The Venezuelan Migration Crisis: Part I

Venezuela has gone from “bad to worse” in recent years. In 1999, Hugo Chavez was elected president and took the country on a journey into Cuba-style socialism. Persistent government intrusion into the economy reduced private sector involvement. Although the oil sector was able to generate enough revenue to allow Chavez to fund his socialist programs (and provide oil to allies at reduced prices), the lack of investment and falling oil prices put the economy in dire straits. After Chavez died in 2013, Nicolas Maduro has been the nation’s chief executive. He has presided over an accelerating political and economic disaster.

Maduro’s mismanagement has led to a migration crisis. Millions of Venezuelans have already fled and surveys suggest many more are considering that alternative. The massive outflow of people is causing severe strain on Venezuela’s neighbors and could eventually become a problem for Mexico and the U.S. In Part I of this report, we review Venezuela’s economic and political situation. Part II will begin with a discussion on migration with a focus on emigrant flows. We will include an analysis of the problems caused by migration, followed by an examination of the possible end to this crisis and the broader geopolitical issues. As always, we will conclude with potential market ramifications.

Venezuela’s Economic Woes

Economic conditions in Venezuela have deteriorated to the point where numerous standard economic indicators are no longer calculated by the government or are so suspect that they are no longer reliable. Still, there are a few data points that provide some color on the economic devastation that Venezuelans have suffered.

Venezuela has slipped into hyperinflation. The IMF is projecting the country’s annual inflation rate will reach 1,000,000% this year.[1] This forecast should be taken with a grain of salt. Once an economy slips into hyperinflation, accurate estimations of inflation can be problematic, in part, because prices change so rapidly. However, what we can take from this forecast is that inflation in Venezuela is very high and the recent decision to issue a new currency with fewer zeros doesn’t change that fact.

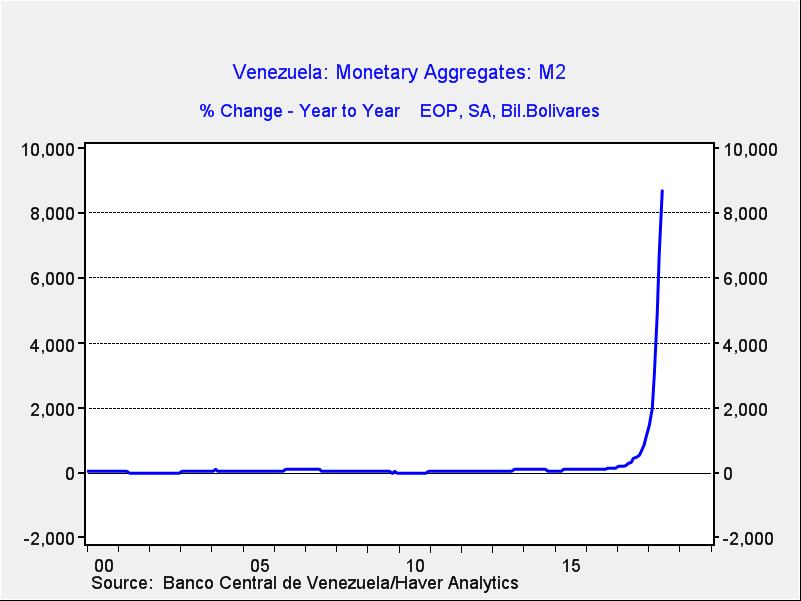

As one would expect, money supply growth is exploding.

This chart shows the yearly change in M2; the annual growth rate of the M2 money supply was 8688.4% in June. Since we don’t have reliable GDP numbers, we cannot calculate velocity, but it would be reasonable to expect that it is skyrocketing. After all, when money is depreciating at a rapid pace (which is what inflation really is—monetary depreciation), it makes sense to convert it to other assets as quickly as possible. The official prime loan rate is 20.6%, meaning that real interest rates are deeply negative; we doubt there is much private sector lending.

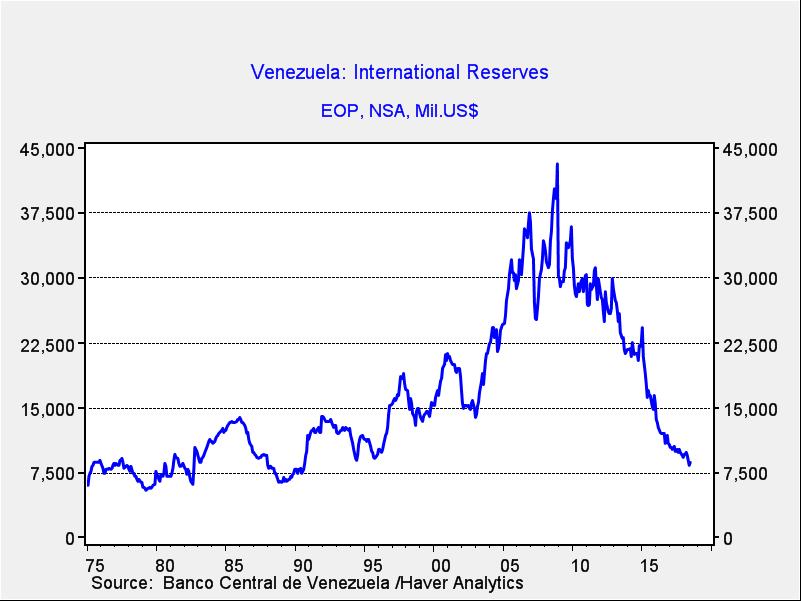

Foreign reserves are declining rapidly.

