The Mid-Year Geopolitical Outlook

As is our custom, we update our geopolitical outlook for the remainder of the year as the first half comes to a close. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

#1. The Political Fragmentation of the West

For most of the period following WWII through the end of the Cold War, Western governments were dominated by center-left or center-right governments. The fall of communism raised hopes of an “end of history”1 where democracy and capitalism won out and no other system of organizing society was realistically possible.

There were some thinkers who warned that ending the intellectual battle between capitalism/democracy and communism/ totalitarianism would lead to other problems.2 Samuel Huntington postulated that the world was instead heading toward a clash of civilizations. However, he saw the clash of civilizations in geopolitical terms. Instead, we are seeing it in domestic politics.

The term “loyal opposition” is used to describe the party out of power. Despite being out of power, this group would remain loyal to the government and the overall path of policy. Therefore, the party that loses an election still generally believes that the policies coming from the incoming government would be different only by degrees.

In the West, the concept of loyal opposition is fading. Elections are now being seen as “zero sum games.” Losing an election appears catastrophic; voters simply don’t like members of other parties and view them as enemies.3 The following quote captures this issue:

In 1960, just 5 percent of Republicans and 4 percent of Democrats said they would be unhappy if a son or daughter married someone from the other party. In a YouGov survey from 2008 that posed a similar question, 27 percent of Republicans and 20 percent of Democrats said they’d be “somewhat” or “very upset” by that prospect. By 2010, that share had jumped to half of Republicans and a third of Democrats.4

This situation isn’t just seen in the U.S.; Europe is developing similar traits. Brexit was a shocking outcome. The fact that PM May couldn’t secure a majority in recent parliamentary elections suggests that “leave” wasn’t all that popular. Perhaps more astounding is that the opposition is led by the Labour Party, run by a “paleo-socialist” who wants to renationalize major industries and essentially reverse Thatcher’s reforms. Meanwhile, the French have elected their youngest president of the Fifth Republic and his new party now holds a majority in the National Assembly.

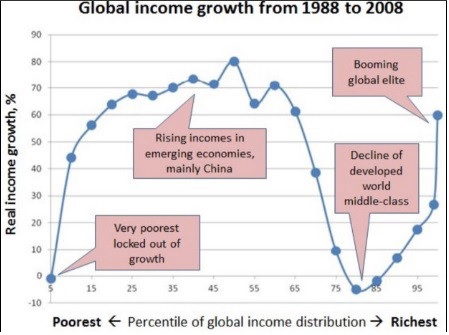

It appears that Western political systems are becoming increasingly disjointed. Why did this happen? The most likely culprits are globalization and deregulation. These policies were primarily responsible for taming the high inflation of the 1970s. Allowing firms to source production in the cheapest areas of the world, use immigrant labor that more easily moves into countries and introduce new technology and methods without serious regulatory restraint has greatly benefited the top 20% of the income brackets in most Western nations. The bottom 80% have missed out on the growth generated by globalization and deregulation.

(Source: Branko Milanovic, Medium)

This chart shows global real income growth in the two-decade period between 1988 and 2008. The developed world middle class did not participate in the global boom.

The tensions from globalization and deregulation have reached a critical point. We are seeing nations turn inward and support nationalist movements. For the world, the fact that the U.S. is deeply affected by these trends is dangerous. America, through its exercise of hegemony, has secured the sea lanes, made global commodities accessible, frozen age-old conflicts in the Middle East, Europe and Asia, and provided the reserve currency and a reliable source of export demand for developing nations. If the U.S. ends this practice, and it appears that we are, the world will steadily become a more dangerous place.

Political leaders need to create a new narrative of unity that offers hope and respect to those who have failed to participate in the globalized and deregulated world. If they cannot do so, wars will become more common. And, given the current degree of political fragmentation, working together will likely require an event to foster unity.

#2. North Korea

The situation with North Korea continues to deteriorate.5 The Kim regime appears driven to build a nuclear warhead and the delivery system to reach the U.S. mainland. The U.S. cannot allow such a threat to exist. The Trump administration has warned that it will consider a military option against North Korea to eliminate the threat against the U.S.

