The Dollar Problem: Part I

In May, the Trump administration exited the Joint Comprehensive Plan of Action (JCPOA), otherwise known as the Iran nuclear deal.[1] In conjunction with its exit, the U.S. implemented new sanctions and the goal of U.S. policy is to reduce Iran’s oil exports to zero barrels by November.

The other parties in the agreement, China, Russia, the EU and Iran, are unhappy with the U.S. decision. The EU is working to create a payment structure which will not use the U.S. financial system.[2] The plan, which creates a special purpose vehicle that will process trade-related payments between Iran and the EU, could become an alternative to the S.W.I.F.T. network, the current system. Although S.W.I.F.T. is headquartered in Europe, it is dominated by the U.S. financial system because of the dollar’s reserve currency role.

Because the U.S. has a tendency to implement financial sanctions against its perceived adversaries, there have been growing calls for an alternative to dollar-based trade. It is not clear whether an alternative system would end up facing U.S. sanctions as some of its users will likely also use the American financial system. Still, the concern about the U.S. “weaponizing” the dollar has raised the idea of a global reserve currency.

In Part I of this report, we will introduce the characteristics of a reserve currency, including a discussion of the costs and benefits of providing the reserve currency. Part II will begin with a short explanation of the S.W.I.F.T. network and its importance to international finance. From there, we will discuss the potential competitors to the dollar, examining the possibility of competing trade blocs. As always, we will conclude with potential market ramifications.

The Reserve Currency as a Public Good

Economists define a public good as a product or service that must be provided by governments because the private market won’t provide the good, or will only provide the good in less than optimal amounts. There are seven public goods a reserve currency nation should provide:

1. Act as consumer (importer) of last resort;

2. Coordinate global macroeconomic policies;

3. Support a stable system of exchange rates;

4. Act as lender of last resort;

5. Provide counter-cyclical long-term lending;

6. Provide a truly riskless AAA asset for benchmarking purposes;

7. Supply deep and predictable financial markets.

Charles Kindleberger, the famous economist who studied asset bubbles, identified the first five public goods and Mohamad El-Erian, chief economic adviser at Allianz, added the last two.

In practical terms, what does providing the reserve currency mean? Here is a simple example. Imagine that a chocolatier in Paraguay wants to purchase a ton of cocoa beans. He calls a dealer in Côte d’Ivoire for a price; the seller offers $2,070 per ton. The buyer in Paraguay notes he does not have U.S. dollars but does have Paraguayan guaraní.

The seller could accept Paraguayan currency but would be disinclined to do so because it isn’t widely accepted. He would likely be restricted to one of two decisions. First, he could use the guaraní to buy goods from Paraguay. Although that outcome makes the trade somewhat better than barter, the cocoa dealer may not find anything he wants in Paraguay. Or, he could invest the guaraní in Paraguayan financial assets. However, he may not be all that comfortable taking on the risk in Paraguayan financial markets.

On the other hand, if the cocoa dealer received dollars, he would have a currency that is widely accepted worldwide and could be used to purchase a plethora of goods and services. And, if the dealer decided to invest the proceeds, he would have the deep and well-regulated U.S. financial markets at his disposal.

So, taking our example further, how does the chocolatier in Paraguay get dollars? The most efficient way would be to export chocolate to a U.S. buyer, then use the dollars he receives to buy cocoa beans from Côte d’Ivoire. Because the reserve currency has widespread acceptance, non-reserve currency nations have an incentive to run trade surpluses with the reserve currency nation to accumulate the reserve currency, which allows them to pay for imports from around the world.

The Bank for International Settlements (BIS) reports that more than 80% of trade-related letters of credit are denominated in U.S. dollars, significantly more than the second most used reserve currency, the euro, at 10%.[3] That means most global trade is conducted in dollars, usually between nations other than the U.S. Essentially, the reserve currency nation must run constant trade and current account deficits in order to provide liquidity for global trade. Thus, the U.S. doesn’t run trade deficits because we “under-save,” as is often heard by pundits in the financial media. Strictly speaking, this is true but it is mostly in response to foreign nations over-saving and moving that saving to the U.S. in the form of exports. If the U.S. were to run persistent trade surpluses, it would act as a global monetary tightening. In other words, by pulling dollars from world markets, the global trading system would face a contraction of available liquidity. If the reserve currency nation refuses to provide enough of its home currency to global markets, world trade is effectively reduced to barter, or counter-trade, meaning that nations can only engage in bilateral trade relations. Using the above example, the Paraguayan chocolatier can only acquire cocoa beans from Côte d’Ivoire if the seller there has something specific he would like to swap from Paraguay. Simply put, global trade would fall sharply if a reserve currency is unavailable.

