Last week, we began our retrospective on the EU. This week we will examine the post-Cold War expansion of the EU, including a discussion of the creation of the euro and the Eurozone. With this background, we will analyze the difficulties the EU has faced in dealing with the problems caused by the 2008 Financial Crisis. We will look at several proposals being floated in the wake of Brexit about reforming the EU and, as always, conclude with potential market effects.

The End of the Cold War and German Unification

The fall of the Berlin Wall and the collapse of the Soviet Union led to dizzying changes across Europe. Nations that existed behind Churchill’s Iron Curtain suddenly found themselves free of Soviet domination. West Germany found itself on the cusp of unification with East Germany.

The prospect of a unified Germany removed one of the features that had historically led to peace in Europe. This worried the rest of Europe; in response, the French made it clear they would oppose unification unless the newly unified Germany could be bound closer to Europe. The answer to this issue was the Maastricht Treaty, which created the European Monetary Union (EMU), or the Eurozone. France wanted Germany to forsake its symbol of national pride, the D-mark, and replace it with a European currency. Given that a nation’s currency is one of the most visible signs of sovereignty, the French believed that relinquishing the currency would bind Germany closer to Europe.

Although Germany was reluctant to give up the D-mark, it did want to unify with its eastern compatriots. Therefore, Chancellor Kohl agreed to the EMU. However, Germany was able to negotiate some of its goals as well. First, the new central bank, the European Central Bank (ECB), would have policy aims similar to the Bundesbank, the German central bank. Its policy goals would be currency stability and inflation control. The ECB had an inflation target of 2%. Unlike the Federal Reserve or the Bank of Japan, it would not have a full employment or economic growth mandate.

Second, Germany was able to create fiscal rules for the Eurozone. The German government was worried about fiscal profligacy; there was a concern that the southern European states would run large fiscal deficits and this would force German taxpayers to bail out these nations. Thus, Germany insisted that there would be no bailouts. The Eurozone nations also agreed to fiscal deficit and debt targets and were required to have low inflation to enter the Eurozone. Although there were calls for a unified fiscal budget and a Eurobond backed by the full faith and credit of the Eurozone, Germany rejected such measures, fearing it would see its saving absorbed by free-spenders in the single currency bloc.

The EMU was set in motion on July 1, 1990, when capital controls were abolished and the principles of the Maastricht Treaty were accepted. By May 1998, 11 nations had agreed to adopt the single currency on January 1, 1999. Two years later, euro notes and coins were introduced. Greece joined the single currency in January 2001 and, by 2015, 19 nations were in the Eurozone.

It should be noted that there is no exit mechanism from the Eurozone. The creators could not conceive of any nation wanting to leave. First, the Eurozone was considered an improvement for nearly all the nations in the group, and second, the EMU was further progress toward European unity. The idea that this progress would reverse was simply not considered. The Eurozone has been characterized as a prison similar to Alcatraz. Because there is no safe escape, no one would ever leave.

Until the 2008 Financial Crisis, the single currency worked rather well. Inflation and interest rates converged among the members. Countries on the southern tier who had suffered through high inflation and interest rates for years found themselves able to borrow at historically low rates.

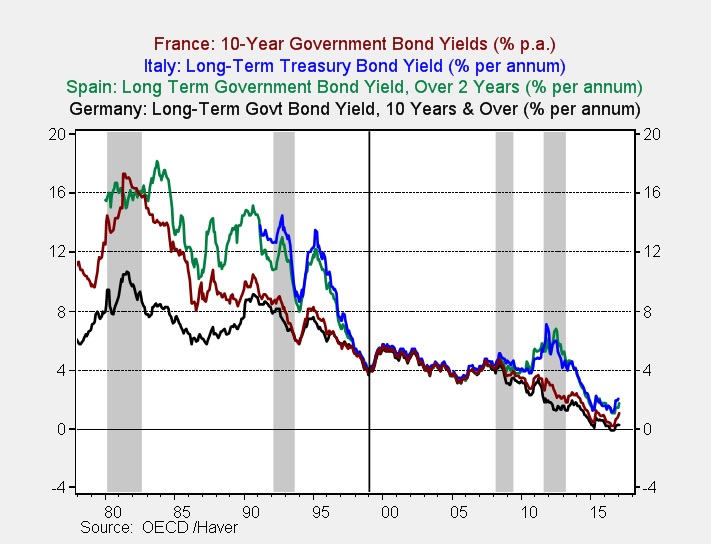

This chart of bond yields shows the impact of the EMU.

