Last week, we published the first part1 of this report looking at how the U.S. and other nations are changing their policies toward nuclear weapons. This is something of a refresh of a report we did seven years ago.2 Since we published this earlier report, we have seen an increase in actual and potential nuclear proliferation. Both the previous and current U.S. administrations are developing new nuclear weapons policies. What spurred this two-part report was the recent false alarm in Hawaii.

Last week, we reviewed the development of nuclear weapons and the U.S. deployment policy from the end of WWII to the end of the Cold War. We offered an analysis of how the theory of deterrence developed over time and introduced the history of the post-Cold War era. This week, we will discuss how the Cold War arrangements have broken down in the post-Cold War world and the nuclear proliferation that has ensued. We will also examine how states will cope with this changing nuclear weapons environment and the evolution of new nuclear doctrines. This will include a discussion on civil defense, nuclear strategy and weapons development. We will conclude, as always, with potential market ramifications.

The Breakdown of the Cold War Order

Nuclear doctrines in the Cold War were eventually based on “Mutual Assured Destruction,” or MAD. However, proliferation has tended to undermine that system. The more countries that have “the bomb,” the harder it is to prevent its deployment. A complicating factor has been the steady withdrawal of the U.S. from the hegemonic role it has maintained since WWII.

Here are the major issues:

The fraying umbrella: During the Cold War, countries under the U.S. or Soviet nuclear umbrellas were highly confident that an attack using nuclear weapons would trigger a similar response from their protector. This status discouraged nuclear powers from using the weapon as blackmail to coerce behavior.

The key element to deterrence was the expectation of response. That certainty is now undermined. First, following the collapse of the Soviet Union, the nations formerly under its umbrella could not expect a Russian response. The U.S. was fortunate that the combined diplomatic efforts of American and Russian leaders were able to convince the nations that emerged from the former Soviet Union to refrain from keeping the legacy Soviet nuclear weapons, which prevented further proliferation. However, Ukraine probably rues the decision to give up its nuclear weapons; if it had kept them, it is likely that Putin would not have been as aggressive against the Orange Revolution. The absence of Russian protection is probably why Syria tried to begin a nuclear weapons program that was thwarted by Israeli bombing.

Second, there is growing uncertainty about U.S. nuclear doctrine. For example, would the U.S. risk a Chinese nuclear response targeting the American mainland if North Korea used its nuclear weapons against Japan? If Japan begins to doubt America’s response, it will be inclined to cross the nuclear threshold. A similar problem is developing in the Middle East. If Iran crosses the threshold, would the U.S. risk a nuclear attack against Europe or the American mainland if Iran used nuclear weapons against Saudi Arabia? To some extent, the “nuclear umbrellas” were a form of free riding. The protected nations didn’t have to make the investment into these weapons. However, as the U.S. pulls back from its hegemonic role, the temptation grows to acquire one’s own nuclear deterrence. Nuclear proliferation likely increases the chances that they will be used.

The deployment of tactical nukes: Nuclear weapons generally come in two types—strategic and tactical. During the 1950s, the U.S. and U.S.S.R. each tested so-called “battlefield nukes,” which were tactical nuclear weapons. Tactical nuclear weapons remained part of the U.S. arsenal until the end of the Cold War. They were never used (although they were considered) during the various Cold War conflicts due to fears that a small nuclear attack would escalate into a nuclear cataclysm.

However, using the same logic discussed in the nuclear umbrella section, low-yield nuclear weapons could be a response to nuclear proliferation. Having small nuclear weapons would give leaders flexibility in responding to threats and actions. For example, if North Korea began a conventional war with South Korea using its massive, embedded artillery placed near the demilitarized zone, the U.S. could use low-yield nuclear weapons to stop the attack and reduce the fallout brought on by a strategic weapon. This attack would probably be more effective in stopping North Korea’s attack and, at the same time, would likely not trigger a strategic response from China. On the other hand, it might trigger such a response from North Korea. However, the Kim regime would have to decide if it wanted to risk a strategic nuclear war with the U.S., which would damage the U.S. mainland but almost certainly lead to the eradication of North Korea.

Russia is developing such weapons as a way to respond to conventional NATO threats; not only would low-yield nuclear weapons likely stop the conventional threat, but they probably wouldn’t bring a strategic response from the U.S. Simply put, the U.S. isn’t likely to risk Washington, D.C. in order to defend Tallinn.

In some respects, tactical nuclear weapons are similar to chemical or biological weapons. They are all weapons of mass destruction and have significant psychological effects. The advantage of tactical nuclear weapons is that they are more controllable.3 WWI showed that chemical weapons, under adverse weather conditions, can negatively affect the launcher. Controlling biological weapons is also fraught with risk.