At the same time, the U.S. has leaned on China to persuade Kim Jong Un to back down. We doubt President Xi will have much success in convincing the North Koreans to give up their weapons program. The “Young Marshall,” as the new leader is known, is behaving as a leader still consolidating his power. In February, all indications suggest that North Korean agents brazenly assassinated his older brother in the gate area of a Malaysian airport using sarin nerve agents. The regime has reportedly executed over 500 officials, including 140 senior officials, in some cases by particularly brutal methods using anti-aircraft guns or flame throwers.6

A war could be avoided if: (a) the U.S. decides it can live with the threat; (b) China coerces North Korea to stop its nuclear program; or © a compromise is reached. The first option is very unlikely as is the second. The third option may be possible—the U.S. may allow the nuclear program to continue if the missile program doesn’t evolve to threaten the U.S. directly. Of course, that would terrify the rest of the region, raising fears that the U.S. is abandoning the region despite Kim Jong Un’s nuclear threats.

Recently, President Trump remarked that China had apparently failed to convince North Korea to give up its nuclear program but expressed gratitude that President Xi “had tried.” This comment could be a signal that the U.S. is preparing for military action by arguing that the best chance of diplomacy has failed. If this comment is taken that way, we could see more aggressive diplomatic efforts from China and South Korea to prevent a war. Unfortunately, President Trump makes so many comments expressing positions that don’t necessarily become policy, so it may be difficult for foreign governments to decipher what the president really means. This situation could actually increase the chances of a conflict.

A war with North Korea would be difficult. Although we would expect the U.S. to prevail, the number of casualties would be huge. Secretary of Defense Mattis has described a war on the Korean Peninsula as “catastrophic.” We would agree.

#3. An Unsettled Middle East

Ever since the Arab Spring, the Middle East has become more volatile. Many changes have occurred since 2010; arguably, Libya is no longer a functioning state. Assad has lost control of most of Syria. Iraq has lost control of significant areas due to the rise of Islamic State. Egypt has seen two changes in government leadership. Turkey has seen a rise in Kurdish nationalism to its south. Although the Gulf Cooperation Council (GCC) states avoided threats to their member governments, several GCC nations did increase social spending to maintain order.

Currently, there are two “hot” wars in the region, in Syria and Iraq against Islamic State and in Yemen. Qatar is under blockade as the other GCC nations are trying to force the emirate to adhere to Saudi whims. Saudi King Salman has recently demoted his nephew from the role of crown prince and appointed his son to that position, potentially creating an eventual succession crisis. The new crown prince has taken a hard line with Iran, which has offered aid to Qatar. Turkey has also supported Qatar with a small troop contingent. It should be noted that Qatar houses the U.S. Air Force at the Al Udeid Air Base; there are 11k American servicemen at the base with over 100 aircraft.

The U.S. has generally kept a “lid” on the region since WWII. That doesn’t mean that there haven’t been a number of events. The Iranian Revolution created an adversarial state for the U.S. The U.S. managed to keep oil flows open for most of the Iran-Iraq War. The Gulf War sent the signal that the U.S. would not tolerate forcible border changes in the region.

Unfortunately, the U.S. opened a Pandora’s Box in the region by overthrowing Saddam Hussein. The territorial integrity of Iraq has steadily deteriorated as the Kurds have created an autonomous region in the north and Islamic State has taken control of parts of western Iraq. The border between Iraq and Syria is not under full control of either state. In Syria, the civil conflict continues and has become a proxy war involving Iran, Russia and the U.S. Recently, U.S. warplanes shot down Iranian drones and a Syrian warplane.

Overall, the region appears to be in flux. As stability deteriorates, we could see a growing refugee problem for Europe and the potential for the disruption of oil flows.

