Last week, we introduced this topic by discussing the Cold War. This week, we will continue our analysis with a reflection on markets, an examination of hegemony and a discussion of the expansion of globalization and the rise of meritocracy and its discontents.

What about Markets?

Market economics is based on how humans actually behave and has been proven to be a superior method of solving the economic problem. However, it works best when those competing, negotiating or trading are doing so under conditions of near-equal footing. According to David Hume’s analysis, justice can only occur among near equals. Under these conditions, pitting self-interest against self-interest leads to the most optimal outcome. However, when there are great differences in power between parties, justice doesn’t really occur and the weaker party is forced to rely upon the mercy of the powerful.[1] Simply put, in unequal relationships, Hume calls for mercy but realizes there will be no justice.

Again, Adam Smith crystalizes Hume’s thought with regard to the economy in this famous quote:

People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or some contrivance to raise prices.[2]

This condition is a flaw of market economics. Governments and society have attempted to address this situation through regulation and charity, respectively. In other words, to improve the lot of the poor, regulation, which limits the power of capital, and charity, which gives the poor an opportunity to improve their situation, were supported. During the Cold War, there was a clear effort to prove market economics and democracy were superior to communism by generally building the middle class and creating something of a “worker’s paradise.”

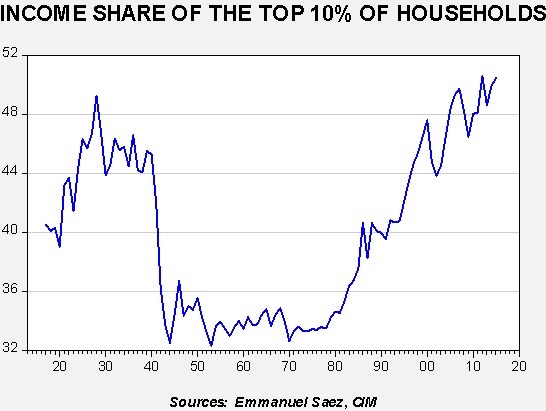

This effort can be seen in the following two charts. The first chart shows the level of income captured by the top 10% in the U.S.

This data begins with the onset of the income tax in 1913, which provides accurate data on incomes. Income inequality was pronounced before WWII but after the war and during most of the Cold War the top 10% of households held about 33% of income. Although the high inflation years of the 1970s led policymakers to ease regulations, resulting in increases in inequality, income concentration rose rapidly after the Cold War ended.

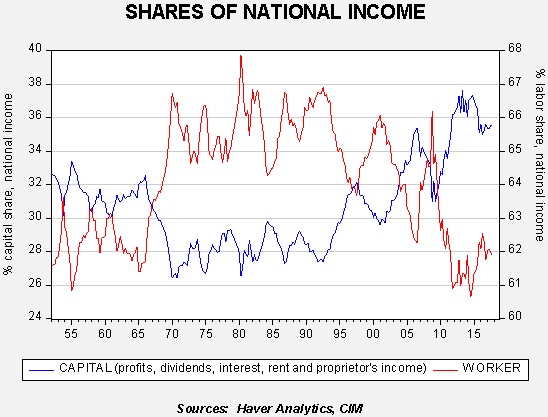

The second chart shows the distribution of national income between labor and capital.

Since the fall of communism, labor has been receiving a steadily falling share of national income relative to capital. In virtually every business cycle, labor suffers a decline and it struggles to break the downtrend. Meanwhile, capital’s share continues to rise.

Although deregulation and globalization, the key factors that have depressed labor wages, were well underway during the 1980s, the trend clearly accelerated after the collapse of communism. It would appear that capitalists, seeing their victory over communism, lost restraint and implemented policies designed to boost capital at the expense of labor. The victory over communism meant that capitalists no longer had to prove they made workers better off than the communists and, with these restraints lost, market economies increasingly favored policies that supported capital’s interests.

Winning the World

During the Cold War, the U.S. accepted leadership of the Free World and acted as the hegemon for the non-communist bloc. The need for a hegemon comes from “hegemonic stability theory,”[3] which postulates that the global economy needs a superpower to function. The superpower provides two broad categories of public goods. First, the superpower must have a large military that allows it to maintain order. This usually means a dominant navy that protects the sea lanes and provides the security for trade. The second is the reserve currency which provides a common medium for global trade.

The military security provided by the hegemon gives nations the incentive to “free ride” and underspend on their own defense. When the British held this role (1815-1930), they relied on an empire to provide bases and soldiers to offset the cost. The U.S. has simply shouldered the burden with some modest offset from treaties. The reserve currency encourages, in fact almost requires, other nations to run trade surpluses with the hegemon to accumulate the reserve currency for trade purposes. This can create the “Triffin dilemma,” where the hegemon needs to run a larger trade deficit as the world economy grows but runs the risk of other nations losing confidence in the value of the reserve currency due to its increasing supply on global markets. In addition, the trade deficit puts increasing pressure on the hegemon’s job market as trade undermines the hegemon’s domestic market.

