At the NATO meetings late last month, the German media reported that President Trump had called the Germans “bad” for running trade surpluses with the U.S. The president threatened trade restrictions, focusing on German automobiles. Needless to say, this comment caused a minor international incident.

Although such incidents come and go, it did generate a more serious question…are German policies causing problems for the world? In this report, we will review the saving identity we introduced in last month’s series on trade and discuss how Germany has built a policy designed to create saving. We will move the discussion to the Eurozone and show the impact that German policy has had on the single currency. From there, we will try to address the question posed in the title of this report. We will conclude, as always, with market ramifications.

The Saving Identity

In the month of May, we published a four-part report on trade that is now combined into a single report.[1] In that report, we introduced the saving identity.

(M - X) = (I - S) + (G - Tx)[2]

The saving identity states that private sector domestic saving (I - S) plus public sector saving (G - Tx) is equal to foreign saving. If a country is running a positive domestic savings balance, either by investing less than it saves or by running a fiscal surplus, it will run a trade surplus (X>M). In public discussion, trade appears to be all about jobs, relative prices, trade barriers, etc. However, regardless of how nations interfere with trade, the saving identity will always be true. As we noted in the aforementioned report, tariffs, exchange rate manipulation and administration barriers will, in the final analysis, be explained through the saving identity.

In the process of economic development, nations must build productive capacity through investment. Both public and private investment are necessary for success. Public investment in infrastructure, roads, bridges, canals, etc., are critical to supporting private investment. In capitalist societies, a legal framework to adjudicate contract disputes and support the enforcement of agreements is also necessary and mostly provided by the public sector. Private investment usually occurs along with public investment. But, all investment requires funding, which comes from saving. That saving can come from both domestic and foreign sources.

Usually, nations that are building productive capacity create policies that either generate domestic saving or attract foreign saving. There are various policies that can support the effort to build saving. Trade restrictions can restrain consumption by raising import prices. High taxes are sometimes used to create public saving; savings schemes to funnel household saving into the private market are also used. And, through a trade deficit, foreign saving can be acquired.

The process of development is fraught with risk. Investment is always hard because it involves making projections about the future and it’s easy to make mistakes. Malinvestment can slow economic growth and lead to financial crises; after all, most investment is funded by debt.

As a nation achieves developed status, the need to restrain consumption declines. Clearly, there will always be a need for investment regardless of the level of development even if it is nothing more than to offset depreciation. An example is the U.S. interstate highway system; although it is being constantly repaired and upgraded, the need to build another highway system is unnecessary.

Thus, over time, as a nation becomes increasingly developed, one would expect to see rising levels of consumption relative to overall GDP. However, this process can become stalled if political constituencies, who have benefited from consumption-constraining policies of development, prevent the transition from occurring. If this happens, policy can become “stuck” and such a nation will continue to promote exports, which means they are capturing demand from abroad.

German Economic Policy

Because Germany is part of the Eurozone and the European Union, its trade policy is set by these two bodies. Thus, overt trade barriers are not put in place by the German government. However, Germany does engage in policies that lead to trade surpluses.

