Advisors who use Dimensional funds are generally believed to more likely adhere to their investment strategies than their peers. A comparison of fund and investor returns calls this conventional wisdom into question.

Advisors who use Dimensional funds are generally believed to more likely adhere to their investment strategies than their peers. A comparison of fund and investor returns calls this conventional wisdom into question.

I chose to analyze the oldest small-cap value fund because the last 15 years haven’t been kind to that asset sub-class. As of May 6, 2022, Morningstar shows Dimensional Fund Advisors Small Cap Value Fund (DFSVX) averaged 6.69% annual returns, lagging the 9.04% performance of Vanguard’s Total Stock Fund (VTSAX). That translates to 164% cumulative growth for the Dimensional fund and 266% for the Vanguard fund.

Whenever I write about the relative performance of funds, I get comments like, “If you go back longer, DFSVX has bested the total-stock fund by three percentage points annually.” But were investors as a whole better off with the Dimensional fund?

I asked Morningstar to run the numbers since inception of the Dimensional fund on May 2, 1993. Its data went back to the beginning of 1995. Did Dimensional investors outperform since then? Though the answer is a resounding “no,” my research also uncovered some behavioral traits of the advisors who control those funds (for the most part, Dimensional’s mutual funds can only be purchased through an advisor and not directly by retail investors). Shockingly, since inception, more funds have flowed out of DFSVX than in.

A primer: Fund and investor returns

The return of any fund is the geometric annual average growth. The investor return is the internal rate of return one gets on their money. A simple illustration is as follows:

An investor puts $50,000 in a fund and earns a 30% return in year one. Feeling confident, she puts an additional $450,000 in that fund at the end of that year. But then the fund declines by 10%. The fund itself earned an 8.87% annualized return but the investor lost $36,500 or a negative 6.68% annually.

Before applying this to the Dimensional fund, let’s look at a real-world example that has been in the news lately – Cathie Wood’s ARK Innovation Fund (ARKK). FactSet’s Elisabeth Kashner calculated that since inception on October 30, 2014, Wood bested the Vanguard Total Stock Fund by 2.33% annually through May 3, 2022. Yet the average investor lagged by 2.45% annually.

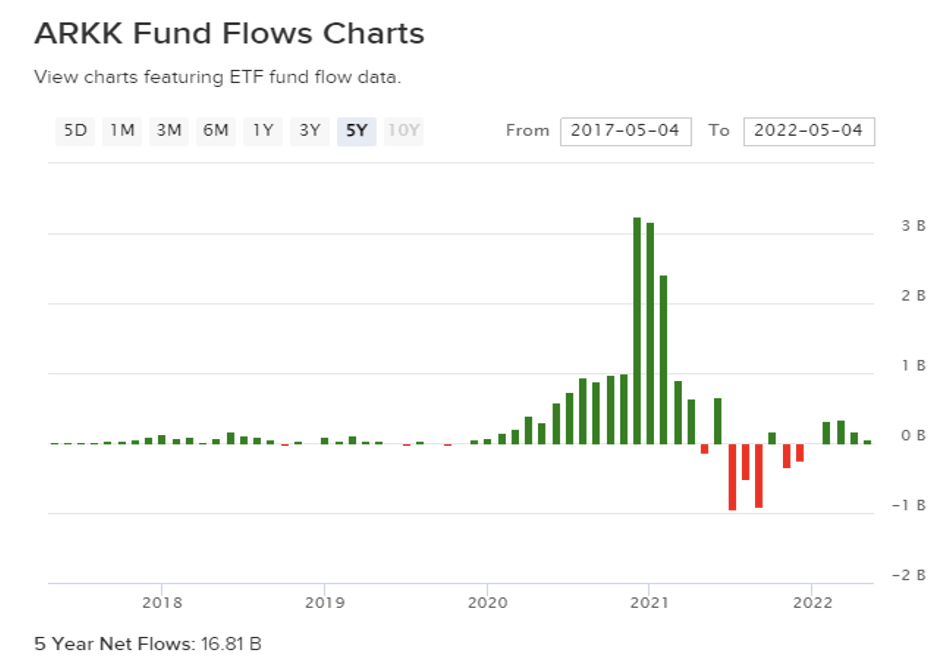

The large difference between these two numbers is illustrated in the following Morningstar chart comparing ARKK to the ETF share class of the Vanguard Total Stock Market Fund (VTI). ARKK performed spectacularly until the last year and a half. Billions of dollars poured in just in time for its dismal performance; the fund had far more money when it underperformed. To its investors’ credit, however, money has not poured out, as investors appear more disciplined, at least for the time being.

Below you can see the flows into the ARKK fund, according to ETFDB.com.