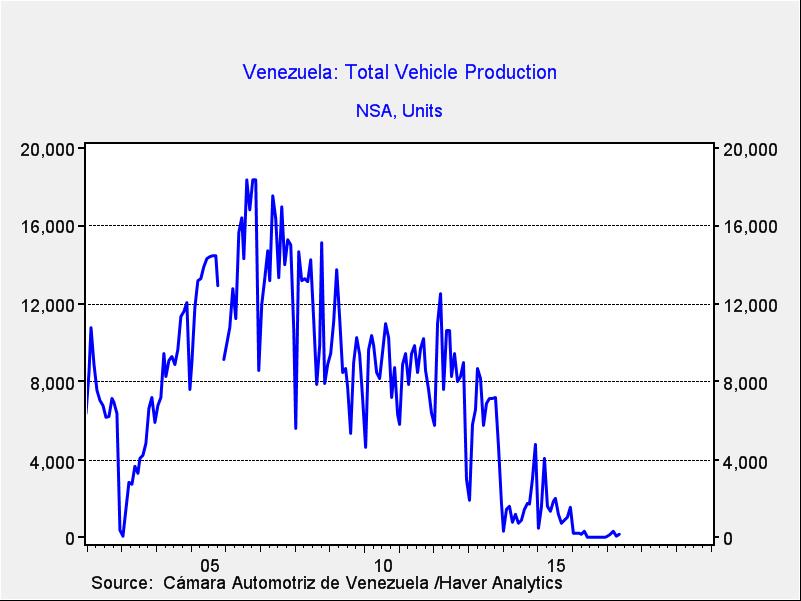

The government hasn’t provided import data since 2015, so an import cover ratio can’t be calculated. Much of the decline in reserves is due to the Maduro government’s attempts to avoid debt default. However, the decline in available reserves has made the goal of avoiding debt default impossible.[2] The inability to borrow has undermined normal business operations; financing working capital becomes impossible in such an environment. Although we don’t have data on automobile production after May 2017, the pattern makes it clear that the ability to import spare parts or produce goods that require time to manufacture becomes problematic under conditions of hyperinflation.

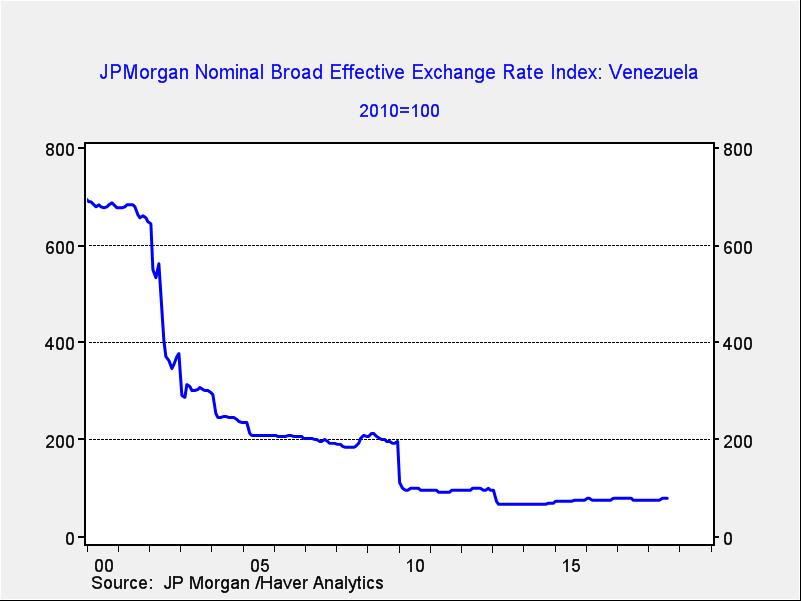

The exchange rate is difficult to ascertain because the government has used various pegged rates over the years to allow groups favored by the government to acquire imports at low prices. And, since reliable inflation rates are difficult to calculate, generating real exchange rate indices is also nearly impossible. Nevertheless, nominal exchange rate indices can be generated and, as one would expect, they provide a dismal read on the economy. The chart below shows the JPM nominal broad effective exchange rate, which is the exchange rate adjusted for trade patterns. The lower the reading, the weaker the currency. Since Chavez took power in 1999, the exchange rate has been on a downward trajectory.

