Emerging Markets: The Biggest, Fastest Growing, and Arguably Least Understood Pool of Credit in the World

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Emerging market (EM) debt’s composition, risk, return, and correlation characteristics have transformed over the years. Yet many investors today use EM debt for the wrong reasons, manage it imprudently, or overlook the best parts.

- EM debt used to be characterized by a higher distribution of more extreme outcomes. But now its distribution of returns resembles that of more mainstream asset classes such as U.S. corporate debt.

- The main reason to consider EM debt is for its diversification benefits relative to other spread sectors such as U.S. corporate debt, in our view, rather than as a way to hunt for high returns.

- Macro risk in EM has shifted from economic complexity, which can be modeled, toward political uncertainty, which can be impossible to predict. Thus, taking only a macro-driven approach toward alpha generation is more likely to backfire today than in years past.

In amateur tennis, fully 80% of points scored are the result of an errant shot, such as hitting the ball out of bounds. This was the insight that Charles Ellis used to characterize investing in his classic “The Loser’s Game.” It is not what investors get right that defines success, it is what they do not get wrong.

While he was writing in 1975, this idea captures a lot of what happened to emerging market (EM) debt during the mid-2000s. Investors who were leaning into risk and trying to time the market around macro events started to play a loser’s game. The winner’s game, in contrast, shifted toward bottom-up trades that are uncorrelated to election cycles, geopolitical events, and other systemic macro events – areas where it has become more difficult to have an edge as an investor.

EM debt has become the largest pool of credit in the world, according to the Bank for International Settlements, surpassing the U.S. over the past decade. Along the way, many of EM’s fundamental attributes have been transformed. As the market has evolved, so too must investment strategies adapt.

The best countries or regions are generally not those being hyped as the next success stories. In contrast to conventional wisdom, EM often rewards investors who minimize losses rather than maximize gains, and who avoid concentrated positions in high-yielding countries. We believe EM debt should be used primarily as a diversification tool – rather than a source of seeking high returns – prioritizing lower-risk countries and senior debt structures.

EM debt has similar default and recovery rates to U.S. corporate debt but also more volatility, especially for lower-quality issuers. That’s one reason why we believe bottom-up relative-value analysis and portfolio construction are more important to EM today than top-down macro analysis. In addition, active management in EM debt has consistently outperformed passive investing, according to Morningstar data.

Rapid economic growth through the early 2000s masked many underlying complexities in EM, but growth has slowed. In this piece, we attempt to unmask the asset class, identifying universal features of EM and how they can help in achieving broader investment objectives.

Storytelling versus hypothesis testing

The optimistic stories told by EM investors for decades revolved around demographics, urbanization, a rising middle class, and GDP growth catching up to developed market (DM) levels. Today’s stories are more nuanced. Catch-up growth continues, but at a slower pace. Policymakers are better at business cycle stabilization, but there is greater political and geopolitical uncertainty than before.

These stories aren’t inaccurate, but they have not always mattered for investment returns. EM equities should have been the biggest beneficiary from stronger growth, for example, but fared worse than both DM equities and EM debt.

Here, rather than storytelling, we take a more scientific approach. The investment hypothesis for EM debt is as follows. It should be used primarily as a means to reduce concentrations to other domestic risks without sacrificing yield.

Investors should not treat EM as a space to hunt for high returns. It may sound counterintuitive, but the case for EM debt should not be anchored on spreads, yields, or some other valuation metric. It should be based primarily on diversification benefits, in our view.

Therefore, investors should consider taking a page from Warren Buffett’s book: 1) prioritize lower-risk countries with reasonable valuations over high-risk countries with great valuations, and 2) move to more senior parts of the capital structure (from equity to debt).

Of course, there are exceptions. But this is the top-level hypothesis that seems best supported by the data.

