I recently traded emails with someone who is probably smarter than me. He was very interested in buying a single-premium immediate annuity (SPIA) with payments linked to inflation, which is also called a real annuity. In the finance literature, real annuities are often depicted as the perfect product/investment for a retiree.

But after obtaining some quotes and running an analysis, I concluded the idea was “nuts.” I’ll explain.

I’m not against annuities. I’m generally a fan of guaranteed income for retirees. Guaranteed income can significantly simplify the incredibly complex retirement income decision process and ensures1 a retiree always has some minimum level of lifetime income. Most retirees would be better off with more guaranteed income.

I’m all for linking annuity payments to inflation, in theory. An annuity with benefits linked to inflation has been talked about lovingly by retirement researchers for decades. It’s the Holy Grail to help mitigate retirement consumption risk.

The problem with real annuities is the inflation cost of living adjustment is super expensive relative to plain vanilla nominal annuities and those with a fixed increase (e.g., 2% per year). You can overpay for anything, and at current prices people are overpaying for inflation protection. In other words, my criticism is about market realities, not about theory. Let’s dig in.

Annuity payouts

To explore payouts for annuities, I pulled some quotes from CANNEX on April 28, 2019. The annuitant was assumed to be a 65-year-old male buying a $100,000 annuity with annual payments that begin immediately, and no period-certain or cash-refund rider. (A period-certain rider provides guaranteed benefits for a certain period, usually to between 10 and 20 years, while a refund rider pays a beneficiary the difference between the annuity premium and the sum of payments received by the annuitant.) Only about 25% of annuities quoted on CANNEX are life-only, but focusing on life-only benefits simplifies modeling.

I obtained three sets of quotes for SPIAs: a nominal annuity (where payments are constant for life); an annuity with a 2% fixed annual compound cost-of-living adjustment (or COLA, meaning the payment increases by 2% per year); and a real annuity (where benefits are linked to inflation, defined as the Consumer Price Index for All Urban Consumers, CPI-U). You can see how the payments differ for the three annuities in the charts below for each $1 of initial payments. The payments for the real annuity are based on expected inflation, but the actual future payments are obviously uncertain.

For the nominal annuity, there were 21 companies offering quotes from ranging from $6,113 to $6,643. This is a reasonably tight spread, where the best quote is only 5.73% larger than the smallest.2 Annuity payouts are also often quoted in percentage terms, which is the annual payment divided by the premium. The nominal annuity with the highest benefit ($6,643) would therefore have a payout of 6.643% ($6,643/$100,000=6.643%).

For the 2% fixed COLA annuity there were 14 companies offering quotes ranging from $4,866 to $5,168.

For the real annuity there was only one company offering a quote with a payout of $4,449. The same insurance company offering the real annuity also offered quotes at $6,244 for the nominal annuity and $5,030 for the 2% fixed COLA. Neither of these quotes was the best for the respective annuity type, but I mention it here and include the insurer in the analysis for reference purposes.

We would expect the real annuity payout to be lower than the nominal annuity payout, since the payments will increase with inflation. What is surprising is that the real annuity pays out significantly less than the best 2% fixed COLA annuity quote. The payout rate for the 2% fixed COLA annuity is 16.16% higher than the real annuity. This suggests the real annuity isn’t a good deal, but it’s worth running some numbers to quantify the exact cost.

The value of an annuity

To determine the value of an annuity, I calculated the mortality-weighted net present value for each type (nominal, 2% fixed COLA, and real). I used mortality rates from the Society of Actuaries 2012 Immediate Annuity Mortality table with improvement to 2019, discount rates based on the Treasury High Quality Market (HQM) Corporate Bond yield curve (as of March 2019), and expected inflation from the Cleveland Federal Reserve (as of April 2019).

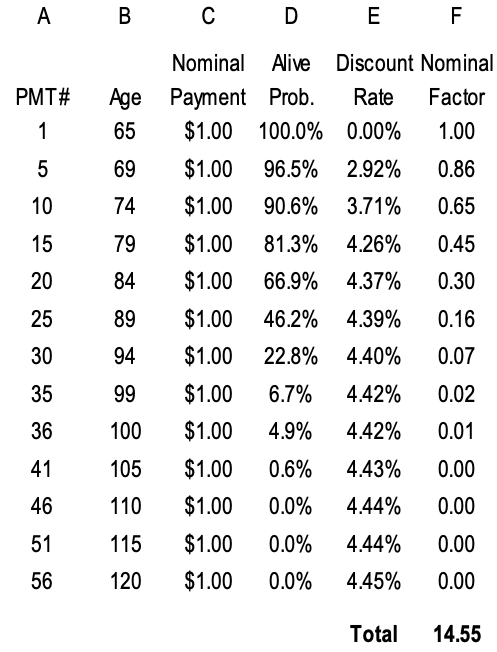

In the Exhibit below I provide an example of how the calculations work for the nominal annuity at five-year intervals.