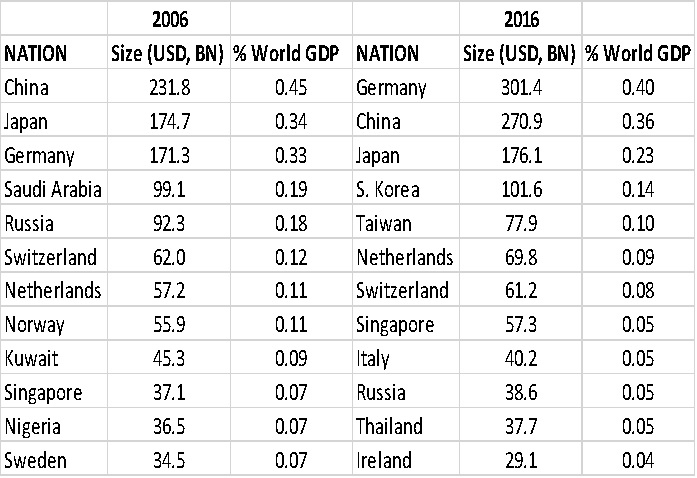

Here are the 12 largest current account surplus nations from 2006 and last year. As the table indicates, Germany has moved up from the third largest surplus to the largest in the world. China and Japan are also large; the former is still considered a developing nation, so its surplus, though controversial, is somewhat understandable. Japan continues to have a saving surplus that no Japanese administration has been able to successfully address. It is also worth noting that in 2006, due to high oil prices, a large number of Middle East oil producers were in the rankings. Lower oil prices did affect the rankings in 2016.

(Sources: IMF, CIM)

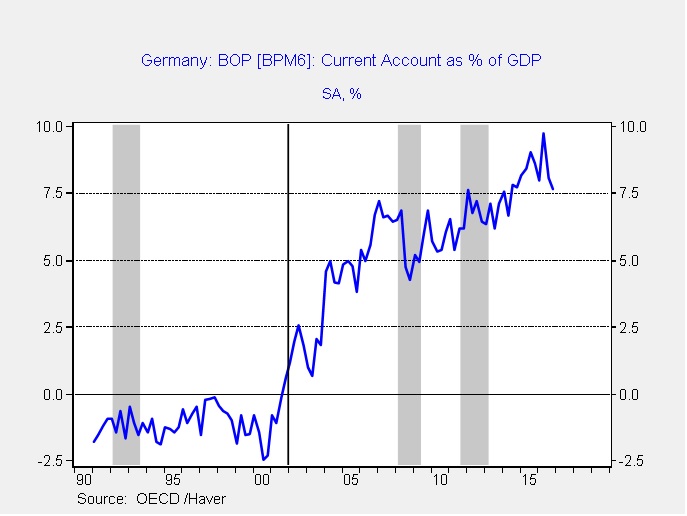

Germany’s current account surplus has been rising since the euro was adopted as the single currency of the Eurozone. The vertical line on the chart below shows when the single currency became legal tender in the Eurozone.

German GDP data suggests that consumption has been constrained.

This chart shows consumption as a percentage of GDP for both Germany and the U.S. Until the mid-1980s, German and U.S. consumption trended higher, with German consumption increasing at a faster rate. However, by the mid-1980s, German consumption had slumped and has recently declined even further. Meanwhile, U.S. consumption continued to rise into the Great Financial Crisis and has stabilized around 68% of GDP. It is arguable that U.S. consumption is inflated by the reserve currency role; if U.S. consumption fell, it would likely trigger a global recession. But the fact that German consumption has declined is troublesome. Although an aging population may be part of the reason, we note that similar data from Japan, clearly an older and fast aging economy, is currently 56% of GDP and was nearly 60% in 2014.

Although it is commonly held that trade imbalances occur due to tariffs, quotas and exchange rate manipulation, in reality, imbalances occur due to basic macroeconomics.[3] To show how this works, let’s again refer to the saving identity:

(M - X) = (I - S) + (G - Tx)

Consider the following, where the equation in black represents the home nation and the equation in red is the rest of the world:

(X - M) + (I - S) + (G - Tx) =

(I - S) + (G - Tx) + (X - M)

What is often missed in the analysis is that there is a focus on a single nation. If a home nation creates an imbalance that generates a trade surplus, by definition, a trade deficit must be created in the rest of the world. Assume the home nation creates a policy where S>I; if the government doesn’t absorb the excess saving, the equation is balanced via a trade surplus that generates a trade deficit in the rest of the world. In the rest of the world, the resulting trade deficit is balanced by either a rise in private investment in excess of saving or by a fiscal deficit.

This relationship characterizes what happened in the Eurozone. The Eurozone is not just the region that uses the single currency; it is a subset of the EU which is a free trade zone. Thus, nations cannot use currency depreciation or overt trade barriers to offset macroeconomic policies designed to generate trade surpluses in another Eurozone member state.

