Long-Horizon Investing, Part 3: The Riskiness of "Low-Risk" Assets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This is part three of a five-part series that develops an analytical framework for long-term, retirement-oriented investing. You can read part 1 here and part 2 here. The author would like to thank Joe Tomlinson and Michael Finke for their helpful comments on this article series.

Climbing to the mountaintop: A financial fable

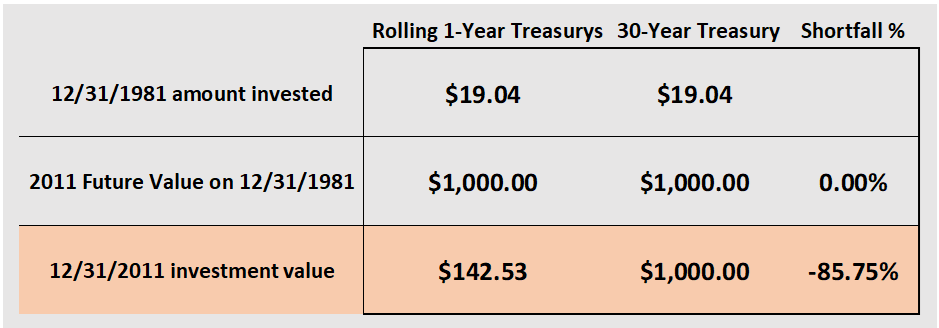

Once upon a time, a solitary figure kept a 1981 New Year’s resolution by ascending a high peak to meet a sage financial guru. “Oh guru,” said he, “in 30 years’ time, I will require exactly $1,000 for reasons conveniently private and personal for the preservation of plausible verisimilitude.”

“Very well,” the sage replied, “I see my St. Bernard has fetched my Wall Street Journal; let me check something… Ah yes, the 30-year Treasury rate this day, conveniently stripped of coupons for the preservation of narrative simplicity, is 13.65%.1 My abacus informs me that you may thus ensure $1,000 in 30 years by purchasing $19.04 of such bonds today.”2

“But master,” moaned the man, “Have I not heard that 30-year Treasurys are highly volatile, as risky as stocks but without the expected return premium? Is there not some way for me to invest more safely?”

The weary guru sighed. “I see you have some learning. But for all your knowledge, you lack wisdom. Still, I have learned through experience the hopelessness of keeping such as you invested in the long-run risk-free asset by ignoring the intermediate swings. Therefore, I merely admit that yes, you may choose to hold short-term Treasurys instead. As you so fervently desire, the dollar amount of your account will never go down.”

“Wondrous, thank you, my sage!” As the man began his descent to speak with his broker, the guru muttered under his breath, “Do not thank me for leading you astray. You have brought this upon yourself through a false definition of risk.”

The man faithfully rolled one-year Treasurys every year from then on. Each year the balance in his account grew larger, as the master had promised it would. But as the calendar rolled over to January 2011, he discovered the following, to his chagrin:

“Surely the sage financial guru has led me astray!” came man’s plaintive wail. “How shall I accomplish my private and personal goal? Is there not some way I could have guaranteed $1,000 today without ever losing money in the meantime?”

Came the reply from the disembodied voice of the guru from the mysterious beyond: “In investing, you can have safe present value OR safe future value, but not both!”3

Climbing to the mountaintop: Think forward, reason back

Standard forms of risk/return analysis are generally divorced from specific goals. As such, they tend to measure absolute return against absolute risk, which could be stated as “make as much money as possible with whatever risk you can stomach.” In this framework, the primary variable in optimal portfolio construction is “risk tolerance” (e.g., as measured through survey responses).

A more true-to-life methodology is goals-based. At some point in the future, an investor wishes to have the money to do something or a combination of somethings: Produce a stream of retirement income, buy a new car, provide for medical expenses, leave a legacy, etc. Each of those goals has an appraisable future value (i.e., the price tag – typically inflation-adjusted – that will be required to meet the goal when the time comes). And in this framework, the primary variable in optimal portfolio construction is “risk capacity,” wherein the more vital or less flexible is any specific goal, the less risk should be taken in achieving it.