After WWII, the U.S. economy represented almost 35% of global GDP. It was initially able to supply the reserve currency without serious disruption. However, by the early 1970s, pressure had risen on the dollar. President Nixon responded by closing the gold window and ending the Bretton Woods arrangement. This changed the world reserve system from a “dollar/gold” base to a “dollar/Treasury” base. By accepting Treasuries in lieu of gold, the U.S. was able to continue to supply dollars but now had the added benefit of forcing foreigners to fund America’s fiscal deficit. This change encouraged even wider fiscal and trade deficits.

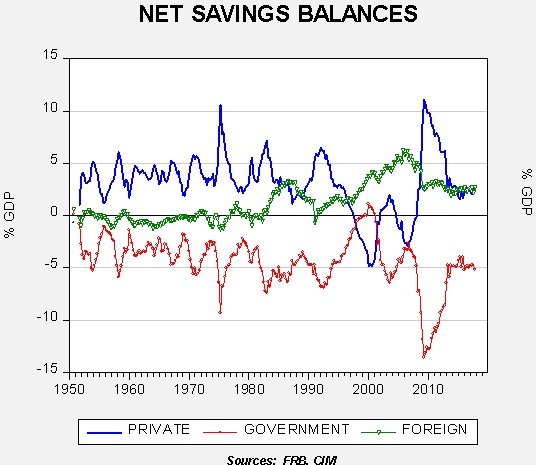

The next chart shows U.S. net savings balances. The net savings of the three major sectors (private, government and foreign) will always equal zero because the relationship is a macroeconomic identity. Private sector saving is the combination of net household saving (income less consumption) and net business saving (net revenue less investment). Government saving is taxes less spending. Foreign saving is the inverse of the current account.

Since the 1980s, private saving has steadily declined mostly due to falling household saving. Fiscal deficits, with some notable exceptions, have also tended to widen. The gap has been filled from foreign saving.

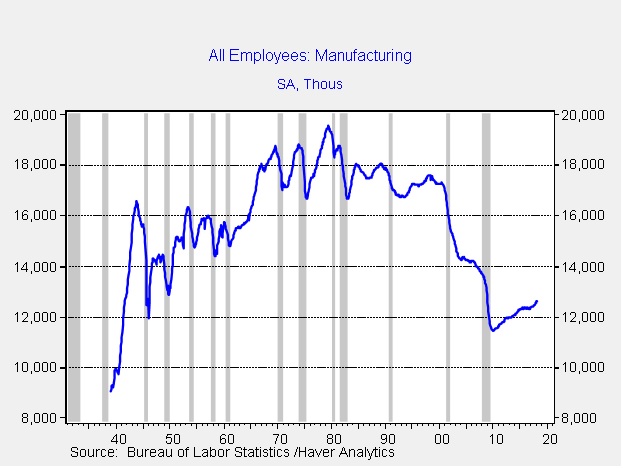

The trade deficit for the U.S. is a mixed benefit. On the positive side, foreign imports in excess of exports gives American consumers a plethora of low-priced goods for consumption. At the same time, it has adversely affected employment. Manufacturing has been especially vulnerable, although automation has also affected employment in this sector.

It’s a Small World After All

Winning the Cold War also convinced policymakers that it was safe to support foreign investment and long supply chains. During the Cold War, a firm investing overseas faced the potential for expropriation as a Marxist government could come to power and simply take away one’s investment.[4] However, this concern fell away once communism was no longer viable. In addition, the Washington Consensus supported open capital markets, which eased foreign investment into emerging markets.

The second important factor that boosted globalization was technology. Richard Baldwin[5] suggested that information technology has changed globalization. The first wave of globalization began in the early 1800s and ended in the early 1990s. In the first wave, falling transportation costs allowed the goods of the industrial revolution to be sold across the world. However, the technology itself was expensive and hard to transfer, so there was a “Great Divergence” where the rich industrialized countries and workers enjoyed tremendous benefits. In other words, workers in the industrialized world were, over time, able to take advantage of fixed industrial capital and demand higher wages. Marx’s classic work, Capital,[6] was laden with long passages about the dismal lives of the working class. Those circumstances improved over time, something Marx never imagined, in part because the industrialized world could not tap the lower wages in the non-industrialized world. Firms were forced to pay higher wages for labor peace. In addition, the U.S. was fighting the Cold War and political solidarity was desired.

Baldwin argues that information technology undermined labor’s power in the industrialized world. By using information technology, techniques and knowledge can be easily transferred across the globe; for example, clerks in India can now process checks or work in call centers. Workers in the West now find themselves facing competition from lower wage workers abroad as the first wave of globalization, shipping, is combined with transferrable know-how, allowing costs to decline. Essentially, information technology reduces the cost of transferring people and allows the very talented to leverage their skills on a global scale. The ability to maintain incomes has become a problem for those without high skill levels.