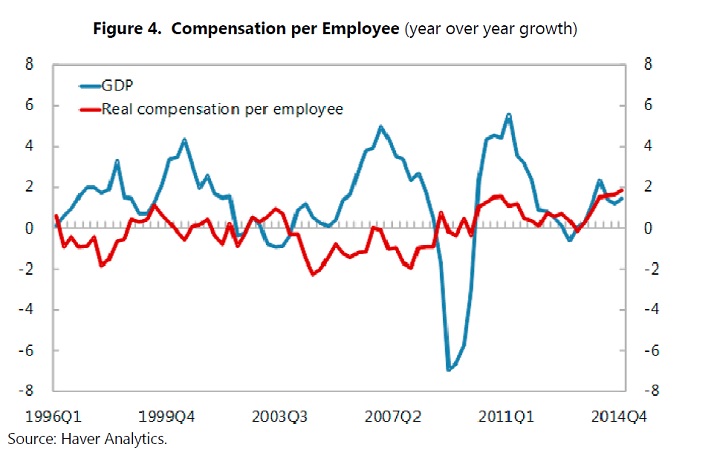

Starting in 2003, Germany instituted a series of labor market reforms called the Hartz Plan. These reforms loosened restrictions on employment and eased rigid compensation rules. The effect was to reduce real compensation.

(Source: IMF[4])

Note that from 2003 into 2008, real worker compensation in Germany was negative while real GDP rose. Referring to the saving identity, the drop in wages would constrain consumption and boost saving. The excess saving led to the rapid expansion of the current account surplus, shown above.[5]

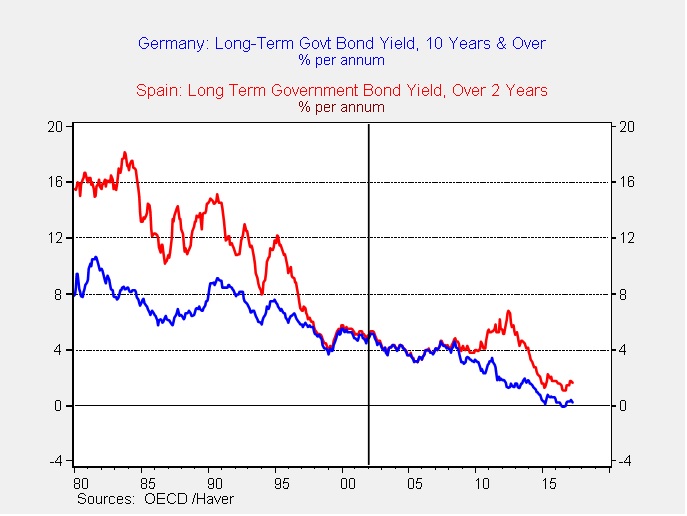

German austerity coincided with strong expansions in other parts of Europe, especially the southern tier, which benefited from falling interest rates. These countries, which had years of high inflation and elevated interest rates, found themselves able to borrow at German interest rates. This led to consumption and building booms in several Eurozone nations, including Spain.

Note that Spanish interest rates converged on German rates as the single currency was implemented. This drop supported Spanish consumption during the same period of German labor market austerity.

So, are the Germans “bad”?

Germany’s policies have exacerbated global imbalances. The 2008 Great Financial Crisis was followed by a series of Eurozone crises that started with Greece in 2010 and spread to Ireland, Spain, Italy and Portugal. These nations all faced debt problems; in Greece, it was mostly government debt, while in Spain and Ireland, it was housing debt.

