This is the final report of our four-part series on trade. This week, our discussion on trade continues with a look at the relationship between trade, employment and inflation. We will also conclude the series with market ramifications.

What are the tradeoffs of trade?

Trade is part of a broader societal tradeoff between equality and efficiency.1 To function, societies need some degree of both. Nations with a high level of inequality tend to become politically unstable. At the same time, perfect equality tends to stifle initiative and prevent the building of productive capacity. Efficiency helps an economy provide goods and services at reasonable costs. Complete inefficiency makes everyone poor.

Okun’s insight is that societies balance equality and efficiency to maintain order. What we observe in history is that there doesn’t appear to be a balance point; in other words, this isn’t an optimization problem. Instead, we see broad periods of oscillation where one goal or the other is waxing or waning.

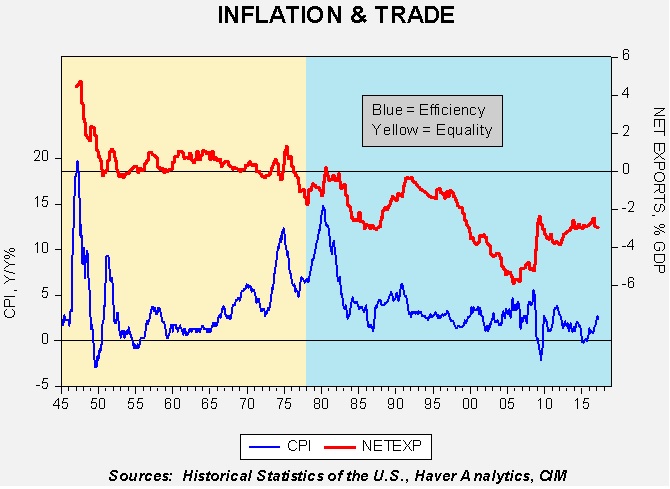

When society needs to improve its efficiency, it prefers globalization. This goal can lead to a trade deficit. The chart below overlays the yearly change in U.S. CPI with net exports as a percentage of GDP. We have shaded the chart in yellow and blue; the former represents a period when equality was the primary focus of policy and blue is when efficiency was the primary goal.2 Note that as inflation fell the trade deficit widened. Essentially, inflation fell by forcing U.S. firms to face increasing competition.

At the same time, this drive to efficiency created increasing inequality.

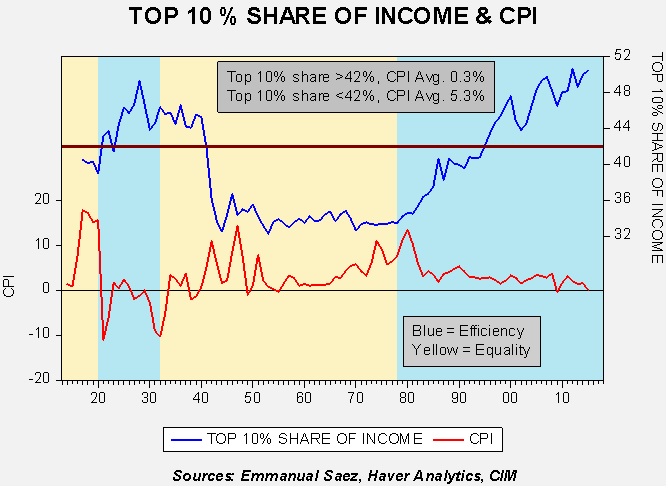

The chart above shows the yearly change in CPI with the top 10% share of national income. Again, we have defined equality and efficiency periods using the same color scheme over a longer period. As the box on the chart shows, inflation tends to be low when the top 10% of households are taking 42% of national income or more.

Perhaps the best way to think about trade is that we are all consumers and, in that way, we benefit from imports which increase the supply of goods and services and lower their prices. However, when a worker competing against these imported goods and services finds his job in jeopardy or becomes unemployed due to trade, the attractiveness of free trade to that worker is reduced significantly. Simply put, lower priced imports seem to only be a benefit if they don’t threaten my livelihood.