Representative long-term interest rates on government bonds for France, Spain, Italy and Germany are shown on this chart. Note how rates converged at the beginning of the euro in 1999 and remained close until the Financial Crisis. The financial markets believed that there was no appreciable difference in credit risk among nations in the Eurozone. The crisis ended that notion.

The Financial Crisis created conditions that led to the European Debt Crisis of 2010-11.1 This event revealed two difficult issues for the EU. First, banks live in Europe but die in their country of origin. In other words, there was no mechanism in the EMU to deal with widespread bank failures. Banks in Europe regularly lent money across borders but the national government was responsible for the liquidation if they failed. Although the national central banks continued to exist, within the Eurozone they could not act as lender of last resort because they did not have the ability to expand the money supply. That mandate rested with the ECB. Thus, bank failures could easily turn into bank runs.

Second, there was no agreement on what caused the European Debt Crisis. The Germans believed that the crisis was due to excessive borrowing, either from the public or private sectors. This position is shared by most northern European members of the Eurozone. If this is the problem, austerity is the best response. Although the creditor nations within the Eurozone would be willing to assist those in trouble, bailouts were, by law, illegal.

On the other hand, the debtor nations believed that the debt crisis occurred because of the structure of the Eurozone. Because the Eurozone was part of a free trade bloc, there was no way for a nation to deal with a balance of payments problem by trade barriers. And, within the Eurozone there was no way to depreciate one’s currency to deal with a balance of payments problem. If a nation, say, Germany, engaged in policies designed to boost saving, excess production would be thrust upon the rest of the Eurozone. The only way for these debtor nations to act against Germany would be to save more than Germany did…which would lead to excess saving and slower growth. If this was the cause, the best response would be debt relief and stronger spending in the creditor nations.

The second difficult issue revealed where the real power in Europe rested. Although Brussels was often the target of derision for its bureaucratic control, in reality, Europe is being dominated by Berlin. While there is a strong case to be made that the debtor nations ran into trouble due to structural issues, the policy response has favored the creditor nations. It is worth remembering that the major goal of creating the EU was to harness the benefits of the German economy and avoid German dominance. That attempt appears to have failed.

Immigration

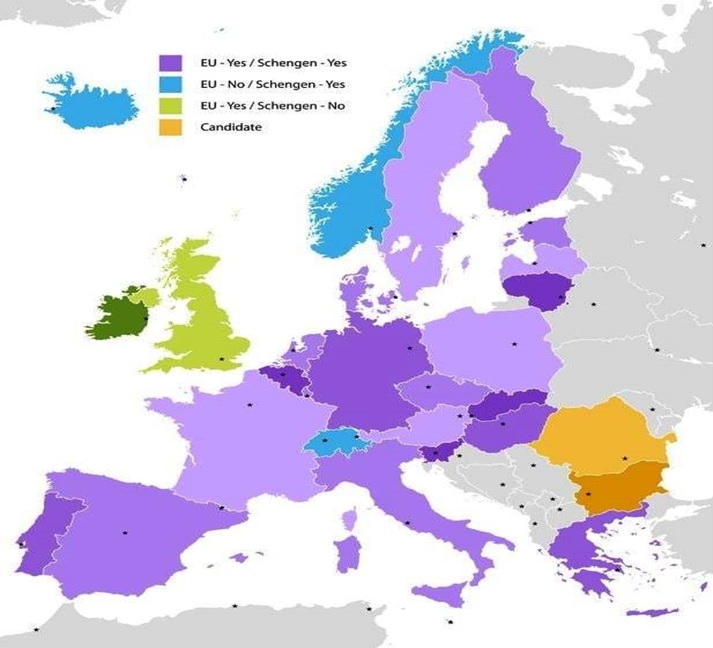

The pictures of refugees clinging to unseaworthy vessels, risking everything to travel across the Mediterranean as they flee North Africa and the Middle East, are a common feature in the media. European refugee policy is straightforward; they should be accepted in the nation they first enter and are processed, which puts a great burden on the southern European nations who lack the resources to handle the high numbers of refugees. Later, the EU can decide if the refugees can gain asylum. This system was never designed for the masses that have poured into Europe. One of the elements of sovereignty is enforcing a border. However, within the EU “Schengen zone,” there is free movement of peoples. Thus, once inside the zone, these refugees can move anywhere. This map shows the members of the Schengen zone in purple.

