Going All In – The Bubble in Profit Expectations

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDuring each speculative run-up in asset prices – whether the dot-com bubble, the housing bubble, or more recently the rapid rise (and fall) of the stocks of electric vehicle companies – there’s typically a moment when Wall Street strategists, analysts, and investors go all-in on that theme.

At the end of 1999, year-ahead profit margins for the S&P 500 Index were projected to be 8.5%, according to Factset estimates. By the time the market peaked in September of 2000, year-ahead profit margin estimates had jumped by more than 4 percentage points, as analysts looked for large and immediate benefits from the wide-spread spending on technology that occurred during that period. As it happened, S&P 500 profit margins would peak at 8.7% by January 2001, falling by a quarter over the following year. An economic recession would follow later that year. From its peak, the S&P 500 Index would fall nearly 50% by October 2002, as expectations for growth and profitability were reset.

How far and how long periods of “all in” expectations last is only known with hindsight. And it’s impossible to know how optimistic investors might become about the prospects for artificial intelligence. But when looking at current estimates for S&P 500 Index revenues and earnings for the next few years, it can be said with confidence that the all-in phase is already here. Now that we’re in the middle of second-quarter earnings announcements, it’s a good time to highlight some of these expectations.

Before looking at the expectations embedded into earnings estimates, it’s fair to ask: do estimates even matter to stock prices? The relationship between earnings and stock prices over time has been variable. There are periods in history where the correlation between the two would suggest that there’s no connection between the direction of earnings and the changes in stock prices.

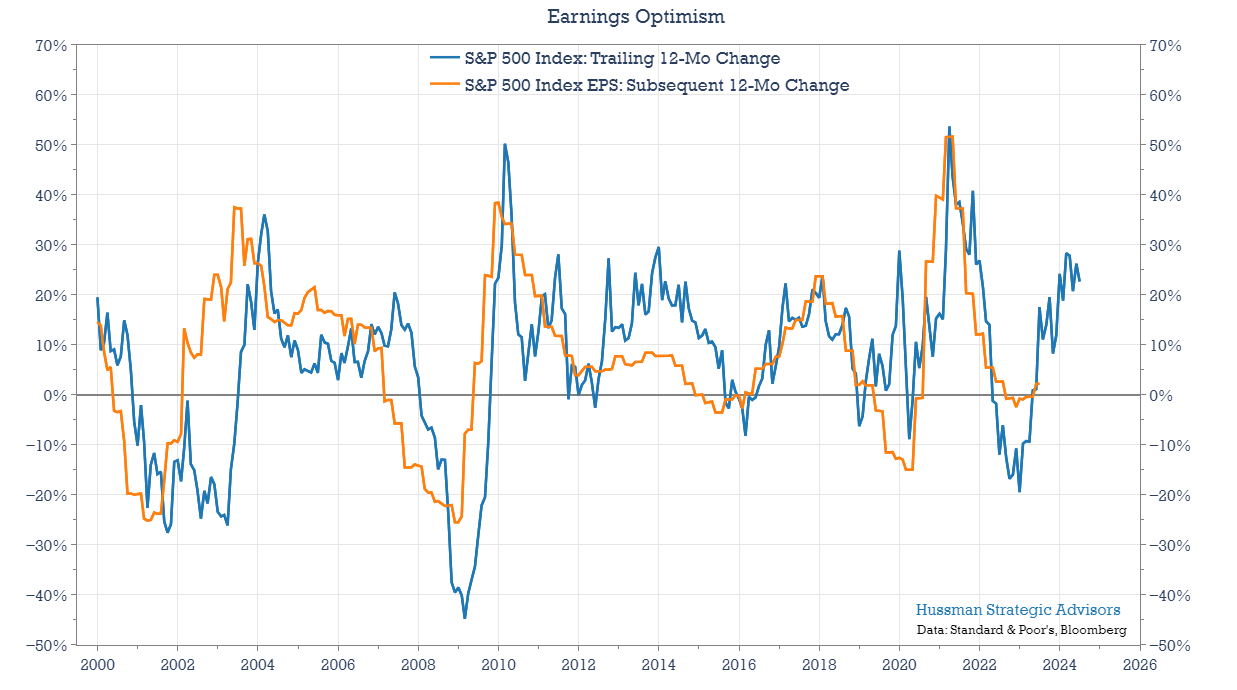

In 2000, the rolling correlation of earnings and stocks prices was actually strongly negative during a stock market bubble that disconnected price from fundamentals. Earlier, in the 1970’s and 1980’s, the relationship was positive, but not particularly strong. During the last 25 years, the relationship between the two has been clearer. You can see the relationship between the two by comparing changes in the S&P 500 Index and earnings projected by Wall Street analysts. Similarly, you can see it comparing changes in the S&P 500 and changes in index earnings over the following 12 months. The graph below shows this relationship in recent decades. The blue line shows the year-over-year change in the S&P 500 Index. The orange line shows the change in S&P 500 earnings over the following 12 months.

Figure 1. Earnings Optimism

The relationship isn’t perfect, but in recent decades, investors have generally pushed prices up in anticipation of higher earnings, and have backed away from a bullish stance when earnings growth is expected to moderate or decelerate. There is one clear miss – when the market raced ahead in 2012 and 2013 and subsequent earnings growth was more modest. In that instance, the market would end up not making any progress over the next 2 years, breaking out of its trading range only when expected earnings turned up in 2016 and 2017. At the peak of the next two spikes in earnings growth – in 2019 and 2022 – the 12-month change in stock prices and the subsequent 12-month change in earnings were well-matched.

For this same relationship to hold, index earnings would need to grow a lot over the coming year. In fact, they would need to grow at a rate that is more than double current forecasts. S&P 500 Index earnings are expected to end the year at $245, according to Bloomberg estimates. Next year they are expected to jump to $278, and then to $302 in 2026. That’s 2024 growth of about 9.7%, then 13.7%, and then 8.6%. Based on the relationship between prices and subsequent earnings in recent decades, either earnings are going to come in at more than twice the forecasted growth rate over the coming year, or stocks have moved far ahead of earnings the last few months.