An anatomy of the asset class

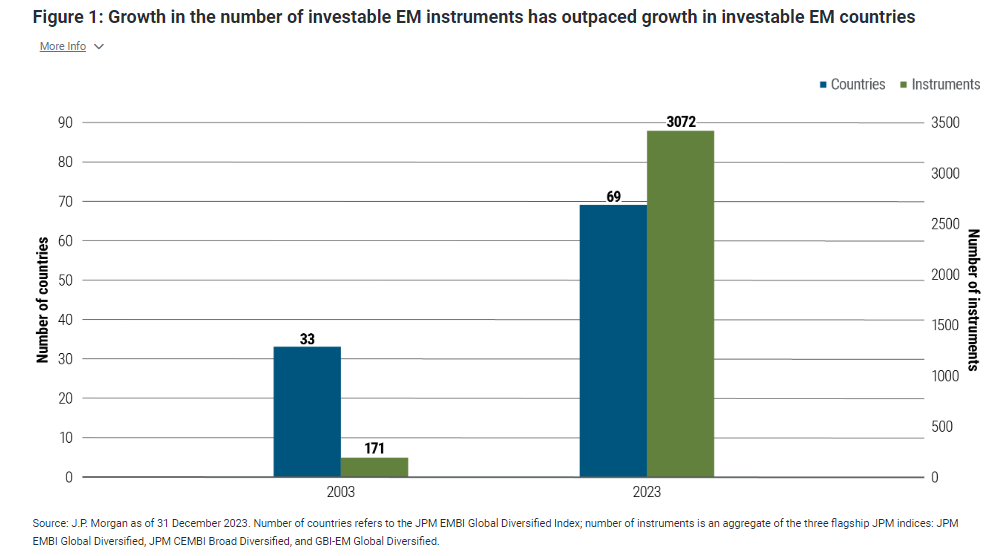

The number of investable EM countries has more than doubled in the past 20 years. We now model about 200 individual macro risk factors (such as foreign exchange, rates, and spreads) across about 85 countries. Correlations across this matrix range from 0.8 to -0.7, according to data going back 20 years, calculated by PIMCO. So there is extreme diversity within the asset class.

Moreover, some factors are “risk-on” while others are “risk-off,” i.e., positively or negatively correlated to global systemic factors such as oil or equities. There are now about 12 sovereign bond issuers that have provided similar portfolio ballast during risk-off events over the past 15 years as U.S. Treasuries, the perceived ultimate risk-off asset. During this 15-year period, a basket of EM local bonds hedged to U.S. dollars (as gauged by 5-year swaps) generated higher returns than comparable U.S. Treasuries (also as gauged by 5-year swaps) and had a similar success rate in hedging equity drawdowns but less of a payout when drawdowns occurred.

This increase in the number of countries has been overshadowed by the rise in available instruments, which has grown nearly 20-fold (see Figure 1) in the past two decades. Investors can now disaggregate country-level macro risk factors into fine granularity.

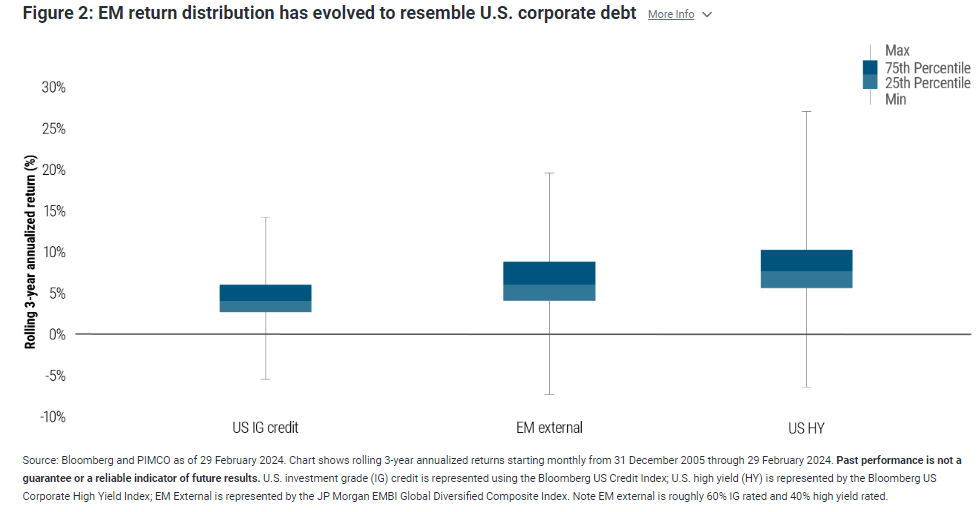

This is positive for the asset class. EM debt used to be characterized by fat tails – i.e., a higher distribution of more extreme outcomes. But now its distribution of returns resembles that of more mainstream asset classes such as U.S. corporate debt (see Figure 2).