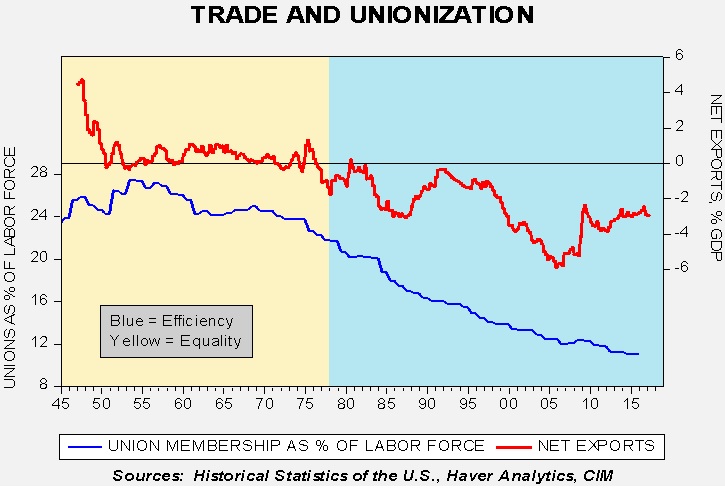

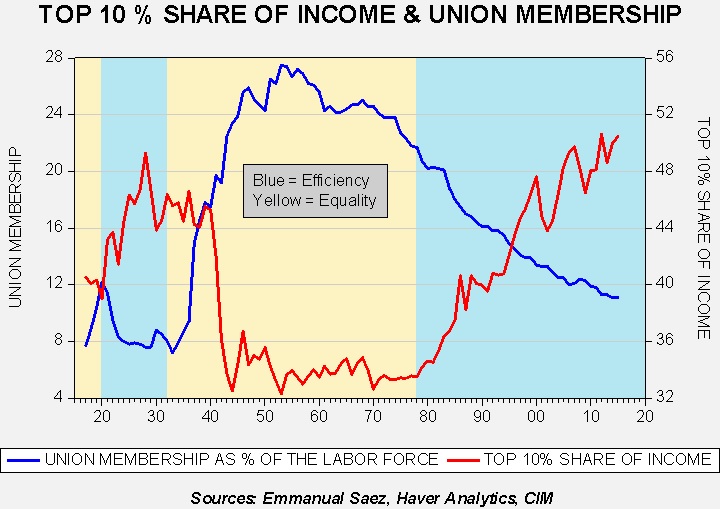

Unions flourish in environments where supply is concentrated and constrained. As this chart shows, the widening trade deficit accelerated the decline of the union movement in the U.S. This decline coincides with lower inflation.

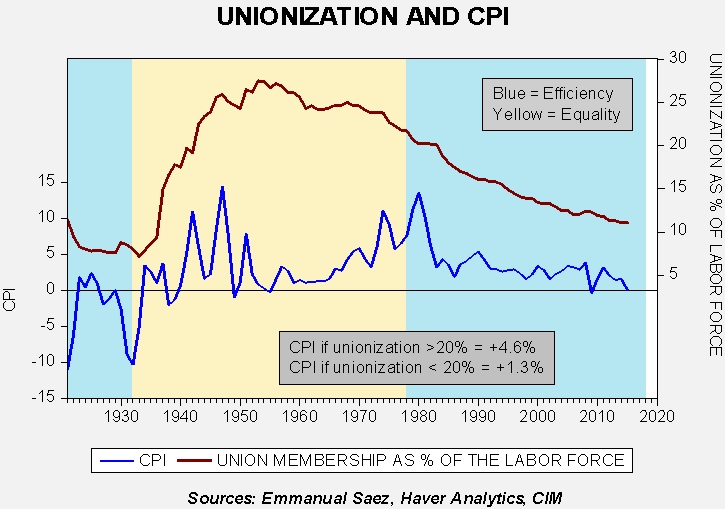

As the box shows, when unionization is under 20% of the labor force, CPI is significantly lower than when unionization is at a higher level.

Finally, to complete the argument, this chart shows the effect of unionization on inequality.

This chart overlays unionization as a percentage of the labor force with the top 10% share of national income. It shows that unionization is inversely correlated at the 90.3% level with the amount of income captured by the top 10% of households.

When the Trump administration argues that trade has worked against the U.S., the above charts describe the issue. Trade lowers inflation at the cost of inequality. Unions played a role in reducing inequality at the cost of higher inflation. Trade barriers should also reduce inequality at the cost of higher inflation.

Again, referring to the saving identity, where the private investment/savings balance (I-S) plus the public spending balance (Govt-Taxes) is equal to the trade account, M-X (Imports less Exports):

(M - X) = (I - S) + (G - Tx)

Higher inflation will likely boost saving by reducing consumption. As goods rise in price, household real income will likely decline. As S rises relative to I, assuming no change in the fiscal balance, imports should fall relative to exports.