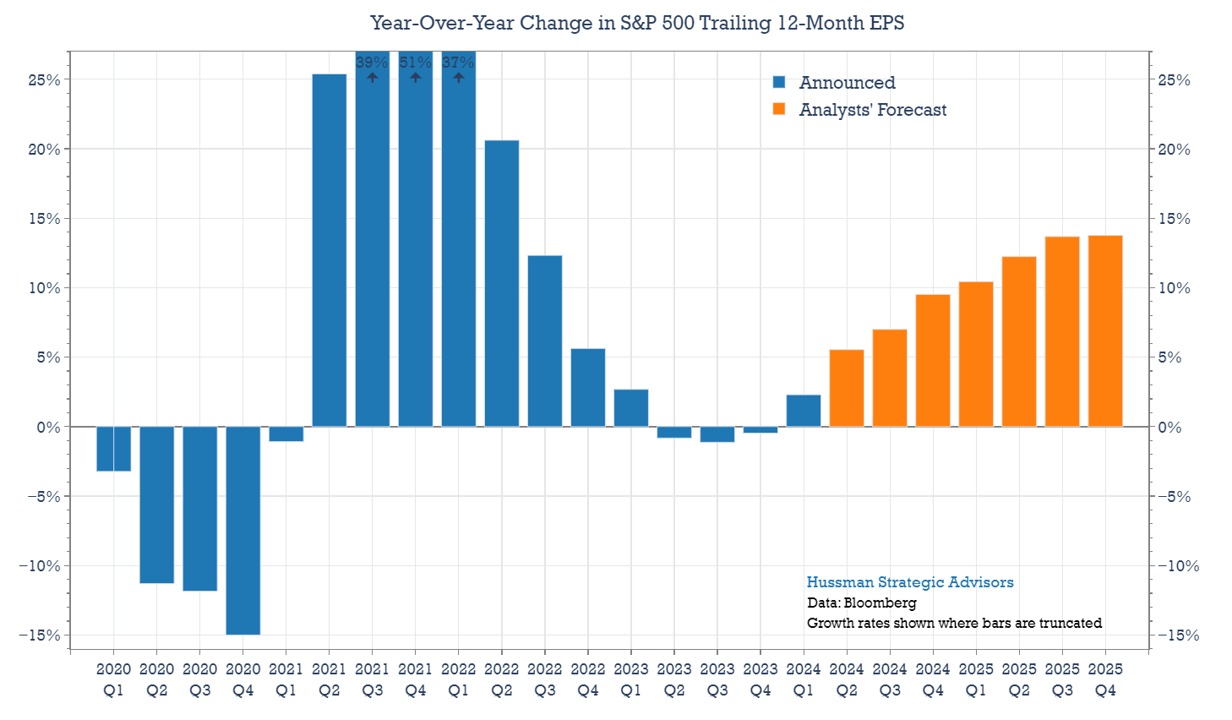

The next chart shows recent earnings growth alongside analysts’ forecast through the end of next year. It illustrates a consistent, stepwise increase in projected growth over the next 18 months. By the end of next year, analysts anticipate earnings per share will have grown by 13.7% year-over-year.

Figure 2. Year-Over-Year Change in S&P 500 Trailing 12-Month EPS

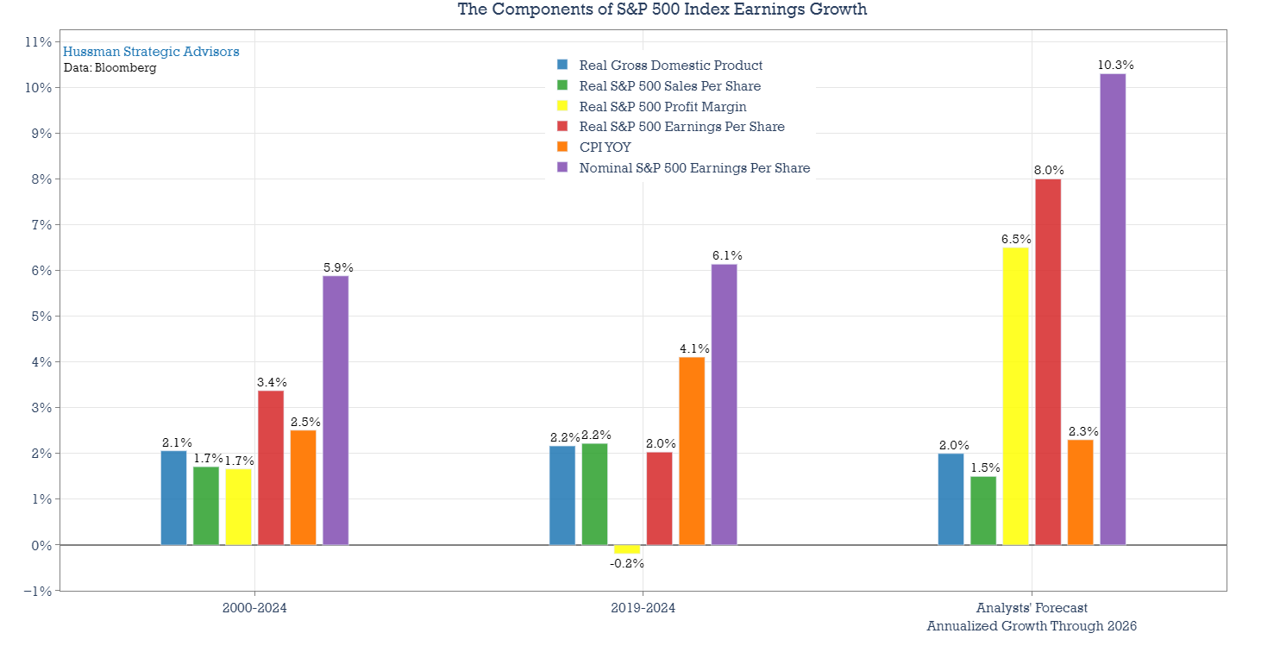

To put current expectations for earnings growth into perspective, we need a good benchmark for long-term earnings growth. How fast do earnings typically grow over extended periods? What drives this growth? How much is attributable to real growth, inflation, and profit margin expansion? The graph below breaks annualized earnings growth into several components, specifically, real sales growth, inflation, and margin expansion. The growth rates are grouped into three distinct time periods. The first two sets of bars represent component growth rates over the past 24 years and the past five years, respectively. The final set shows analysts’ forecasts for each component through 2026.

To provide some general economic context, the blue bars show the annualized growth rates of real GDP. The other bars show various components of overall earnings growth: The green bars show the annualized growth rates of real sales per share. The yellow bars show the annualized change in the S&P 500 Index profit margin (using net profits). Growth in real sales plus growth in profit margins is equal to growth in real index earnings per share, shown as red bars. The orange bars reflect the annualized changes in inflation during each period. Finally, the purple bars show the growth rates of nominal index earnings per share (real earnings growth plus inflation)

There are a few notable characteristics to highlight from the first set of bars. First, over extended periods of time the growth rates in real sales of S&P 500 companies and real GDP are roughly the same. Aside from slight variations, the economy and S&P 500 Index sales can be expected to grow in tandem. Second, profit margin expansion was a significant component of earnings growth over the past 24 years, contributing half of the growth in real earnings during this period. Combined with a modest inflation rate of 2.5%, nominal earnings grew at a rate of 5.9% annually over those 24 years. (Log changes are used in this decomposition of nominal earnings growth to take advantage of their additive properties.)

The second set of bars also has some interesting characteristics. Nominal earnings growth (in purple) over the past five years nearly matches the growth rate since 2000. Earnings grew 6.1% versus 5.9% during the longer period. However, the composition of this growth differed significantly. Real sales growth was similar in both periods, at 2.2% and 1.7%, respectively. But over the past five years, margin growth did not contribute positively to earnings growth. In fact, slightly lower margins created a minor drag. Without margin expansion, real earnings grew by just 2%, compared to 3.4% over the longer period. What filled the gap to reach annual nominal EPS growth of 6.1%? Much higher inflation. The CPI expanded at 4.1% annually over the last five years compared to 2.5% over the longer period.

Figure 3. The Components of S&P 500 Index Earnings Growth

The last set of bars show analysts’ forecasts for annualized changes through 2026. Here, we’re using forecasts for just a couple of years, and over short periods of time earnings growth can be volatile in both directions. So earnings could certainly grow at 10-11% a year during this period. But it’s important to notice the composition of that expected growth. Real sales are forecasted to grow annually by 1.5%, aligning closely with the growth in real sales observed over the last 24 years. The CPI Index is expected to average 2.3% annually, which is consistent with longer term inflation rates. To get to 10.3% overall growth in earnings then, significant help from margin expansion is necessary. And when we back out expected profitability – we can see that earnings will need margin expansion of 6.5% annually.

This rate of margin expansion would be nearly four times the expansion observed since 2000, a period already favorably influenced by consistently declining interest rates. The heady optimism in forecasted earnings is hiding in these aggressive expectations for profit margins. With profit margins being the crucial driver of anticipated earnings growth, any shortfall in this area would significantly impact the overall growth rate.

How likely is it that these profit margins will be achieved? The answer depends partly on whether the factors that have driven margins higher in recent decades can be expected to continue, and partly on more cyclical factors like economic expansion and recession.

