The Malevolent Hegemon: Part II

In Part I, we examined the basic role of the hegemon and the unique model the U.S. has created, which we dubbed the “Benevolent Hegemon.” This week, we discuss why many Americans have become disenchanted with this model, which is pressuring policymakers to either jettison the superpower role or significantly redefine it. Next week, we will conclude the series by discussing the emergence of a new hegemonic model we call the “Malevolent Hegemon.”

The Costs of Benevolence

The U.S. did not naturally aspire to hegemony. From a geographic perspective, the U.S. lives in splendid isolation; neither Mexico nor Canada is a major military threat. As Otto Von Bismarck noted, the U.S. is “surrounded by weak powers and fish.” Unlike many nations, the U.S. can choose whether or not it wants to be involved in the world. Paradoxically, this also means the U.S. is an ideal superpower because it faces no local threats and doesn’t need to devote resources to protect against nearby threats.

Americans did view the threat of communism as significant enough to accept the substantial costs of hegemony. Here are some of the changes entailed in accepting the superpower role:

Distortions of government: The U.S. Constitution created a republic with checks and balances that were designed to impede rapid changes in policy. A generally weak executive was coupled with a bicameral legislature that has one house represented by population and another by state. This structure was designed to prevent majority dominance. Added to this mix was a judiciary that could also restrain legislative or executive excess. The arrangement was generally workable when the U.S. was a small, agrarian republic. However, superpowers must often act quickly in response to global events. Instead of writing a new constitution that would have created a much stronger executive branch, the presidency simply evolved to take this power mostly by reducing the influence of Congress. In addition, the judiciary became an active shaper of policy. Centralizing power was necessary to execute the role of the hegemon, but it did fundamentally change the process of U.S. governance.

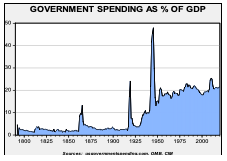

At the same time, the demands of hegemony required a larger government. Not only is there a large military requirement but providing the reserve currency fosters the need for nearly constant fiscal stimulus. In other words, the government needs to help stimulate consumption in order to act as the global importer of last resort.

A large standing military: Prior to the onset of the Cold War, the U.S. typically mobilized for war; once the war ended, there was rapid demobilization. However, during the Cold War, defense spending remained elevated to build the military infrastructure required to meet the costs of hegemony.

Once the U.S. accepted the superpower role, it was no longer a republic characterized by a small federal government and a small military that only expanded for war. However, Americans seemed to long for a return to the days of small government and military parades to mark the clear end to conflicts. For the most part, though, that is not the position of the hegemon; a cursory examination of British history shows persistent far-flung wars that often did not end in clear victory. That has been the U.S. experience for most of the Cold War.1

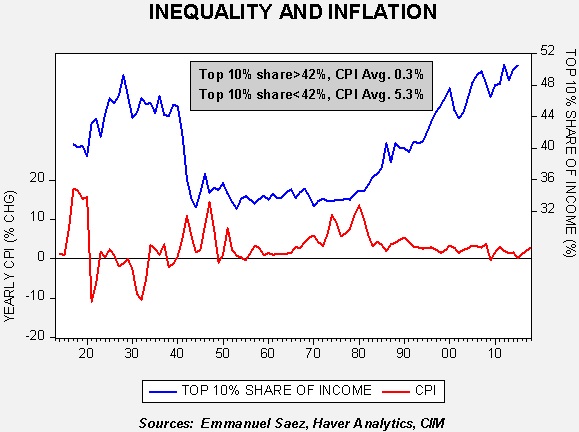

Distortions to the economy: The reserve currency forced the U.S. economy to consume more than normal and also run persistent current account deficits. From 1945 until the late 1970s, policymakers attempted to keep inequality under control by supporting unionization and high levels of regulation. Unfortunately, that policy mix turned out to be quite inflationary.

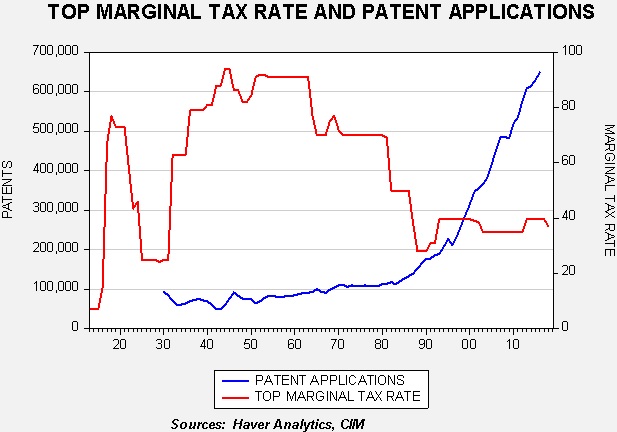

Beginning with the Carter administration, policymakers began a process of globalization and deregulation in order to reduce inflation. Marginal tax rates were cut to encourage entrepreneurship.