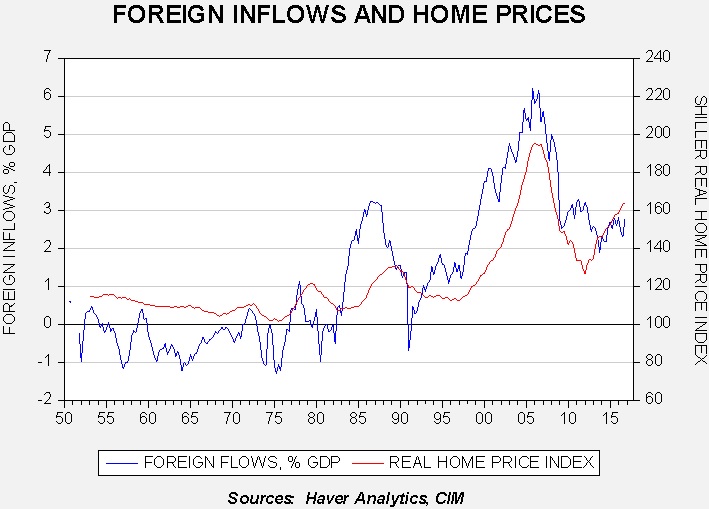

There is one other factor that a trade deficit brings. As we noted last week, former Fed Chairman Bernanke suggested that during the last decade the U.S. was dealing with a savings glut that was keeping Treasury rates lower than would be expected with the FOMC tightening policy at the time. When a nation runs a trade deficit, it’s really importing foreign saving. If a nation is in need of investment and can’t generate it domestically, these inflows are supportive. However, if there is a lack of prudent investment opportunities, the inflows can lower interest rates and spur imprudent behavior.

This chart shows real home prices and foreign flows. Although the relationship prior to the mid-1990s was not overly strong (+56.5%), from 1995 to the present it increases to 81.5%. Although the housing bubble wasn’t just due to the savings glut, it does appear that it was a contributing factor.

Obviously, some of this is due to the dollar’s reserve currency status. By being the global importer of last resort, the U.S. is open to trade and thus will face foreign inflows. Unfortunately, as the U.S. economy’s relative size to the world economy contracts, the potential increases for these inflows to distort American financial markets and cause “bubbles.”

If the U.S. reduces its trade deficit, what happens to the rest of the world?

In the 1920s, it was becoming apparent that Britain was struggling to maintain its role as the global importer of last resort. The dollar was becoming the de facto reserve currency but the U.S. did not want the burdens that accompanied that role. In response to a rapidly weakening economy, the U.S. passed the Smoot-Hawley tariff. Other nations retaliated and global trade contracted.

The 1930s showed that nations that were net exporters tended to struggle more than net importers. During WWI, the U.S. had become a major exporter and wanted to maintain that position. At the same time, the world wanted dollars and tried to acquire them by exporting to the U.S. The trade war reduced U.S. exports.

Exporting nations often have excess productive capacity. As growth slows, this capacity acts as a drag on future investment. For importing nations, there is often a general lack of productive capacity. When trade impediments become widespread, importers tend to build capacity which boosts investment. This is usually accompanied by higher inflation which reduces real income and lifts saving to fund the investment. This investment may prove to be less efficient than what is available overseas. Nonetheless, it does boost the importer’s economy. The Depression years showed that exporting nations tended to face greater struggles.

Accordingly, if the U.S. decides to forcibly reduce the trade deficit through tariffs and quotas (or by depreciating the dollar), the outcome will likely be higher inflation but more employment. On the other hand, the world’s major exporters—China, Germany and Japan—would likely face a significant slowdown in growth.

Wouldn’t adopting this position on trade signal an end to the superpower role?

Perhaps. Or the U.S. could force foreign nations to build productive capacity in the U.S. to reduce the trade deficit. Although that may increase the trade deficit in the short run, it would create jobs in the U.S.3

(M - X) = (I - S) + (G - Tx)

Again, using the saving identity, as I rises from foreign investors, and nothing else changes, foreign saving must fund it. However, once the investment is made, future investment becomes less necessary, increasing the odds that I<S in future years, reducing the trade deficit.

If the U.S. is no longer willing to act as the importer of last resort, the Japan Model of development probably no longer works. Although it isn’t necessarily an end to the superpower role, it will change in ways that are difficult to predict and could create a world where we see the rise of regional hegemons that will more likely use some form of colonization to avoid the problems that come with excess productive capacity.4

So, how should we view a trade deficit or surplus?