Economist Robert Triffin described the reserve currency country problem in the 1960s. Because the reserve currency provides global liquidity, the reserve currency country must run a persistent current account (trade) deficit. As noted above, if the reserve currency nation runs a surplus, it would act as a global monetary policy tightening. However, this deficit would need to be “manageable.” If it becomes too large, it could shake foreign investors’ confidence in whether the risk-free asset is truly risk-free.

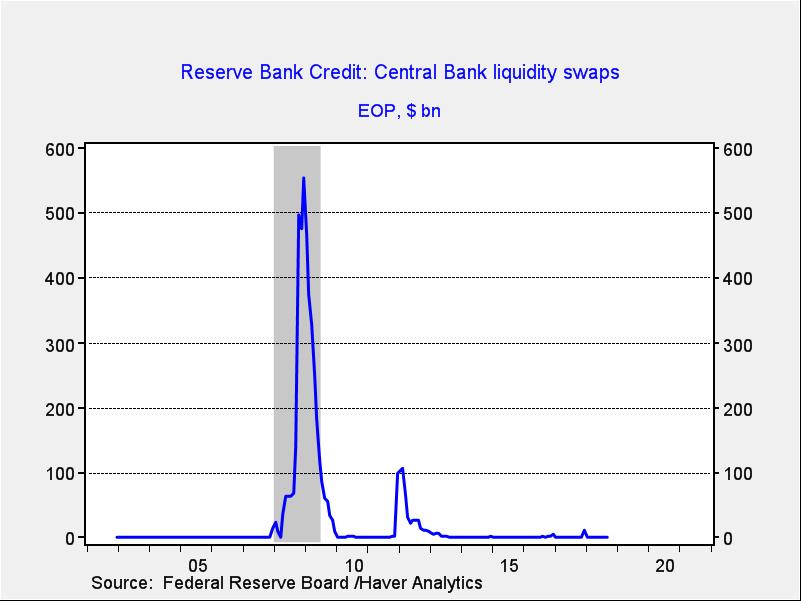

Another key role the reserve currency nation plays is managing global financial crises. For example, the U.S. created “Brady bonds” in the late 1980s to serve as dollar-denominated financial assets that U.S. banks could buy in exchange for foreign loans that were either non-performing or heading in that direction.[4] The program not only relieved pressure on U.S. banks, but it encouraged new lending for emerging economies. The U.S. was involved in the 1994 Peso Crisis and the 1997 Asian Economic Crisis.[5] The U.S. also provided dollar swaps to the world’s central banks during the 2008 Great Financial Crisis, making the Federal Reserve the central bank to the world. The chart below outlines the degree of dollar support from the Federal Reserve.

The benefits of providing the reserve currency are rather simple; you receive goods and services from the world in exchange for your currency. In effect, the U.S. exports dollars and imports goods and services. And, when foreigners receive dollars, they can use them to buy U.S. goods and services, but they can also use them to buy goods and services from other nations. If they don’t want to spend their dollars immediately, they can hold them in U.S. financial assets. Thus, their investing tends to lower U.S. interest rates and boosts the value of other financial assets as well.

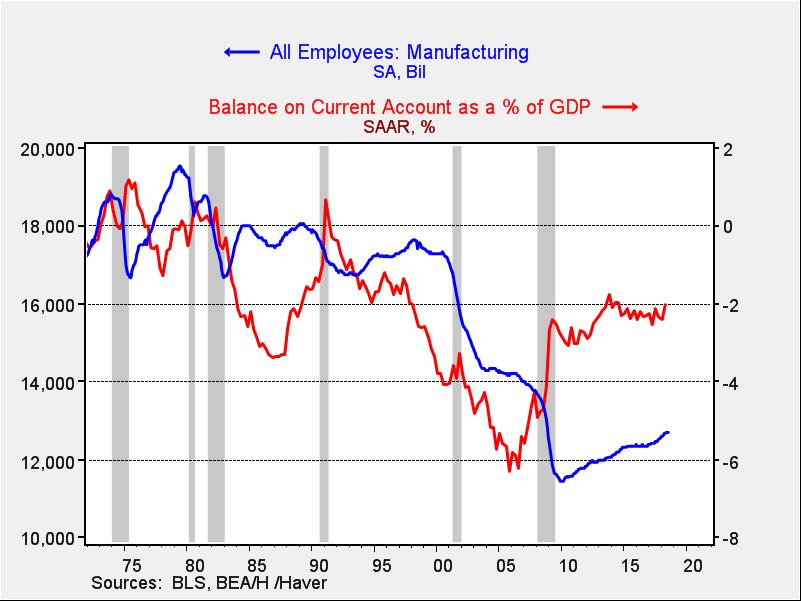

The costs are borne primarily by import-competing industries.

This chart shows U.S. manufacturing employment compared to the U.S. current account, scaled to GDP. As the deficit widened, manufacturing employment has declined. Obviously, not all of these jobs were lost due to trade; some became obsolete due to automation. But, trade played a major role.