Applying this to DFSVX versus VTSAX returns

It would be inappropriate to compare Dimensional’s relatively low-cost and academically based Fama French design to a recent hot fund that turned ice cold. And Dimensional itself has said for some time that factors can underperform for long periods of time. But the principle of investor and fund returns still applies.

Morningstar Direct was able to go back to the beginning of 1995 (not too long after its 1993 inception) and obtain both fund and investor returns. To compare, I used the oldest of the total U.S. stock funds – the Vanguard Total Stock Index Fund. I started with the VTSMX investor share class but then switched to the lower cost VTSAX share class the first year it was available. Investor-return data was available only through the end of 2021.

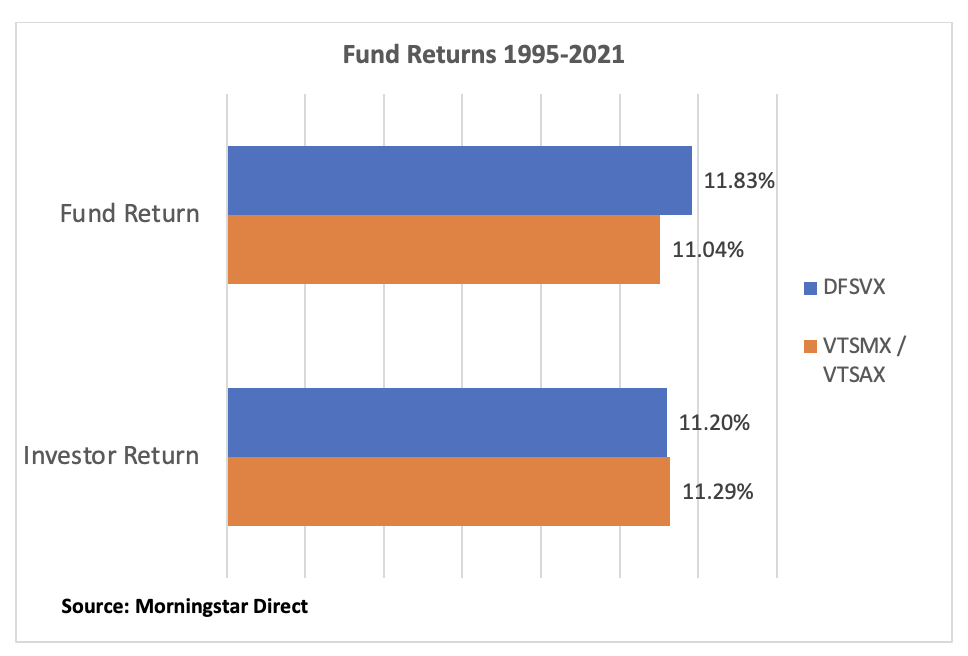

Though the returns differed by only 79 basis points, over 27 years of compounding, a $10,000 investment in DFSVX grew to $194,680 versus only $159,023 for the cap-weighted Vanguard fund. But investors, on average, did better with the Vanguard Total Stock Fund. The difference (9 basis points) may seem small, but this is just the start. I’ll explain the three issues one must consider when evaluating returns in a bit.

The key takeaway relates to the behavior of the investors in each of these funds. It is not fair to compare their performance without that context, since a small-cap value fund has a very different profile than a market index fund. It is, however, the most volatile among Morningstar’s style boxes, so it is reasonable to ask whether investors were compensated for that risk.

Is it behavior?

Vanguard investors had slightly higher returns than the fund itself. On the other hand, Dimensional investors underperformed the fund. Investor behavior could be one explanation, but Dimensional correctly pointed out that even steady cash flows can result in differences between fund and investor returns.

