This week, we continue our discussion on trade by examining the reserve currency issue.

What is the reserve currency?

When a country runs a trade surplus, it creates excess saving that must be either invested overseas or held as foreign reserves. If a gold standard is being used, the excess saving/foreign reserves can be held as gold (or other precious metals). In theory, reserve managers can hold just about any asset as foreign reserves. However, if the ultimate goal of generating saving is to build the productive capacity of the economy, then the best foreign reserve assets should be safe and easily convertible, with broad acceptability in markets.

Here is an example we often use to describe why the reserve currency is important. Imagine that a chocolatier in Paraguay wants to purchase a ton of cocoa beans. He calls a dealer in Côte d’Ivoire for a price; the seller offers $1,800 per ton. The buyer in Paraguay notes he does not have U.S. dollars but does have Paraguayan guaraní. The seller does not want the Paraguayan currency because it would limit his purchases to Paraguay because the guaraní isn’t widely accepted. The seller in Côte d’Ivoire would be able to buy a wider variety of goods (or have wider avenues for investment) from selling cocoa if he receives U.S. dollars instead.

So, how does the chocolatier in Paraguay get dollars? The most efficient way would be to export chocolate to a U.S. buyer, then use the dollars he receives to buy cocoa beans from Côte d’Ivoire. Because the reserve currency has widespread acceptance, non-reserve currency nations have an incentive to run trade surpluses with the reserve currency nation to accumulate the reserve currency, which allows them to pay for imports from around the world.

Is the reserve currency a global public good?

Economists define a public good as a product or service that must be provided by governments because the private market won’t provide the good, or will provide the good in less than optimal amounts. There are seven public goods a reserve currency nation should provide:

1. Act as a consumer (importer) of last resort;

2. Coordinate global macroeconomic policies;

3. Support a stable system of exchange rates;

4. Act as lender of last resort;

5. Provide counter-cyclical long-term lending;

6. Provide a truly riskless AAA asset for benchmarking purposes; and

7. Supply deep and predictable financial markets.

Charles Kindleberger, the famous economist who studied asset bubbles, identified the first five, and Mohamad El-Erian, the chief economic adviser at Allianz, added the last two.

The Bank for International Settlements (BIS) reports that more than 80% of trade-related letters of credit are denominated in U.S. dollars, significantly more than the second most used reserve currency, the euro, at 10%.1 That means most global trade is conducted in dollars between nations other than the U.S. Essentially, the reserve currency nation must run constant trade and current account deficits in order to provide liquidity for global trade. Thus, the U.S. doesn’t run trade deficits because we purposely “under-save” as noted earlier. Strictly speaking, as the saving identity shows, we do undersave but the reason for this activity is really the issue. It may be due to domestic policy but it can also be forced upon the U.S. by the actions of foreign trade policy.

Because of the reserve currency role, we believe the undersaving (in other words, the trade deficit) is mostly in response to foreign nations oversaving and moving that saving to the U.S. in the form of exports. If the U.S. were to run persistent trade surpluses, it would act as a form of global monetary tightening. In other words, by pulling dollars from world markets, the global trading system would face a contraction of available liquidity. If the reserve currency nation refuses to provide enough of its home currency to global markets, world trade is effectively reduced to barter, or counter-trade, meaning that nations can only engage in bilateral trade relations. Using the above example, the Paraguayan chocolatier can only acquire cocoa beans from Côte d’Ivoire if the seller there has something specific he would like to “swap” from Paraguay. Simply put, global trade would fall sharply if a reserve currency is unavailable.

How does the reserve currency factor into trade?

When a nation runs a trade surplus it accumulates foreign currency. In the era of the gold standard, the exporter could be paid in gold. As we noted in Part I, David Hume generally proved that accumulating gold eventually would lead to higher inflation and lead to a reversal in the trade imbalance.

