A Framework for Assessing Variable Spending Strategies

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits This is part one of a two-part series.

This is part one of a two-part series.

Being flexible with spending matters. My analysis shows that variable spending strategies – including floor-and-ceiling, guardrail, actuarial and other methods – can dramatically increase sustainable retirement spending.

In this article, I provide the background and history behind variable spending strategies, followed by a framework for evaluating the effectiveness of those strategies. I then use that framework to evaluate a well-known strategy – constant inflation-adjusted spending. In part two, which will appear next week, I evaluate a series of other strategies.

In 1994, William Bengen introduced the concept of the 4% rule for retirement withdrawals. He defined the sustainable spending rate as the percentage of initial retirement portfolio that can be withdrawn after adjusting for inflation in subsequent years. Using U.S. historical data, he found that a retirement portfolio will not deplete for at least 30 years with an allocation of at least 50% to stocks. Bengen’s rule adjusts spending annually for inflation and maintains constant inflation-adjusted spending until the portfolio depletes. Spending does not respond to the investment performance of the portfolio, other than facing the necessity that spending falls to zero if the portfolio depletes.

While this assumption may reflect the preferences of many retirees to smooth their spending as much as possible, retirees will inevitably adjust their spending over time in response to the performance of their portfolio. Retirees will not generally play an implied game of chicken by keeping their real spending constant as their portfolios plummet toward zero.

Constant spending from a volatile portfolio amplifies sequence-of-return risk. But that can be partially alleviated by reducing spending when the portfolio value drops. Reducing spending in the event of a market decline provides a release valve for sequence-of-return risk that can allow the initial withdrawal rate to increase. This is because the current withdrawal rate does not have to be increased by as much when the portfolio loses value, allowing for less assets to be sold at a loss and more to remain available in the investment portfolio to benefit from any subsequent market recovery. Reducing sequence-of-return risk in this manner develops synergies, making it possible to spend at a higher average level than a constant inflation-adjusted strategy without any flexibility, while maintaining the same overall risk of portfolio depletion.

Traditional safety-first advocates would argue that the Bengen strategy is inherently flawed – those seeking constant spending should use a less volatile retirement portfolio, and those who accept portfolio volatility should also accept spending volatility. Without the flexibility to adjust spending, a more conservative spending rate is the primary risk management technique for a total-return investment portfolio. This spending lever may lead to an unnecessarily low lifestyle in retirement, and it is also not an efficient solution to sustaining spending. With spending flexibility, the initial withdrawal rate can increase by more than one might think by decreasing sequence risk. Spending estimates obtained with a constant inflation-adjusted assumption may be overly conservative for those willing and able to adjust their spending later.

While a constant inflation-adjusted spending strategy provides a useful benchmark and baseline for analyzing sustainable retirement-spending strategies, it should not be viewed as realistic or reasonable. Efficient retirement strategies must adjust spending somewhat for portfolio volatility. The question is how and when to make those spending adjustments.

Before exploring this, we need to consider how to evaluate strategies that allow spending to vary over time. The initial withdrawal rate is insufficient, since a built-in allowance for spending declines allows the initial withdrawal rate to increase. The probability of success does not work, since with some strategies that only spend a percentage of what’s left, it becomes impossible to deplete the portfolio, even if spending amounts do fall very low.

Rather, we should investigate how spending and the remaining portfolio balance evolve over time in both good and bad market environments. To make comparisons between different strategies meaningful, we also need to consider each with the same underlying return assumptions, and we need to calibrate the amount of downside risk taken by each strategy.

As an alternative to failure rates, I suggest calibrating the downside risk across strategies with a customized “PAY” rule. For a PAY rule, a retiree accepts a P% probability that the remaining portfolio balance falls below a threshold amount of $A (in inflation-adjusted terms) by year Y of retirement (Probability, Amount, Year). The probability of success is just one type of PAY rule in which the $A amount is $0. A generalized PAY rule is a way to compare strategies while otherwise dealing with the reality that higher initial spending rates can be justified if spending is subsequently allowed to drop more steeply. It provides a controlled anchor for those spending drops by calibrating the accepted degree of portfolio depletion. When it is combined with consistent market assumptions and a view of the entire distribution of outcomes, we can compare different variable strategies on an equal footing.

