The 2019 Geopolitical Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs is our custom, we close out the current year with our geopolitical outlook for the next one. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape in the upcoming year. It is not designed to be exhaustive, but rather it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

Issue #1: China

China is trying to navigate the transition from being a high growth/low cost nation to a normal developed one. Since the industrial revolution the world has seen a series of nations accomplish this transition. In this phase, the economy is dominated by investment; the nation has an industrial base to build and thus has to find funds to pay for this project.

There have been two models to fund this development. The first involves attracting foreign money to the economy to pay for the investment. The foreign investor risks malinvestment or expropriation at the hands of the developing nation in hopes of high return. At the same time, the developing nation can’t get the reputation of “stiffing” foreign investors, otherwise the terms of investment will become too onerous or the flows will simply stop.

The second model involves generating the funds internally by suppressing consumption. This suppression can be accomplished in a myriad of ways. The currency is usually undervalued to raise the price of imports to reduce consumption. Taxes are often placed on consumption as well. Household deposit rates are usually below the rate of inflation to force higher saving,1 and there are restrictions on the capital account to prevent funds from leaving the country. Under this model, it is also normal to have a modest, or non-existent, social safety net to further boost precautionary savings.

The weakness of the first model is that it is dependent on foreign investors. If foreign investors become jaded on investing in the high growth/low cost country, then the model fails. The weakness of the second model is that, at some point, the industrial capacity exceeds domestic demand. If the model is to be maintained, new sources of consumption must be found. In nearly all cases, that source is exports.

Britain’s development was mostly internally generated. The U.S. relied on foreign investors. Development in Germany and Japan, prior to WWII, was internally generated. Since WWII, all development has come through the second model because nations could rely on the U.S., the provider of the reserve currency, to play the role of importer of last resort. So, since WWII, Germany, Japan, the Asian tigers and China have all followed the internal model that relies on export promotion. The development model worked best so long as the U.S. fulfilled the role of importer of last resort.

No nation remains in the high growth/low cost stage indefinitely. At some point, internal costs rise and foreign nations push back against losing market share to the high growth/low cost nation. In fact, under a gold standard, the high growth/low cost nation, which tends to run trade surpluses, accumulates gold and faces rising inflation. The increase in inflation makes exports less competitive and undermines growth. Thus, under a gold standard, the high growth/low cost nation is almost “naturally” forced to adjust.

Without a gold standard, the high growth/low cost nation can artificially hold down its exchange rate to keep exports competitive. However, the high growth/low cost nation must eventually transition into a normal developed economy. No nation in history has made this transition in a seamless manner.

At the point of transition, the high growth/ low cost nation finds itself with excess capacity. And, especially with the internal development model, that capacity is usually funded with debt. To make the transition, the country has to adjust the capacity to a lower level of demand or it must find new areas of demand to absorb that capacity. There have generally been four methods used to make this transition:

Debt restructuring: The industrial infrastructure that has been built is an asset with a liability attached. Once it becomes clear that the asset has less value, the debt needs to be restructured. This adjustment can be done quickly or slowly. When the U.S. faced this situation, it made the change quickly—the adjustment is known as the Great Depression. A slow adjustment has occurred over the last three decades in Japan. Clearly, this outcome is painful, but necessary.

There is another element to debt restructuring. During a debt workout, the bondholder sometimes becomes an equity holder in restructuring. Someone needs to absorb the losses of the asset so that a new owner can take the depreciated asset and make it economically viable again. If the asset is transferred to a broader group, the losses can be spread out and the asset may have more time to recover. Development usually occurs in the hands of the few, entrepreneurs with the foresight and drive to build industrial capacity. However, restructuring can shift that asset to the many, either in the form of direct ownership or by policies that shift economic resources to a wider group of households.

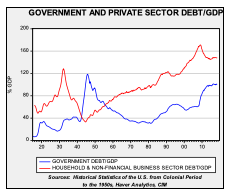

To show how this process worked in the U.S., note the shift in private and public sector debt during and after the Great Depression.

The drop in private sector debt shows the impact of deleveraging but the war allowed the effective ownership to be broadened. From a financial standpoint, WWII was a massive private/public sector debt swap that allowed for broader ownership of private sector assets. In addition, high marginal tax rates facilitated the shift of incomes from capital to labor. This action completed the restructuring necessary for the U.S. to transition from being the high growth/low cost producer to a normal nation. In other words, domestic consumption, and not exports, became the primary source of demand that absorbed industrial capacity.

Mass mobilization war: During periods of war, the excess capacity is either absorbed by the war effort or destroyed during the conflict. This is how Japan and Germany resolved their excess capacity situations before WWII. The U.S. also used its excess capacity to supply goods for the war effort. The heavy government intervention in the economy, as noted above, supported the facilitation of assets to a broader base of households, supporting consumption that was able to utilize the production capabilities.