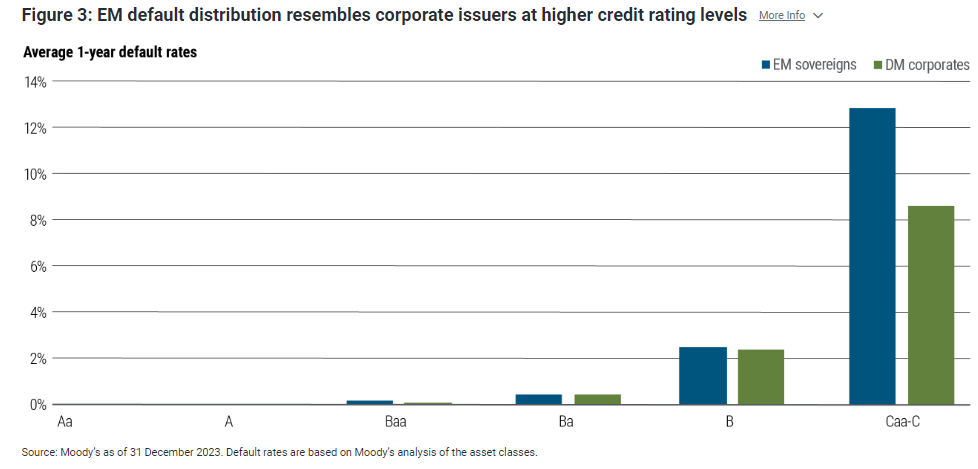

Fundamental credit risk is also similar. Defaults along much of the credit ratings quality spectrum, from AA to single B, are in line with U.S. corporate issuers (see Figure 3).

Recovery values (and loss-given-default) are also nearly identical, at about 40%. However, there are three nuances to note.

- Default probabilities for issuers rated CCC are higher for EM than for U.S. corporates. (Spreads are wider too, so we are not commenting on whether this cohort is relatively rich or cheap.) This is because the rules of the game can get rewritten for the lowest-quality EM issuers because of political upheaval, whereas U.S. corporate issuers rated CCC operate within a more defined system of stable rules and bankruptcy law.

- While the EM and U.S. corporate default data share a similar mean, the EM data has a wider standard deviation. Default events in EM have a wider range of outcomes.

- Workouts can take longer in EM. A U.S. corporate restructuring may take months to work through a court system. By contrast, it may take years to negotiate terms among international creditors, the International Monetary Fund, and other bilateral lenders. All else equal, this means that the present value of a nonperforming EM debt instrument undergoing a restructuring will be lower (even if the ultimate recovery value is the same).