A serious drawback with the gold standard was that the global money supply depended upon the mining industry. If the global aggregate supply curve expands due to industrialization but the gold supply remains fixed, deflation is unavoidable. At the same time, however, it also acted as an automatic stabilizer for foreign trade flows. In other words, gold generally prevented a nation from running persistent trade deficits or surpluses as shown by Hume.

Because the supply of gold is not backed by liabilities and thus does not generate interest, over time, the gold standard changed into a currency-gold standard. Nations would use either gold or the currency of the global hegemon for reserve purposes. Using currency allowed the reserve managers to earn interest. At the same time, a nation holding reserves understood that they could exchange the reserve currency for gold.

At Bretton Woods in 1944, the U.S. created a reserve system that replaced the British pound with the U.S. dollar for foreign reserves. The U.S. agreed to exchange dollars for gold at $35 per ounce. This system remained in place until 1971 when, under pressure from European nations draining American gold reserves, President Nixon suspended gold deliveries. The world thus shifted to a dollar-Treasury reserve standard.

This new standard broke the gold link; in theory, it meant the hegemon could expand the supply of the reserve currency without limit. Unlike the limits that were part of the gold standard, it was now possible for the U.S. to run large trade deficits that could be triggered by either fiscal spending or the lack of private or public saving relative to investment. After 1971, the limits to foreigners absorbing the hegemon’s spending were (a) foreigners deciding that they held too much of the reserve currency and opting for another currency, or (b) the hegemon deciding, likely for domestic employment reasons, that the trade deficit was too large.2

Because virtually all developed nations have used the Japan Model of development, none of them has an interest in becoming the reserve currency provider because it would require them to run trade deficits. In other words, it would require such a nation to reverse the policy of export and investment promotion to one of consumption and import promotion. Thus, there are really no obvious replacements to the U.S. dollar for reserves purposes, not because other currencies are not attractive but because these nations have no interest in jettisoning the Japan Model.

The U.S. management of the reserve currency was part of America’s Cold War strategy. The U.S. was open to trade and used trade relationships to build coalitions in the Free World. This is likely why the Japan Model became prevalent. The U.S. supported it by being the global importer of last resort. At the same time, there were both benefits and costs to the dollar-Treasury model of managing the reserve currency.

Let’s return to the saving identity to explore this issue.

(M - X) = (I - S) + (G - Tx)

Because the U.S. is willing to run persistent trade deficits, it can run fiscal deficits as well. Wars, large tax cuts, transfers and other fiscal spending can all be funded with foreign saving. At the same time, the need for private saving can be quashed by this same trade deficit.

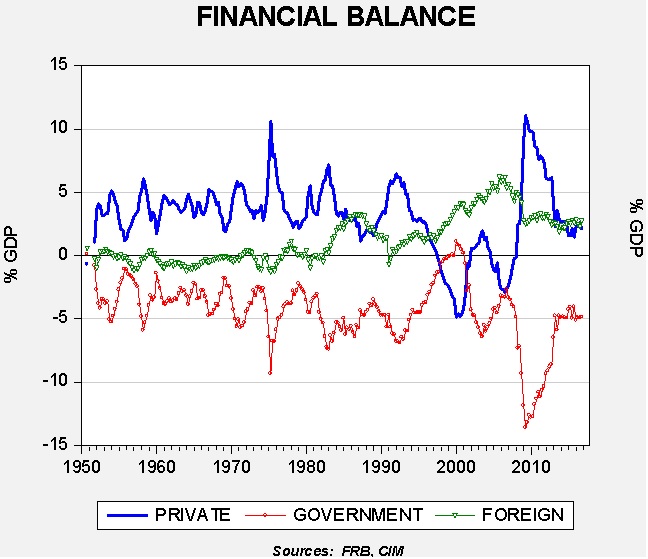

This chart, from the Fed’s Flow of Funds3 data, shows that the private sector has usually been a supplier of saving, meaning that the investment/saving balance was mostly positive. Until the 1980s, private saving funded both the fiscal deficit and mostly balanced trade, represented by foreign flows. When the foreign reading is positive, it means the U.S. is running a trade deficit.4 Note that the private saving balance became negative in the late 1990s. This occurred for two reasons. The Clinton administration ran a small fiscal surplus during this period and foreign saving flowed into the financial system via the trade deficit.