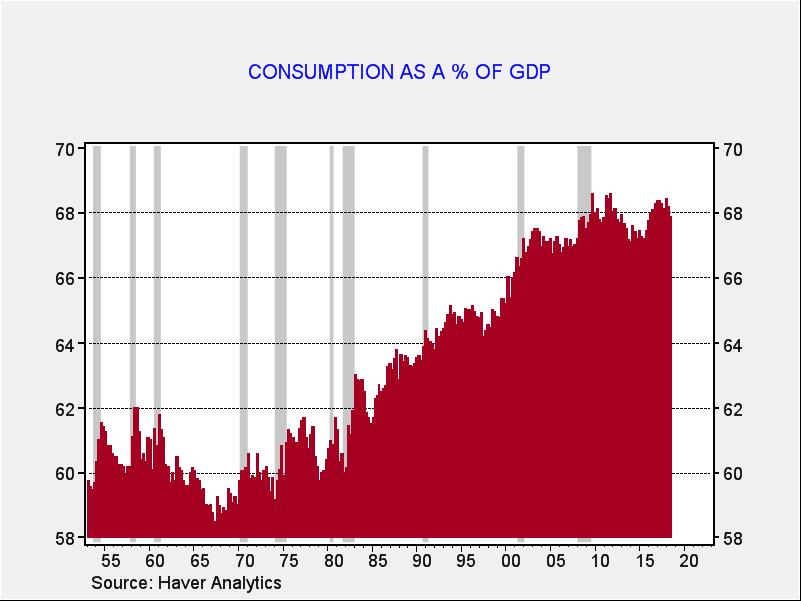

The need to be the global importer of last resort also distorts the reserve currency nation’s economy, forcing consumption to be higher than it would be otherwise.

In the U.S., consumption as a percentage of GDP is around 68%. Without the reserve currency role, consumption would more likely be around 64% or less. The need to consume has tended to cause either inflation or higher levels of consumer indebtedness.

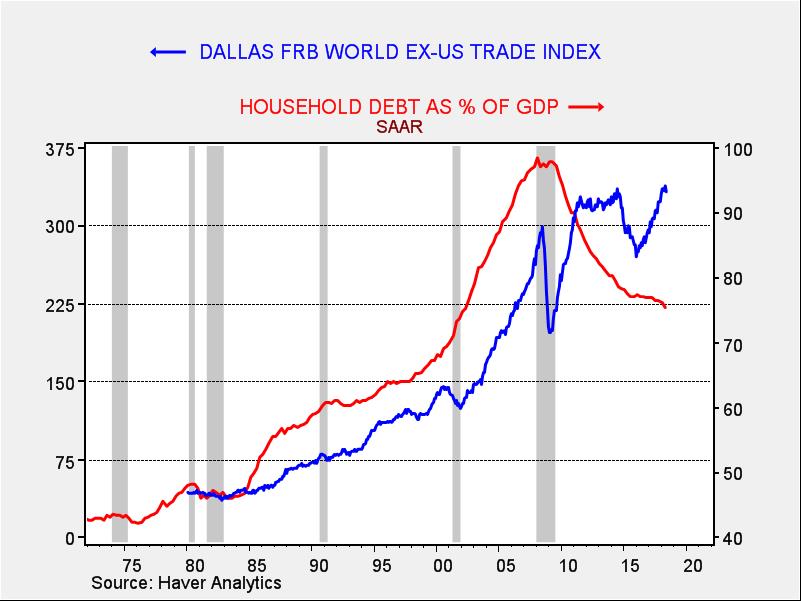

This chart shows U.S. household debt as a percentage of GDP along with the combined import and export indices for the world, excluding the U.S. Note that the growth of trade was facilitated by household indebtedness and the growth of world trade has stalled as the U.S. household sector has deleveraged.

Part II

Next week, we will conclude this report with an examination of the S.W.I.F.T. network and its importance to international finance. From there, we will discuss the potential competitors to the dollar, examining the possibility of competing trade blocs. As always, we will conclude with potential market ramifications.

Bill O’Grady

October 1, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[1]https://www.nytimes.com/2018/05/08/world/middleeast/trump-iran-nuclear-deal.html

[2]https://www.washingtonpost.com/world/2018/09/26/yes-world-leaders-laughed-trump-theres-another-less-obvious-sign-diminishing-us-influence/?utm_term=.1012f272b77d

[3] http://www.bis.org/publ/cgfs50.htm

[4] https://www.emta.org/template.aspx?id=35

[5] This famous magazine cover is an example of America’s role in global financial stability: http://content.time.com/time/covers/0,16641,19990215,00.html

© Confluence Investment Management

Read more commentaries by Confluence Investment Management