#4. A Resurgent Russia

The Russian economy was able to recover in the last decade due to rising oil prices. The economic recovery led the Russian political leadership, embodied in Vladimir Putin, to restore Russia’s long-term geopolitical goal of creating buffer regions to its west and south. Russia mostly sits on a plain. To protect itself, Russian leaders throughout history have expanded their influence into the “near abroad” to force invaders to extend supply lines. This is a proven defense method, defeating Napoleon and the Third Reich. After WWII, the Soviets controlled Eastern Europe, much of the Caucasus region and Central Asia.

Russian history also shows that it’s expensive to maintain this buffer and, occasionally, the area of control contracts. Over time, after these periods of retreat, Russian leaders have worked to restore the buffer. To a great extent, that is what Putin is attempting to accomplish now. He is trying to create a Eurasian free trade zone. Geopolitically, Russia must have a friendly power in Ukraine or the core of the Russian state is not defensible. Thus, NATO’s consideration of Ukrainian membership was ill-advised unless the treaty organization (read: U.S.) was prepared to go to war with Russia. Georgia is not quite as critical as Ukraine but still very important and Putin wasn’t going to allow Georgia to join NATO, either.

Just because Russia wants to expand its influence into its near abroad doesn’t mean the West must acquiesce. At the same time, Western leaders should expect Russia to behave this way and if they don’t want to allow Russian influence to expand then they have to be prepared to expend resources to prevent it. Without U.S. leadership, the odds favor an expansion of Russian influence, which is a negative outcome for the former Eastern Bloc.