Retirees need to decide on the parameters for the PAY rule to calibrate the accepted level of downside risk. A more conservative retiree would choose a lower probability for P% to avoid the bad outcome, a higher threshold for $A to preserve more wealth as a safety margin, and a longer retirement horizon for Y to be less likely to outlive the assets in the plan. These three variables are chosen jointly, leading to an overall level of risk for the spending plan. If each parameter is chosen to be extra cautious, the overall degree of plan conservativeness will be extremely high, with the implication that retirement spending must be less. Factors to consider in choosing parameters for the PAY rule include flexibility to reduce spending, desires for spending to keep pace with inflation, fear of outliving the planning horizon, legacy goals, and the availability of other reserve assets or insurance for spending shocks.

Many proprietary variable spending strategies are needlessly complicated. I want to bring clarity to the discussion by identifying key levers at work within different proposed strategies and then compare them under the same capital-market assumptions, calibrated to have the same downside risk. The goal is to determine the variable spending strategy feels right for each situation.

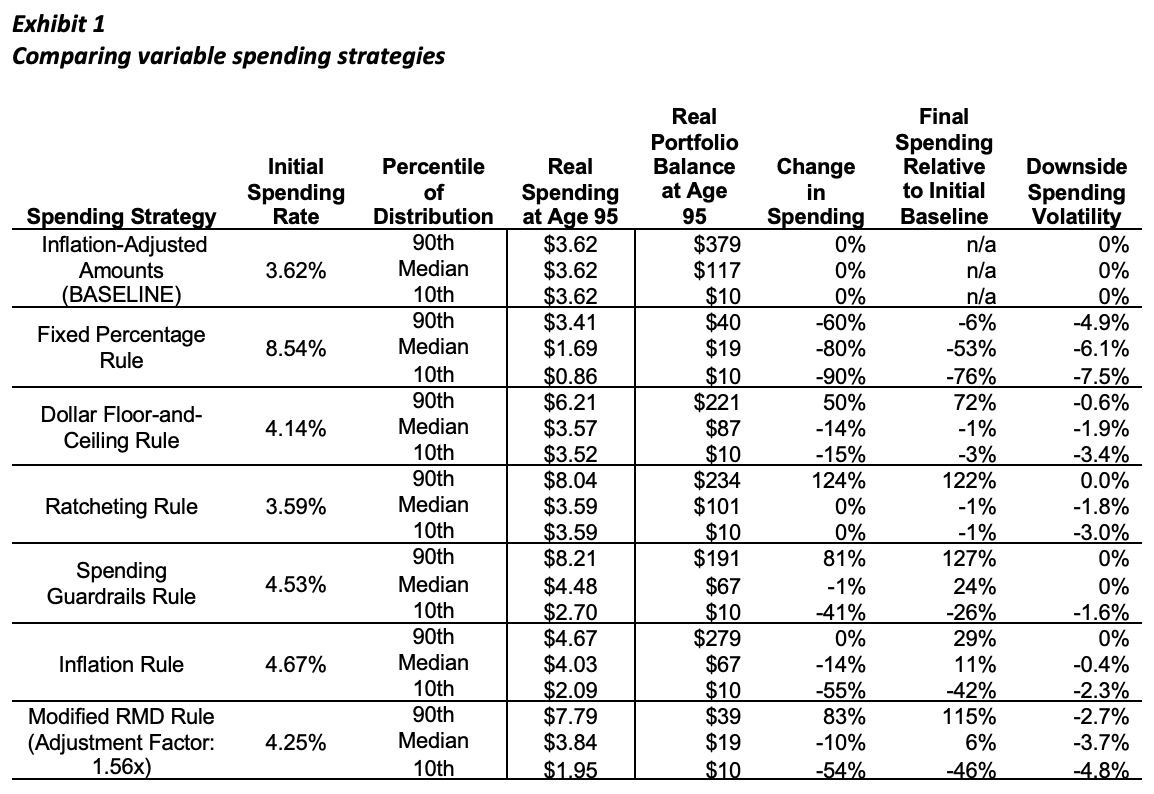

When comparing different spending strategies, there are several useful metrics. We evaluate the overall distribution of spending, the direction of spending over retirement, and the degree of spending volatility. Retirees will surely wish to consider the implications for spending and wealth when markets do well versus poorly. To demonstrate the range of possibilities, outcomes for spending and remaining wealth will be shown for the 90th percentile (markets do well), median or 50th percentile (the midrange outcome in which half can expect to do better and half worse), and the 10th percentile (markets do poorly). Exhibit 1 summarizes these comparisons for different strategies using a PAY rule in which a 62-year-old couple accepts a 10% probability that their portfolio balance falls below $10 in inflation-adjusted terms (based on an initial $100) by the end of age 95 (after 34 years of retirement).

For each strategy, the initial spending rate is shown, with the assumption that retirement wealth is equal to $100. These numbers are all scalable; you can multiply the assumed $100 initial wealth by the factor needed to obtain actual wealth to know the implications for spending and remaining wealth from a different starting point. For instance, spending $4 annually from wealth of $100 is the same as spending $40,000 from wealth of $1,000,000.

I simulated strategies with annual data, assuming withdrawals are made at the start of each year, and used annual rebalancing to restore the targeted asset allocation of 50% stocks and 50% bonds. I used 1.75% as the representative real interest rate, 2.5% as the long-term inflation rate, and 4.29% as the average nominal return for long-term U.S. government bonds. For stocks, I added a 6% risk premium to long-term government bonds to reflect the average arithmetic stock return, along with a 20% standard deviation. That is an arithmetic mean of 10.29%. I did not apply volatility to the bond returns, creating an implicit assumption that individual bonds are being held to maturity rather than in bond funds. This is a simplification, since because bonds might need to be sold as part of rebalancing. The tax implications for different spending strategies are not considered.