As John Hussman discussed in Universal Capitulation and No Margin of Safety, corporate profit margins based on earnings before interest and taxes (EBIT) have not changed significantly in 75 years. The increase in profit margins has been driven mainly by lower taxes, particularly before about 1981, and by lower interest costs due to progressively falling interest rates since 1981.

During the past 25 years, S&P 500 Index net profit margins have increased at about 3 times the pace of margins before interest and taxes. Continually lower interest rates explain much of this faster improvement in profit margins. By 2020, when the 10-year Treasury bond yield hit a record low of 0.5% and Baa corporate yields reached just 3.1%, this dynamic had run its course. The longer interest rates remain elevated, the more interest expenses will act as a headwind to better profit margins, rather than the tailwind they have been for decades.

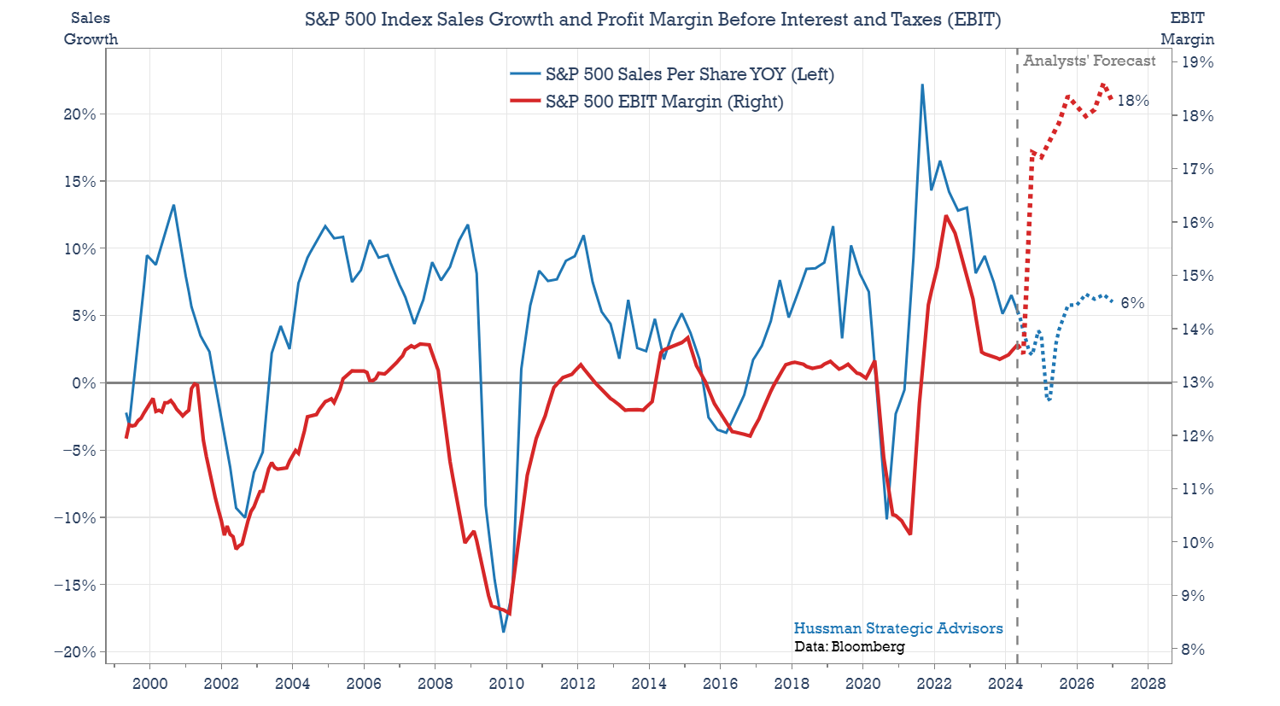

The second component of profit margin variability results from cyclical forces. During periods of high nominal economic growth, especially when labor costs don’t immediately scale with new sales, profit margins tend to rise. Conversely, during economic slowdowns, profit margins tend to fall. These characteristics of margins are illustrated in the chart below. The solid red line represents the S&P 500 Index’s profit margin, before interest and taxes (EBIT divided by sales). We’ll use EBIT margins to isolate the cyclical impacts from the secular ones. Prior to the period shown — during the 1990’s — there was a secular rise in index-level margins, increasing from about 9.5% to almost 13%. However, since then, margins have mostly plateaued (with a slight positive slope).

In 2001, EBIT margins reached 13%, and twenty years later, in 2021, they were still at around 13%. However, margins were not consistent. They fluctuated partly with nominal sales growth, which is influenced by both economic growth and inflation.

Figure 4. Sales Growth, Inflation, and S&P 500 Index Profit Margin

The dotted portions of the lines represent analysts’ estimates for the next two years. Sales growth is expected to be marginally positive over the coming year, then increase to about 6% year-over-year by the end of 2026. This equates to an annualized growth rate of approximately 4% through the entire period, which aligns with the long-term average sales growth rate of 4.2%. EBIT margins are where analysts are penciling in a break with history. Margins are expected to jump from the current 14% to 18% next year, and then remain at that high plateau.

If analysts’ forecasts are achieved, margins would surpass their previous peak of 16% in 2022. But notice the underlying driver of the 2022 peak margin levels: nominal sales growth was more than 20% on a year-over-year basis (boosted partly by 9% inflation). The extraordinary growth rates in sales were fueled by the economy’s reopening and the government’s fiscal response to COVID-19. This context highlights how remarkable current forecasts are, projecting margins 2 percentage points higher than those peak levels with only about one-third of the expected sales growth.

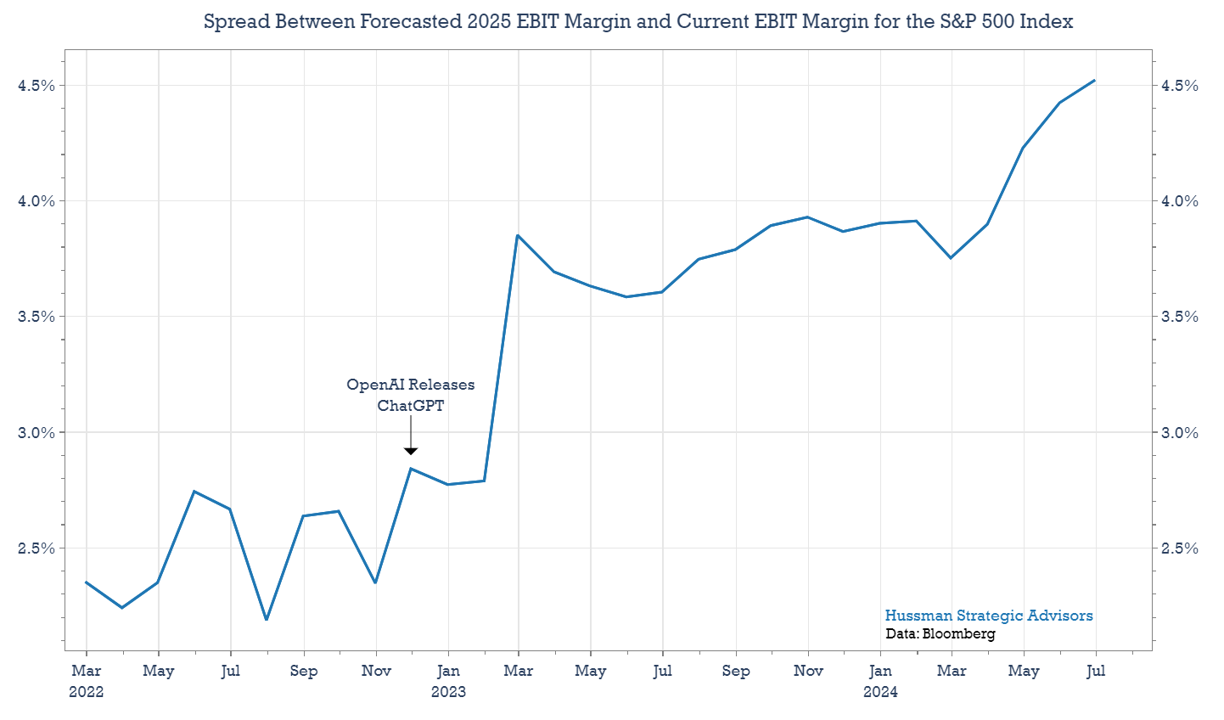

The chart above presents analysts’ projected profit margins for this year and the next. The chart below shows the upward shift in these expectations over the past two years. It highlights the spread between analysts’ anticipated profit margins for 2025 and current margins. Clearly, OpenAI’s release of ChatGPT – and discussions about the underlying technology – has been a significant catalyst for these much higher profitability expectations.