#5. China’s Financial Situation

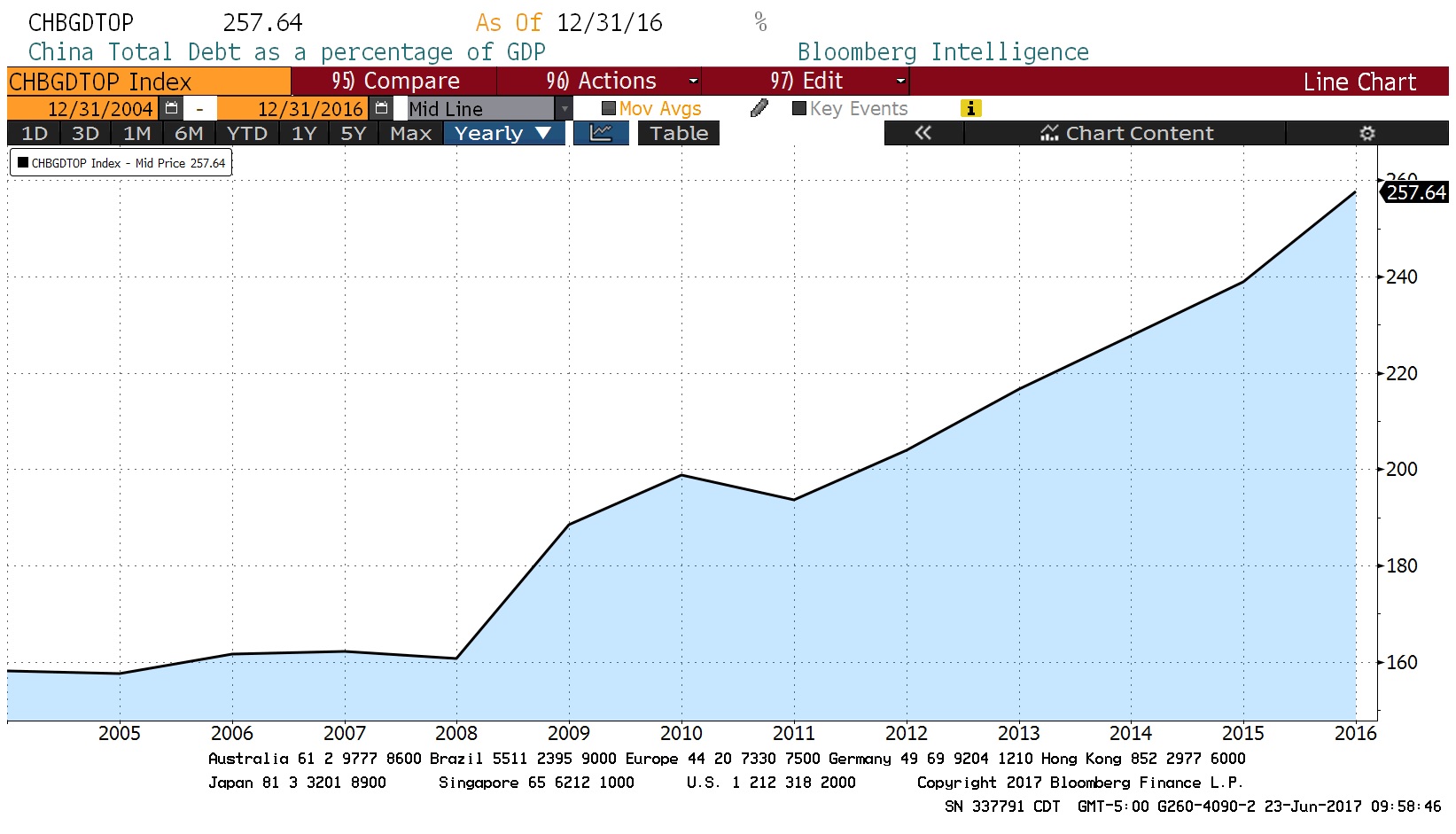

China’s debt has been growing at a furious pace. As the chart below shows, since the financial crisis, China has been taking on debt rapidly in order to maintain economic growth.

(Source: Bloomberg)

Rapid debt growth has been associated with economic crises in other nations. China does have high household savings rates that, so far, have protected the country from a financial crisis. However, this rapid rise in debt will almost inevitably lead to malinvestment and a rise in non-performing loans. The key issue is how the losses are allocated. In the past, China has allocated loan losses to the household sector. We suspect that will happen again.