In this view, realizing a goal is a bit like reaching a mountain peak. You know the height of the peak in advance, and you have a choice: The risk-free option is an investment that guarantees to get you to the mountaintop – no more, no less – for a predetermined price. With the same dollar amount in risky assets (at least those with a risk premium, see below), you will exceed the peak4 on average and in most cases, but you also risk falling short.

In Parts 4 and 5 of this series, we will consider real-life examples, most notably a stream of income in retirement. In this article, for simplicity, we will consider single-point goals like the “$1,000 in 30 years” example above. Also, although real (i.e., inflation-adjusted) buying power is typically a more realistic measure, we will begin by analyzing nominal goals, because more historical data is available.

Before moving on, a quick word on nomenclature: I will use the terms “risk-free security,” “horizon-matched Treasury,” and just “Treasury” (where unambiguous) interchangeably below. What I intend in all cases is a zero-coupon, government-guaranteed promise to return a prespecified (nominal or real) dollar amount on a specific future date. With nominal Treasurys, the analogous instrument is a STRIPS bond. Unfortunately, TIPS STRIPS do not exist, though thankfully TIPS coupon rates, and the reinvestment risk they bring, are relatively small. We’ll also see in Part 4 how the complexities of real-life goals ameliorate this coupon problem somewhat.

You won’t believe how risky “low risk” securities can be!

A typical approach in analyzing historical data for portfolio optimization insights is to compare the historical risk and return of stocks to that of a cash proxy or a short-to-intermediate-term bond index over various time horizons. This is, for example, the approach taken in the chapter of Jeremy Siegel’s book Stocks for the Long Run that I discussed in Part 2. It is also the approach taken by David Blanchett, Michael Finke, and Wade Pfau in their 2013 analysis, “Optimal Portfolios for the Long Run.”

