Uncertainties surrounding China’s currency and broader economic transition continue to cloud the global economic outlook. In 2017, the feedback loop between rising U.S. interest rates and pressure on China’s exchange rate mechanism may well be a key determinant of returns across asset classes. The greatest risk in 2017 is that China is forced to choose in favour of financial system stability at the expense of exchange rate stability. If the Chinese yuan’s quasi-peg ends, we could expect a massive volatility spike in financial markets worldwide.

China’s sheer size means that a large yuan depreciation, a sharp slowdown in growth or some combination thereof would be highly disinflationary to the rest of the world. In this scenario, China’s current account surplus would again inflate as domestic demand slumps. Such a growth shock would be supportive of duration (interest rate risk) in sovereign bonds issued by the U.S., Europe and Japan.

Following a research visit to China last month, we came away confident that economic data should continue to look reasonably robust through the first quarter. This reflects the lag effect of past strength in real estate sales and belated infrastructure spending coming online. Recall that it was a combination of the botched yuan depreciation in August 2015 and hard landing fears that triggered the fallout in global markets. The unexpected strength of the property market in 2016 should also support industrial metals prices early in 2017; property sales volume generally leads China-related commodity prices (coal, copper, iron ore and steel) by nine months.

Into the second quarter, however, a slowdown in growth already looks baked into the cake. The extreme degree of fiscal stimulus and credit growth, along with tax incentives that brought forward demand for new cars in the second half of 2016, will fade.

Add to this the lagged effect of the recent property clampdown in many major cities, and we may see growth hindered.

Tighter capital controls have been insufficient to stop capital outflows and the associated bleed in foreign exchange (FX) reserves. Monetary policy is thus potentially constrained from reacting to weaker growth without exacerbating the capital outflow problem.

Key Uncertainties in China’s Outlook

Policymakers don’t appear hesitant to disrupt the financial status quo. Upending the consensus view that the leadership will be highly risk-averse ahead of the autumn 2017 National Party Congress, President Xi Jinping and the government have sanctioned moves to address key sources of financial stability risk earlier than expected. Access to mortgage and developer financing has been tightened, while the People’s Bank of China (or PBOC, the central bank) and the regulatory commission have cracked down on various forms of shadow bank leverage. The primacy of Xi as core leader is associated with primacy of the state in the economy. This domestic source of uncertainty tends to increase private sector demand for U.S. dollars.

A trio of external uncertainties – interest rates, trade and security policy – also increases demand for dollars. Just as exchange rate stability over the past 20 years has been used as a Chinese political tool to gain soft power, it could become a political weapon in reaction to potential aggression from the Trump administration.

Finally, we believe the quality of policy advice to the Chinese leadership has likely deteriorated. The Central Leading Group for Financial and Economic Affairs has replaced the much larger State Council as the primary body for economic policymaking. It mostly comprises bureaucrats with little market experience. Scope for policy mistakes in reaction to events has never been higher.

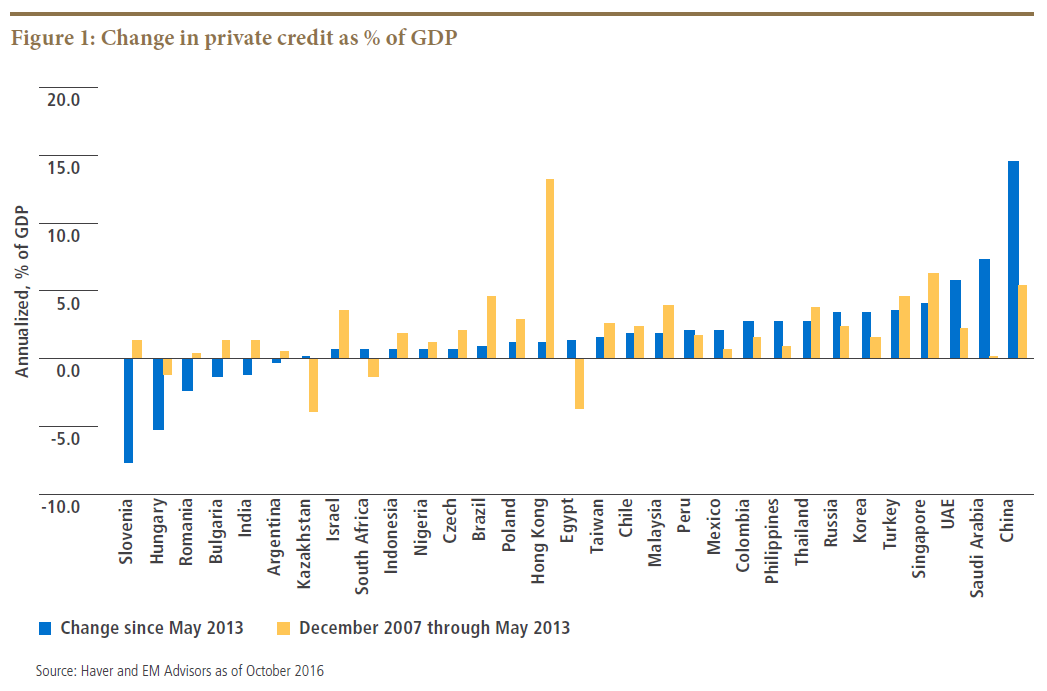

The conclusion is that while Chinese growth looks stable into early 2017, a more marked slowdown by the second quarter appears inevitable. Growth has been stabilized only after massive fiscal and credit stimulus. China’s total government and private sector debt will likely surpass 285% of GDP this year, a 90% increase since 2008.

Moreover, persistent balance-of-payment deficits and the continuation of strong credit growth have led to a structural rise in dependence on wholesale funding for broad credit growth. Abundant liquidity is increasingly an illusion in China: The effective private loan/deposit ratio is approaching 100%, while total augmented claims are 123% of system deposits as of November 2016, based on our calculations. The wholesale market has become a large and crucial source of credit funding.

The paradox of Chinese drift is that its success in maintaining the juggling act between multiple internal and external objectives only adds to the risk of a hard landing and greater global fallout in the future. This paradox stems from the fact that the balancing variable is ever-increasing debt.

Interest Rates, Flows and Trade: No Silver Lining?

The silver lining around rising U.S. interest rates is that they tend to be allied to cyclical upswings. Thus, there is typically a positive demand offset to an otherwise negative-for-EM rise in external borrowing costs and a reversal in portfolio flows. Unfortunately, history has repeatedly shown that capital flow movements stemming from changes in U.S. interest rates tend to dominate any positive trade-related effects from stronger U.S. demand. The current cycle looks more consistent with the 1990s than the mid-2000s, when the emergence of the Asian savings glut led to persistent FX reserve increases and recycling back into Treasuries. Thus, long-term U.S. yields were stable through most of the Fed tightening cycle.