Reflections on Trade: Part II

In this multi-part report, we offer several reflections on trade that we hope can provide some insight into how to use macroeconomics to judge the veracity of certain claims. In Part I, we laid out the basic macroeconomics of trade. This week, in Part II, we will discuss the impact of exchange rates and examine the two models of economic development, the “Japan Model”1 and the “American Model.”2

The Japan Model of development calls for policies that drive up household saving. This is usually done through financial repression and wage suppression. This model is designed to provide cheap investment funds to build up the productive capacity of the country.

In contrast, the American Model of development relies on foreign investment. In this arrangement, the trade deficit is an import of foreign saving for investment.

As a review from Part I of our report, the following saving identity means that the private investment/savings balance (I-S) plus the public spending balance (Govt-Taxes) is equal to the trade account, M-X (Imports less Exports).

(M - X) = (I - S) + (G - Tx)

If a nation’s saving equals its investment and it runs a balanced fiscal budget, then it will run a balanced trade account. It doesn’t matter what the exchange rate is or what trade policy is in place; if the private and public sector balances, there will also be balanced trade.

Can a nation prevent a trade deficit through protectionism?

Yes, but the same identity described above is still in place. It is often believed that trade restrictions affect only the foreign saving part of the saving identity. However, because the identity is like a balance sheet, it actually must balance the other parts of the identity as well. Let’s assume a nation runs the Japan Model but the rest of the world won’t accept the exports. Investment, in the form of unwanted inventory, will rise, absorbing the excess saving. The unwanted inventory will have a negative impact on the economy using the Japan Model. This could include deflation as the excess inventory lowers prices, unemployment which reduces consumption and saving or rising fiscal deficits as the imbalanced nation tries to maintain the level of GDP.

Is there a cost to the nation deploying trade protection? Although nothing in that nation becomes unbalanced, there is the opportunity cost of not having cheaper imports available. Thus, it would likely lead to higher price levels that would not otherwise occur and lower prices in the nation using the Japan Model.

How do exchange rates affect the identity?

The most common way to explain how exchange rates affect trade is through microeconomics. It is assumed that relative price differences change the demand for imports and exports, thus changing the trade balance. However, as we have seen, the relative price effect has to translate into the saving identity. Nations using the Japan Model for development usually deploy an undervalued exchange rate. By keeping the exchange rate undervalued, it lowers relative costs to the rest of the world, which raises consumption, depresses saving and, assuming stable investment, will create an imbalance in this relationship.

(M - X) = (I - S) + (G - Tx)

In other words, using the saving identity, S falls, creating a private sector saving imbalance. Assuming no change in the fiscal situation, M must rise relative to X in the rest of the world to balance the equation.

In the nation using the Japan Model, an undervalued exchange rate reduces real wages, depressing consumption © and boosting saving (S). As S>I, assuming no change in public saving, exports (X) must rise relative to imports (M).

When the rest of the world refuses to accept the undervaluation of the exchange rate, the rest of the world sees a reversal from the previous condition. Prices will tend to rise on imports which will depress consumption and likely lead to rising saving. That will narrow the private investment/saving balance and reduce M relative to X, again assuming no change in fiscal policy.

What happens in the country using the Japan Model when the exchange rate is forced higher? A rising exchange rate lowers the cost of imports to that nation, reducing overall costs and lifting consumption. This should reduce saving, narrowing the private investment/saving balance and, once again assuming no change in fiscal policy, reduce X relative to M, leading to a smaller trade surplus.

How does foreign investment fit the saving identity?

Nations achieve developed nation status by building productive capacity. This requires saving to fund investment. The Japan Model generates this saving internally; the American Model acquires the saving from abroad.

(M - X) = (I - S) + (G - Tx)

So, using this identity, a nation in development needs to raise investment (I). If it does not have enough saving (S) to meet the demand for I, assuming no change in fiscal policy, M must rise relative to X. A nation running a trade deficit is, in effect, importing foreign saving. That is the essence of the American Model. We note that the Japan Model differs from the American Model by generating saving internally.

Doesn’t this make the Japan Model counterintuitive?

In some respects, yes. It would seem more logical that a nation building its economy would import saving from abroad. Not only would the investment probably offer a higher rate of return to foreign savers who are making the foreign investment, but it would allow the developing nation to build its productive base without suppressing consumption and financial repression.