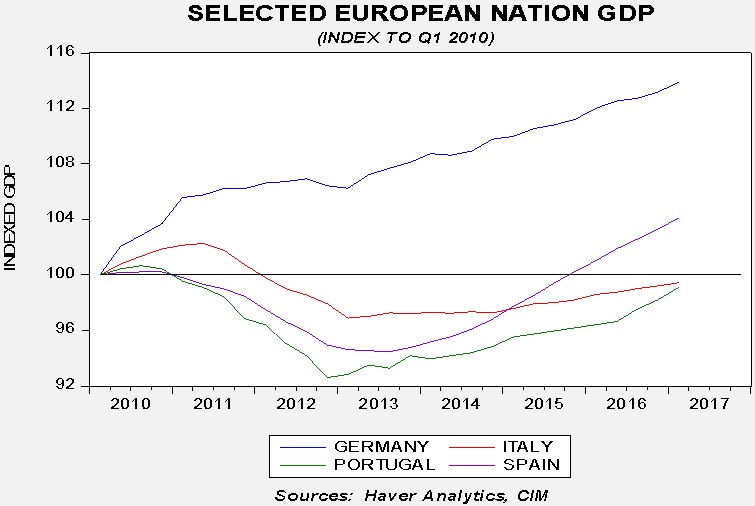

Germany’s response to the crises has been to call for austerity in the affected nations. And, there is solid evidence that they have followed these instructions. In the chart below, we indexed the levels of real GDP for Germany, Portugal, Italy and Spain. Only Spain is above the 2010 level.

Germany could help ease the adjustment process by expanding fiscally and boosting private investment. However, the German political narrative is that the problem nations in the Eurozone brought this crisis upon themselves and need to perform the same austerity Germany engaged in when it implemented its labor market reforms last decade.

So, using the saving identity, let’s examine how the southern tier nations can resolve this problem.

(M - X) = (I - S) + (G - Tx)

Germany wants these nations to run fiscal surpluses (at least at the primary level, which excludes interest payments). That means Tx>G. Austerity tends to depress investment and consumption, and thus boosts saving relative to investment. If Tx>G and S>I, by definition, these nations must run a trade surplus. As the GDP chart above shows, austerity tends to lead to weaker growth. However, given Germany’s strong productivity, it will be quite difficult for the southern tier to export to Germany. Thus, to make the saving identity work, the southern tier must run its surplus with the rest of the world.

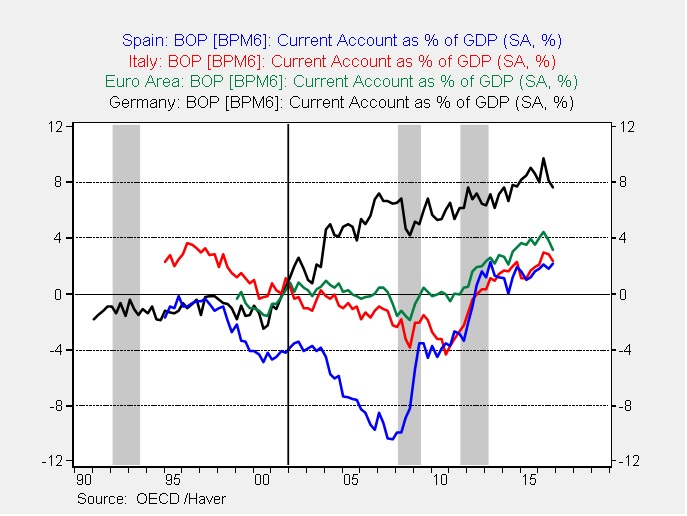

The chart below shows exactly what has happened. From the time the euro was fully implemented as legal tender in Europe, Germany has run a large current account surplus. The Eurozone as a whole did not until 2010, while Italy and Spain achieved surpluses a couple of years later.

Essentially, Germany’s solution to the problems of the Eurozone was for these nations to all run macroeconomic policies similar to Germany. This only works if the rest of the world is willing to accept the Eurozone’s export surplus.

And so, to answer the question raised by the title of this report, Germany isn’t necessarily bad because it sells cars to the U.S. or even because it runs a bilateral trade surplus with the U.S. However, we can argue that Germany’s policy stance is a problem, not only because it absorbs aggregate demand from the rest of the world by restraining consumption, but also because it magnifies this effect through its dominance of the Eurozone. The German policy of creating current account surpluses is similar to what European colonial powers deployed in the 18th and 19th century. And, by forcing austerity on southern Europe, it is slowly turning the Eurozone into a “Greater Germany” in terms of economic policy. Thus, President Trump’s dispute with Germany isn’t wrong but it is somewhat misplaced—the world and Europe could use more consumption and a narrower trade surplus from Germany.