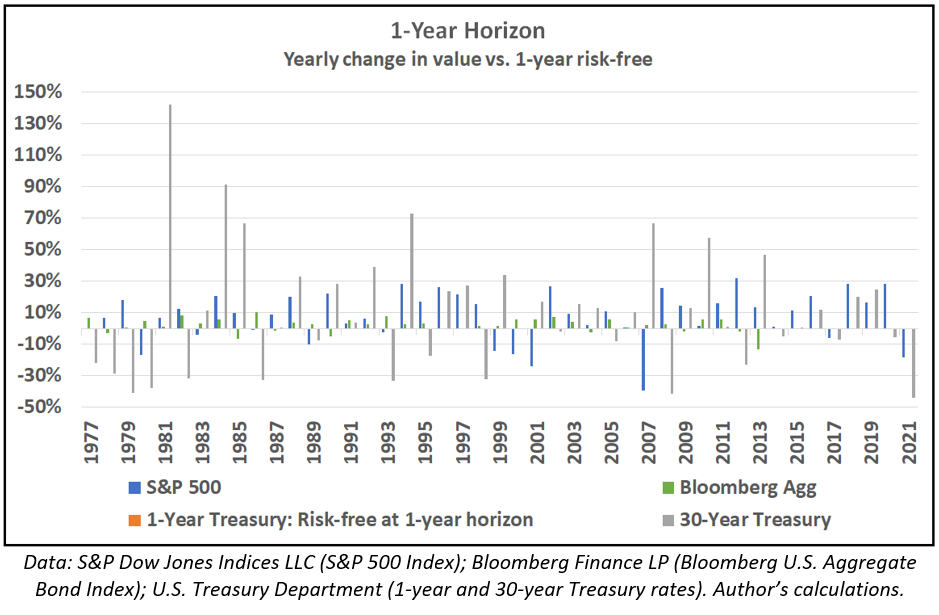

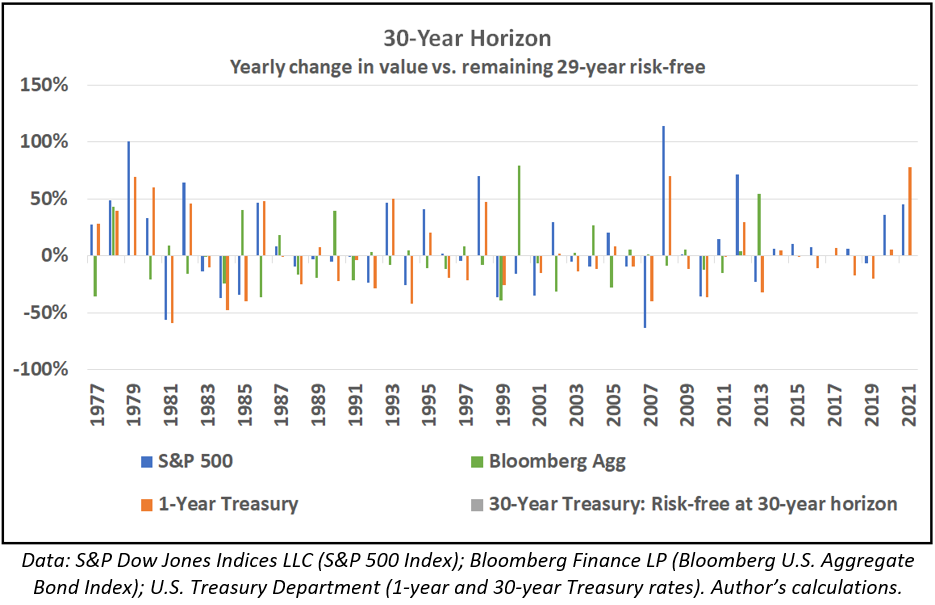

But there is a truly risk-free security for each timeframe.5 It is a horizon-matched Treasury, as defined above. This may sound like a minor technical point, but it is far from it. To see why, consider the following charts, which show, for each historical year, the return of “stocks” (the S&P 500 Index) and “bonds” (the Bloomberg Aggregate Bond Index) versus one- and 30-year Treasurys denominated in terms of a one-year or a 30-year horizon-matched future value. For avoidance of doubt, the same single-year returns are measured in both charts; only the numeraire – the basis of measurement – changes from present dollars to future dollars.

This is a confusing concept, so some elucidation may be in order:

In the one-year case, the first step is to calculate how many dollars are required to guarantee, say, $1,000 in one year, at the one-year Treasury rate. If the one-year rate is, say, 5%,6 then the amount is $1,000/(1 + 5%) = $952.38. You would place $952.38 in each of the four investments and record how they perform over the next year. The “present value” return is calculated as the amount to which each investment has grown divided by $1,000. By re-running this one-year experiment each year, you can determine how volatile each investment has been in one-year forward terms (which I call “present value” above and below, though “one-year future value” might be better). The one-year Treasury has zero volatility in these terms since it is guaranteed in advance to mature at $1,000. This is why there are no visible orange bars in the first chart below.

In the 30-year case, the first step is to calculate how many dollars are required to guarantee $1,000 in 30 years, at the 30-year Treasury rate. If the 30-year rate is 5%, then the amount is $1,000/(1 + 5%)^30 = $231.38. You would place $231.38 in each of the four investments and record how they perform over the next year. Next, project each investment’s year-end value forward 29 years using the (now) 29-year bond’s interest rate.7 (You can think of this as if you were to run a one-year adventure with each investment, then convert all four to the 29-year bond.) The “future value” return is calculated as this value divided by $1,000. By re-running this one-year experiment each year, you can determine how volatile each investment has been in 30-year forward terms. The 30-year Treasury has zero volatility in these terms since it is guaranteed in advance to mature at $1,000. This is why there are no visible grey bars in the second chart below.

But the orange bars (one-year Treasurys) in the second chart are quite volatile. On a one-year horizon, a one-year Treasury is the risk-free asset and 30-year Treasurys are more volatile than stocks. But as the horizon increases, short-term bonds grow increasingly volatile when denominated in terms of the future goal. When the horizon is 30 years, “cash” is nearly as risky as stocks – standard deviation of future value in the latter chart above is 38% for stocks vs. 34% for T-bills – but whereas stocks have a substantial expected risk premium, T-bills typically have, if anything, a lower expected return than the horizon-matched risk-free asset!8 The bond index fares little better, its annualized volatility exploding to 29% when measured against a 30-year future value numeraire.

