We financial planners spend a lot of time calculating and debating safe spending rates for our clients. In response to a recent piece I wrote, Challenging Morningstar’s Safe Withdrawal Rates, Bill Bengen, originator of the 4% rule, commented, “I am really tired of talking about the ‘safe’ withdrawal rate.”

We financial planners spend a lot of time calculating and debating safe spending rates for our clients. In response to a recent piece I wrote, Challenging Morningstar’s Safe Withdrawal Rates, Bill Bengen, originator of the 4% rule, commented, “I am really tired of talking about the ‘safe’ withdrawal rate.”

He is right – our clients are wealthier than the average American. I share many of my clients’ problem of underspending. We are afraid to spend the portfolio we worked so hard for so long to build.

I’m not suggesting we get our clients to spend for the sake of spending. But for many, myself included, there are psychological barriers that prevent us from spending that would bring more enjoyment and happiness. Intellectually, the client understands that dying the richest person in the graveyard isn’t a good goal. But emotionally, they can’t increase their spending.

Below is some research on why our clients built a sizable portfolio while others had high income but little savings. Then I’ll address some specifics on how to get savers to enjoy their money.

Savers and spenders

In the 1996 best-selling book, The Millionaire Next Door, authors Thomas Stanley and William Danko revealed the behavior of millionaires. While millionaires were high-income earners, they were also hoarders of that income who rejected the big spending lifestyle. They tended to drive older cars, shop for bargains, and not tout their wealth. Millionaires attained and maintained that status by hopping off the "hedonic treadmill," which is the tendency to adapt a higher level of income to higher expectations of material goods.

Why did some become millionaires while other high-income earners spent lavishly on the prestigious country club and most recent model of the luxury car? A paper, "Tightwads and Spendthrifts," by behavioral scientist Scott Rick of the University of Michigan, addressed the issue. This paper, along with a predecessor paper he co-authored, proposed that the pain of paying drives tightwads to spend less than they would ideally like. Spendthrifts don't experience the same amount of pain and, therefore, spend far more than they would like.

The paper referred to some research in which participants were given a series of purchase decisions while having their brains scanned by a functional magnetic resonance imaging (FMRI) machine. The decision to make the purchase was inversely related to action in an area of the brain called the insula, a region that is commonly active when experiencing painful stimuli such as offensive odors. The more the activity in the insula, the less likely the consumer was to make the purchase. Those experiencing more insula activity tended to be tightwads. Those with less activity tended to be spendthrifts.

Rick told me there was little genetic correlation for spendthrifts versus tightwads, confirming the Stanley research showing children of millionaires (tightwads) were often spendthrifts. He also said tightwads tended to be more anxiety prone than spendthrifts. This may explain why many clients who are well-positioned for retirement are the ones who fear they will never be able to retire. One recent study showed that 35% of those accumulating $1 million or more in investable assets stated it will take a miracle to ever be able to retire. Rick also gave a second theory, which is that tightwads get a joy from saving. This joy comes from both not spending (to build up assets) and from getting a good deal when they do spend.

Encouraging our hyperopic clients to enjoy their money

Hyperopia is an aversion to indulgence. These people are so far-sighted that they can’t enjoy their money – or at least not as much as they could. Cait Lamberton, now a marketing professor at the Wharton School at the University of Pennsylvania, co-authored a paper, “Seize the Day! Encouraging Indulgence for the Hyperopic Consumer.” As I mentioned, savers tend to have more anxiety and the paper supported this notion that the hyperopic consumer is afraid that short-term indulgence will undermine long-term goals.

I spoke with Lamberton, who brought up the framework of Maslow’s hierarchy of needs. She said that safety is the equivalent of savings but is low in the pyramid; it would be a shame if savers didn’t use some of their savings for the high-level needs. For example, taking the kids and grandkids on a memorable vacation might satisfy a higher social need. Esteem could be taking dance lessons or personal training in a sport you enjoy. It could also be spending on dental work to improve your appearance. For self-actualization, she suggested supporting the arts financially, eco- or volunteer tourism, or buying land to preserve or pass on to family and friends.

Lamberton also suggested viewing expenditures in more utilitarian way. As an example, one could view a massage as a hedonistic expenditure or an investment in one’s health and well-being.