Figure 5. Spread Between Projected 2025 and Current EBIT Margin for the S&P 500 Index

The Center Pole of the Valuation Circus Tent

The data we’ve looked at so far suggests that expected earnings growth is important to investors, and the optimistic projections for profit margins embedded within those expectations could lead to earnings missing estimates in the coming years. However, this isn’t the most important reason to monitor the trend in profit margins over the next few quarters.

If earnings miss estimates by a few dollars next year, that probably wouldn’t be a major event. The larger concern, by far, is that the persistent increase in profit margins in recent decades — and particularly the forecasts for continued expansion — has been a key driver of the current elevated stock market valuations. If the widely held belief that public companies will perpetually become more profitable begins to falter, the steep valuation premium that has been priced into U.S. large-cap stocks over the past decade may evaporate.

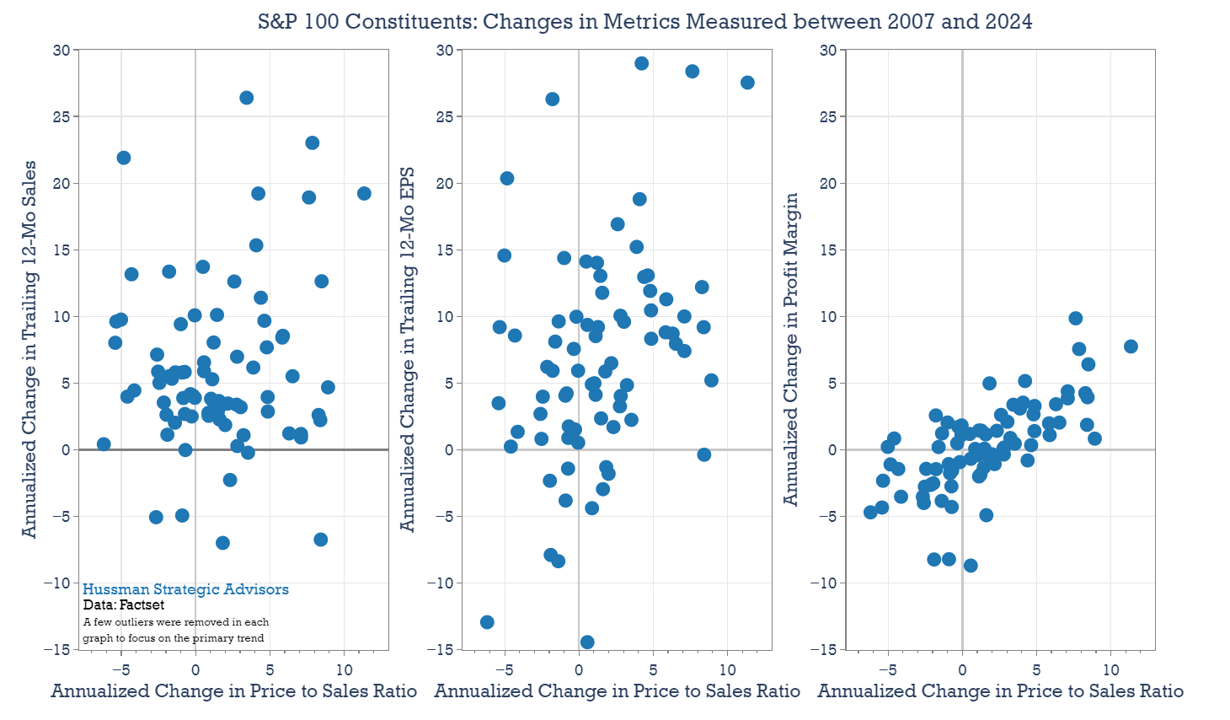

It may seem like an overstatement to credit higher margins as a primary catalyst for the rise in valuation multiples during the recent market advance. But the relationship between the change in valuation multiples and the change in profit margins at the company level has been surprisingly strong. In the graph below, there are three scatter charts that contain data for the companies in the S&P 100 Index, which are generally the largest stocks within the S&P 500 Index. Each graph shares the same horizontal axis, which is the annualized change in the price to sales ratio between 2007 and 2024. In the first chart, the vertical axis is the annualized change in sales. In the middle chart, the vertical axis is the annualized change in earnings per share. In the last chart, the vertical axis is the annualized change in profit margins.

Figure 6. S&P 100 Constituents: Changes in Metrics between 2007 and 2024

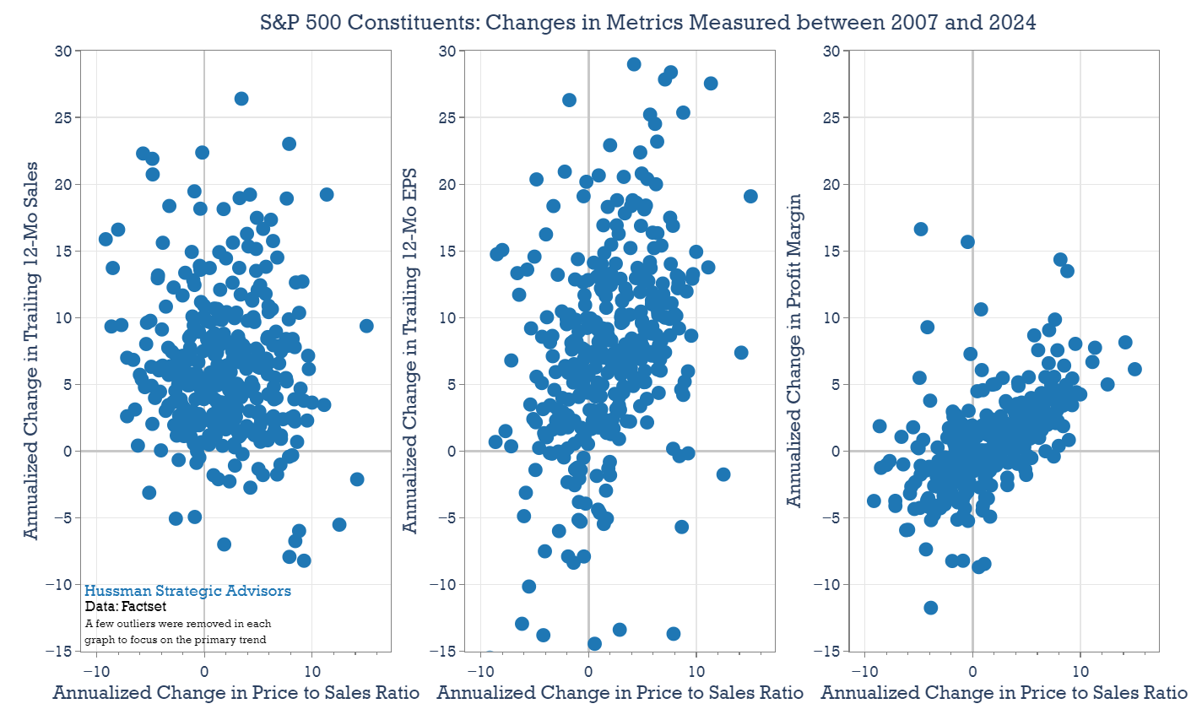

Here is what this same analysis looks like for the companies in the S&P 500 Index.