(This again is an insight I first learned from my favorite business school professor: Nobel laureate Bob Merton. I highly recommend a quick read of the sidebar titled “The Real Meaning of Risk in Retirement” in Prof. Merton’s Harvard Business Review article, “The Crisis in Retirement Planning.”)

In extremis, this duration mismatch can produce the scenario in our opening anecdote: Supposedly safe cash producing a 30-year return 86% shy of what could have been obtained risk-free! Or, inverting for maximum effect, an outcome requiring an additional 600% growth just to reach a mountaintop that could have been summited without risk!

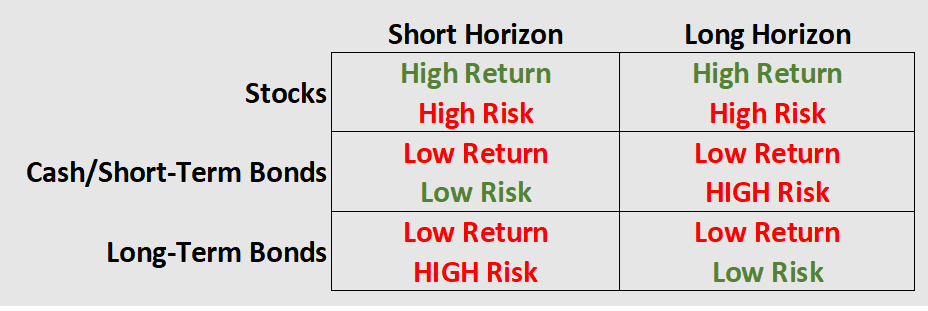

Qualitatively, we can diagram these results as follows:

The proper choice between high-risk/high-return (stocks at all horizons) and low-risk/low-return (short bonds at short horizons, long bonds at long horizons) will depend on risk capacity/risk tolerance. But at least qualitatively, high-risk/high-return (stocks) will dominate high-risk/low-return (short bonds at long horizons, long bonds at short horizons).

In principle, this observation alone could account for the increasing attractiveness with increasing horizon of “stocks” versus “bonds” discovered, for example, by Blanchett/Finke/Pfau. Granted, it neither obviates nor contradicts equity mean reversion as an additional contributing factor. But whereas the “tail risk” arguments from Part 2 of this series lent caution to assuming mean reversion will always produce superior long-run outcomes for stocks, this duration-mismatch argument is an evergreen characteristic of fixed income.

This important observation will be missed by models employing standard Monte Carlo techniques, drawing as they do from a stationary process. I.e., a randomizer with a static mean will miss an effect that emanates from the time-varying mean derived from the evolution of interest rates.

Proper risk mitigation requires proper risk measurement

In conducting historical analyses of long-horizon risk and return, the usual approach is to measure riskiness by measuring the volatility (or downside semi-deviation, etc.) of independent or overlapping multi-period returns at different horizons, much as I did in Part 2. For something like stocks, which are high-risk/high-return at all horizons, this may work just fine.

For 20- or 30-year Treasurys, though, this measurement methodology gives a very wrong impression. The ex-post volatility of separate multi-period returns for long-term Treasurys is quite high, reflecting shifting long-term interest rates over time. But it would be a huge mistake to apply these measurements to ex-ante volatility expectations for a single long-term period starting today. In fact, the ex-ante volatility is zero. The nominal (for standard Treasurys) or real (for TIPS9) return is guaranteed up front, and the dollars required to lock in a future dollar amount (or future buying power) can be calculated precisely today. That is the meaning of risk-free!