Asymmetry of certain risks

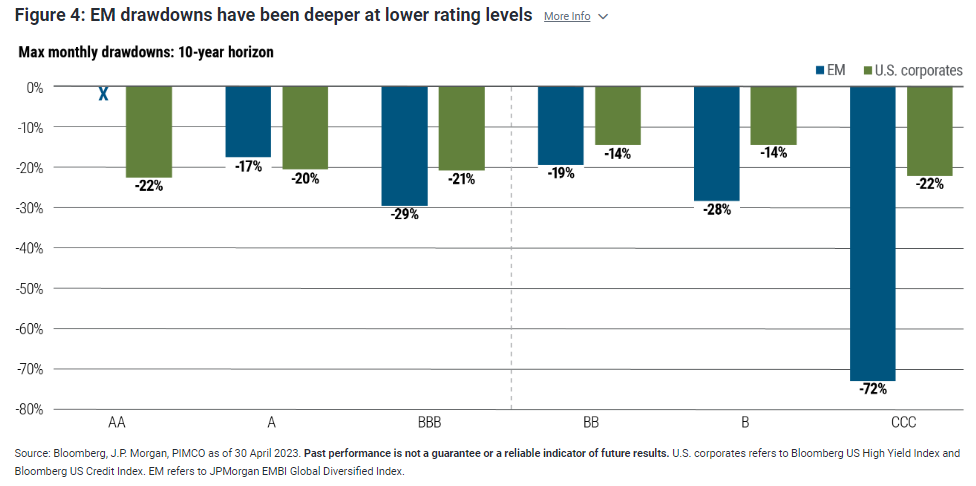

There is an additional empirical nuance, perhaps the most important one of all: the mark-to-market efficiency of returns along the quality spectrum, as captured by metrics such as the Sharpe ratio, a gauge of risk-adjusted return. Similar to fundamental credit risk, measures of mark-to-market volatility increase much more on the lowest-quality bonds in EM than in U.S. corporate debt, rendering a lower Sharpe ratio for EM debt rated single B and CCC.

Drawdowns are also disproportionately deeper during times of acute stress for EM (see Figure 4). Worst of all, the sensitivity to market-based returns, or betas, becomes asymmetric, meaning the downside capture during a market sell-off is larger than the upside capture during a rally.

None of this means that there cannot be compelling value in EM debt rated single B and CCC. But it does explain why too many investors have been seduced by the siren song of high-yielding, low quality frontier markets. The bonds may be cheap, but the efficiency of the resulting returns is poor for investors with anything short of a very long time horizon.

This explains why EM debt offers higher spreads compared with U.S. corporates despite similar fundamental credit risk – about 70 basis points on average on a risk-neutral basis over the past five years. The additional spread is not a sign of market inefficiency. It is compensation for other burdens, such as unfamiliarity (i.e., the need to explain newspaper headlines to one’s investment board), wider bid-ask spreads in secondary markets, and additional mark-to-market volatility, especially on lower-quality bonds. In theory, these additional burdens shouldn’t matter to long-term value investors. But in practice they do.

Investment approach

This siren song also explains why some investors say they’ve been on a roller coaster ride with EM in the past. Beyond general asset class volatility, many have been exposed to 1) poor sizing of the asset class in their broader portfolio, and 2) imprudent risk scaling within the EM debt allocation. Let’s look more closely at both.

Strategic asset allocation (sizing the beta)

If diversification is the main objective, then the correlation of EM debt to a broader portfolio is the most important metric. This is true for any asset class, but it is especially important for satellite exposures that play a more peripheral role in portfolio construction.

An asset inclusion test offers a clear framework. It reduces the decision whether to include an asset class to an optimization function: Maximize a portfolio’s Sharpe ratio subject to the constraints of risk, return, and correlations of the individual assets.

The result is a measure of each asset’s marginal impact on the portfolio’s overall Sharpe ratio. This will be fairly unique for each investor. But generally speaking, EM debt scores better than most other assets. It does so because of favorable correlation characteristics, not solely because of higher yields.

The correlation between EM debt and U.S. corporate debt is about 0.63 over the past 10 years, using J.P. Morgan data. This is relatively low within the world of fixed income spreads. And this is the point: EM debt must be assessed jointly by its risk, return, and diversification properties at the broader portfolio level, rather than narrowly on some rich/cheap valuation metric, and not independently from one’s overall portfolio.

Abiding by these guidelines leads to a more sober assessment of sizing in strategic asset allocations. Many clients, ranging from insurance companies to pension funds, typically have chosen an allocation of 2% to 8%.

Risk scaling (seeking alpha)

Investors are always at the mercy of what the market offers. If markets evolve, so too must investment strategies.

Consider how the EM debt market has evolved. In the early years (1990s and early 2000s), there were few countries in EM. Most issuers readily overpaid to access international capital. Growth was booming but punctuated by homegrown shocks (e.g., 1994 in Mexico and 1997 in Asia). The key skill set was top-down macro analysis. Investors could beat the market by leaning into risk and harnessing excess yields, while hopefully sidestepping country-specific sell-offs.