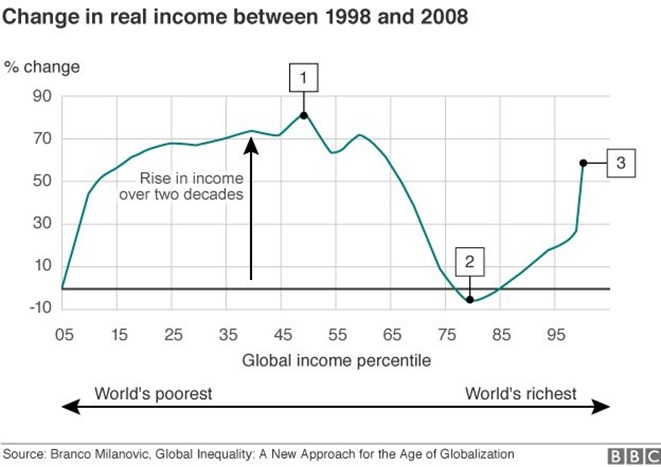

This condition has led to the famous “elephant graph,” created by Branko Milanovic. It shows that real income growth in the emerging world grew strongly from 1988 to 2008, while middle class income growth stagnated in the developed world. This graph goes a long way in explaining the rise of populism in the U.S. and Europe.

The Rise of Meritocracy and the Backlash

The second wave of globalization from information technology coupled with the widespread belief that there were no ideological differences in the world has led to the emergence of a global elite.[7] The creation of the “Davos man,” a cosmopolitan capitalist who can leverage his skills on a global scale and enjoy great success (and wealth), has been part of the new world that has emerged since 1990. This leads to:

…another defining characteristic of today’s plutocrats: they are forming a global community, and their ties to one another are increasingly closer than their ties to hoi polloi back home. As Glenn Hutchins, co-founder of the private equity firm Silver Lake, puts it, “A person in Africa who runs a big African bank and went to Harvard might have more in common with me than he does with his neighbors, and I could well share more overlapping concerns and experiences with him than with my neighbors.” The circles we move in, Hutchins explains, are defined by “interests” and “activities” rather than “geography”: “Beijing has a lot in common with New York, London, or Mumbai. You see the same people, you eat in the same restaurants, you stay in the same hotels. But most important, we are engaged as global citizens in crosscutting commercial, political, and social matters of common concern. We are much less place-based than we used to be.”[8]

The beneficiaries of the new globalization believe their good fortune is due to their efforts and thus they generally oppose efforts to halt “progress.” And, as the quote above shows, they appear to have less in common with the citizens of the nation where they reside and therefore have less interest in national actions to address the “left behind.”

The rise of populist occurrences, including Brexit, President Trump and the recent Italian, Polish and Hungarian elections, are all elements of the backlash against the new form of globalization. There is a feeling that the wealthy have too much political influence[9] and consequently there is the willingness to consider unconventional political candidates.

Part III

Next week, we will conclude this report with a discussion on how China and Russia threaten U.S. hegemony, the potential responses and market ramifications.

Bill O’Grady

April 16, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[1] Hume, D. (1966). An Enquiry Concerning the Principles of Morals. La Salle, IL: Open Court Press (p. 23). “Were there a species of creatures intermingled with men, which, though rational, were possessed of such inferior strength, both of body and mind, that they were incapable of all resistance, and could never…make us feel the effects of their resentment; the necessary consequence…is that we should be bound by the laws of humanity to give gentle usage to these creatures, but should not…lie under any restraint of justice with regard to them, nor could they possess any right or property…our compassion and kindness is our only check, by which they curb our lawless will…the restraints of justice…would never have place in so unequal a confederacy.”

[2] Smith, op. cit., p. 128.

[3] The seminal work on this topic is by Charles Kindleberger. Kindleberger, C. (1986). The World in Depression, 1929-39 (2nd ed.). Berkeley, CA: University of California Press.

[4] For example, Salvador Allende nationalized U.S. mining operations in Chile after winning the presidential election in 1970.

[5] Baldwin, R. (2016). The Great Convergence: Information Technology and the New Globalization. Cambridge, MA: Harvard University Press.

[6] Marx, K. (1977). Capital: Vol. I (original ed. 1867). New York, NY: Vintage Books.

[7]https://www.theatlantic.com/magazine/archive/2011/01/the-rise-of-the-new-global-elite/308343/

[8] Ibid.

[9]http://www.pewglobal.org/2015/02/12/discontent-with-politics-common-in-many-emerging-and-developing-nations/

© Confluence Investment Management

Read more commentaries by Confluence Investment Management