a retiree’s lifetime. However, for many retirees, Social Security is insufficient to offset the fixed/inflexible annual expenses that they will incur throughout their golden years.

For those situations, advisors can build a TIPS ladder, crafting an inflation-protected income stream from government-guaranteed securities. This supplements Social Security’s inflation-protected income, notably without the legislative risk of future payout reductions. But it cannot supplement the longevity hedge arising from Social Security’s lifetime payouts. A TIPS ladder can only secure income for a preselected range of years, generally no longer than the 30-year maximum TIPS maturity.1

This is where the DIA comes in, providing a contractually guaranteed lifetime income stream that can pick up when the TIPS income leaves off. This effectively supplements Social Security’s longevity insurance, also without the legislative risk, albeit introducing a degree of credit risk.2 But it fails to match the inflation insurance deriving from Social Security’s CPI adjustments.

This brings us to the first element in the construction of my dream annuity:

1. My dream annuity pays a guaranteed, CPI-adjusted income stream

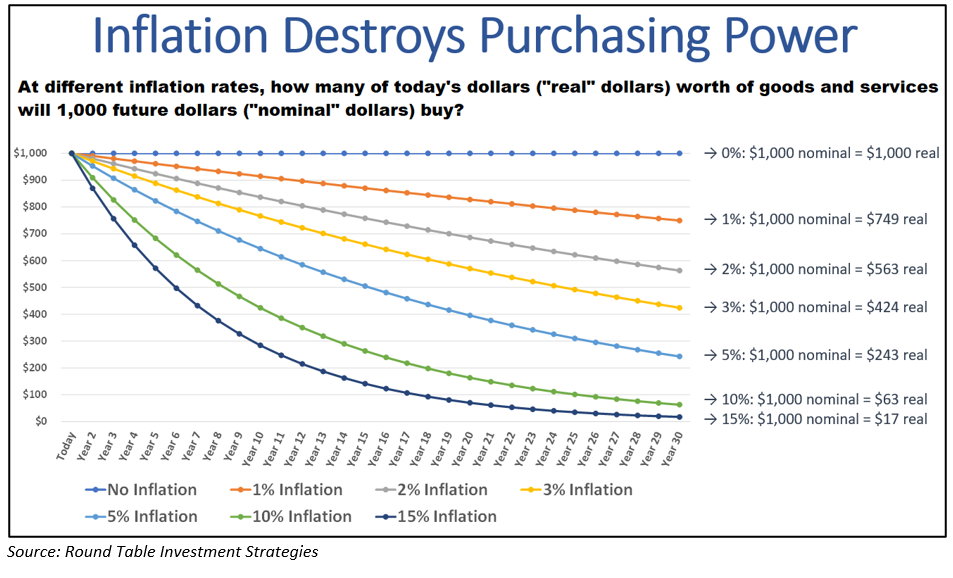

As noted above, the primary benefit to be derived from this annuity is the protection of income in the event of longevity. But the event of longevity is precisely the set of conditions under which persistent inflation has the most cumulatively devastating effect on the purchasing power of a nominal income stream.

We love the concept of secure income at Round Table. But income that does not adjust with inflation is not sufficiently secure against all contingencies.

2. My dream annuity pays out for the lifetime of the annuitant(s)

No need to belabor a point I’ve covered already. Whether single or joint life, the primary goal of my dream annuity is to provide inflation-protected lifetime income for our clients, an unpredictable subset of whom will likely live to a ripe old age – an eventuality for which no traditional investment product is a suitable liability-driven substitute.

Mortality credits are the “secret sauce” that make annuities a powerful element of a goals-based retirement plan. But the sauce lacks savor if it isn’t spiced with inflation hedging.

3. My dream annuity can begin immediately (a CPI-adjusted SPIA) or at any time we choose (a CPI-adjusted DIA)

A TIPS ladder and my dream annuity are nicely complementary. Having the ability to pay now but to choose precisely when the annuity’s income kicks off gives us the freedom to balance liquidity, custody, transparency, creditworthiness, mortality credits, and customer preference to pick the precise point in the future to have TIPS end and the annuity begin.

But there are a couple very important caveats if this is to work properly:

Caveat A: No matter how far in the future we choose to start the income, the CPI adjustments must begin as soon as we make the purchase.

Look back at that chart under characteristic #1. If a client opts for 25 years of TIPS income followed by a DIA, it simply won’t do for the first 25 years of inflation to be ignored, only to start accruing CPI adjustments in year 26.