Finally, Venezuela is a member of OPEC. Nations in this cartel are usually dependent on oil production and exports for economic growth and government revenue.

This chart shows Venezuelan oil production. During the 1990s, PDVSA courted foreign investors into the oil sector and production steadily rose. Just before Chavez was elected in 1999, Saudi Arabia, in a bid to maintain U.S. market share, boosted output and drove oil prices to near $10 per barrel. Chavez sued for peace and oil prices recovered. However, the terms of peace meant that foreign investment was no longer fostered and oil production began to decline. The large decline in 2003 was the PDVSA strike that led to the replacement of seasoned oil workers with party loyalists. Production did hold steady until 2016 when years of low investment eventually led to falling output. Current production is now below 1.5 mbpd. The drop in oil output has undermined the “Bolivarian” economy set up by Chavez and put the country in its current predicament.

Perhaps the most poignant expression of the impact of hyperinflation on the Venezuelan economy is evident in the below photo, showing the amount of currency required to buy a roll of toilet paper.

The average Venezuelan has lost 24 pounds of body weight from 2016 to 2017, and it is estimated that 90% of the country’s citizens live in poverty.[3]

Political Crisis

Given the economic collapse in Venezuela, it is no surprise that President Maduro is unpopular. In the first parliamentary elections under President Maduro in 2015, the opposition coalition of Democratic Unity (MUD) took two-thirds of the seats in the National Assembly, soundly defeating the United Socialist Party of Venezuela, (PSUV), Maduro’s coalition. This should have created conditions for a democratic transition away from Chavez’s successor.

Instead, Maduro and his allies took a number of steps to undermine the outcome of the parliamentary vote. First, the Venezuelan president used the Supreme Court, which he had packed with allies, to undermine the National Assembly. For example, he used the court to squelch a recall election that was to be held in 2016. Second, Maduro then forced a new election for a National Constituent Assembly in July 2017, purportedly to reform the 1999 constitution. MUD fostered protests to oppose the action, but Maduro continues to have a stronghold on the country’s security services. The protests and harsh reaction by the government led to over 125 fatalities and widespread allegations of torture and excessive force by security officers.[4] MUD refused to participate in the Constituent Assembly special election leading to a landslide victory for Maduro’s coalition.

The new Constituent Assembly has supra-constitutional powers and has become a key tool for Maduro remaining in power. The assembly called snap local elections 11 months ago and prevented MUD candidates from appearing on ballots. Polling places were abruptly closed or moved as ploys to prevent opposition voting.[5] In addition, there were widespread reports of vote buying and fraud.[6]

Persistent pressure and the lack of a democratic path to change the government has radicalized parts of the opposition. A group called “Soy Venezuela” is calling for a removal of the government and the dissolution of the Constituent Assembly. There have been recent attempts on the president’s life, including a recent, rather theatrical attack using drones.[7] But, to date, Maduro remains in power.

Conditions are profoundly bad. When economic, social and political conditions deteriorate, there is a strong incentive to look for a better life elsewhere. Recent polls show that 54% of upper income and 43% of lower income Venezuelans want to migrate. What is shocking is that 66% of Chavistas also want to leave. Even the most loyal to the president, the Maduristas, also express a desire to depart.[8]

Part II

Next week, we will conclude this series with a discussion on migration, focusing on emigrant flows. An analysis of the problems migration is causing will be included as well as an examination of the possible end to this crisis and the broader geopolitical issues. As always, we will conclude with potential market ramifications.

Bill O’Grady

September 17, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

[1] https://www.bloomberg.com/news/articles/2018-07-23/venezuela-s-inflation-to-reach-1-million-percent-imf-forecasts

[2] https://www.bloomberg.com/news/articles/2018-08-17/venezuela-debt-wreck-marks-new-milestone-as-6-1-billion-unpaid

[3] https://www.reuters.com/article/us-venezuela-food/venezuelans-report-big-weight-losses-in-2017-as-hunger-hits-idUSKCN1G52HA

[4]https://www.hrw.org/report/2017/11/29/crackdown-dissent/brutality-torture-and-political-persecution-venezuela

[5] https://d2071andvip0wj.cloudfront.net/065-containing-the-shock-waves-from-venezuela.pdf, International Crisis Group, page 4.

[6] https://www.washingtonpost.com/news/monkey-cage/wp/2017/10/20/did-maduros-party-really-dominate-sundays-election-in-venezuela-these-polls-should-make-you-skeptical/?utm_term=.1a343eeaf4aa

[7]https://www.nytimes.com/video/world/americas/100000006042079/how-the-drone-attack-on-maduro-unfolded-in-venezuela.html

[8] https://geopoliticalfutures.com/coping-venezuelan-migration/ (paywall).

© Confluence Investment Management