This leads to a counterintuitive conclusion: It is very common in financial articles to see questions like, “With rates higher, are bonds now attractive?” The implication is that the higher the interest rate, the more fixed income exposure an investor will want. In the context of “risky bonds” in a “risk portfolio,” perhaps this makes some sense. (Or perhaps not, if you believe as I do that expected stock return is best estimated as a risk premium above the return available from less risky securities, whatever that may be.10)

But in the context of securing a vital goal with non-risky assets, this reasoning is precisely backwards. The higher the interest rate, the fewer risk-free assets are required to meet your non-negotiable goals, and vice versa.11 This is a good example of why I prefer a goals-based approach to determining an investor’s risk capacity, and why I prefer risk capacity, so ascertained, over “risk tolerance” as the ground-level determinant of optimal portfolio design. (See the final footnote in Part 1 of this series for more detail on tolerance versus capacity.)

Let’s get real

As noted above, most goals are better stated in inflation-adjusted terms. But because TIPS made their first appearance fewer than 30 years ago, we can’t use real rates to do as much historical analysis. Nonetheless, there are some conspicuous examples in the historical record.

For instance, suppose an investor with a 30-year goal held “cash” (e.g., short-term Treasurys) as the “low-risk” portion of her portfolio as of 12/31/2010. Two years later, this would have grown by 2.5% in inflation-adjusted present-value terms. But a big drop in long-term real rates means her cash value would have fallen by about 34% in real future value terms12– i.e., the metric relevant to the goal!13

This also provides us with a response to an objection canny readers may have raised to this article’s opening anecdote: With one-year nominal Treasury rates now just above 5%, the events of 1981-2011 (i.e., a 1,400-basis-point decline in short-term interest rates) cannot repeat. To date, the 0% lower bound on Treasury rates has proven impermeable, and a -9% rate is unimaginable.

Unfortunately, we have no such assurances with real rates, which can and have dropped significantly into negative territory. To make matters worse, it is probable that the most likely scenario for more severely negative real rates is one in which the economic costs of fighting persistently high inflation are ultimately deemed too severe to be worth it…which is likely the same scenario (perhaps a prolonged banking crisis?) under which risk assets’ real returns are most likely to underperform, rendering the proper choice of risk-free asset that much more important!

Granted, this scenario is unlikely. But that very improbability makes the risk inexpensive to hedge, as demonstrated by the sub-2.5% breakeven inflation rates observed across the Treasury curve at present.

Importantly, even if/when TIPS rates go negative, they still represent the risk-free real rate of return! A horizon-matched TIPS rate, even if negative, is the rate at which you can guarantee a future inflation-adjusted dollar amount. (Albeit by putting down more than that dollar amount today; note that the inflation adjustments imply that the nominal dollar amount will likely still grow over time.) Any investment with a higher expected return will carry the risk of an even less favorable real return over any horizon.

An MPT-analogous framework

The basic tenets of modern portfolio theory (e.g., Markowitz’s mean-variance optimization and Sharpe’s CAPM) were constructed with respect to a single-period analysis.14 The period in question is generally assumed to be short, and as such, a short-term Treasury typically plays the role of the risk-free asset.

But over varying period lengths, the above analysis suggests the following framework:

The “risk asset portfolio” consists of an “efficient frontier” combination of both stocks and bonds. (And whatever else, but let’s keep things simple.) But the optimal combination of stocks and bonds will vary with the horizon. In particular, insofar as a typical (e.g., total market) bond portfolio has a relatively low duration, stocks will comprise an increasingly large portion of the efficient portfolio as the horizon grows long. This accords with the results of Siegel, Blanchett/Finke/Pfau, etc.15

As the horizon grows, the allocation to bonds, especially bonds with an expected credit premium, will decrease as a percentage of the portfolio, due to the increasing riskiness of duration-mismatched fixed income described above, but it will not necessarily disappear. This is analogous to the declining weight in an MVO framework of a non-correlated asset if you increase the asset’s expected volatility.