Imperialism: Acquiring colonies creates a compliant outlet for exports. The colony can be forced to buy the excess production of the restructuring high growth/low cost producer. This was the favored method of absorbing excess capacity among European nations before WWII. However, it is still used today; we would argue that the Eurozone is essentially a German colony that is forced to absorb excess German capacity.

Value chain advancement: Usually, the high growth/low cost nation is a producer of a large amount of low-value goods. If this nation can shift its industrial base to more sophisticated goods then the revenue gained from these products can be used to restructure the economy. In other words, the higher value products replace the lower value goods in the economy and allow the excess capacity to be transformed.

In reality, nations making the transformation from high growth/low cost use more than one of these methods. For example, Germany, which began this process in the 1970s (after starting over following WWII), used value chain advancement (Volkswagens to BMWs) and imperialism. Britain initially used imperialism and mass mobilization war. Eventually, it restructured by shifting assets to a broader set of households through the nationalization of major industries after WWII. On the other hand, Japan has failed to make this shift to broaden the benefits of its base of productive assets and thus has suffered from over thirty years of economic sluggishness.

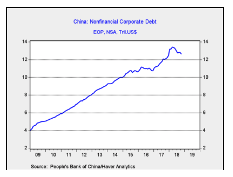

China is rapidly heading to the point where this restructuring needs to occur. Its debt levels are becoming unsustainable and the world is rebelling against taking more of its exports. Although China’s GDP calculation is suspect, conservatively, its total debt/GDP ratio is 237%, with household and non-financial corporate debt at 147% of GDP. Debt levels are high because China is still using investment to drive growth but can’t rely on exports to absorb the excess capacity.

The least disruptive adjustment method from an economic perspective would be to shift excess capacity assets to the household sector. This would lift household wealth and spur consumption, helping absorb the excess capacity currently being used for exports. However, such action would be politically disruptive because high-ranking members of the Communist Party of China (CPC) have been the beneficiaries of the current policy. Although the anti-corruption crackdown might have been used to cow CPC members into accepting this shift, in reality, it appears Chairman Xi deployed the anti-corruption campaign simply to solidify power.

Instead, China appears to be focusing on value chain adjustment (China 2025) and imperialism (the “One Belt, One Road” initiative). However, the Trump administration is putting obstacles in the way of these methods. First, the U.S. is restricting technological transfers which slows value chain adjustment significantly. Second, the U.S. is offering an alternative to joining the one belt, one road program. Given the debt issues that some nations are facing from Chinese “investment,” the U.S. offer looks attractive. In reality, the trade conflict between the U.S. and China is something of a sideshow. The real threats are technology transfer restrictions and impeding foreign investment.

If the U.S. doesn’t allow China to use value chain advancement or imperialism, then China must either choose mass mobilization war or debt restructuring. We strongly doubt China will choose war, although the likelihood probability isn’t zero. Debt restructuring runs the risk, at best, of a massive growth contraction or a long period of stagnation. Either outcome would put the CPC in deep trouble.

China’s transformation is a long-term issue, but the intersection of trade tensions and debt could have an impact in the coming year. Chinese non-financial firms hold about $12 trillion of debt.

What is interesting is that firms have been borrowing in dollars; estimates suggest that firms may be on the hook for $3 trillion of debt in dollars.2 It appears the firms are borrowing in dollars due to lower debt service costs. Dollar bonds were probably attractive to Chinese investors looking to protect themselves from currency depreciation. However, this debt is risky if the CNY depreciates as it would increase debt service costs and raise the odds of default.

The textbook response to tariffs is depreciation; that is part of the reason countries tend to use trade tools other than tariffs because, outside the gold standard, floating exchange rates can quickly adjust to tariffs, making them ineffective. Therefore, it would be expected for China to allow the CNY to weaken in the face of U.S. tariffs. However, Chinese authorities may not have this policy available to them as a sharp depreciation in the CNY might trigger a debt crisis. That is a key risk we will be watching in 2019.

Issue #2: European Politics

There are four areas of concern in Europe. First, Brexit will be heading into its climax in the first half of 2019. There is potential for a “hard Brexit,” a separation from the EU without a trade agreement that would likely lead to a deep downturn in the U.K. economy. It is also possible a new referendum will be held that could return the U.K. to the EU fold, triggering a massive rally in U.K. financial assets. It’s a binary outcome for the most part. We are leaning toward the latter outcome.