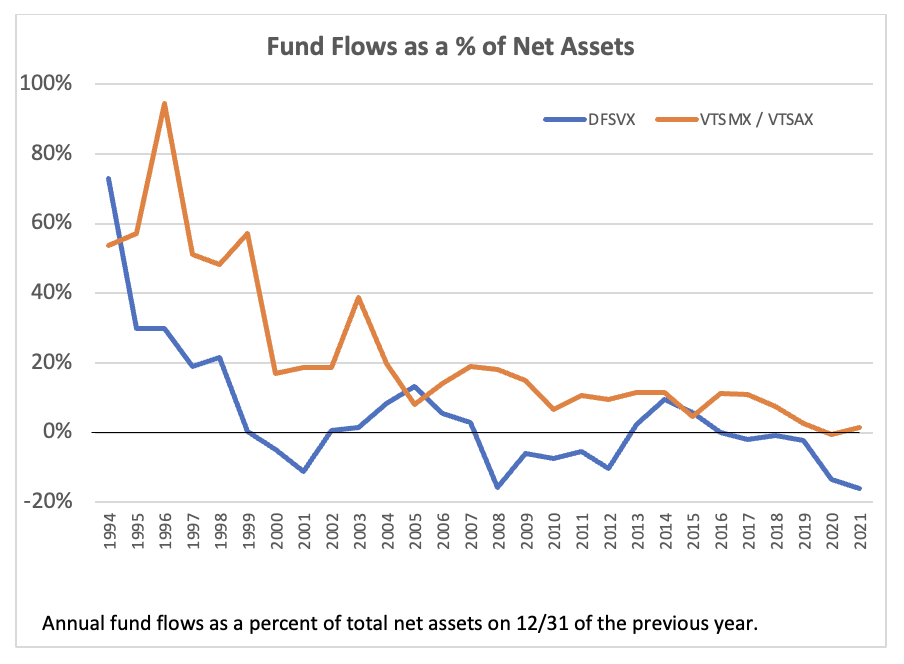

Morningstar Direct provided me with fund flows for the two funds. Since the sizes of the two funds are vastly different, I calculated the fund flows each year as a percentage of assets beginning that year.

Fund flows as a percentage of assets were far more volatile in the early years, as both funds were relatively small (had small denominators) compared to assets today. By this measure, Dimensional had more volatile fund flows, including negative flows in 10 of the last 15 years. This is the timeframe of its underperformance versus the cap-weighted fund. The Vanguard fund did have outflows in 2020, but, on average, the Vanguard investors were more disciplined than DFA investors and their advisors.

This counters the philosophy of Dimensional approving advisors who are disciplined. In fairness, those outflows occurred during a period when evidence also shows advisors were broadly pulling out of value funds and ETFs in favor of passive, indexed approaches. There is no reason to believe Dimensional advisors were less disciplined than other advisors who embraced value-based investing.

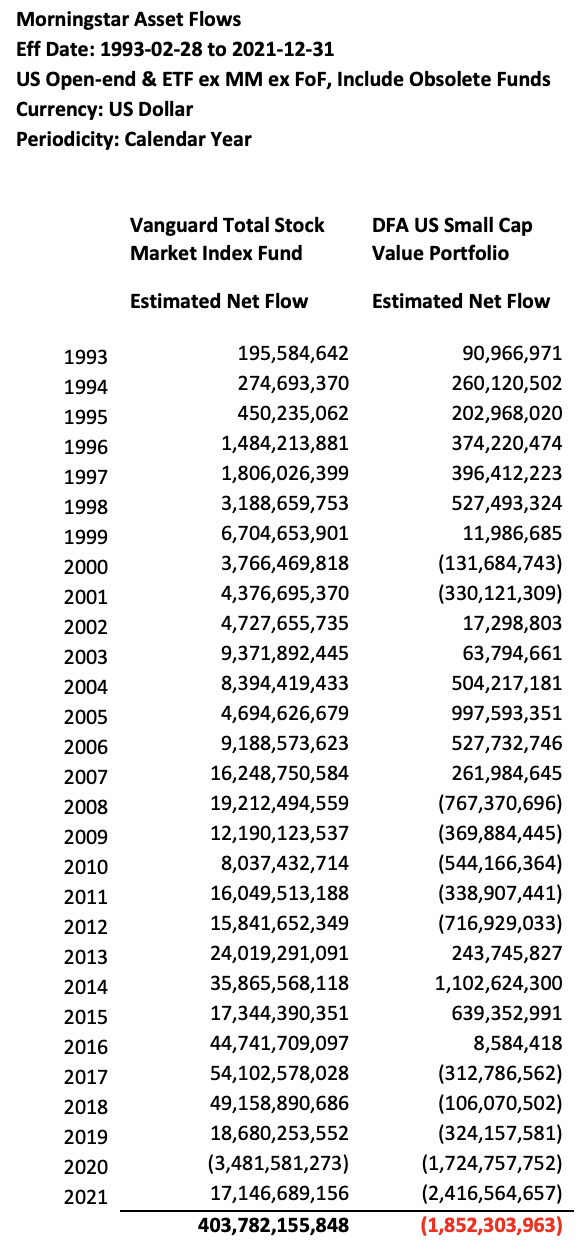

What shocked me the most was the fact that DFSVX in the aggregate since inception has had over $1.8 billion in negative fund flows. I was so surprised by this data that I asked Morningstar to confirm, which it did. Below are the annual fund flows:

I spoke to Wes Crill, the head of investment strategists and a vice president at Dimensional. He stated:

Dimensional believes in research-driven investment solutions that pursue size, value, and profitability premiums (in equities) with broad diversification and low turnover. Our portfolios use information in market prices every day to systematically pursue higher expected returns while managing risks and controlling costs.