Ramifications

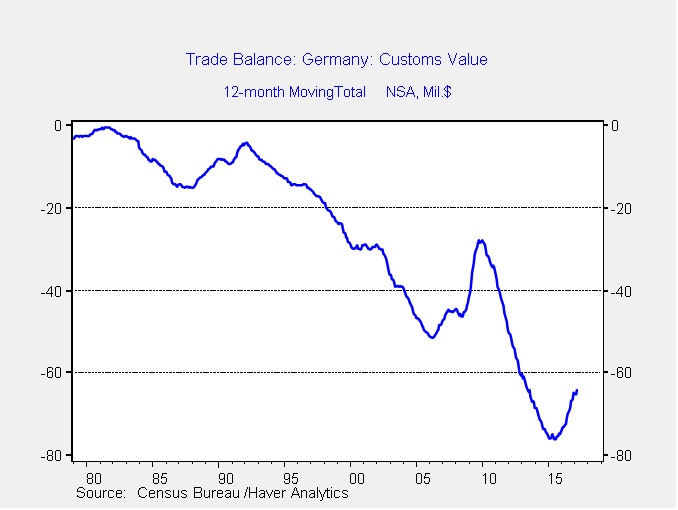

Germany runs a large trade surplus with the U.S.

On a rolling 12-month basis, Germany has a surplus of $63.4 bn. This is the third largest, after China’s $347.9 bn and Japan’s $69.4 bn. And, the Eurozone’s $125.9 bn deficit has widened since the series of Eurozone debt crises began in 2010, when it was a mere $50.2 bn.

If this bilateral trade relationship is a problem for the Trump administration and he wants to narrow the trade deficit with Germany/Eurozone, what options are available?

Implement U.S. austerity: Using the saving identity, the U.S. could force a reduction in the trade deficit by raising taxes and running a fiscal surplus. Although the White House doesn’t set interest rates, he could encourage the Federal Reserve to tighten monetary policy. However, the goal of reducing the trade deficit is really about increasing employment. Thus, this option is highly unlikely.

Deploy trade barriers: The U.S. could implement trade barriers on European goods. This may run afoul of WTO regulations, although we doubt the Trump administration would care. Still, deciding how to implement trade barriers is difficult and it runs the risk of Europe responding in kind. This may actually lead to job dislocations in the U.S.

Depreciate the dollar: The administration could start “jawboning” the dollar lower through public pronouncements and could intervene directly in the currency markets to push the dollar lower. However, the most effective way to weaken the dollar would be to deliberately appoint dovish governors to the FOMC. President Trump has three openings on the committee now and will likely have two more next year. By filling the committee with governors committed to reflating the economy, the dollar would likely weaken and improve American trade competitiveness.

Of the three, we believe the most likely is currency depreciation. A stronger euro would lead to a narrower trade deficit with the Eurozone and avoid the political problems and retaliation that come with trade barriers. Given Germany’s preference for a strong currency, we would not expect much pushback from Berlin. A weak dollar policy would be opposed by the establishment wing of the GOP but the nationalist wing would likely come to embrace such a policy. For this reason, investors should probably expect a weak dollar policy to evolve in the coming months.

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[2] Imports (M), exports (X), investment (I), saving (S), government consumption (G) and taxes (Tx).

[3] See aforementioned WGR trade series and:

Pettis, M. (2013). The Great Rebalancing: Trade, Conflict and the Perilous Road Ahead for the World Economy. Princeton, NJ: Princeton University Press.

[5] Interestingly enough, Germany had a fiscal deficit of over 3% of GDP from 2003 to 2006. A sharp drop in private sector investment, which fell from 23% of GDP in 2000 to under 19% of GDP by 2005, suggests that labor market austerity led to a drop in investment that contributed to excess private sector saving and the current account surplus.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management