This chart shows the highest marginal tax rate and patent applications. Note that patent applications soared after the tax rate was cut in the early 1980s. Before then, marginal tax rates were high enough to discourage entrepreneurship and thus the incentive to acquire a patent was diminished. That obviously changed after the tax rate was reduced.

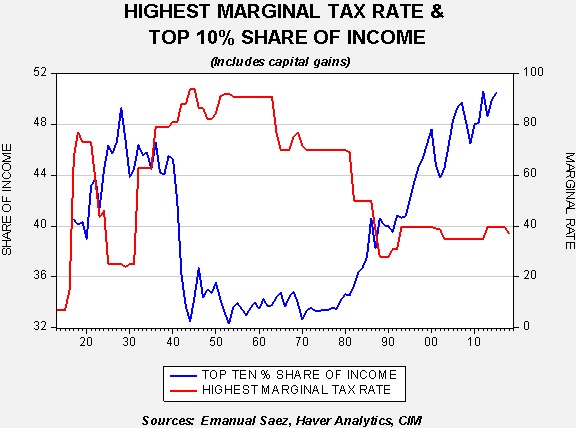

However, falling tax rates fostered inequality. High tax rates don’t boost government revenue; there is no evidence showing that high or low tax rates affect the overall level of fiscal revenue. Rather, marginal tax rates do affect firm and household behavior. High marginal tax rates reduce inequality because there isn’t much point for senior executives to aggressively seek income if the government is going to tax it away. Thus, restraining the income growth of the bottom 90% isn’t worth it to the top 10% under conditions of high marginal tax rates. That changes when tax rates are lower.

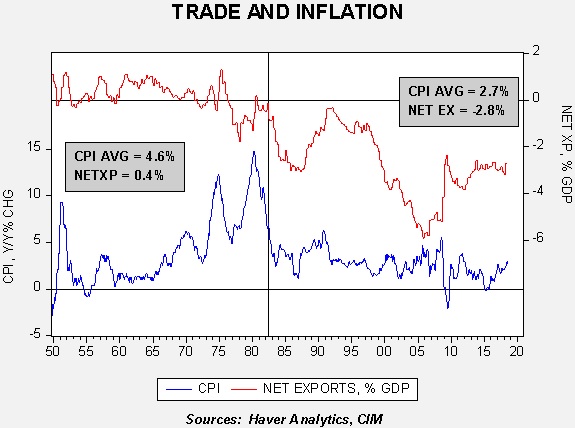

As the trade deficit widened, inflation declined. Foreign goods and services increased supply but also weighed on employment.

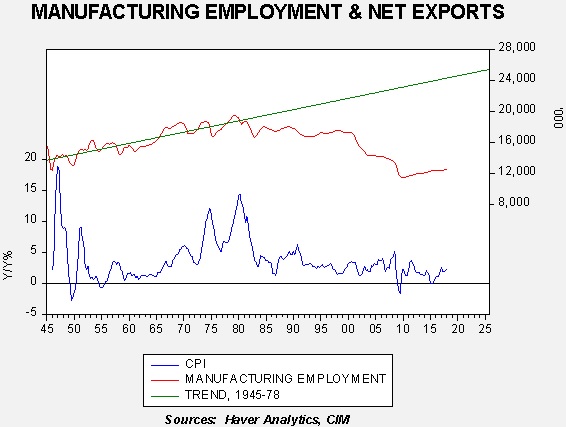

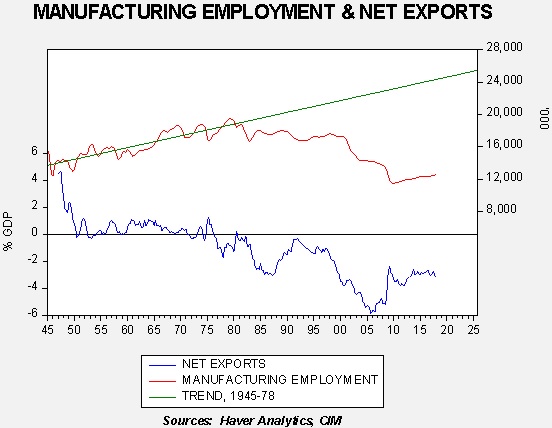

This chart looks at manufacturing employment and CPI. We have calculated a trend line for manufacturing employment for the years from 1946 to 1978 and extended that trend line to the present. As the chart shows, employment competition from abroad reduced U.S. manufacturing employment but also reduced inflation. A similar story between net exports and manufacturing employment exists as well.

It is apparent that manufacturing employment fell well below trend as the trade deficit widened.