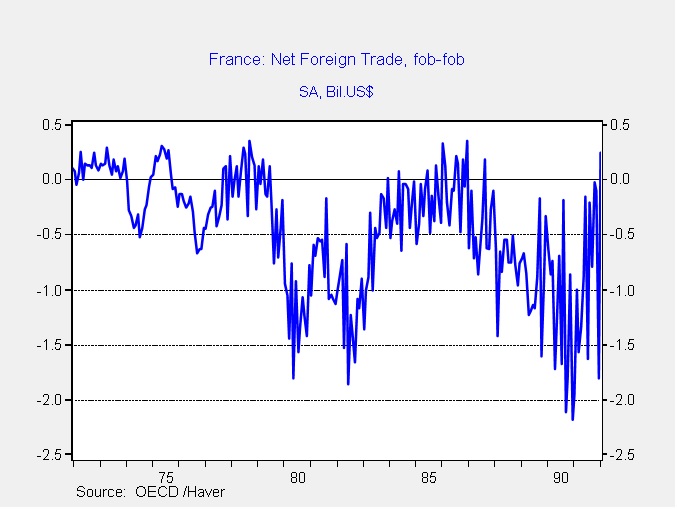

Perhaps one of the biggest misunderstandings I have tried to address over the past four weeks is that having a trade deficit doesn’t mean a nation is a country of spendthrifts, and running a surplus doesn’t make a nation morally superior. The trade account is complicated. Sometimes, it becomes fairly clear that the behavior of a nation leads to a trade deficit. For example, in France during the early 1980s, François Mitterrand, a Socialist, ran on a platform of fiscal stimulus. The outcome was a rise in the trade deficit and little growth. As the chart below shows, the French trade deficit ballooned in the early 1980s after Mitterrand’s stimulus mostly funded imports.

Again, using the saving identity, if G>Tx, and private saving fails to rise, the trade deficit must rise. Eventually, Mitterrand had to reverse these policies.

This example should be a cautionary tale for the Trump administration. The saving identity shows that if taxes are cut, either domestic saving must rise to offset the fiscal deficit or the trade deficit will rise. If the administration tries to prevent the trade deficit from rising either by tariffs or a rising dollar, domestic saving will have to rise. If incomes rise sharply due to rising domestic growth, the saving could be generated in such a way that the economy could still grow and fund the fiscal deficit.5 However, given that the tax cuts will mostly benefit the higher income brackets, it is quite likely that domestic saving will rise and be funneled into financial assets which would boost already aggressively priced financial markets.

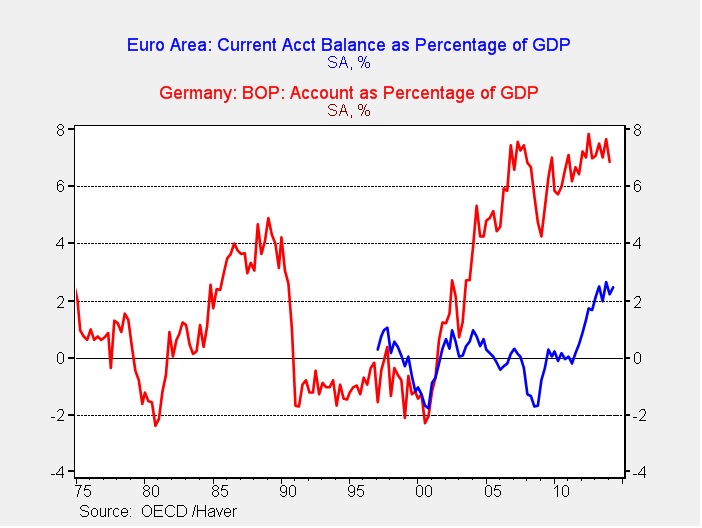

Here is an example where a nation ran a trade deficit because other nations ran surpluses. A good case could be made that excessive German saving caused trade deficits in parts of the Eurozone that could not be resolved by depreciation. The trade deficit, or the rise in the flows of saving from Germany, led to housing bubbles in Spain and Ireland. The German position is that other nations need to restructure to become like Germany. The problem is that it begs the question—who will absorb the exports?

This chart shows the current account as a percentage of GDP for the Eurozone and Germany. Since the onset of the Eurozone in 1999, Germany has been running a very high current account surplus. Until the Great Financial Crisis, the Eurozone mostly experienced a balanced current account or a slight deficit. Since the onset of various debt crises in Europe, the entire Eurozone is now running a current account surplus. Again, this only works when “somebody” (read: the U.S.) absorbs the exports.

We may be reaching the point where the U.S. is unwilling to continue providing the reserve currency due to the distortions it causes to U.S. financial markets and the inequality it causes. If that is the case, the world economy is vulnerable to a trade shock.

