The most important and challenging financial problem is how much one can safely spend in retirement. In January of last year, I disagreed with Morningstar’s 3.8% real spend rate over 30 years; I thought that was too high. Then real rates on TIPS surged from -1% to 2%, and I was able to build a 30-year TIPS ladder for myself and clients with a 4.4% real distribution.

The most important and challenging financial problem is how much one can safely spend in retirement. In January of last year, I disagreed with Morningstar’s 3.8% real spend rate over 30 years; I thought that was too high. Then real rates on TIPS surged from -1% to 2%, and I was able to build a 30-year TIPS ladder for myself and clients with a 4.4% real distribution.

I now agree with Morningstar.

But implementing the TIPS ladder is clunky, so I challenged the fund industry to simplify and improve with a TIPS ladder Fund. Stone Ridge Asset Management has done just that with its new LifeX Inflation Protected mutual funds. In fact, it went beyond my challenge and implemented some longevity-risk pooling as well as monthly distributions including during the nearly six years between 2034 and 2040 when there currently are no maturing TIPS. I interviewed Nate Conrad, head of LifeX at Stone Ridge Asset Management. Nathan Dutzmann first wrote about these funds in Advisor Perspectives.

I took a deeper look and performed an economic analysis.

There are two series of LifeX mutual funds – one pays a fixed nominal rate while the other has inflation-protected increases. I’m examining only the inflation protected, as the nominal series could be devastated by inflation.

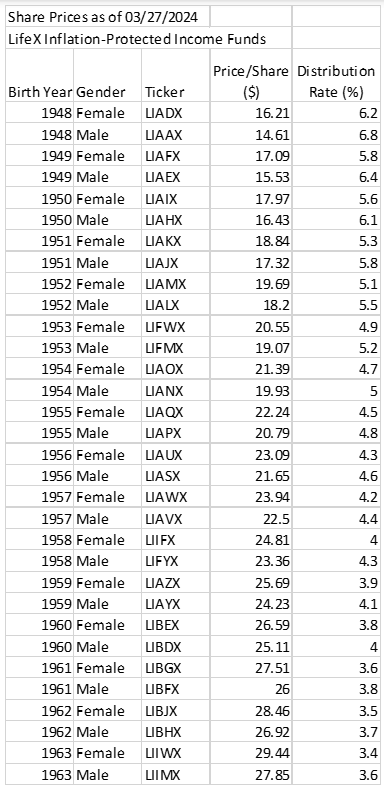

LifeX inflation-protected funds

- Each open-end mutual fund is offered exclusively to investors of a particular birth year and gender (currently born between 1948 and 1963) and is only available through the advisor channel.

- The funds intend to distribute monthly payouts until the end of the year in which the investor turns age 100.

- The funds offer daily purchases and sales of shares until December of the year in which the investor turns age 80, at which point the funds will reorganize into a closed-end successor fund (the “successor funds”). Heirs would inherit the net asset value if the investor died before age 80 but, like most single-premium immediate annuities (SPIAs), nothing after age 80.

- The successor funds intend to make payments to those still alive until December 31 of the year the cohort turned age 100, at which point any remaining funds would be distributed to the investors still alive.

- All funds currently have a 1% annual expense ratio.

As of March 15, 2024, the funds had the following payout rates, which would increase every year with the consumer price index (CPI). Payout rates vary from a low of 3.4% for a 60-61-year-old female born in 1963, to 6.9% for a 75-76-year-old male born in 1948. LifeX updates rates daily here.

Analysis

I decided to compare the product to a build-it-yourself TIPS ladder for a 65-year-old male born in 1958. I’m comparing the 30-year TIPS ladder to the LIFYX fund. Building a 30-year TIPS ladder using TIPS that matured the earliest in each year yielded a 30-year distribution rate of 4.53% a year, according to TIPSladder.com. That compares to a 4.3% yield for LIFYX. The small differential is reasonable since LIFYX is simple to buy, professionally managed, pays out monthly, and starts this year rather than in 2025. Conrad pointed out that its funds have mortality risk pooling and building a 35-year TIPS ladder (to age 100) would yield far less and have a large amount of uncertainty since we don’t know what the yields will be on TIPS issued over the next five years. He also pointed out that the tax efficiency of LifeX funds could be better than the direct TIPS ladder.

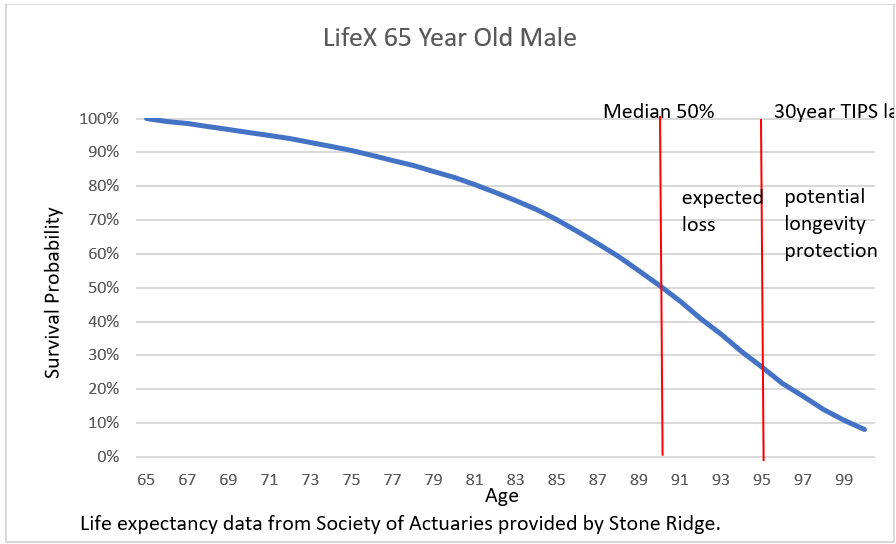

Conrad told me Stone Ridge used proprietary and confidential conservative actuarial tables from New York Life, and he did provide some life expectancy tables from the Society of Actuaries with the highest health status. This 65-year-old male would have a 25-year life expectancy, a 26% chance of living 30 years (beyond the TIPS ladder), and an 8% chance of living to age 100.

