Morningstar released its report, “The State of Retirement Income,” in late 2022. Its key finding was that a balanced portfolio had a 90% success rate withdrawing an inflation-adjusted 3.8% annually over a 30-year period. That’s a large increase from the 3.3% in its 2021 report. A $1 million portfolio could support an additional $5,000 in inflation-adjusted spending, which is a 15.1% increase over last year’s number. Morningstar’s results showed higher safe spending rates across all asset allocations over all time horizons.

Morningstar released its report, “The State of Retirement Income,” in late 2022. Its key finding was that a balanced portfolio had a 90% success rate withdrawing an inflation-adjusted 3.8% annually over a 30-year period. That’s a large increase from the 3.3% in its 2021 report. A $1 million portfolio could support an additional $5,000 in inflation-adjusted spending, which is a 15.1% increase over last year’s number. Morningstar’s results showed higher safe spending rates across all asset allocations over all time horizons.

I don’t agree with those results.

I sent an email to the three Morningstar authors, Cristine Benz, Jeffrey Ptak, and John Rekenthaler noting I’d be writing about it and asking some questions. They are brilliant researchers who have helped countless investors achieve financial independence and have always demonstrated an open mind to feedback. The response from Rekenthaler didn’t surprise me: “The paper was intended to spark discussion. I will be happy to address your questions, and will be interested to see what you have to say.”

Return assumptions

The key assumptions in the report were the forecasted long-term returns. These returns are driven by two factors – the expected annual arithmetic returns and the volatilities, measured as standard deviations, for individual asset sub-classes. The greater the standard deviation, the lower the long-term geometric returns will be compared to the arithmetic returns. Morningstar dramatically increased its return assumptions.

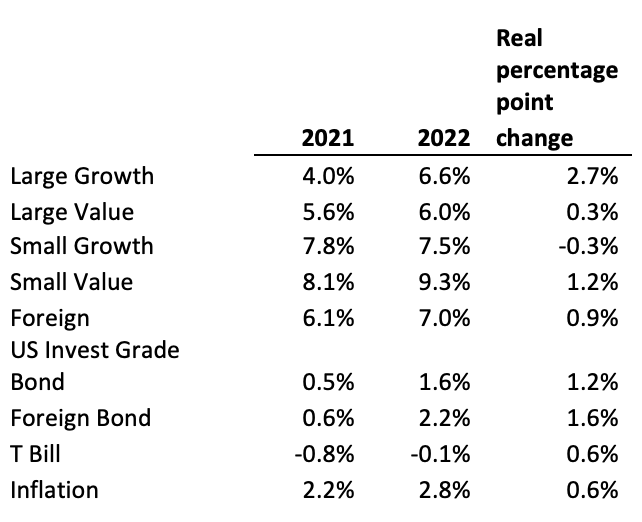

Morningstar also increased the assumed inflation rate. I do all of my modeling in real, inflation-adjusted dollars and returns. That translated to real returns as follows:

For example, Morningstar assumed large-cap growth, which represents 30% of the stock allocation, to return 2.7 percentage points annually more than it assumed last year. Morningstar increased the real annual returns of U.S. stocks from 5.6% to 6.8% and international stocks from 6.1% to 7%. There was very little change in the standard deviations. That meant those higher forecasted long-run returns were responsible for the higher safe spending rates.

Both stocks and bonds are a better buy today than they were a year ago. But I’m reflecting on the past, which is far easier than predicting the future. I can’t prove that Morningstar’s return assumptions are too high, but I believe the equity risk premium is far more stable than is justified by those large, one-year increases. I was in Japan in 1989 after its equity prices fell steeply, and its stock market is still below that level. This is one reason why Mark Hulbert wrote that a 1.9% safe spending rate is more appropriate.

But there are other more objective factors that show the return assumptions are too high. Morningstar assumed there are no investment expenses. Funds and ETFs have expenses on top of fees that we advisors charge. I’m happy to say fees are declining and give credit to Morningstar performance analysis and its documentation of the relationship between fees and returns. In an article I wrote last year, Rekenthaler calculated that paying 1% in fees (to the fund manager, the advisor, or both) lowered the safe spend rate by 0.4 percentage points.

An even bigger impact on real-world returns can be found in emotions. The most recent Morningstar “Mind the Gap” study showed that investors underperformed the funds themselves by 1.7 percentage points annually over the past 10 years, mostly by performance chasing. Over the years, I’ve provided evidence that advisors overall time investments poorly. How many investors rebalanced and bought more stocks in the 33 days between February 19 and March 23, 2020 when stocks lost 35%?

Even if you agree with the new market return assumptions used by Morningstar, there is ample evidence investors don’t get market returns.