Although deregulation and globalization did contain inflation, it did so at the cost of higher inequality, reducing the growth of income and wealth for the bottom 90%. But the importer of last resort role required Americans to expand consumption levels as the U.S. share of global GDP contracted.

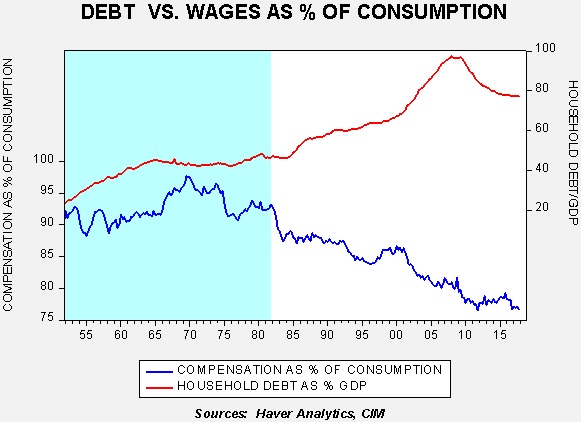

The lower line on this chart shows worker compensation as a percentage of consumption. This measures how much consumption is funded by wages and benefits. From 1950 to 1982, between 90% and 95% of consumption was paid for by compensation. Note that number steadily declined as deregulation and globalization policies were implemented. The upper line of the chart shows household debt as a percentage of GDP. As the portion of consumption funded by compensation fell, households maintained their buying by taking on increasing levels of debt. The 2008 debt crisis severely curtailed the use of debt to fulfill the importer of last resort role.

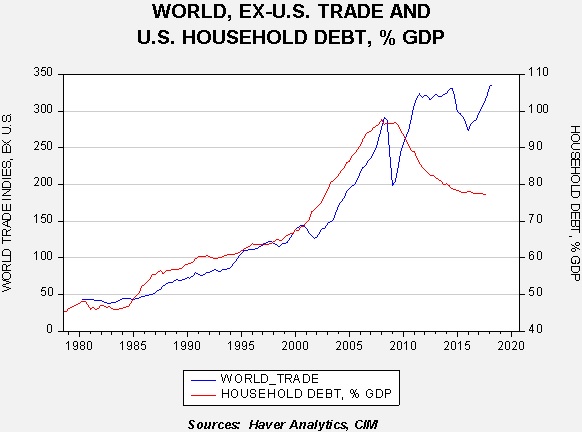

This chart shows U.S. household debt as a percentage of GDP along with the Dallas FRB import and export trade indices, ex-U.S. We add the two trade indices together to get a measure of world trade.

Although we have seen a recovery in world trade recently, the uptrend clearly stalled as U.S. households deleveraged after the financial crisis. Essentially, the growth of world trade depends on the U.S. consumer to provide the reserve currency to the world by consuming imports.

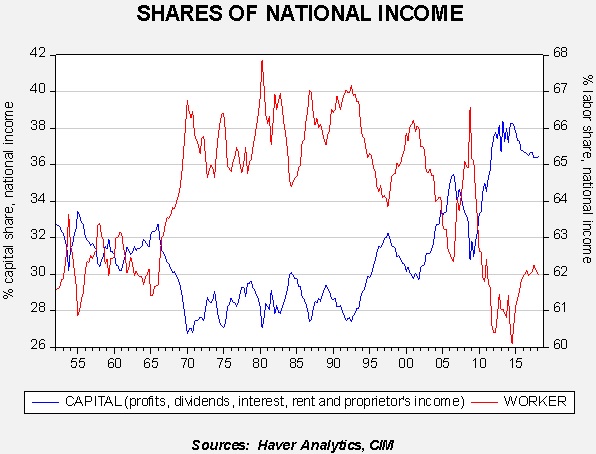

Finally, since the fall of communism we have seen a decided shift in U.S. national income shares to capital and away from labor. As the chart below shows, labor’s share of national income rose in the mid-1960s and held around 66% until 1990. Since then, capital has captured an increasing level of national income compared to labor in each business cycle. This data suggests that once communism fell, the elites in the U.S., who are mostly paid via capital income, no longer felt obligated to prove capitalism was superior to communism and thus were no longer worried about reducing the relative income to workers.

During the period of U.S. hegemony, policymakers have been unable to shape an economy that can restrain inequality without causing inflation. The inability to manage this issue has led to periods of significant social and economic disruption. Simply put, policymakers can either focus on equality by reducing efficiency at the cost of higher inflation or concentrate on efficiency and control inflation at the cost of high inequality. To date, they have not been able to resolve this dilemma and maintain the superpower role. The rise of Occupy Wall Street and the Tea Party are right- and left-wing populist responses to the current inequality problem.

Part III

Next week, we will conclude this report by describing what we see as the new emerging model of hegemony.

Bill O’Grady

December 3, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 With the exception of the First Gulf War, although containing Saddam Hussein turned out to be a constant struggle.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management