Figure 7. S&P 500 Constituents: Changes in Metrics between 2007 and 2024

For the bulk of these companies, there’s been essentially no relationship between sales growth and higher valuations during the period from 2007 and 2024. There’s been a slightly stronger relationship with earnings growth. But that is a by-product of the much stronger relationship with the change in profit margins.

This reliance of high valuation multiples on expanding profit margins is probably one of the most underappreciated risks in the market right now. Not only are investors paying record valuation multiples that rely on record profit margins, but the rise in market valuations has been much more tightly linked to those elevated margins – and expectations for even higher margins next year and the year after – than investors may realize. Record price to sales multiples and expectations for inexorably rising profit margins are tied at the hip.

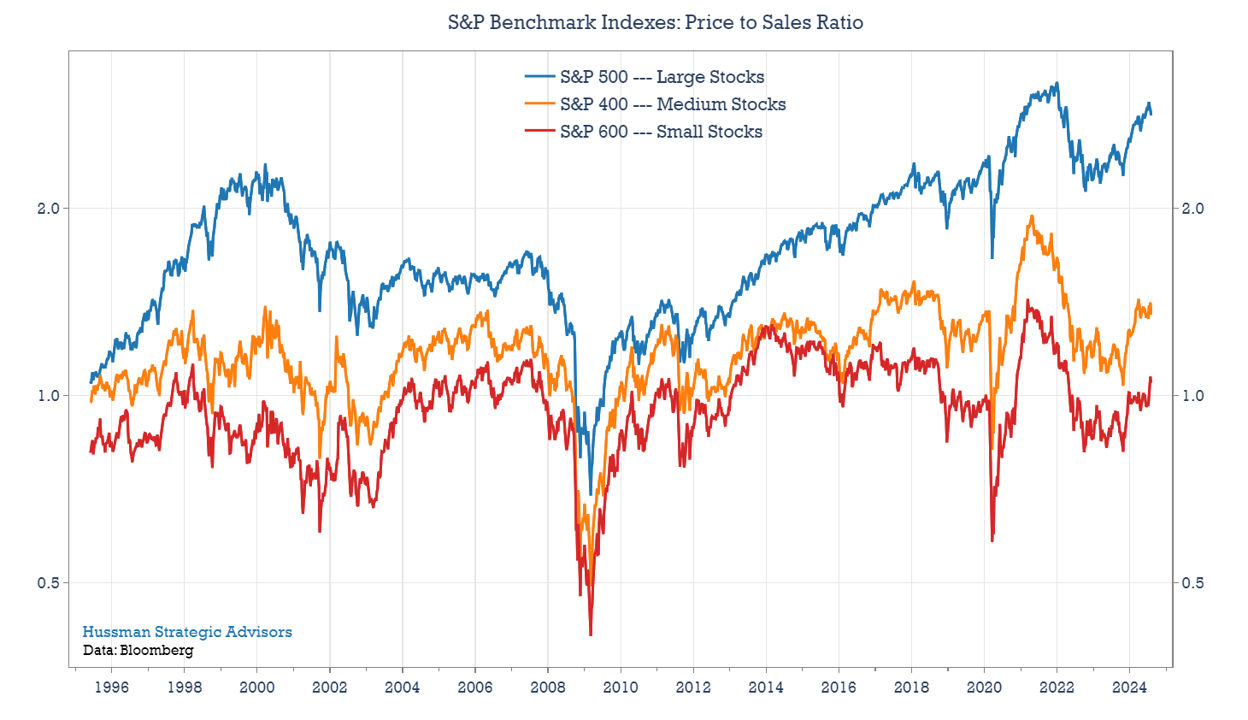

Let’s look at each one of these components of risk – the higher multiples and higher profit margin expectations – separately. Focusing on the price multiples of different sub-groups within the market is crucial, as relative valuations have become increasingly uneven and divergent since the early-2022 market peak.

The chart below shows the price to sales ratio for the S&P 500, the S&P 400 (medium-sized companies), and the S&P 600 (small companies) indexes. In late 2021, the valuation ratios for all three indexes were at all-time highs. Two and half years later, large cap stocks are just as expensive. The price to sales ratio of the S&P 500 is sitting at the 98th percentile of history for the period shown. Contrast that with the S&P 400 Index, which is at the 89th percentile, and the S&P 600 Index, which is at only the 56th percentile. The current difference between the price to sales ratio for the large and small indexes is currently 1.8 points, a record spread between the two.

Figure 8. Price to Sales Ratio: S&P Benchmark Indexes

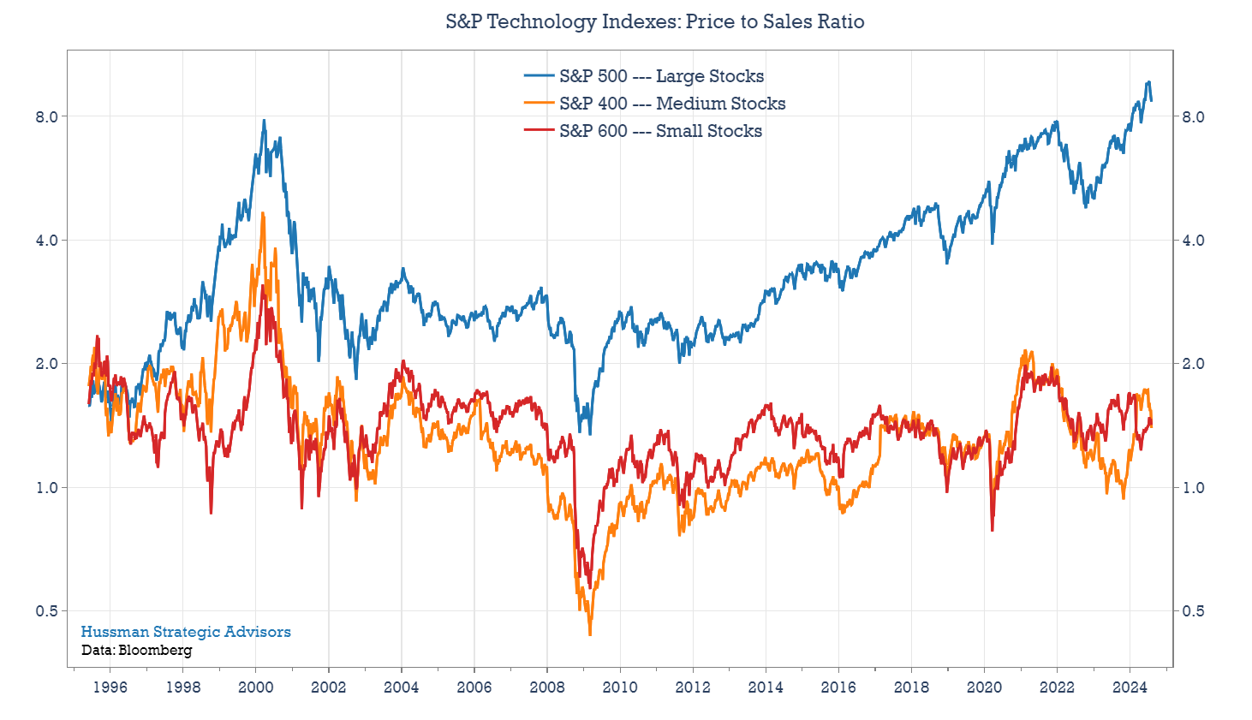

This divergence in valuations has been particularly pronounced within the technology sector. The chart below highlights the valuation differences between various sizes of technology stocks. The S&P 500 Technology Index is currently trading at 8.7 times sales, just off an all-time high. In contrast, the S&P 400 and S&P 600 technology indexes are not as overvalued relative to their historical averages. The valuations of mid-cap technology stocks are at the 72th percentile (having rallied this year as investors look beyond the more obvious large-cap artificial intelligence plays). The valuations of small-cap technology stocks are at the 62th percentile. At the recent market peak, there was an 8-point difference in the price to sales ratio between large and small technology companies. For 17 years, through the end of 2018, this spread averaged just 1.5. Today, an extraordinary premium is being placed on large-cap technology stocks, even relative to other technology stocks.