Second, Italy is at loggerheads with the EU over budget issues. We expect the parties to come up with a face-saving agreement but the potential exists for challenges to the EU and the Eurozone that could lead to Italy’s exit from both. Odds favor remaining but Italy hasn’t really benefited from being in the single currency and will, at some point, either leave or force liberalization on the Eurozone. Odds are this outcome doesn’t occur in 2019 but the probability is elevated.

Germany is in the midst of a new era as Angela Merkel fades from the political scene. Although Merkel’s preferred candidate, Annegret Kramp-Karrenbauer, was elected to lead the CDU, her margin of victory was narrow and she may not be able to hold power. With centrist parties floundering in Germany, there is the potential for additional elections and a more radical government to take power.

Lastly, France is facing a populist uprising of some note. President Macron has been trying to implement market reforms similar to what the U.S. and U.K. did in the 1980s. He is running into deep opposition from the less affluent countryside and has been forced to retreat. If Macron’s policy path is thwarted, it isn’t clear whether his political movement will survive; if it fails, France could face a populist backlash.

Issue #3: Rising Western Populism

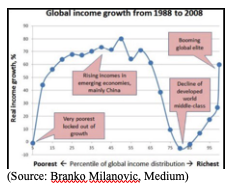

The later chart in this section showing shares of national income offers some insight into the growing anger over inequality.

(Source: Branko Milanovic, Medium)

This chart shows global real income growth in the two-decade period between 1988 and 2008. The developed world middle class did not participate in the global boom.

Populism has two variants, a left-wing version and a right-wing version. The latter tends to be more nationalistic, while the former is more inclusive. Although both versions exist in the political system at all times, populism tends to rise during periods of economic stress and widening income differences. Essentially, populism is a symptom of elite failure—the masses believe the elites are no longer looking out for their interests and are primarily taking care of themselves.

The recent funeral of President George H.W. Bush spawned a series of editorials remarking on the demise of America’s White Anglo-Saxon Protestant (WASP)3 elite that mostly dominated the country during the Cold War. These leaders had a sense of noblesse oblige where leaders believed they were given the right to rule but owed it to the rest of society to do so in a way that at least acknowledged their existence. The WASP leadership was not without flaws; they were often bigots and distrustful of those who didn’t come from their “tribe.” But, they also seemed to understand that they got where they were, at least, in part, from the accident of birth and thus recognized some degree of obligation to the rest in return for their status. Their response to their role was to create a broad path to the middle class that entailed the support of large, concentrated firms and high marginal tax rates that discouraged companies from boosting the incomes of executives.

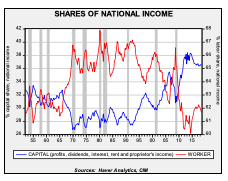

The current elites believe they got where they are on merit alone and thus they owe nothing to anyone.4 Because they earned their privileged status, today’s elites feel no compulsion to help the rest. Especially since the fall of the Soviet Union and the end of the threat of communism, the owners of capital have been improving their situation at the expense of labor. The chart below shows the shares of national income going to capital and labor. Since 1990, the share going to capital has been increasing with each business cycle, while labor’s share has declined.

History shows there are cycles to elite behavior.5 We are currently in a cycle favorable to capital, which we believe started in the late 1970s in response to the inflation crisis of that decade. The rise of populism appears to be a negative response to an elite class that seems to ignore the needs of the masses.

The resolution of this problem will almost certainly be inflationary. Populists of all stripes tend to support increased government spending and regulation to protect jobs. Rising fiscal deficits coupled with regulation and trade interference are a classic recipe for inflation. Although it hasn’t occurred yet, political trends continue to signal that populism is becoming increasingly popular and such policies will probably become more common next year and beyond.

Issue #4: Saudi Succession

The Saudi Royal Family has been in the news following the brutal murder of Jamal Khashoggi in October. Although this incident has created difficulties for Western governments, in reality, no nation is going to completely sever relations over this event. The Kingdom of Saudi Arabia (KSA) is too important to the oil markets and the Middle East to completely end contact.

However, the incident did highlight the problem of succession. The KSA was founded by Ibn Saud, a charismatic sheik who created the modern kingdom. Through military campaigns and intermarriage, Ibn Saud gradually unified the territory on the Arabian Peninsula to create the modern Saudi state. During this process, he had at least 22 wives and 45 sons, 36 who survived to adulthood. He ruled Saudi Arabia from its founding in 1932 until 1953.

Due to the large number of sons, Ibn Saud created a succession plan that would shift from brother to brother rather than the more traditional process known as primogeniture, in which the reign is passed from the eldest brother to his eldest son. This new succession plan did manage to maintain peace among the founder’s sons but it also held the potential for an eventual crisis as the generation of the sons of Ibn Saud aged out, which is where we are at present.