At the same time, the development of smaller nuclear weapons will make it easier for leaders to use them. The primary unknown is deterrence and response; in other words, would a nation possessing strategic nuclear weapons be more or less likely to respond to a tactical nuclear attack with strategic weapons? That is the unknown factor, but it does appear there will be situations where these weapons can be used with great effect and not escalate to a strategic nuclear weapons response.

Retaliation adjustments: A new draft of U.S. nuclear strategy4 is being reviewed by the Trump administration. In the past, the criteria for a “first use” of strategic nuclear weapons was a similar threat from another strategic nuclear power or a biological weapons attack from an adversary. The current draft expands that criteria to include a cyber attack against U.S. infrastructure, such as the power grid or the financial system. It also includes similar attacks against allies.

The draft does acknowledge that America’s response to such an attack would not be limited to strategic nuclear weapons (or, for that matter, tactical nuclear weapons), but it also states that “under extreme circumstances” the U.S. may consider nuclear retaliation.

Adding a nuclear response to a devastating cyber attack does have some logic. If the U.S. clearly signals that such retaliation is possible, it may act as a deterrent. However, expanding the list of items that can trigger a nuclear response does carry some significant risks. Cyberwarfare is a particular problem because it can be difficult to precisely pinpoint who is responsible for the attack. The potential for “false flag” operations is high. For example, if Israel wanted the U.S. to attack Iran with nuclear weapons, delivering a massive cyber attack on the U.S. but disguising it in such a way to make it look like it originated from Iran could be effective. Obviously, a government-sponsored action like this would be fraught with risk. If the U.S. was able to determine that the attack really came from Israel, it could permanently sever relations. Another scenario would be that a pro-Israel, non-governmental group would deliver the cyber attack. Non-state actors, such as terrorist groups, could take similar actions. Rogue elements within the security apparatus of various nations may consider comparable acts. The anonymous characteristics of cyberwarfare make the deterrence effect of nuclear weapons questionable. But, if the U.S. does expand the type of events that could cause a nuclear response, the odds likely increase that such a response is forthcoming.

What is to be done?

Anyone born before 1960 can likely remember (depending, of course, on their pharmacological behavior during their teens and twenties) the civil defense instructions and drills that were part of childhood in the 1950s and early 1960s.5 “Duck and cover” drills and the omnipresent fallout shelters were designed to improve the chances of survival following a nuclear attack. However, by the late 1960s, it had become obvious that the likelihood and attractiveness of surviving a full-scale strategic nuclear attack were rather low. Both the U.S. and U.S.S.R. possessed enough warheads to destroy both nations and likely generate enough fallout to eliminate most human life. The concept of “nuclear winter” added to the pessimism.6

However, nuclear proliferation and the reintroduction of tactical nuclear weapons, coupled with the steady erosion of American hegemony, have increased the odds of a non-strategic nuclear attack on the U.S. or an ally. This brings us to the Hawaii false alarm. If North Korea were to attack Hawaii with a nuclear weapon, we would expect the Trump administration to respond with a massive strategic attack. After all, what credibility would the nuclear deterrent have without such a reply? However, that outcome isn’t a certainty.

China, Japan and South Korea would argue for a lesser response, simply because they would face radiation risk from the fallout. North Korea, realizing it was about to be hit with an existential attack, would not only launch missiles against the U.S. but likely also strike Japan and maybe South Korea. The surrounding nations would beg for a conventional counterattack. In any case, we still think the most likely outcome would be, to quote Colin Powell, that North Korea would be “a charcoal briquette.”7

However, the important takeaway from the Hawaii false alarm was that if it had been a real attack, the devastation would not have been widespread on the mainland. No doubt it would have been a disaster for our 50th state, though. But, these sort of nuclear attacks may be more common in the future. Instead of the despair of a nuclear war destroying the whole nation, it may be more common for smaller scale attacks to take place.

Simply put, we may be in a world where limited nuclear wars become the standard. This will require a rebuild of our civil defense facilities and re-education of the public on how to cope with a limited nuclear weapon.

Ramifications

The Hawaii incident was mostly a non-event for the markets. Of course, that’s because the primary problem was that the mistake terrified people and officials handled it poorly by not immediately correcting the mistake. Had the warning occurred during market hours, we would have expected a sharp pullback in equities and perhaps a rally in Treasuries, a fairly standard market reaction to a geopolitical event.

