The Fundamental Logic of Annuities with Lifetime Income

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The following is excerpted from Chapter 5 in Wade Pfau’s recently updated book, Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success. It is available at Amazon and other leading retailers.

Before digging deeper into different types of annuities, it is worth first focusing on how a basic life-only income annuity works and how it fits into retirement planning. A simple annuity can effectively replace bond holdings in a retirement plan that are earmarked to meet the lifetime spending goal. The question is why should a retiree hold any bonds in the portion of their asset base designed to cover ongoing retirement spending goals?

Premiums for the income annuity are invested in bonds (the insurance company adds your premium to its bond-heavy general account). The annuity then provides payments precisely matched to the length of time they are needed. Stocks provide opportunities for greater investment growth. Individual bonds can support an income for a fixed period, but they do not offer longevity protection beyond the horizon of the bond ladder created. Bond funds are volatile, exposing retirees to potential losses and sequence risk while still not providing enough upside potential to support a particularly high level of spending over a long retirement. Risk pooling with an income annuity can support a higher level of lifetime spending compared to bonds. Stocks also offer the opportunity for higher spending, but without any guarantee that stocks will outperform bonds and provide capital gains during the pivotal early years of retirement.

Income annuities can be viewed as a type of coupon bond which provides payments for an uncertain length of time in which the principal value is not repaid upon death. Another way to think about income annuities is that they provide a laddered collection of zero-coupon bonds that support retirement spending for as long as the annuitant lives. Much like a defined-benefit pension plan, income annuities provide value to their owners by pooling risks across a large grouping of individuals.

Longevity risk is one of the key risks which can be managed effectively by an income annuity. Investment and sequence risk are also alleviated through the more conservative investing and asset-liability matching approach on the part of the insurance company for the underlying assets held in the insurance company’s general account. The payout rates for an income annuity assume bond-like returns and longevity is further supported through risk pooling and mortality credits, rather than by seeking outsized stock market returns.

Longevity risk relates to not knowing how long a given individual will live. But while we do not know the longevity for any one individual, insurance company actuaries can estimate how longevity patterns will play out for a large cohort of individuals. The “special sauce” of the income annuity is that it can provide payouts linked to the average longevity of the owners because those who die early end up leaving money on the table to subsidize the payments to those who live longer. Though it may seem counterintuitive to subsidize payments to others, this act can allow all owners in the risk pool to enjoy a higher standard of living than bonds could support. All annuity owners know that the mortality credits will be waiting for them if they do end up living beyond life expectancy.

Meanwhile, sequence risk relates to the amplified impacts that investment volatility has on a retirement income plan that seeks to sustain withdrawals from a volatile investment portfolio. Even though we may expect stocks to outperform bonds, this amplified investment risk also forces conservative individuals to spend less in case their early retirement years are affected by a sequence of poor investment returns. Many retirement plans are based on Monte Carlo simulations with a high probability of success, which implicitly assumes lower investment returns. An income annuity also avoids sequence risk because the underlying assets are invested by the annuity provider, mostly into individual bonds which create income that matches the company’s obligations for covering its promised annuity payments.

In hindsight, those who experienced either shorter retirements or who benefited from retiring at a time with strong market returns would have probably preferred if they had not purchased an income annuity. Income annuities are a form of insurance. They insure against outliving assets due to some combination of a long life and poor market returns. In the same vein, someone who purchased automobile insurance might wish they had gone without if they never had an accident. But this misses the point of insurance. We use insurance to protect against low probability but costly events. In this case, an income annuity provides insurance against outliving assets and insufficient income late in retirement.

Income annuities offer an important benefit to those who do not make it long into retirement, especially for those who are particularly worried about outliving their assets. That benefit can be seen when comparing the income annuity to the alternative of basing retirement spending strictly on a systematic withdrawal strategy from an investment portfolio. To “self-annuitize,” a retiree must spend more conservatively to account for the small possibility of living to age ninety-five or beyond while also being affected by a poor sequence of market returns in early retirement. The income annuity supports a higher spending rate and standard of living than this from the outset. All income annuity owners, both the short-lived and long-lived, can enjoy a higher standard of living during their life than they would have otherwise felt comfortable with by taking equivalent amounts of distributions from their investments.