Figure 9. Price to Sales Ratio: S&P Technology Indexes

The second risk — elevated profit margins and expected profit margins — is more difficult to summarize in a single metric. We know that the “secular” increase in profit margins was largely driven by falling interest costs in recent decades, and that despite a wave of corporate refinancing that temporarily locked in record low rates in 2020 and 2021, that driver of profit margin expansion is largely behind us. Meanwhile, several more questions are worth considering. What part of the margin increase in recent years has been driven by cyclical forces rather than secular ones? How much of the increase reflected temporary pandemic subsidies that directly and indirectly boosted corporate revenues and earnings. How much of the increase resulted from one-time adjustments to business models or changes in work dynamics due to COVID-19 (in which case further margin expansion shouldn’t be assumed)? Finally, how much profitability is at risk if new pressures on margins materialize, either from new regulations, new dynamics of competition, or a slowing economy?

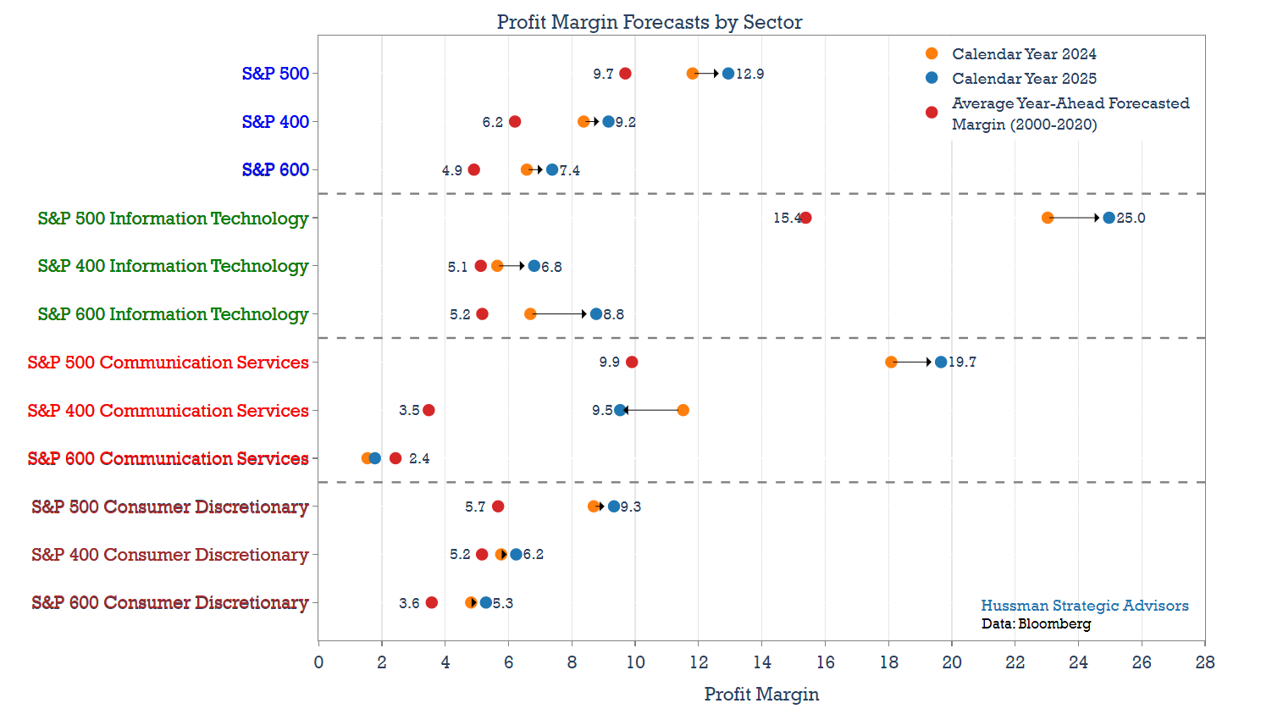

On that last question, the chart below highlights how far current forecasts are from longer-term average levels, and also the pace at which margins are expected to keep rising. Profit margins are shown for each overall index and three key sectors of each index. For each benchmark, expected profit margins for this year (in orange) and next year (in blue) are shown.

Additionally, I’ve included the average year-ahead forecasts for the 20-year period ending in 2020. This data provides insight into the improvements already achieved in profit margins but it also underscores the potential risk if these improvements aren’t permanent. The amount of risk at hand can be estimated by the amount of spread between the red dots and the blue dots. The data also reflects the high level of optimism regarding these companies’ continued profitability over the next couple of years. A significant portion of their valuation likely hinges on these optimistic margin projections.

Figure 10. Sector Profit Margin Projections

The Performance of Highly Profitable Companies

There is an irony in investors driving up the prices of the most profitable stocks to record-high valuations. That’s because historically, this strategy has an unusual characteristic: the most profitable companies often do not end up being the best performing stocks.

When you study the performance of single-characteristic long-only portfolios – like stocks ranked only by price to book, or dividend yield, or momentum – they typically have two features. The first feature is that the highest ranked stocks by these characteristics – the cheapest companies or the stocks with the strongest momentum – tend to have the highest return when compared to the remaining stocks based on the same characteristic. The second feature is that equal-weighted versions of these strategies tend to do better than market-cap weighted versions. There are exceptions, but for the most popular single-characteristic portfolios like different variations of value and momentum, it’s true. (All of the results in this section rely on Ken French’s factor portfolio returns data.)

Portfolios of the most profitable stocks lack both of these features. First, market-cap weighted versions tend to outperform equal-weighted versions. And second, equal-weighted portfolios made up of the most highly profitable companies tend to underperform companies with lower levels of profitability.