(Source: EU)

In practice, some nations, notably Hungary, have blocked their borders, while others have refused to accept more than a mere token number of refugees.

Recent terrorist threats have also raised concerns. The Islamic terrorists that attacked in France lived in Belgium, and there were no border checkpoints to prevent their entry. The free movement of people is at risk due to the refugee crisis.

European Security

It is obvious that a third world war hasn’t happened in Europe, a testament to the success of the EU and NATO to contain nationalism and protect Europe from Soviet expansionism. However, it is arguable that the reason for European peace has a problem of multicollinearity. We don’t know for sure if either or both were the key reason for European security. My opinion is that NATO was probably more important and this treaty only worked because the U.S. was willing to shoulder almost all the burden of Europe’s defense. Containing nationalism is not unimportant but the recent performance of European militaries2 suggests that they are not a serious threat to themselves.

President Trump has suggested that U.S. support of NATO may become conditional on higher defense spending from European members of the treaty group. What the new president doesn’t fully grasp is that the U.S. has been able to dictate security policy in Europe because it supplies it; once European nations pay more for their own defense, they may be inclined to prefer their own security policies as well. This change, coupled with nationalism, could return Europe to conditions that fostered broader wars in the first half of the 20th century.

The Response

Since the creation of the EU, there have generally been two responses to problems in Europe. One response has been “more Europe,” meaning more functionalism where Brussels takes greater control, or an expansion of Europe as seen in response to German unification. The other strategy is that the EU tends to “muddle through,” meaning problems get pushed into the future for eventual resolution.

The problems facing the EU now may not be resolved by either tactic. “More Europe” would likely call for a full faith and credit Eurobond and the ECB taking power over national banking systems. These changes are probably not going to occur. Muddling through is simply leading to rising populism as Europeans want some sort of resolution.

There is a growing chorus calling for a restructuring of the EU.3 In this view, there would be four tiers of membership. The widest would be a periphery membership for those who only want free trade. They would not use the single currency allow the free movement of people nor follow the bureaucrats in Brussels on rules except for those that affect trade. A second tier would be part of the free trade group, pay into the EU budget and accept most of the rules of Brussels. A third tier would accept full membership in the EU but not join the single currency. Finally, the core would be members of the EU and the Eurozone.

Up until now, the EU has been reluctant to move in this direction for fear that it would be a retreat from a more unified Europe. If peace in Europe is due to the steady progression of unity, this fear is well founded. On the other hand, if peace is mostly due to U.S. power, then this structure would make much more sense. Southern Europe probably shouldn’t be in the Eurozone. Nations losing the ability to depreciate their currencies to maintain competitiveness has led to nearly a decade of stagnant growth.

Such a structure would need to be bi-directional; in other words, nations could move within the Eurozone to the second, third or fourth tier, or opt for “more Europe” policies by moving from the outer to the inner tiers. Essentially, being in the core means a nation is comfortable being dominated by Germany. In the long run, a dominant power in Europe is probably necessary to maintain peace; if the U.S. is no longer willing to provide this role, Germany is the most likely candidate to take America’s place.

Ramifications

If the structure of Europe is going to change and nations within the Eurozone become more fluid, the behavior of the euro’s exchange rate could become quite volatile. For example, if Italy, Spain or Greece leave the Eurozone, the single currency might rally because the remaining members would be seen as stronger and more stable economies. On the other hand, the financial market turmoil that might ensue from a nation leaving the Eurozone could be unsettling and cause currency depreciation. Still, in the long run, the case for a more flexible EU is strengthening. The fact that Britain would consider leaving opens the door to others. Think of it this way…the initial group consisted of six nations, and now there are 28 EU members out of the 40 nations within Europe.4 A “one size fits all” solution probably doesn’t make much sense.

It appears to us that the current structure is probably not sustainable and a new, looser configuration makes more sense. It will be difficult for elites in Europe to give up their hopes for a unified Europe. However, Brexit, the threat of populism, the persistence of weak economic growth, periodic debt crises and immigration worries suggest that what has worked before isn’t working anymore.

Although shifting to a less restrictive structure would probably lead to a more stable Europe over time, getting there could lead to higher instability. Thus, investors should treat European assets cautiously.

Bill O’Grady

April 10, 2017

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

2 Libya is a good example.

4 We count 40 European countries according to some sources; there is some dispute over the continent classification of certain Middle Eastern countries.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management