Ramifications

The ramifications for markets are complicated. But, there are a couple of trends that appear most likely to occur.

The Japan Model may not be sustainable. The Japan Model of development has clearly been the most successful development model in the postwar era. Because there is a tendency to moralize trade (surpluses are evidence of superiority), it is assumed by many that this model works because citizens do the right thing and save (another individual virtue that suffers from the fallacy of composition). Although the model is often characterized as “export promotion,” it is probably better thought of as “investment promotion”; it only works if there is an active “importer of last resort.” If the U.S. decides to no longer support that role in a fashion consistent with the postwar period, nations using this model will be faced with difficult choices. One is to accept long-term stagnation due to overcapacity; this is what Japan has done. The other is to follow the time-honored path of imperialism, which China may be attempting. Of course, colonialism needs American acceptance as well. It remains to be seen if the U.S. will allow the return of imperialism. If the Japan Model is no longer feasible, everything we know about development and emerging markets has to be reexamined. This doesn’t mean that one shouldn’t invest overseas, but the risk metrics may be different than expected…in other words, there may be more risk there than is currently being discounted.

If the U.S. decides to actively reverse the trade deficit, inflation is the most likely result. Although the U.S. could reduce the trade deficit by running fiscal surpluses, it is highly improbable that this outcome would be adopted. Thus, raising domestic saving in order to reduce the trade deficit will likely require falling real wages which would constrain consumption. Higher inflation would be the mostly likely way to reduce real wages. Higher inflation will, over time, lift long-duration asset yields and weaken prices. In other words, long-term rates will rise and P/E multiples will contract.6 Simply put, policies designed to narrow the trade deficit are not friendly to capital in general.

Trade isn’t really a bilateral exercise and treating it that way becomes a game of “whack-a-mole.” If the goal of policy is a narrower trade deficit, the avenues to accomplishing that goal include boosting saving by cutting government spending, raising taxes and reducing consumption or investment. However, if the real goal is to coerce changes in behavior from individual nations, then selective tariffs and currency appreciation will work but just won’t change the trade account. In other words, if we target China for tariffs but don’t address the saving identity then other nations will replace the imports lost from China.

Taxing consumption might be the best way to reduce the trade deficit. Raising the cost of consumption would likely lift saving. However, that may not make citizens happy and for the reserve currency provider to tax in this fashion would be profoundly detrimental to the world economy. Reducing the trade deficit is really an exercise in boosting domestic saving. Such policies, commonly called “austerity,” are not popular. In the end, the political classes really want jobs for their citizens. Trade restrictions may not be the best path to achieve that goal.

Finally, in broad terms, there are three classes in any economy—labor, capital and consumers. All of us fall under the third category, but are also divided between the first two categories. It is difficult to craft policies that favor all three categories; usually, one or two benefit, while one is adversely affected. Trade tends to support the interest of capital and consumers, but can hurt labor. Restricting trade can hurt capital and consumers, but helps labor. There is some degree of confusion around this concept. It is commonly asserted that trade helps “everyone” through lower prices. Although that is usually true, if one loses one’s job to imports, low prices aren’t much comfort.

Low inflation tends to help all three categories but it mostly helps consumers and capital. During equality periods, where labor tends to be supported, firms tend to pass along price increases. Thus, consumers tend to suffer from rising prices. If U.S. policymakers back away from free trade toward protectionism, prices will tend to rise. This will, at least in nominal terms, benefit labor but harm consumer interests. In a sense, it is trading weak labor markets for inflation. That is the “trade” we are monitoring.

Bill O’Grady

May 22, 2017

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

|

e

[1] Okun, A. (1972). Equality and Efficiency: The Big Tradeoff. Washington, D.C.: Brookings Institute.

[2] The breaks between equality and efficiency periods are our estimates, roughly aligned with presidents we believe signaled a change in policy emphasis.

[3] President Reagan’s “voluntary” import quotas on Japanese cars spurring Japanese automakers to source production in the U.S.

[4] A good article about this process is found at: https://www.nytimes.com/2017/05/02/magazine/is-china-the-worlds-new-colonial-power.html?emc=edit_tnt_20170504&nlid=5677267&tntemail0=y&_r=0.

[5] Interestingly enough, this is what happened in WWII. The government deficit soared as spending rose for the war effort. Household incomes rose too, but there was little to spend money on because of rationing. Household saving rose, not only funding the war effort but also paying back household debt.

[6] Usually, earnings rise in nominal terms and equities tend to outperform bonds in a rising inflation environment.

© Confluence Investment Management