Upon entering retirement, a retiree has several options regarding allocations between stocks, bonds, and income annuities. Let us consider a simple example with four different approaches. With the basic understanding in place, we can then dig in deeper.

Bonds

Suppose a retiree wants to stretch the nest-egg over twenty years and will earn 0 percent returns by investing in bonds. We could assume higher bond returns, but that would simply complicate the math without changing the intuition behind the example. Since insurance companies also invest in bonds, higher interest rates would increase the annuity payout rate as well. With 0 percent returns, these bonds allow for spending at 5 percent of the initial portfolio balance—the sustainable spending rate—every year for twenty years. With this spend rate, bonds will leave nothing to support spending beyond year twenty.

Income annuities

Now suppose life expectancy is twenty years and longevity risk is added to the equation. Some will not make it twenty years; others will live longer. With the 0 percent returns the annuity provider earns from bonds, the provider could still support this 5 percent spending rate through risk pooling and mortality credits no matter how long the annuitant survives.

“Self-annuitization”

Now suppose the retiree “self-annuitizes” instead by managing this longevity risk without insurance. This requires picking a planning age one is unlikely to outlive. Suppose the retiree decides to plan under the assumption that retirement will last for thirty years. In this case, to spread assets out over thirty years with a 0 percent investment return, the spending rate must fall to 3.33 percent. Note as well, the spending rate could only be 2.5 percent to support expenses for forty years. In this situation, there is a direct relationship between a longer life and a lower rate of spending. Retirees are forced to spend less to the extent they worry about outliving their portfolio. In terms of an unintended legacy, if one did live for twenty years, then a third of the assets would remain with a thirty-year plan, or half of the assets would remain with a forty-year plan. Compared with an annuity, using bonds leads to a lower than possible retirement lifestyle and potentially an unintentionally large legacy, but with risk for shortfalls for an even longer than planned lifetime.

Stocks

Alternatively, one could seek an investment return higher than 0 percent by including stocks. With a fixed annual investment return of 3.1 percent, the retiree could support the 5 percent spending rate for thirty years. With a 4.2 percent investment return, spending could be supported for forty years. The question then centers around how likely it is for the portfolio to earn these higher rates of return through a stock-heavy focus.

Stocks create risk. Seeking this higher investment return requires the retiree to accept portfolio volatility with a growing allocation to stocks. Spending from investments further heightens sequence risk. A few poor returns early on could easily derail the attempt to support that 5 percent spending rate for as long as the plan targets. While it is possible to obtain the higher returns necessary to support a bigger spending level in this way, there is no guarantee that this approach will be successful. The stocks strategy provides greater upside potential for wealth to grow, but it also creates greater downside risk that the retiree will not be able to meet the spending goal throughout retirement. The range of potential outcomes widens.

The introduction of stock market risk requires two additional elements for the decision-making of our risk averse retiree. What failure probability does she comfortably and willingly accept that her portfolio will not be able to support spending through the planning age? As well, how high of stock allocation is she willing to accept, in terms of her ability to stomach the daily volatility experienced by her investment portfolio? With volatile investments and a fixed spending goal, some probability for portfolio depletion must be accepted by anyone seeking upside potential through the risk premium.

Annuitized assets do not provide upside in the sense that a legacy would be left when markets do well, but they also eliminate downside spending risk. The long-lived do receive a form of upside through mortality credits. The effective return from the annuity matches what the stocks needed to earn to support those longer retirements. For our example in which we said that stocks required a 4.2 percent return to fund a 5 percent distribution rate for 40 years, an annuity is providing this same return to an owner who happens to live this long.

“Self-annuitizing” requires lower spending, and stocks could support higher spending with upside growth, but that adds risk as well. As for bonds, ultimately, the question is this: why hold any bonds in the part of the retirement portfolio designed to meet spending obligations? The income annuity invests in bonds and provides payments precisely matched to the length of retirement, while stocks provide opportunities for greater investment growth above bonds. Bonds alone hold no advantage.