However, there is a more important issue to consider.

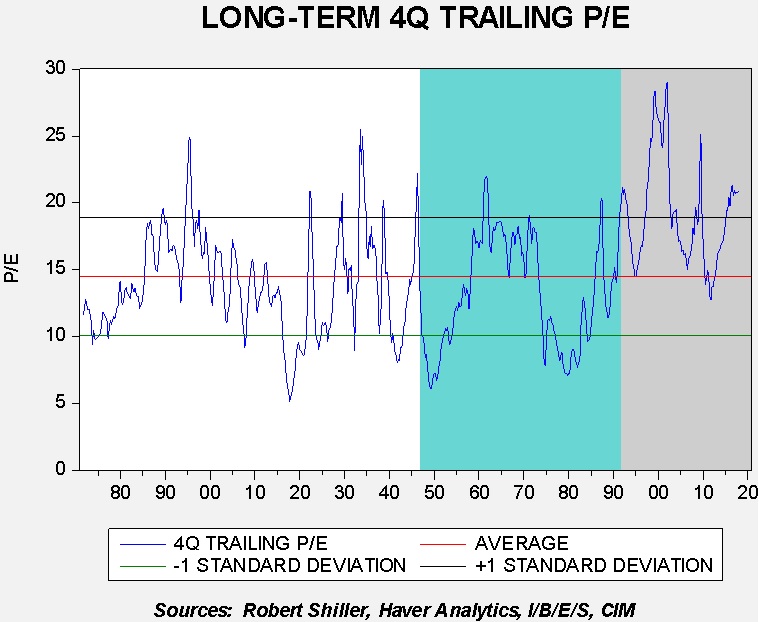

This chart shows the S&P P/E ratio since 1870. It’s on a four-quarter trailing basis except for the last two data points, which include forward consensus estimates for two quarters. The average and standard deviations are for the full time series. The gray shaded area marks the end of the Soviet Union. The blue shaded area represents the Cold War. Note that during the Cold War, the P/E ranged within the average and standard deviation. After the Cold War, the P/E shifted well higher; in fact, it has only approached average on three occasions since 1991.

If one assumes that P/E ratios are, at least in part, estimates of investor sentiment, then it makes sense that the end of the Cold War lifted that sentiment. After all, communism was a competing system of organizing government and addressing the economic problem.8 The end of communism meant that there was no legitimate competing system to capitalism and democracy.9 That outcome should be bullish for equities. In addition, the embedded fears that the Cold War would eventually lead to a hot war that could end human life on Earth must have had an effect on investor sentiment. The crowning of American hegemony and the unipolar moment meant that the U.S. and neoliberalism were ascendant.

Over the past decade, it has become evident that that expectation was overly optimistic. The U.S. unipolar moment is likely coming to a close and the world is rapidly becoming a more unstable and dangerous place. That doesn’t mean that the U.S. necessarily faces an imminent attack or that the changing world won’t be conducive to business success. However, it will be a more complicated world, as the Hawaii false alarm suggests. Part of the reason the mistake occurred was because workers were unfamiliar with the process of sounding the alarm. The lack of fear from a nuclear attack has led civil defense units to focus more on natural disasters. There is currently no evidence to suggest that nuclear proliferation has affected P/Es, but it would not be a huge surprise if, at some point in the future, investor sentiment is affected by the realization that we are living in a more dangerous world than when the Cold War ended. The Hawaii false alarm has the potential to change long-term investing sentiment. On the other hand, it would probably take something much more dramatic, like an actual nuclear conflict, to affect the long-term trend in P/E ratios. Still, this bears watching because such a shift would have a dramatic impact on equity values.

Bill O’Grady

January 29, 2018

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[1] See WGR, 1/22/18, Thinking the Unthinkable (Again): Part I.

[2] See WGR, 1/10/2011, Thinking the Unthinkable: Civil Defense.

[3] This is obviously an assumption because they have never been used in war.

[4]https://www.nytimes.com/2018/01/16/us/politics/pentagon-nuclear-review-cyberattack-trump.html

[5] https://www.youtube.com/watch?v=IKqXu-5jw60

[6] https://www.smithsonianmag.com/science-nature/when-carl-sagan-warned-world-about-nuclear-winter-180967198/

[7]http://fpif.org/diplomacy_by_dereliction_us_policy_toward_korea_is_in_disarray/

[8] The economic problem being how to allocate limited resources to unlimited wants.

[9] Made famous by Francis Fukuyama. See:

Fukuyama, F. (1992). The End of History and the Last Man. New York, NY: Avon Books.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management