The Japan Model does appear more self-reliant. Instead of being dependent on foreign investors, who have been known to withdraw investment on a whim, the Japan Model nation is using domestic saving. However, it is really an exchange of risks. Instead of accepting the risk that foreign investment may be reduced or flee, the Japan Model accepts the risk that foreign markets won’t be closed off to exports. As we will discuss later, the Japan Model has worked since WWII because the U.S., as global hegemon, is essentially the global importer of last resort.

Are there other issues that emerge from the Japan Model?

There is an interesting issue that occurs with development using any model where consumption is suppressed. As noted earlier, suppressing consumption is designed to create saving which is used to fund investment. Because saving is forced, it is likely that interest rates will also be kept lower than what a free market may generate. This condition could lead to malinvestment or overinvestment.

Investment is one of the most difficult activities for any nation. That’s because it requires some element of forecasting the future. In the early stages of development, almost any investment will generate a positive return. However, as development progresses, the need to allocate investment efficiently rises. The abundance of saving increases the likelihood of excessive investment, which can cause productive capacity to exceed consumption. If this excess capacity remains in place, it will eventually reduce the return on capital and stagnation will develop.3

It should also be noted that funding investment is generated by the financial system. Investing firms either borrow or issue equity to fund investment. In most developing economies, the financial system tends to be immature and most of the funding comes through the banking system in the form of debt. Although both forms of financing have their own risks, in general, debt carries macroeconomic risks as excessive debt can lead to financial crises.

European powers faced an overinvestment problem before WWI. As they raced to develop their economies they found themselves with excess productive capacity. To maintain saving in excess of investment they needed to export their surplus saving (or, to put it another way, their excess productive capacity). This was achieved through colonization. Colonies were forced to overconsume and undersave, leading the colonies’ investments to exceed domestic saving. This condition was resolved by running a trade deficit; these imports were provided by the colonial power. Essentially, colonies allowed the development model of oversaving to be maintained.4 The colonies became unnecessary after WWII because the productive capacity of most colonial powers was destroyed during the war.

The U.S. did not follow this model of development. In part, the U.S., due to its large domestic market, was able to avoid the excess productive problem for nearly five decades. From 1870 until WWI, the U.S. was generally able to prevent overcapacity.5 Still, the large domestic market didn’t prevent the eventual creation of excessive productive capacity. The Great Depression showed that the U.S. was plagued with overcapacity once exports fell (in part due to retaliation from the Smoot-Hawley Tariff).

However, this problem did take a while to develop and the devastation caused by WWI, which boosted demand for U.S. exports, likely played a role in creating the excess capacity. During development, the U.S. industrial revolution was mostly funded by British investors (and the U.S. ran a trade deficit during this period). Interestingly enough, there were investment booms and busts that occurred despite the fact that a domestic saving model wasn’t adopted. Significant losses were suffered by overseas investors. In the Japan Model, these losses are borne by domestic investors and often these losses are non-performing loans, which require a politically painful workout period.

How do these two development models manage the transition from developing nation to developed nation status?

History suggests that no nation achieves developed nation status without stress. The history of economic development suggests that the world has a “parade” of high growth/low cost producers which reflect the spread of industrialization. These nations, due to their high growth, are often considered economic “miracles.” The Soviets, who experienced high growth during the 1950s and 1960s, were projected to “bury” the U.S.6 Those concerns evaporated by the 1970s. Japan was thought to have created a new form of capitalism during its growth phase; no one believes that anymore. China has been lauded in a similar fashion, although we believe that China’s turn as the high growth/low cost producer is rapidly coming to a close.

We think the case can be made that generating saving internally creates the most problems. The Japan Model, as noted, funds investment mostly through domestic saving. Consumption is usually constrained by having a weak currency, which keeps prices high, along with tariffs and other trade barriers which have the same effect as a weak currency. Another feature of the model is low deposit rates, a form of financial repression. Low deposit rates usually encourage higher saving rates to achieve saving goals and lower borrowing costs to borrowers (investors). In addition, even lax environmental rules, which make it easier to build plant and equipment, bring pollution, which raises health care costs to households. If the social safety net is weak, even more saving is generated to pay for future health care costs.

It should be recognized that the process of development is difficult in both capitalist and communist economic systems. The problems in capitalist democracies are well documented. However, communist regimes faced similar problems. Because both the U.S.S.R. and China relied on domestic saving, both squeezed households to create a source of funds. In the U.S.S.R., the industrialization under Stalin led to millions of deaths (although, to be fair, many of those executed were perceived political threats). China’s development has clearly been on the back of constrained household spending.7

What tends to occur over time in the process of development is that productive capacity becomes excessive. In other words, overinvestment occurs. Although this problem tends to happen regardless of whether a nation generated saving internally or acquired it from abroad, the Japan Model has been dominant in the postwar era and so the most recent examples of the issues tied to development are linked to that model. In addition, because the Japan Model specifically keeps interest rates low, the potential for malinvestment is probably higher than in a nation using the American Model, which uses prevailing interest rates to discount investment.