For all practical purposes, that would put us back in the same position we’re in now, having to guess at a future inflation rate3 to pick the correct amount of future income. If we’re creating, say, $10,000/year in real income with TIPS, we should be able to buy $10,000 in real (today’s dollars) income in the DIA – at a fair price for the inflation adjustments, of course – so it seamlessly picks up where the TIPS ladder leaves off.

Caveat B: We should have the option to buy a DIA as far out as we please.

Some clients may simply choose a CPI-tracking single premium immediate annuity (SPIA) and be done with it. Others may elect to cover, say, their current life expectancy with TIPS, and buy a DIA starting then. Still others may retire at 60 or 65, lock in 25-30 years of income with TIPS, and look to purchase a CPI-tracking DIA for extended longevity insurance alone.

The last option is my most common recommendation. This is primarily because today’s DIAs aren’t inflation-linked, so they aren’t offering everything we want from them. But as Michael Kitces and Wade Pfau have demonstrated, mortality credits accrue most of their benefit when people outlive their life expectancy, and clients will sometimes prefer to maintain planning flexibility with “technical liquidity” for the years when TIPS in an IRA or brokerage account can accomplish the job.4 It is important to be able to purchase a DIA with income starting as late as age 90, or possibly even later. (This isn’t crazy! My grandmother lived to 102 and was cognitively unimpaired to the end.)

There are annuity providers who allow for this, but I’ve noticed to my chagrin that many DIAs have much younger age cutoffs for the income start date. Please don’t do that with my dream annuity!

4. My dream annuity can be purchased without death benefits, surrender/remainder value, and the like

If you feel compelled to offer these riders as optional add-ins, I understand. But that just adds the burden on us of explaining to our clients why we don’t recommend them, especially for the DIAs we just discussed.5

The goal here is to optimize the outcome based on the cost when purchasing inflation-protected lifetime income, and these goodies increase the upfront cost per unit income. Legacy and liquidity are goals we can target more effectively with other investments, including those purchased with dollars that are not spent on annuity riders.

5. Yet somehow my dream annuity has a cash value or other method of eliminating conflicts of interest for fee-only advisors

Okay, I’m going to ditch the obfuscating euphemism in this section heading: An ideal annuity is one on which a commission-free advisor can charge an AUM-based fee:

It is ideal for the advisor because, well obviously.

It is ideal for the client because it might actually get recommended by sizable swaths of the advisory profession.

It is ideal for the annuity industry for the same reason.

The annuity industry has gotten the message: Advisors increasingly understand the value of annuities, but fee-only advisors don’t want to become product salespeople just so they can make annuities work in their practice. Commission-free annuities are a good start. Annuities with a cash value they can advise on is a huge step. But the products with that feature add complexities that we and many other advisors simply aren’t interested in. Offer SPIA/DIA products – especially CPI-adjusted versions – with a fee-able cash value regardless of illiquidity and you’ll have responded to a genuine market need at last.

This is not ridiculous! Annuities have a present value after all! Find a way to make it explicit!

Okay…admittedly I don’t quite know how this would work. Perhaps the “cash value” would be based on the ever-changing actuarial value of the future income, as noted above. Perhaps it would be based on an amortization of principal. Also, if the client fires their advisor, does the fee go to the client as additional income? Perhaps the whole thing could be structured as a FIA, where the reference index is tied to CPI? We’re open to suggestions! But to unlock the enormous potential from the fee-only investment advisor profession, you need to solve this.

But look, if it isn’t possible, I’ll say this for my firm: We’re fiduciaries, we care about this concept – obviously! – and we will buy the product for our clients anyway.

No substitutes

Fixed, so-called cost-of-living adjustments (COLAs) are not a viable substitute for CPI adjustments.

A 2% COLA is a sad joke if we experience persistent 5% inflation. A 5% COLA could still fall short of even worse inflation, but more importantly, with breakeven rates under 2.5% across the Treasury curve, a 5% COLA is far too expensive relative to what a superior, CPI-adjusted guarantee should logically cost.6

Yes, persistent 5%+ inflation is unlikely. But the unlikely, multi-sigma combination of extended longevity and inflation is exactly the risk we’re trying to offset.7 And those sigmas are why it should be affordable! (Contra long-term care insurance, for example.) If we knew in advance that each of our clients would experience average longevity against a serene backdrop of 2% inflation, we wouldn’t need life annuities in the first place.