Today, there are far more countries and instruments to consider. Growth is middling and recent shocks are mainly exogenous and systemic (e.g., the 2008 global financial crisis, 2013 Treasury taper tantrum, and 2020 pandemic).

It is difficult to have an edge in macro analysis. Not only is it a more crowded field, but the nature of risk has shifted – from economic complexity, which can be modeled, toward political uncertainty, which can be impossible to predict.

In our opinion, the key skill set for investing in EM debt today is bottom-up relative-value analysis and portfolio construction. It is the ability to identify small arbitrage opportunities, instrument by instrument, and then combine and scale each in a way that a basket of these trades is more efficient than any one is independently.

Convexity – or the nonlinear relationship between prices and yields – is key. It embeds downside cushion during market sell-offs – prices fall but decreasingly so. This is particularly important given the excess volatility and asymmetric beta sensitivities noted earlier, especially at the lower end of the quality spectrum.

Of course, top-down macro analysis remains critical – but as a starting point. It must be thoroughly mapped to create space for the bottom-up alpha process to flourish. We model and measure 10–15 distinct bottom-up trade types and scale them in portfolios based on their Sharpe ratios and correlations to the beta. This is an engineering challenge, which leads to much more bounded results than if it were a forecasting challenge.

Playing a winner’s game

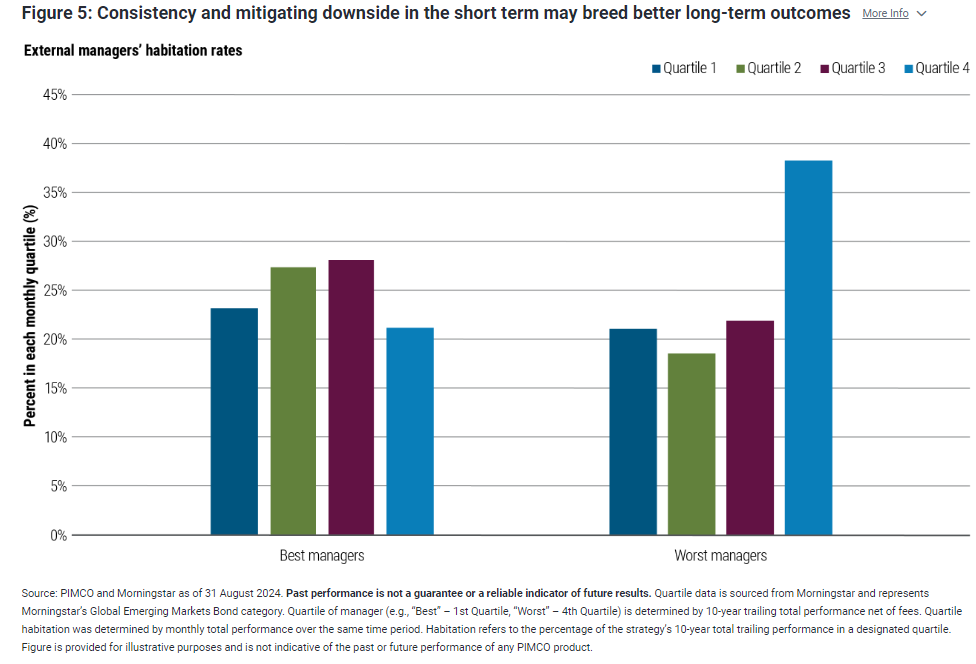

The tennis analogy mentioned earlier – winning by limiting errors – is not just a metaphor. It comes through clearly in the data. Consider the best and worst EM debt investors over the past decade (see Figure 5), and compare the journey, month-by-month, of each along the way. Did the best investors achieve their status by maximizing victories or by minimizing defeats? The answer is clear.

The best and worst investors had about the same frequency of 1st-quartile monthly returns (23% versus 21%, respectively). But the best investors had a dramatically lower frequency of bad months. They experienced 4th-quartile monthly returns 21% of the time, versus 38% for the worst managers.