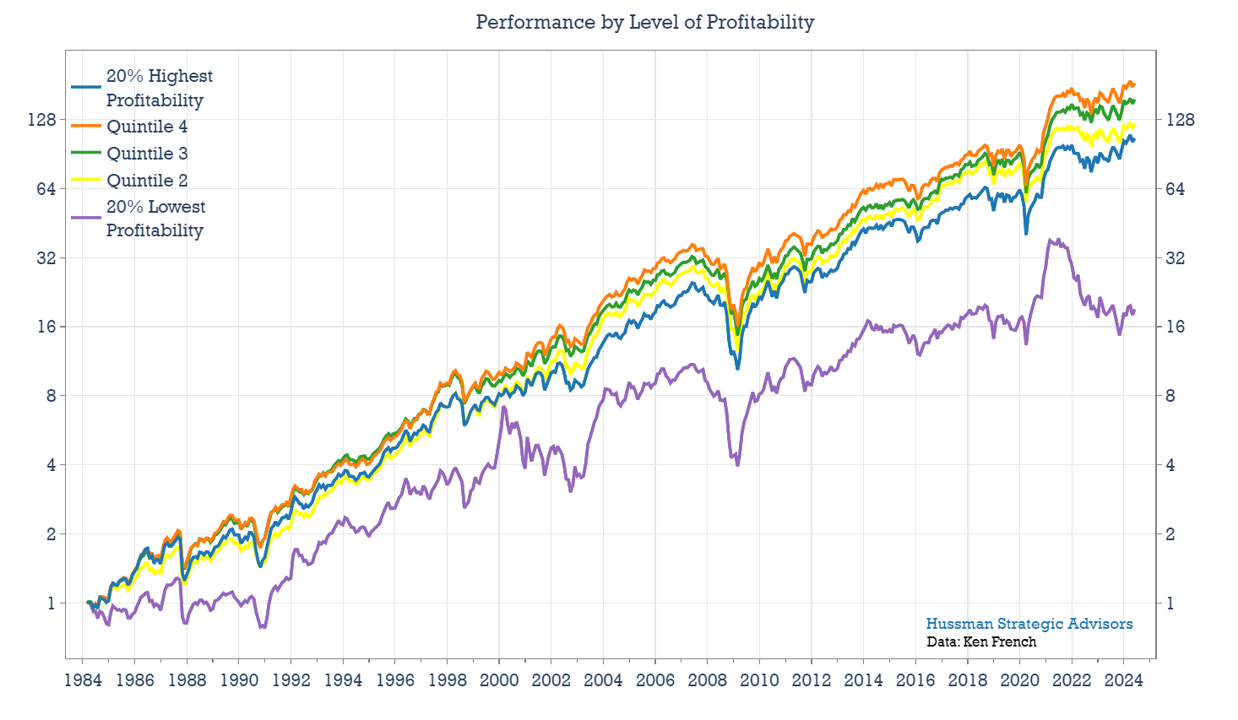

In the chart below, I’ve plotted the returns of equal-weighted portfolios based on varying levels of profitability (defined as sales minus cost of goods sold, interest expense, and selling, general and administrative expenses divided by book equity). These portfolios include the top 20% of stocks ranked by profitability, the next 20%, and so on, down to the bottom fifth.

The results show that holding the top 20% of the most profitable stocks has not been the best-performing strategy over the last four decades. It’s not the second or third best strategy either. Surprisingly, it’s the fourth best. Only the portfolio of the bottom 20% of stocks – which typically holds companies that are characterized by significant losses, high debt, slow growth, and low credit ratings – performs worse. And this is a consistent pattern. Compare these five portfolios over the past 10, 20, 30, and as shown, 40 years, and you end up with the same result: the most profitable companies do not end up being the best-performing portfolio.

Figure 11. Performance by Level of Profitability

Why is this the case? Why wouldn’t the most profitable companies outperform less profitable ones, similar to how cheaper companies tend to outperform more expensive ones and stocks with greater momentum typically outperform those with less momentum? The primary reason is that investors tend to overpay for profitability.

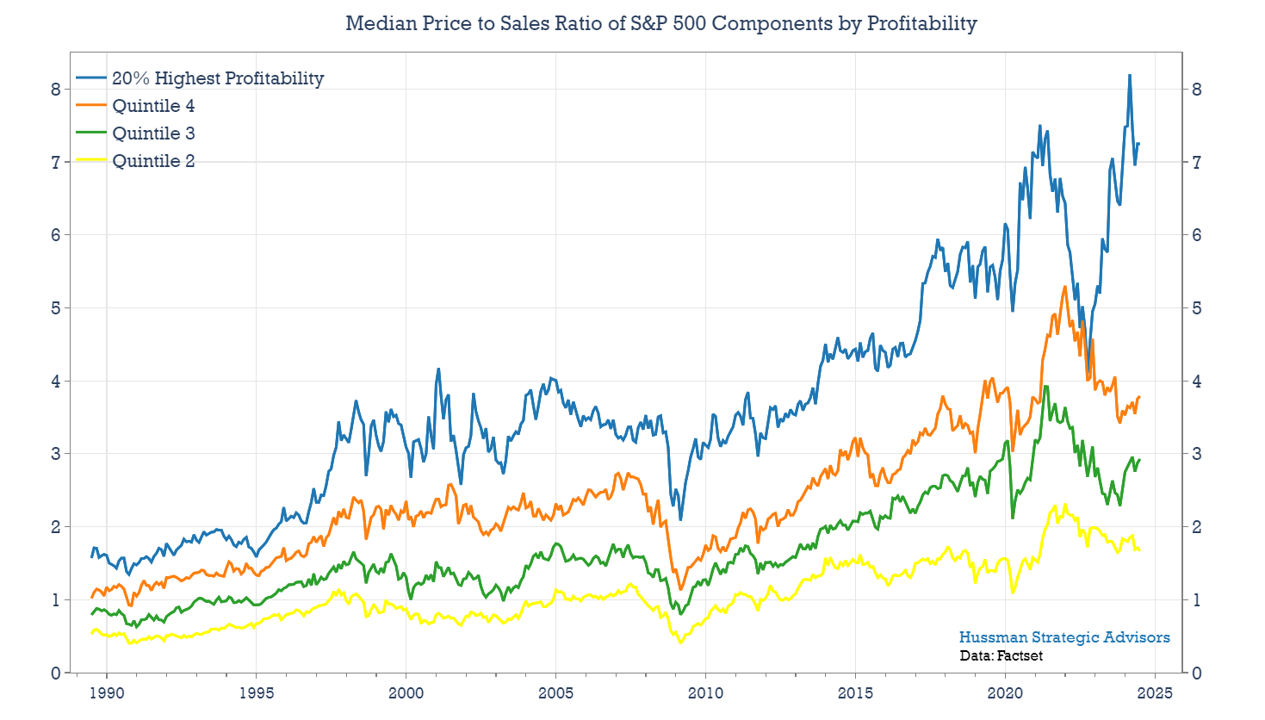

Currently, investors are paying significantly higher multiples for profitable stocks relative to the rest of the market. In the chart below, each line represents the median price to sales ratio for the top four quintiles over the past 25 years. The blue line shows the median price to sales ratio for the most profitable stocks, while the orange, green, and yellow lines represent the median ratios for the second, third, and fourth quintiles, respectively.

At their peak levels earlier this year, the most profitable companies were trading at the highest price to sales ratio seen in the past 25 years, and likely the highest in history. Also, while the price to sales ratio multiples for all of the groups have generally risen over the last 15 years, it has been the most pronounced for the most profitable companies the last couple of years. The average spread over the time period shown between the portfolio of companies with the highest profitability and the average of the remaining quintiles (the second, third, and fourth) is 3. It’s currently 4.3.

