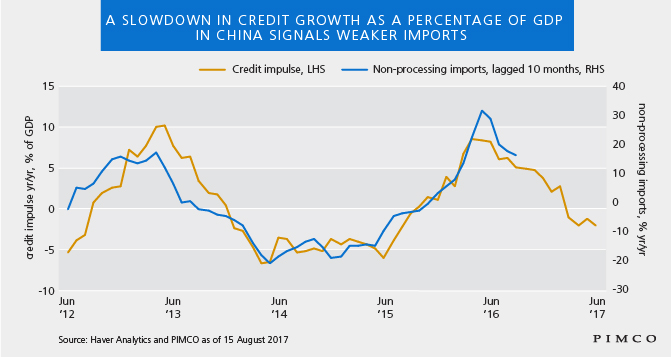

The use of credit to fuel growth in China is weakening, a trend that has begun to depress demand for imports. Given China’s seminal role as an engine of global growth, the ripple effects will weigh on growth prospects for the countries most exposed to Chinese demand, including those in Asia and Latin America.

When it comes to emerging market (EM) assets, deteriorating growth prospects inevitably create a tougher climb. However, differences with China's past credit cycles leave us comfortable with continued exposure to the asset class.

A different credit cycle

In many respects, this current credit cycle in China is similar to previous episodes. Chinese credit policy remains decidedly counter-cyclical: Regulators are responding to the 2014-15 credit boom after a solid, if belated, recovery in GDP growth. Our contention is that regulators have once again over¬tightened by failing to recognize the effects on the real economy of a crackdown on shadow banking. Nonetheless, the current slowdown is effectively policy-induced and can eventually be reversed.

The differences with past cycles, moreover, point to a softer landing ahead.

Major macroeconomic imbalances made previous downturns harsher. In 2008-09, for instance, demand from developed markets collapsed. In 2013-15, EM demand collapsed (as the taper tantrum intersected with a sharp tightening in the Chinese credit impulse, the change in the growth rate of aggregate credit to GDP. In 2018, neither of these sources of demand is likely to suffer similarly precipitous declines.

At the micro level, the earnings relief for firms in excess-capacity sectors such as mining and materials has been fading, but not collapsing. Stress in these highly indebted sectors lies at the core of our earlier concerns about traditional and shadow bank credit risks. Last year’s recovery in commodity prices buoyed profitability for excess capacity manufacturers, effectively bailing them out (temporarily) of a growing debt hole. As slowing activity and tightening credit begin to weigh on commodity prices, credit stress in these sectors should rise once again, albeit not to the extremes of 2014-15.

Compared to expected 2017 GDP growth of 6.7%, activity will likely need to slow to less than 6% before the Chinese authorities feel compelled to respond with easier credit. We would argue that the substantial credit headwind already baked into the growth cake makes this the base case for 2018. Any reforms or deleveraging undertaken after the 19th Party Congress in Q4 will add to the slowing trend.