The risk-free asset also varies with the time horizon, as it is always a horizon-matched Treasury. Again, this asset is truly risk-free, even though the risk-free rate will change over time as interest rates change, just as occurs in a standard MPT framework. In CAPM terminology, the “Sharpe ratio” of this asset would be undefined, with a numerator of 0% (i.e., the risk-free rate minus the risk-free rate) over a denominator of 0% (no volatility in future-value terms), just as with the special case of the short-term risk-free rate in traditional CAPM. The choice of where on the resulting capital market line an investor should be situated – i.e., the preferred combination of the risk-free asset and the horizon-matched risk-efficient tangency portfolio of stocks and bonds – would then be dictated by risk capacity (preferably as ascertained by a goals-based analysis) and risk tolerance.

Wrapping up and moving on

Having completed our “toy model” exploration, we are finally ready to consider long-run investing toward real-life goals, both in retirement (portfolio optimization and withdrawal techniques to achieve goals with varying levels of flexibility) and pre-retirement (compiling assets to support a future retirement). These will be the topics of Parts 4 and 5, respectively.

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Data from the St. Louis Fed’s FRED website: https://fred.stlouisfed.org/series/DGS30.

2 See footnote 5 for methodology.

3 I-Bonds are arguably a partial exception because they are not market-traded, as I described in this article: https://rtinvestments.com/insights-blog/are-i-bonds-fabled-free-lunch/

4 “Exceed the peak”? So, like, walking on thin air? Okay, it’s an imperfect analogy…

5 At least for any timeframe up to the 30-year maximum Treasury bond maturity.

6 This discussion assumes APY interest rates (i.e., annual compounding), but “constant maturity Treasury” (CMT) rates assume semiannual compounding, and thus require conversion to APY values using the formula outlined on this U.S. Treasury webpage.

7 In the absence of 29-year CMT rates, I use the new year’s 30-year rate as a proxy.

8 Fun side note: In the “horrible” year of 2022, stocks went up in long-horizon future value terms!

9 Again, this is only entirely true for theoretical zero-coupon TIPS, since coupons introduce a modicum of reinvestment risk.

10 This argument holds even if the equity risk premium itself is time-varying (e.g., per mean reversion arguments), except perhaps insofar as there may be a nonzero correlation between risk-free rates and the equity risk premium. An example of the latter could be a “flight to quality” causing a systematic increase in the equity premium and decrease in the risk-free rate. But 2022 exemplifies the reality that such negative correlation is not as systematic as one may wish to believe.

11 Wonky footnote: This observation is related to yet another mind-bending concept, which readers will be astonished to discover I first learned from Bob Merton: Because most investors’ financial assets (e.g., their bond portfolios) are of shorter duration than their liabilities (e.g., income needs throughout retirement), they have a “negative duration” profile. This means most investors benefit from an increase in interest rates – the exact opposite of what they think has occurred when they see their portfolio balances decline! (Granted, if stocks go down too, the relationship is less straightforward. However, see footnote 8.)

12 Again, calculations use the 30-year real rate as a proxy for the 28-year real rate on 12/31/2012. Calculations also adjust for CPI evolution over those two years.

13 Granted, the opposite can happen, as last year exemplifies. Volatility is always bidirectional. The question is whether such risk is worth taking, and the answer is surely “no” when there is no expected risk premium for taking it. Admittedly, there probably is an inflation risk premium for holding nominal Treasurys, but it is very small. We don't know exactly how breakeven rates decompose into expected inflation and risk premia, but given that breakevens are presently less than 2.5% across the curve, it's hard to imagine the risk premium being more than, maybe, 0.5% (i.e., expected inflation <2%).

14 Bob Merton (who else?!) was the first to observe, in his Intertemporal CAPM paper, that multi-period considerations in the presence of many market participants with different goals on different horizons – and thus different definitions of risk – add significant complexity to questions of asset pricing and portfolio optimization.

15 The efficient portfolio may also vary based on risk tolerance, as also observed in Blanchett/Finke/Pfau, perhaps especially in the region where the capital market line is above and to the right of the tangency portfolio, i.e., where levering at the risk-free rate may prove difficult. This observation will become relevant when we discuss the role of human capital in a pre-retirement portfolio in Part 5 of this series.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All