The early succession after Ibn Saud’s death was volatile. His eldest son, Saud, was deposed due to his reckless behavior, including uncontrolled spending and a war in Yemen. He was replaced by Faisal who was assassinated. The third king, Khalid, was a self-acknowledged caretaker. Crown Prince Fahd was in effective control from 1975 and became king in 1982. Fahd’s rule stabilized the kingdom and, as a result, the world became accustomed to reliable leadership in the KSA. However, it became apparent that the stability offered by the sons of Ibn Saud would end as subsequent kings took office as elderly men. King Abdullah was 81 at his elevation and the current king, Salman, took power at age 79.

In June 2017, King Salman removed then-Crown Prince Nayef, an older second generation prince, in favor of the king’s son, Mohammad bin Salman (MbS). The new crown prince was initially lauded as a reformer. He did ease social conditions, implementing restrictions on the clerical police, changing regulations on women driving cars and offering an aggressive economic reform plan. At the same time, much like his uncle, King Saud, the successor to Ibn Saud, MbS has been reckless. His war in Yemen continues to be a drain on resources with no end in sight. A year ago, he turned the Riyadh Ritz Carlton into a makeshift prison for princes and powerful private Saudi citizens accused of corruption.[6] The prime minister of Lebanon was held against his will and forced to make statements against Iran and Hezbollah. He also implemented a blockade of Qatar, a member of the Gulf Cooperation Council. In August, the KSA recalled its ambassador to Canada and expelled the Canadian ambassador to Saudi Arabia over Canadian criticism of human rights abuses in the KSA.[7] The KSA, never overly tolerant of internal criticism, has become even less accepting under the effective government of MbS.[8] And, of course, the Khashoggi murder was extraordinarily rash.

One potential outcome is that the generational shift to the grandsons of Ibn Saud may be as tumultuous as the succession to the sons of the first king. There are hundreds of king-eligible princes and their fear is that a King MbS would favor his own children and forever shut out the other grandsons of Ibn Saud. MbS’s reckless behavior may, in part, reflect his legitimate worry that his elevation to power has created enemies among his fellow royals. At the same time, this reckless behavior increases the chances of instability. In other words, the shift to the next generation of the royal family may carry much more risk than generally anticipated.

Ramifications

Each of these risks requires its own response. A Chinese debt crisis is a deflationary event. Long-duration Treasuries would likely be the best performing asset, whereas emerging markets and commodities would be at greatest risk. Similarly, all the issues facing Europe would favor long-duration Treasuries and the EUR would also be vulnerable.

The last two issues would have different market effects. Populism, once established, would be inflationary. The impact on markets would depend on financial regulation. If regulation and policy allow the interest earned on cash to exceed inflation, then cash would be the preferred asset. We doubt that would be allowed, so commodities and gold would outperform, while long-duration bonds would suffer. A succession crisis in the KSA would clearly be bullish for oil and offer a side benefit for alternative energy, which tends to trade inversely to oil prices.

Obviously, there are some inconsistencies in these market ramifications. To some extent, this should be expected. Investors should use these issues as guideposts; if they become a concern, we would expect the aforementioned market actions to take place. However, it is unlikely they would all occur at the same time. For guidance, we recommend monitoring our publications, including the Daily Comment and the Weekly Geopolitical Report.

Have a happy 2019!

Bill O’Grady

December 17, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

1 This claim is sometimes challenged—if the interest rate is low, why wouldn’t households save by purchasing consumer goods for inventory? This objection, though legitimate, neglects to realize that any consumption decision has two effects, income and substitution effects. If the interest rate is below the level a household needs to earn, it will save even more to generate the desired interest rate return. The substitution effect would trigger hoarding. The secret is to keep inflation low enough to prevent hoarding but keep interest rates even lower.

2 https://www.scmp.com/economy/china-economy/article/2173461/china-underestimating-its-us3-trillion-dollar-debt-and-could

3https://www.nytimes.com/2018/12/05/opinion/george-bush-wasps.html

4https://www.nytimes.com/2018/12/08/opinion/sunday/wasps-meritocracy-ross-douthat.html

5 Turchin, Peter. (2016). Ages of Discord: A Structural-Demographic Analysis of American History. Chaplin, CT: Beresta Books.

6https://www.nytimes.com/2017/11/04/world/middleeast/saudi-arabia-waleed-bin-talal.html

7 https://www.wsj.com/articles/saudi-arabia-recalls-ambassador-to-canada-1533512832

8https://www.washingtonpost.com/world/middle_east/khashoggi-death-throws-new-light-on-saudi-princes-crackdown-on-dissent/2018/10/22/8b9b72da-d56c-11e8-8384-bcc5492fef49_story.html?utm_term=.f9fda2db5493&wpisrc=nl_daily202&wpmm=1

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All