Risk assumptions

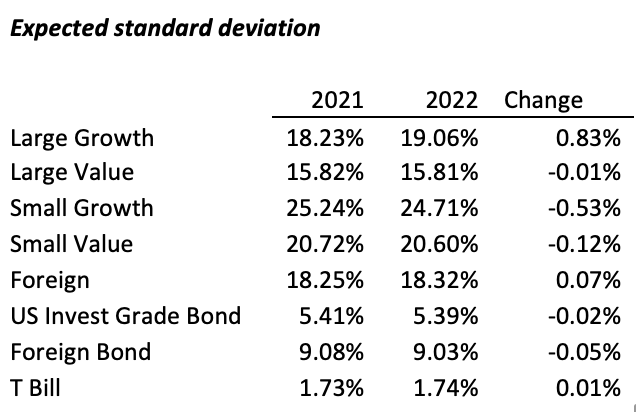

Below are the annualized standard deviations Morningstar used in this study as well as last year’s. They haven’t budged much. Despite 2022 being the worst year in the history of the bond market, the standard deviation of bonds decreased slightly.

In a Barron’s piece, I wrote that if we lived in a world of normalized distributions, what happened to the Bloomberg aggregate bond index fund this year would be a once in 50-million-year event, using the 10-year standard deviation going into the year. Of course, we live in a world of fat tails, meaning that events with low probabilities occur more than are statistically predicted. Rekenthaler confirmed fat tails weren’t considered but said neither was reversion to the mean, which would somewhat offset fat tails. But, as in the Japanese stock market, reversion to the mean hasn’t happened over the last 33 years.

The world is far riskier than what normalized distributions predict when developing safe spending rates. In fact, if you look at the history of the longevity of sovereign countries, there may be a slightly less than 10% chance the U.S. government will not last 30 years. The world has deep risks, as William Bernstein has documented: inflation, deflation, confiscation, and devastation.

Dynamic spending strategies aren’t binary

The study also noted that dynamic spending strategies can increase the initial safe spending rates if retirees are willing to lower the overall spending later if the portfolio doesn’t perform as expected. I’m in general agreement and this is consistent with David Blanchett’s spending smile. Blanchett noted, “The ‘smile’ can likely be attributed to the fact younger retirees are better able to travel and enjoy retirement, while older retirees incur higher relative medical expenses.”

Yet rules can be too rigid. For example, one method is to skip the inflation adjustment in a year in which the portfolio has declined in value, though this binary decision doesn’t consider magnitudes. A .01% increase in inflation, for instance, would mean a larger withdrawal, while a 0.01% decrease would forgo the adjustment. And that .01% decrease would have the same spending as a 50% loss in value. Rekenthaler agreed, noting it’s simpler to model without using dynamic spending rules, and his attempt was to show which decisions have the greatest effect.

Conclusion

Morningstar’s work on safe withdrawal rates is the best I’ve reviewed. It goes beyond my modeling and looks at safe withdrawal rates across multiple asset allocations and calculates safe withdrawals for periods between 10 and 40 years. It demonstrated that a more evenly split allocation to stocks and bonds generally had a higher safe withdrawal rate than either an aggressive allocation (more equities, taking on too much risk) or a conservative allocation (all bonds and cash, unlikely to best inflation by much). That said, expenses, emotions and living in world of fat tails will reduce safe spending rates.

It will take decades to reveal who is correct. William Bengen, noted for developing the 4% rule, now thinks 4.7% is a safe spending rate. I took $1 million of my own money to build a 4.36% real withdrawal, though it leaves no residual after that 30-year period.

My logic for using conservative safe spending rates is that the cost of running out of money is greater than the cost of dying with money. As I tell clients, I’d rather have them come back to me in a decade saying they have too much money than informing me they are running out of money.

The former is an easier problem to solve.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Morningstar released its report, “The State of Retirement Income,” in late 2022. Its key finding was that a balanced portfolio had a 90% success rate withdrawing an inflation-adjusted 3.8% annually over a 30-year period. That’s a large increase from the 3.3% in its 2021 report. A $1 million portfolio could support an additional $5,000 in inflation-adjusted spending, which is a 15.1% increase over last year’s number. Morningstar’s results showed higher safe spending rates across all asset allocations over all time horizons.

Morningstar released its report, “The State of Retirement Income,” in late 2022. Its key finding was that a balanced portfolio had a 90% success rate withdrawing an inflation-adjusted 3.8% annually over a 30-year period. That’s a large increase from the 3.3% in its 2021 report. A $1 million portfolio could support an additional $5,000 in inflation-adjusted spending, which is a 15.1% increase over last year’s number. Morningstar’s results showed higher safe spending rates across all asset allocations over all time horizons.