History does show that the policies designed to generate investment develop a political constituency. In other words, the group in society that has benefited from policies that constrain consumption and boost saving wants them maintained even after development has been achieved. These policies take on the role of “self-evident truths.”8 Because those who have benefited from the development model have become wealthy, they usually become politically powerful as well. As a result, these policies remain in place past their period of optimal usefulness.

The adjustment to more consumption and less investment is difficult for any country. It usually takes something drastic, such as war or depression, to force change. As noted above, when European nations reached this point, they turned to imperialism to absorb their productive excess. The U.S. arguably needed the Great Depression to make this adjustment, even with using foreign saving, which should, in theory, be better than internally generated saving because foreign investors are using market discount rates to make investment decisions.

A case can be made that Japan has never managed to make the transition.

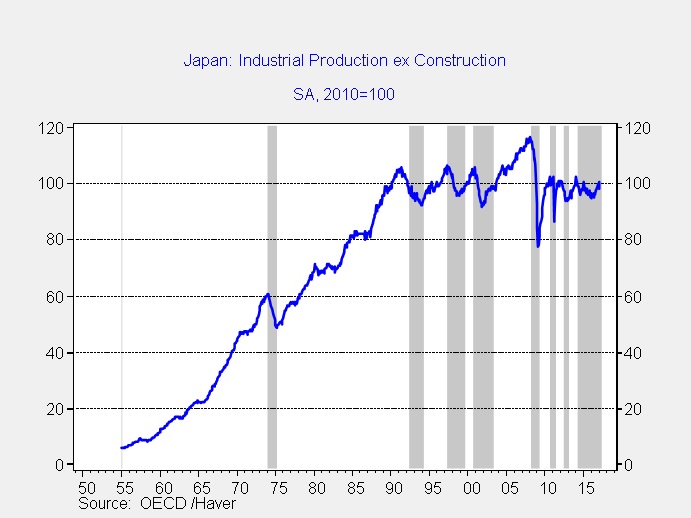

This chart shows Japan’s industrial production. Although we did finally see a new peak in early 2008, the uptrend from 1955 to 1990 was clearly broken. We have put Japan’s recession bars on the chart; since 1990, Japan has suffered through seven recessions, three of which exceeded two years.

Germany, who also continues to use export promotion and has high levels of domestic saving, has effectively used the Eurozone as a colony. Because nations within the Eurozone cannot use currency depreciation or trade protection, the other nations within the currency bloc are forced to absorb Germany’s excess saving by running trade deficits. This is the root of the problem in southern Europe.9

China has enjoyed a remarkable period of growth but is showing similar strains as those seen in Japan in the late 1980s. Debt levels are high, foreign nations are balking at Chinese exports and the need to transition to higher consumption and less investment has been slow due to, we believe, a strong constituency within the Chinese Communist Party opposed to changing the current model because many high-ranking members of the party have greatly benefited from that model. To be fair, all nations that strive for developed status struggle to make the transition from high investment to high consumption. China’s transition issues are not unique in that regard.

Next week, we will discuss the role of the reserve currency.

Bill O’Grady

May 8, 2017

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 We call this the Japan Model because it has been adopted by Asian nations for development.

2 We call this the American Model because it is how the U.S. acquired saving during its industrial revolution, which began in earnest in 1870.

3 The theory of underconsumption and excess production was developed by a number of radical economists. Although Marx only alluded to this issue, Engels developed this concept further. See: Engels, F. (1947). Anti-Duhring. Progress Publishers. Originally published Leipzig 1878.

4 See: Hobson, J.A. (1902). Imperialism: A Study. New York, NY: James Pott & Company.

Lenin, V. (1999). Imperialism, The Highest Stage of Capitalism. Chippendale, NSW, Australia: Resistance Books. Originally published 1917.

5 We do acknowledge that this wasn’t true in all industries. Excess capacity likely occurred in railroads.

6 This is a quote from Nikita Khrushchev in the mid-1950s; although often attributed to nuclear conflict, it appears he was referring to the superiority of communism as an economic system.

9 Pettis, op cit, Chapter 6.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management