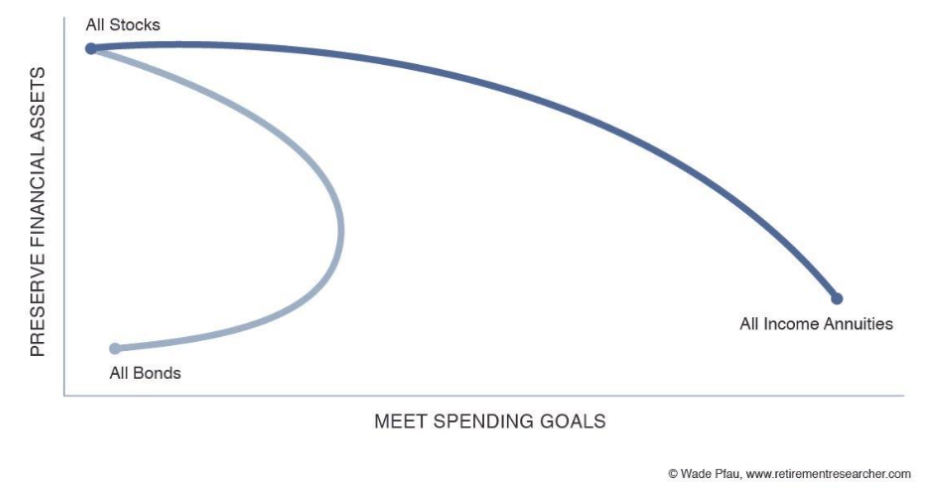

We can illustrate this with an “efficient frontier for retirement income,” which considers different combinations of stock funds, bond funds, and income annuities to best meet two competing financial objectives for retirement: satisfying spending goals for life and preserving financial assets. What I found in simulating different outcomes is that the efficient frontier generally consists of combinations of stocks and income annuities. Bond funds do not make it to the frontier, and they do not serve a useful role for meeting spending goals in the optimal retirement income portfolio. Exhibit 5.1 provides a stylized representation of the efficient frontier. Meeting more spending and preserving more assets means moving in the upper-right hand direction, and the shark-fin shape of the frontier shows how combinations of stocks and income annuities beat combinations of stocks and bonds.

Exhibit 5.1

Retirement Income Efficient Frontier

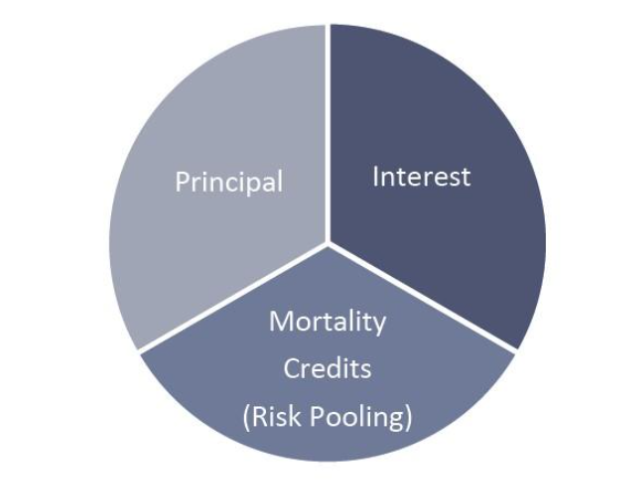

The income annuity provides a license to spend more from the start of retirement due to the insurance company’s ability to pool risk. Supported spending from an income annuity is higher because it is based on reaching life expectancy, and should the retiree live beyond life expectancy, the higher income continues to be sustained because of the subsidies arriving from those who died early. The expectation that subsidies will arrive as needed allows spending to increase for everyone from the very start of retirement. Exhibit 5.2 highlights how mortality credits represent a third source of spending with an income annuity beyond the spenddown of principal and the interest generated by that principal.

Regarding sequence risk, for those who “self-annuitize,” there are two options for deciding how to spend from investments. One is to spend at the same rate as the annuity with the hope of either dying before running out of money, or the hope that the investments earn strong enough returns to sustain the higher spending rate indefinitely. This approach requires acceptance of the possibility that the standard of living may need to be cut later in retirement should the hopes for sustained investment growth not pan out. The alternative is to spend less early on and, should good market returns materialize, increase spending later or leave a bigger legacy. The problem with intending to increase spending over time is that it is the reverse of what most people generally wish to do, which is to spend more in early retirement and cut back as life slows down at more advanced ages.

Exhibit 5.2

Sources of Income Annuity Payouts

Wade D. Pfau, Ph.D., CFA, RICP is a founder of Retirement Income Style Awareness, LLC. He is also a principal and director at McLean Asset Management and RetirementResearcher.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All