I spoke to Clark Howard, a popular consumer media host who has helped many save, to get some advice on how to help people spend. He told me that being diagnosed with prostate cancer in 2009 made him realize his mortality and that he needed to start spending before he was too old to enjoy it. He suggested one should imagine 10 dream experiences, and then “go for it” by doing them over the next few years. Going forward, it can become a habit. He also stated that the joy of saving can be consistent with spending money if one is mindful about getting a good value. As an example, I recently experienced the joy of saving by staying at a five-star Waldorf Astoria hotel for $140 a night, which included a daily buffet breakfast for my wife and me.

Duke behavioral economist, Dan Ariely, suggested making a pledge to spend at least a fixed amount of money over the next year. For example, pledge to spend at least $120,000 – if you fail, the spending shortfall will go to a particular charity that you don’t necessarily want to support. Or, as a different strategy, you could stick to a regular budget but also include at least one extravagant experience each year.

Jim Dahle, founder of the White Coat Investor web site, has addressed the issue in his piece, 8 Ways to Spend More Money. Among his suggestions, try taking up an expensive hobby or “buying time” such as hiring someone to mow the lawn.

I posed the question of how to encourage spending to members of the Bogleheads forum. It’s comprised of some of the most successful, helpful, and frugal people. The first response was “Ha-ha, you came to the wrong place.” Another comment read, “I had a friend who was making $1 million a year in his 40s and 50s. He amassed over $10 million by age 50. He gave his wife grief for shopping at Walmart. He died in his early 60s and never enjoyed his money.” The online thread listed many ways these savers learned to enjoy their money.

Retirement researchers David Blanchett and Michael Finke addressed the issue in their paper, Guaranteed Income; A License to Spend. Blanchett told me creating a guaranteed cash flow changes the relationship with retirement savings. I couldn’t agree more, as the TIPS ladder I built along with delaying Social Security gave me a six-figure real (inflation adjusted) cash flow for the next 30 years. It satisfied my safety need and made it easier to spend for higher level needs.

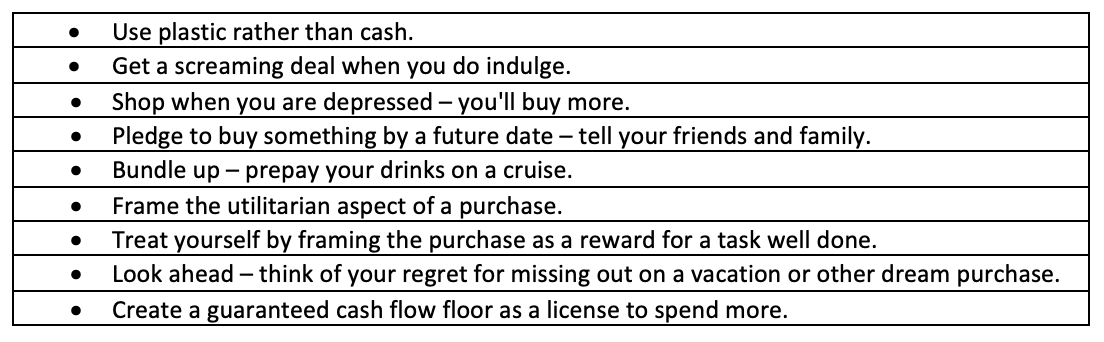

Below are some ideas to increase spending.

Conclusion

As far as problems go, finding ways to spend more money is one most Americans would love to have. But for those of our clients who have worked hard for their money and been disciplined about their spending and saving, flipping the switch from saver to spender can be emotionally challenging. Let’s help them reframe their thinking so that they can use their nest eggs to pursue a happier, more meaningful life.

A newly published book, More than Enough, by Mike Piper, brilliantly discusses some of the complex financial planning issues our clients will face when they realize they have more money than they’ll need in their lifetime.

Though I frequently advise clients to spend more for things they enjoy, I also disclose that I am a hypocrite. I tell them. “Do as I say, not as I do.” The human relationship with money can be quite complex and I’m still trying to improve my own preferences and habits. Financial planner – heal thyself.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

We financial planners spend a lot of time calculating and debating safe spending rates for our clients. In response to a recent piece I wrote, Challenging Morningstar’s Safe Withdrawal Rates, Bill Bengen, originator of the 4% rule, commented, “I am really tired of talking about the ‘safe’ withdrawal rate.”

We financial planners spend a lot of time calculating and debating safe spending rates for our clients. In response to a recent piece I wrote, Challenging Morningstar’s Safe Withdrawal Rates, Bill Bengen, originator of the 4% rule, commented, “I am really tired of talking about the ‘safe’ withdrawal rate.”