This is consistent with the asymmetric return profile of the asset class discussed earlier. The efficiency of returns from higher-quality countries can be overshadowed by the inefficiency of returns from lower-quality countries. Likewise, years of positive alpha, or market outperformance, can be wiped out in a single drawdown episode.

Our process is explicitly designed around these empirical realities for the asset class. It is designed to minimize the incidence of 4th-quartile monthly returns. (Please reach out to your PIMCO representative for statistics specific to PIMCO.)

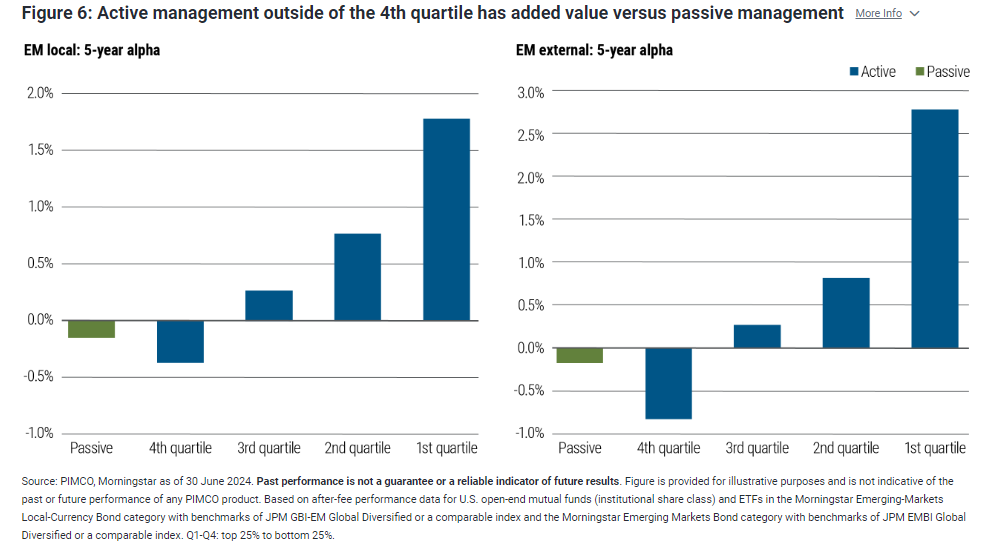

What about passive investing? It has been remarkably consistent, ranking at the lower end of the 3rd quartile year after year (see Figure 6).

The vast majority of active managers perform much better. Moreover, this better performance does not have to feel like a roller coaster.

Investors can treat EM debt as a structural allocation, used to de-concentrate from domestic sources of credit risk. They can size the allocation based on its effect on the Sharpe ratio of their overall portfolio. And, most importantly, investors should manage the EM allocation with caution. That can mean avoiding the temptation to migrate toward high-conviction, high-concentration positions in high-yielding countries, which can magnify macro-driven volatility. That game may have worked two decades ago. But it is a difficult game to win today.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. Diversification does not ensure against loss.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

Alpha is a measure of performance on a risk-adjusted basis calculated by comparing the volatility (price risk) of a portfolio vs. its risk-adjusted performance to a benchmark index; the excess return relative to the benchmark is alpha. Beta is a measure of price sensitivity to market movements. Market beta is 1. Convexity is the curvature in the relationship between bond prices and interest rates. It reflects the rate at which the duration of a bond changes as interest rates change. Correlation is a statistical measure of how two securities move in relation to each other. The correlation of various indexes or securities against one another or against inflation is based upon data over a certain time period. These correlations may vary substantially in the future or over different time periods that can result in greater volatility. The Sharpe Ratio measures the risk-adjusted performance. The risk-free rate is subtracted from the rate of return for a portfolio and the result is divided by the standard deviation of the portfolio returns.

The terms “cheap” and “rich” as used herein generally refer to a security or asset class that is deemed to be substantially under- or overpriced compared to both its historical average as well as to the investment manager’s future expectations. There is no guarantee of future results or that a security’s valuation will ensure a profit or protect against a loss.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2024-0802-3767239

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All