Equity-linked annuities (e.g., FIAs) are not a viable substitute for my dream annuity.

FIAs are viable products for some advisors. With their “everything in one package” convenience, they can have their uses. But not in our layer cake system, which is designed to be a sophisticated, multi-pronged, liability-driven approach to solving the retirement puzzle.

FIAs may produce superior income if we get historically average equity returns. But if we knew in advance that we would get those returns, clients wouldn’t need an annuity at all, because a total-return approach could produce even more income even while growing the asset base.8

A CPI-linked annuity is the proper goals-based investment to cover required/inflexible income needs even if stock returns are poor. I know long-run poor stock returns are improbable. But I consider a low probability of eating cat food in your 90s to be an unacceptable risk nonetheless. I still recommend risk assets after non-negotiable expenses are covered. Moreover, this approach increases risk capacity with those assets, and enables me to effectively craft a rising equity position across the total portfolio (again à la Kitces and Pfau) with minimal cognitive dissonance for our clients.

Wrap-up

Okay. I’ve said my piece. I’ve pulled no punches. My cards are on the table. I’m out of dumb clichés.

Please make this happen! Social Security has been automatically adjusting for inflation for nearly 50 years. We’ve known for a long time that CPI-adjusted lifetime guarantees are the ultimate bedrock for a secure retirement. A product that enables retirees to deepen that bedrock layer would be the ultimate gift to Americans nearing or in retirement.

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Technically, duration matching may produce a decent facsimile to the CPI target beyond 30 years, but this essentially sacrifices a degree of certainty in the earlier years to create something of benefit in the later years. And there are other reasons why it may not be worth it, including the fact that the mortality credit tradeoff looms large 30+ years into a typical investor’s retirement. However, Round Table does use the duration matching technique in our inflation-protected income model’s pre-retirement glidepath, to begin semi-securing a future stream of inflation-protected income before the target retirement date, when the final years of the projected income stream may be well beyond 30 years.

2 Pray excuse an obscure footnote wherein I lob into the luminiferous aether an impotent plea for the development of CPI-adjusting tontine annuities.

3 Or else inefficiently trying to offset any underestimate with additional long-term TIPS.

4 A possible counterargument could exist in cases where there aren’t sufficient IRA assets for us to locate the TIPS in an IRA: “Phantom income” rules, while understandable, nonetheless rather frustratingly front-load taxable income on a TIPS ladder. (Important note: This is a totally different meaning of the word “income” to what is used everywhere else in this article!) I admit I don’t know how taxation would work in my dream annuity, but if it smooths out the taxable income over time, that could be a big reason to put the TIPS/annuity boundary earlier, or even just go with the SPIA.

5 I acknowledge that an annuity surrender value or commutation can mimic the “technical liquidity” mentioned previously with TIPS, perhaps most beneficially with large-sum SPIAs or near-term DIAs. I just want the option to forgo liquidity in favor of greater payouts – an option that doesn’t even exist with TIPS!

6 Okay, I get it: The TIPS tenors that limit us to a 30-year ladder reduce your options in the “deep longevity” years as well. But on top of mortality pooling, inflation swaps and the like are another set of tools to which your finance departments have access while our clients do not.

Speaking of inflation swaps: Annuity providers’ hedging portfolios often include credit bonds to juice returns, but “credit TIPS” are not a thing. I’m ambivalent at best on this topic. The higher income is nice, but an annuity guarantee backed by a portfolio with credit risk increases the credit risk of the annuity itself (and/or the moral hazard risk of punting the products to state guaranty organizations). But since I’m not going to win that argument, I will at least note that inflation swaps can transmogrify nominal credit bonds into inflation-adjusted credit bonds…so the expected return differential between risky credit bonds and risk-free TIPS is no excuse for the year-1 income differential between nominal and inflation-linked annuities to be far greater than breakeven rates would imply.

7 To make matters worse, it seems probable to me that the most likely scenario for persistently high inflation is one in which the economic costs of fighting inflation are ultimately deemed too high to be worth it…which is likely the same scenario under which risk assets’ real returns are most likely to underperform, rendering a guaranteed real income floor that much more important!

8 Here we’ve glossed over lots of details about withdrawal rates, dynamic withdrawal rules, sequence of returns risk, etc. However, if we dug into all those details, we would still draw the same conclusion.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All