Graphically, the analysis is as follows.

The likely outcome (50th percentile) is that LIFYX would payout five fewer years to the investor’s heirs since their life expectancy is just over 25 years (though the Society’s online calculator for a male non-smoker in excellent health shows a 22-year life expectancy). If we go with the 25 years from LifeX, the expected total payout is about 5 years fewer than the 30-year TIPS ladder but there is also a 26% chance this person could live more than 30 years, meaning he outlived the 30-year TIPS ladder. There is also an 8% chance he could outlive the LIFYX payments to age 100.

This hypothetical man would be giving up an expected 16.7% of the investment to his heirs (which could also be his spouse) in exchange for up to five years of additional longevity protection. Conrad confirmed there was no joint-life product, but each spouse could buy their own.

For a 75-year-old man buying the 1948 fund, the mortality credits are far greater. LIAAX has a 6.8% distribution yield, and the cohort has a 16-year life expectancy. A 20-year TIPS ladder yields a lower 6.14% distribution yield.

I asked Conrad why someone wouldn’t want to build their own ladder and then buy their product closer to age 80. He responded, “We believe that LifeX offers positive longevity credits, net of expenses, for investors of all eligible ages.” But clearly, buying closer to age 80 would be economically superior. Conrad told me LifeX would likely close a fund to new investors once the cohort got to age 79 or so.

Finally, Conrad said that I needed to include a fee on the TIPS ladder. Even a 0.40% annual fee for someone to build and manage the TIPS ladder would lower the distribution yield of the TIPS ladder by 0.25% annually. I disagree with Conrad, as I’ve found building the TIPS ladder is not very time consuming and managing can simply be letting the TIPS mature. LifeX funds, on the other hand, can only be bought through advisors typically charging AUM-based fee. Advisors must always take the perspectives of what’s best for their clients.

I also noted to Conrad that the mutual fund wrapper would have the holders absorbing some of the costs of the larger bid-ask spreads as others moved in and out while it remained an open-ended mutual fund. Conrad stated that this was a matter of a few basis points in dragging down distribution yields.

There could be some unquantifiable risks such as actuarial calculations being wrong due to adverse selection or Stone Ridge deciding to shut down the funds if they can’t make enough profit if assets don’t flow in. Competitors with lower expense ratios could be one reason, though Conrad said Stone Ridge has filed for a patent.

My conclusion

This is a brilliantly designed, self-liquidating series of funds that did more than I stated in my challenge to the fund industry. It smoothed out the payments and provided some longevity protection.

There was only one challenge that wasn’t met. I wrote, “Creating and maintaining such an ETF would be child’s play for the ETF issuer, and the expense ratio should be very low – perhaps 0.05%.” LifeX has a 1% ER. On the other hand, these LifeX funds provide some longevity protection and smoothed-out monthly payments. That’s far beyond child’s play and becomes quite valuable as one approaches age 80, though one must buy it before Stone Ridge closes new purchases. After age 80, it’s a brilliant tontine- like product with assets backed by the U.S. Treasury.

Edward F. McQuarrie, professor emeritus in the Leavey School of Business at Santa Clara University, told me, “It's a very clever use of mortality credits for those in their mid-70s, which Stone Ridge can use to pay expenses and pad the payout to investors, unlike a regulated insurance company, which would have to hold on to those mortality credits to handle the very long-lived centenarian customers, plus reserve against mistakes and bad luck with experienced mortality."

I concur; before age 75, it’s mostly an expensive TIPS ladder fund. But later in life, those mortality credits could justify the 1% annual expense ratio. The consequences of running out of money are higher than dying with money. On the other hand, I wouldn’t put most of a portfolio in either LifeX or a TIPS ladder. I hope this is just the beginning and others will develop funds with similar strategies with lower costs.

It’s emotionally hard for savers like our clients to spend more money. We are always afraid of running out of it. A TIPS ladder is a license to spend. But a TIPS ladder with mortality credits can be a license to spend even more if the value of the mortality credits exceeds the costs. Under the right circumstances, LifeX has come up with a compelling solution.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Allan Roth

The most important and challenging financial problem is how much one can safely spend in retirement. In January of last year, I disagreed with Morningstar’s 3.8% real spend rate over 30 years; I thought that was too high. Then real rates on TIPS surged from -1% to 2%, and I was able to build a 30-year TIPS ladder for myself and clients with a 4.4% real distribution.

The most important and challenging financial problem is how much one can safely spend in retirement. In January of last year, I disagreed with Morningstar’s 3.8% real spend rate over 30 years; I thought that was too high. Then real rates on TIPS surged from -1% to 2%, and I was able to build a 30-year TIPS ladder for myself and clients with a 4.4% real distribution.