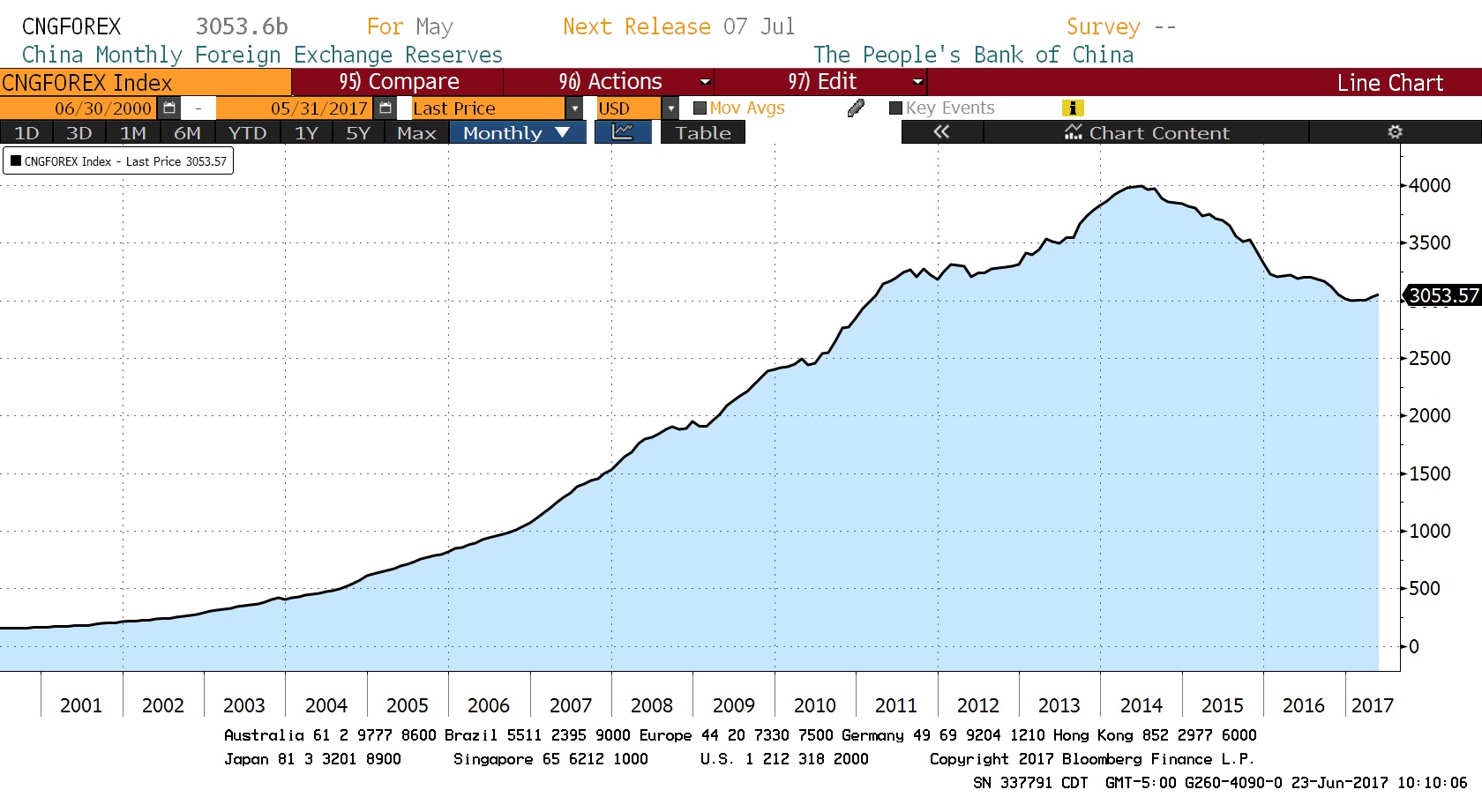

However, there is a concern that households and others may be worried about the assignment of losses or worse. Foreign reserves have been falling steadily for two years, although they have stabilized so far this year. They are still down almost 24% from the peak in 2014.

(Source: Bloomberg)

Late last year, the Chinese government implemented more stringent rules to prevent money from leaving China. These measures have worked to arrest the decline but are not consistent with other measures to open Chinese financial markets.

Some of China’s capital flight is coming to the U.S. Local West Coast real estate markets have become targets of Chinese investors.7 Although capital flight is a benefit for the foreign nations that receive the flows, it could destabilize China’s economy.

The Communist Party of China (CPC) is holding its annual meetings in October. This year’s meetings are of significant importance because President Xi will select a new Standing Committee of the Politburo. In China’s system, a president becomes more powerful in the second five-year term because he gets more say in the selection process of Politburo members. Xi will want to avoid major crises before October, fearing it could undermine his influence. In the long run, China needs to grow at a much slower pace, probably around 3%, to stop the rise in debt levels (China can grow at almost any level it wants as long as it can increase its debt). Cutting growth to sustainable levels will be very difficult; if Xi is going to be able to make this adjustment, he will need a solid cast of CPC members in the Politburo to support him. Thus, we expect the Chinese economy to avoid major spills until after the October meetings.

Ramifications

Overall, the most acute problems are North Korea and Russia. However, we ranked the political fragmentation of the West as the first problem because it has the potential to generate the most surprises for the financial markets. Wars in North Korea or the Middle East would be majorly negative for financial markets but there would likely be enough signaling from the participants to prepare for problems. On the other hand, political fragmentation has yielded surprises like Brexit, Donald Trump, Jeremy Corbyn, etc. These events have caught financial markets off guard and additional events could undermine the bullish market sentiment that has been in place this year.

Overall, the message to investors is that we are in a situation where some degree of caution is warranted. We have seen a rather impressive rally in Treasuries this year despite FOMC policy tightening and hopes of fiscal stimulus. We suspect some of this rally is due to investors holding some “insurance.” This will probably become a bigger factor for the rest of 2017.

Bill O’Grady

July 10, 2017

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

5 For details, see our recent two-part WGR series on The Second Korean War: Part I, 6/19/17; and Part II, 6/26/17.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management

(Source: Bloomberg)

(Source: Bloomberg) (Source: Bloomberg)

(Source: Bloomberg)