The 20th payment, at age 84, would be $1 (column C). The payment is nominal, so it does not increase at all (i.e., it shrinks in purchasing power over time). There is a 66.9% probability that the annuitant survives to age 84 (column D). This means an insurance company would only need to set aside $0.669 for each $1 of expected payments (assuming a large pool of annuitants) for that age. Given a discount rate of 4.37% (column E), which I assume can be invested in zero coupon bonds for 19 years,3 the $0.669 payment is reduced to $0.296 when you factor in assumed investment returns. If we add up all the nominal factors (column F), to age 120, the total factor for the nominal annuity ends up at 14.55.

I performed the same calculations for the 2% fixed COLA (where the payments in column C increase by 2% per year) and the real annuity (where payments increase by cumulative expected inflation), and got total factors of 17.79 and 17.56, respectively. The 2% fixed COLA has a slightly higher factor than the real annuity because expected inflation is less than 2% until the 25th payment.

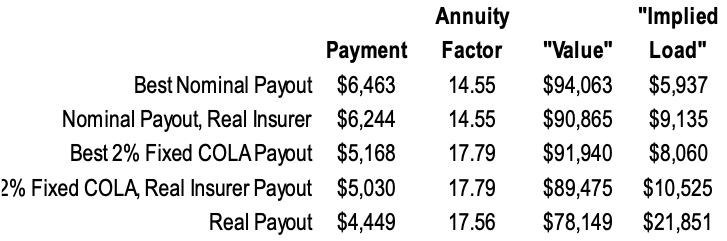

Next, I multiplied the specific annuity-type factors by the actual payouts available to estimate the expected “value” of the various annuities. The value is the expected benefit the annuitant will receive from buying the annuity (the higher the value, the better). Subtracting the value from the cost of the annuity (or the premium, which is $100,000 in this case) gives us an estimate of the “implied load” of the respective products. The implied load is the average expected loss that is being incurred by the annuitant when purchasing the annuity (the higher the cost/implied load, the worse for the annuitant). Those calculations are below.

The lowest implied load is for the best nominal annuity payout, at $5,937. As a reminder this was also the most competitively priced type of annuity, with 21 companies providing quotes. The implied load is greater for the best 2% fixed COLA annuity (at $8,060), but is still significantly less than the implied load for the real annuity (at $21,851). The implied load for the real annuity is 3.7 times that of the best nominal payout and 2.7 times the best 2% fixed COLA payout.

Other considerations

The analysis suggests that purchasing an annuity with benefits linked to inflation is incredibly expensive compared to either a nominal annuity or even one with a 2% fixed COLA payout. It’s preferable to have income that is guaranteed to rise with inflation, but the cost of doing so is significant.

Why is this? The COLA annuity costs a lot more than the nominal annuity because those inflation-linked increases are going to compound over time, and longevity causes the insurer greater uncertainty. The insurer isn’t necessarily being unfair, it’s accounting for this unique type of risk and likely responding to a lack of competition, but that doesn’t change the purchase reality for consumers.

The good news is that consumers might not need inflation protection as much as they think.

For most retirees, any annuity purchase will likely represent only a fraction of their total wealth; therefore, the marginal impact of benefits potentially declining in real terms (if inflation ends up being a big deal) won’t be catastrophic. For example, Social Security retirement benefits have a near-perfect hedge to inflation (since they are linked to it). If you want inflation-linked income (or guaranteed income in general) delaying Social Security retirement benefits is the best place to start (and probably the only thing that academics of all stripes agree). Homeownership and financial assets (like stocks and bonds) have been decent inflation hedges4, especially low-duration fixed income and Treasury Inflation-Protected Securities (TIPS).

While research commonly assumes retiree spending increases lockstep with inflation, this doesn’t track reality. Actual retiree spending is pretty noisy but it tends to decrease in today’s dollars throughout retirement based on research I’ve done. For example, if we assume base inflation is 3%, retiree spending might only rise by 2% a year, on average, throughout retirement (1% less than regular inflation). Retiree spending is also pretty flexible and retirees typically have the ability to adjust spending if need be.

Lastly, even if you’re convinced inflation is not being correctly priced in the real annuity, there are other, cheaper ways to exploit the mispricing. For example, you could buy the nominal annuity and add TIPS.

Conclusions

The higher the effective cost of any type of income guarantee, the less attractive the guarantee becomes. My analysis shows the effective cost of a real annuity today is 3.7 times the nominal annuity with the highest payout and 2.7 times an annuity with a 2% fixed COLAs with the highest payout. While a retiree would still bear inflation risk with the 2% fixed COLA, this should be an acceptable risk for the vast majority of retirees. Other assets directly or indirectly linked to inflation can fund retirement, and an annuity usually constitutes a small portion of one’s retirement income.

Therefore, while an annuity with payments linked to inflation (i.e., a real annuity) sounds highly attractive in theory, its cost is significant, and does not make sense for the vast majority of retirees.

David Blanchett, PhD, CFA, CFP® is the head of retirement research for Morningstar Investment Management LLC.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use.

1 Based on the claims paying ability of the insurance company.

2 The spread widens significantly when you look at deferred annuities and can easily exceed 20%.

3 Payments are at the beginning of the period, which is why it’s not 20 years.

4 Past performance does not guarantee future results!

More Fixed Income Topics >