Based on valuation theory, we expect the size, value, and profitability premiums to be positive every day. The realized premiums are more likely to be positive as you extend the period, going from around 60% positive over a 1-year horizon to over 85% over 10 years. But the premiums are not guaranteed over any horizon. If they were, you would only be able to expect the risk-free rate. Uncertainty is part of why you earn a premium.

Crill did not comment on the fluctuations in DFSVX fund flows indicating that advisors may be poorly timing when to use factors. It’s also possible some of the outflows were due to the clients needing the money to live on or going to other, newer factor-based funds, such as the Advantis US Small Cap Value ETF (AVUV).

Looking at the total picture

The investor performance of DFSVX was only 9 basis points less annually than the total stock fund, but consider three additional points.

Until recently, the investor generally had to pay an advisor to get access to Dimensional funds. That needs to be considered when looking at total performance. Recently, Dimensional launched a very similar ETF, the Dimensional Small Cap Value ETF (DFSV) which can be bought without an advisor.

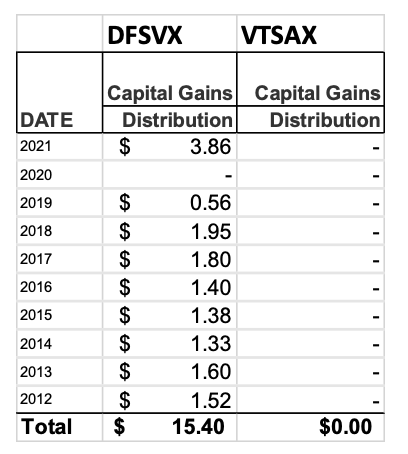

Taxes are fees too. While Dimensional notes tax efficiency is a goal, it has distributed $15.40 in gains over the last decade versus $0.00 for the Vanguard fund, according to Lipper. Some of the gains in 2021 were short-term. I bought a little DFSVX nearly 20 years ago and have been surprised at the poor tax efficiency. And, if fund flows continue to be negative, DFA could be forced to liquidate more stocks to meet the redemption cash requirements and pass-through gains to fundholders who didn’t sell.

In fairness, however, total-market index funds are by design very passive, generate negligible turnover and are tax efficient; the more a fund deviates from the total market (as is the case with a small-cap value fund), the more likely it is to generate turnover and be tax inefficient. Dimensional is known for its trading capabilities, which it claims minimize the adverse effects of fund flows, and it is possible that its small-cap-value fund is more tax efficient than its competitors.

Crill told me that DFA has other funds that have greater tax efficiency.

Finally, in looking at performance, one must consider the riskiness of each investment. Fama and French never said factors were a free lunch. And to DFA’s credit, every time I talk to them, they note factors are compensation for taking on more risk.

Conclusion

Crill stated, “Valuation theory says that a stock’s price equals its expected cashflows discounted at its expected rate of return. All else equal, stocks with lower prices or higher expected cashflows have higher expected returns. Hence, value stocks with lower relative price (price-to-book) should outperform growth stocks with higher relative price.”

I agree. But the expectation of market outperformance is due to taking on more risk. And one must consider taxes and discipline in looking at returns. The past tax efficiency could be improved with the newly launched and very similar Dimensional US Small Cap Value ETF (DFSV) due to in-kind redemptions of ETFs. Yet discipline is up to the advisor and consumer. Overweighting any part of the market is making an active bet. Though small-cap value is likely a better buy now (relative to the overall market) than 10 or 15 years ago, one must have the discipline to stay the course to recognize those better odds stated by Crill.

So far this year, the DFA US Small Cap Value fund is significantly outperforming the Vanguard Total Stock Fund.

If you use factor tilting, use it in moderation and be very cost-conscious. Small-cap value is only a tad over three percent of the stock market, so keep this bet to a moderate level. Beta captures the market return, which can be accomplished by owning an ultra-low cost and tax-efficient cap-weighted total-stock index fund. Don’t be fooled into thinking overweighting factors is another form of beta. Still, a low-cost, factor-driven strategy for part of a portfolio is a reasonable active strategy. I’m keeping my small amount of DFSVX and continue to view DFA as an outstanding fund family.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Advisors who use Dimensional funds are generally believed to more likely adhere to their investment strategies than their peers. A comparison of fund and investor returns calls this conventional wisdom into question.

Advisors who use Dimensional funds are generally believed to more likely adhere to their investment strategies than their peers. A comparison of fund and investor returns calls this conventional wisdom into question.