Returning to the discussion of spending strategies, I already described the constant inflation-adjusted spending strategy. Exhibit 1 shows that with these capital market assumptions and the assumed PAY rule, the initial spending rate is 3.62%. Incidentally, if we modify the PAY rule to allow for full portfolio depletion instead of preserving 10% of funds, the withdrawal rate is 3.83%. Advantages of this strategy include that it provides smooth and consistent income if wealth remains. One’s budget is more predictable, especially when account balances remain strong. Spending does not change and there is no downside spending volatility. As well, this strategy performs well at preserving assets for legacy. Since it does not include a means for increasing spending beyond inflation, it preserves the highest levels of remaining assets at the median and 90th percentile, while the 10th percentile was calibrated to be the same for each strategy. Even at the median, the real portfolio balance has grown after 34 years of retirement.

But it suffers from several disadvantages, primarily the retiree’s vulnerability to wealth depletion. Spending remains consistent until wealth hits zero. Though not shown in the exhibit, the historical failure rate measure for this strategy has been 7%. There will be cases with significant downside spending volatility. If the retiree has insufficient income sources outside the investment portfolio, this will have devastating implications. As noted, this strategy also uniquely increases sequence-of-return risk by calling for constant real spending from a volatile investment portfolio.

The constant real spending strategy is extremely inefficient. If market performance is better than whatever would be considered a “worst-case” scenario when a spending rate is chosen, spending will fall well below what would be feasible and sustainable. It effectively offers retirees the least amount of spending among any of these strategies. Wealth will continue to grow unabated as the current spending rate drops (a constant real spending amount from an increasing portfolio means a lower subsequent spending rate).

Next week, in part two of this series, I will examine the remaining strategies in exhibit 1 and offer my thoughts on the overall value of flexible spending rules in the context of retirement planning.

Wade D. Pfau, PhD, CFA, RICP® is a co-founder of the Retirement Income Style Awareness tool, the founder of Retirement Researcher, and a co-host of the Retire with Style podcast. He also serves as a principal and the director of retirement research for McLean Asset Management. He also serves as a Research Fellow with the Alliance for Lifetime Income and Retirement Income Institute. He is a professor of practice at the American College of Financial Services and past director of the Retirement Income Certified Professional® (RICP®) designation program. Wade’s latest book is Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All