Figure 12. Median Price to Sales Ratio by Profitability

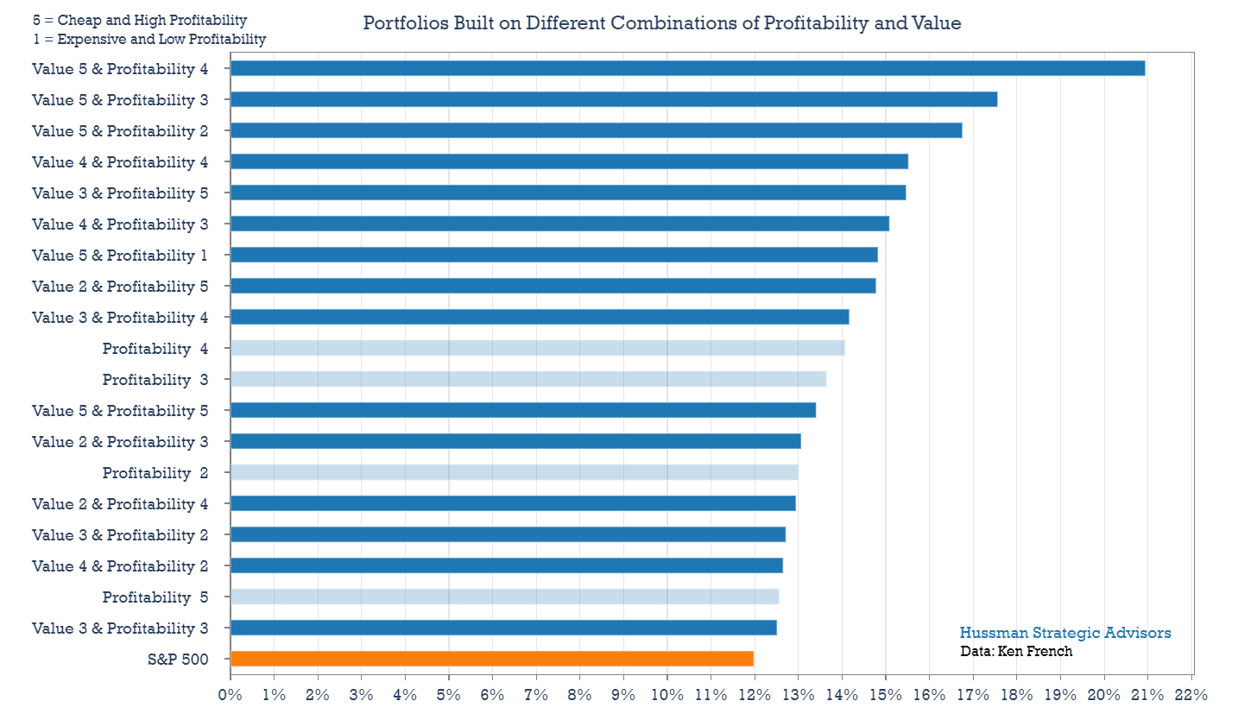

The best way to avoid overpaying for profitable stocks is to add value criteria to the selection process. To support this idea, we can look at a broad set of historical performance results. I’ve calculated the returns of 30 portfolios over the last 40 years, all ranked by either profitability or both profitability and valuation. Five of the portfolios are ranked by just profitability (the same portfolios that were used to plot the returns above). The other 25 portfolios are at the intersection of portfolios formed on value and on profitability.

The results are shown in the graph below, and include only the portfolios that outperformed the S&P 500 Index over the time period. The number 5 is used for the quintiles with the highest rank. For example, Value 5 includes the cheapest stocks, and Value 1 includes the most expensive stocks (ranked by price to book value). Profitability 5 is the portfolio of the stocks with the highest profitability, and Profitability 1 holds the companies with the lowest levels of profitability.

What the results suggest is that having some exposure to value is almost always warranted. It typically doesn’t pay to chase profitable stocks at any price.

Figure 13. Portfolios Built on Combinations of Profitability and Value

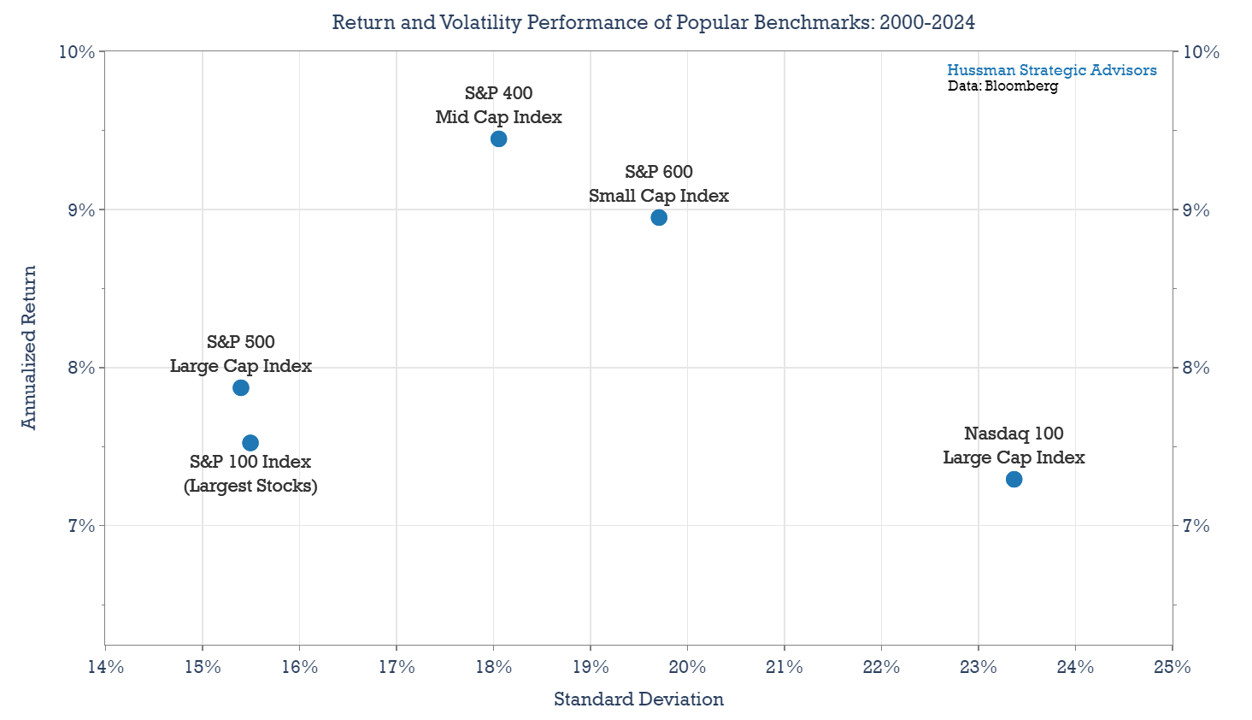

This may be an opportune time to reassess the risks in your portfolio. At the beginning of this piece, I noted that the “all-in” moment for peak expected profit margins occurred in 2000 when expectations rose by 4 percentage points. During that period, the Shiller cyclically adjusted P/E (CAPE) hit a record 45, more than double its level from four years earlier. This was a time of peak price multiples on peak expected margins, with speculation heavily concentrated in the largest stocks, particularly tech stocks. Many of the characteristics of today’s market resemble those of that period. It’s important to consider the impact on long-term returns that typically follow such periods.

The chart below shows the annualized returns and volatility of all major indexes since the market peak in 2000. Twenty-four years later, the stocks that were priced for perfection still lag behind those that had more modest valuations and embedded expectations at the time. Recovering from the losses incurred by buying stocks at peak multiples on peak profit margins is extremely challenging, even over very long periods.

Figure 14: Return and Volatility Performance of Popular Benchmarks

Seth Klarmin famously said that the root of all financial bubbles is a good idea carried to excess. By the time this market cycle is complete, investors may find that the expectation of inexorably rising profit margins was the idea that was carried too far. Missing profit margin expectations next year could pose risks beyond just lower reported earnings. The greater risk is that progressively rising profitability has been the primary catalyst driving market valuations higher this cycle. If this central pillar gets knocked out, the premium valuations of U.S. large-cap stocks could be left with little support.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse.

Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Allocation Fund, as well as Fund reports and other information, are available by clicking “The Funds” menu button from any page of this website.

Estimates of prospective return and risk for equities, bonds, and other financial markets are forward-looking statements based the analysis and reasonable beliefs of Hussman Strategic Advisors. They are not a guarantee of future performance, and are not indicative of the prospective returns of any of the Hussman Funds. Actual returns may differ substantially from the estimates provided. Estimates of prospective long-term returns for the S&P 500 reflect our standard valuation methodology, focusing on the relationship between current market prices and earnings, dividends and other fundamentals, adjusted for variability over the economic cycle. Further details relating to MarketCap/GVA (the ratio of nonfinancial market capitalization to gross-value added, including estimated foreign revenues) and our Margin-Adjusted P/E (MAPE) can be found in the Market Comment Archive under the Knowledge Center tab of this website. MarketCap/GVA: Hussman 05/18/15. MAPE: Hussman 05/05/14, Hussman 09/04/17.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All