The continued high flows from overseas into the U.S. financial system continued in the last decade. Federal Reserve Chairman Bernanke referred to this as a “savings glut,”5 where emerging economies were building their foreign reserves after the Asian Financial Crisis in the late 1990s. For the most part, this influx kept rates low and encouraged borrowing in the U.S. This likely contributed to the real estate bubble.

For most of the postwar period, but especially since the 1980s, the U.S. has been open to trade which boosted foreign flows into the U.S. These flows have entered the U.S. for a number of reasons. Some of this lending was designed to support the Japan Model which was being deployed by China to build its productive capacity. China would send us goods; we would send them back Treasuries.

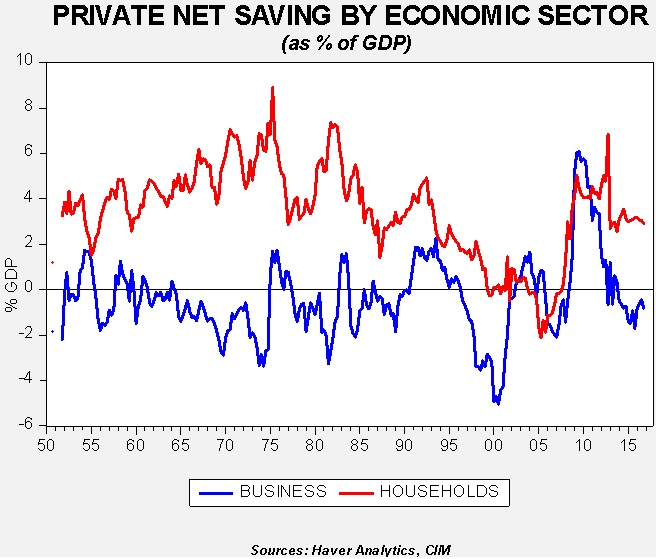

This chart shows U.S. private saving (as a percentage of GDP). Household saving rose steadily from the 1950s into the mid-1970s. For most of the period, businesses were net dissavers, which isn’t necessarily a bad outcome because this forced firms into the capital markets to raise funds for investment. As inequality rose, saving steadily declined and was mostly replaced by foreign saving.

When a nation provides the reserve currency, every nation in the world has an incentive to run a trade surplus with the hegemon. The reserve currency is generally accepted across the world and can be used to buy just about anything. And, in the case of the U.S., financial markets are deep and a plethora of “risk free” fixed income instruments are available to use as saving vehicles. For much of the postwar period, the U.S. economy has been large and able to absorb imports; these imports tend to keep inflation low as the aggregate supply curve is really the world’s supply curve.

Being the reserve currency is a mixed blessing. Foreign financial flows can distort financial markets. It can encourage excessive borrowing and keep interest rates lower than they otherwise would be. Foreign competition puts U.S. workers under constant pressure. For those who can successfully compete with foreign goods and services or are insulated from trade, rewards can be substantial, but many workers are unable to keep their jobs in the face of imports. The combination of ample financial flows and low inflation can encourage investors to take excessive risks. Like most things in life, where one stands on a position can be determined by where one sits, but the recent political tensions and the rise of populism are, in large measure, due to the reserve currency issue.

Next week, we will conclude our reflections on trade.

Bill O’Grady

May 15, 2017

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

2 For a detailed study of Nixon’s policy decision with regard to the gold standard, see: Hudson, M. (1972). Superimperialism. New York, NY: Holt, Rinehart and Winston. (Chapters 12, 13).

3 The official name is the Financial Accounts of the United States.

4 Strictly speaking, it’s a current account deficit but trade deficit works for explanation purposes and, in any case, it’s the largest component of the current account.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management