As is our custom, we close out the current year with our outlook for the next one. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape in the upcoming year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

Issue #1: The Trump Doctrine

The election of Donald Trump was the second major shock to the Western political establishment in 2016, the first being the Brexit vote. At this point, there is clearly a growing rejection of the policy consensus that has been in place since at least 1990, with the fall of communism, and perhaps even 1944, with the Bretton Woods agreement.

Although Trump’s foreign policy is still evolving, there are two key emerging themes:

There is lots of “brass” in the administration. Trump is putting a number of former generals in positions of power. Although this has raised concerns among some commentators about the loss of civilian oversight, we suspect it will make the new administration more cautious about deploying military force. We view Trump as a Jacksonian.1 This particular archetype of foreign policy figure tends to intervene abroad less than Wilsonians or Hamiltonians. The military men in the government will likely be reluctant to deploy troops and, if they do, they will likely insist on following the Powell Doctrine which places hurdles before deploying troops. Specifically:

1. Is there a vital national security interest being threatened?

2. Do we have a clear and attainable objective?

3. Have all the risks and costs been fully and frankly analyzed?

4. Have all non-violent policy tools been fully exhausted?

5. Is there a plausible exit strategy?

6. Have the consequences of our action been fully considered?

7. Is the action supported by the American people?

8. Do we have broad international support?

It is worth noting that the Iraq War, the Afghanistan War and the intervention in the Balkans would not have passed these conditions.

Jacksonians deplore limited war that ends without a clear victory. They do not brook anything but unconditional surrender. Those objectives mean that war is only undertaken if necessary. And, having former military figures in these roles means that these people have personal experience with the costs of war and will probably use it sparingly. Thus, we would expect less military activity, but if intervention is required then it would be reasonable to expect targeted operations with overwhelming force.

In contrast, Hamiltonians tend to use foreign policy to support American firms and Wilsonians deploy troops for moral causes. We would expect neither to occur under Trump which means that other nations may not be able to rely on American support without a direct U.S. interest.

The U.S. may become a malevolent hegemon. Broadly speaking, the global superpower has two roles. The first is financial—it provides the reserve currency which means it absorbs enough imports to provide enough of its currency for global trade. This also means it must have a deep financial system to provide investable vehicles that foreigners can use to hold reserves. The second role is to provide global security.

Although no hegemon is perfectly benevolent, the U.S. has been relatively benign compared to others. The last two, the British and the Dutch, had colonies, for example. They forced the colonies to provide commodities and made them accept finished goods. Instead, the U.S. has used its large relative size to absorb the world’s imports and provide dollars for reserve and trade purposes.

Militarily, the U.S. contained the Soviet Union and froze conflicts in Europe, the Middle East and the Far East. In Europe, through NATO, the U.S. essentially demilitarized the continent by providing its security. The same was accomplished in the Far East by demilitarizing Japan. These actions prevented another European war and a rekindling of Sino-Japanese tensions. In the Middle East, the U.S. honored the colonial borders which maintained hostile stability. The colonial European powers had created colonies that were designed for outside control. In most cases, tribal, ethnic and religious groups were either separated or combined in ways that were not conducive to independence. In addition, minority groups were put in power so they would be dependent on the European colonialists in order to remain in power. Although these nations were destined to be unstable without authoritarian governments, the U.S. honored these borders to maintain stability. Finally, the U.S. Navy also protected the sea lanes to foster trade.

American political leaders have always had to balance the superpower requirements with domestic needs. From 1945 to 1978, the U.S. did this by fostering the creation of high-paying, low-skilled jobs. This was done through high marginal tax rates and industry concentration which stifled the introduction of new technology and entrepreneurship. Unfortunately, by the 1970s, this economic structure was unable to contain inflation, so policymakers adjusted the model by supporting globalization and deregulation. This led to falling inflation at the cost of rising income inequality. Many households increased their borrowing in the face of falling incomes. The failure of this policy became evident with the 2008 Financial Crisis.

Since the crisis, policymakers have struggled to find a proper response. Are deregulation and globalization “self-evident truths”2 that should always be protected and supported? If so, is it possible to reduce income inequality? Can the U.S. continue to provide the global public goods that its superpower role requires?

Although it is early, there is growing evidence to suggest that Trump may rewrite America’s superpower role with the goal of improving the lot of the bottom 80% of the income distribution. It remains to be seen what form this may take. However, it appears Trump may require foreign nations that want access to the dollar to pay more for that privilege. This may mean that if a nation wants to sell its products in the U.S., it will be required to build production facilities here. If it refuses, it may find itself facing barriers to trade. The Trump administration may also penalize domestic firms that offshore production through tariffs. Nations under America’s security umbrella may be forced to pay for those services, which could be in the form of minimum purchases of arms from American firms.

Most hegemons extracted some sort of tribute from the world for the global public goods they provided. The U.S. has been relatively munificent compared to other superpowers, and it would be politically popular to create conditions that support Americans by shifting some of the costs of hegemony to the rest of the world.

However, it should be noted that such a shift carries risks. The U.S. managed to prevent WWIII through its policies. Allowing Japan and Europe to rearm might also lead them to become more aggressive and independent in foreign policy. It should be noted that the last two world wars sprang from Europe; a remilitarized continent with an independent foreign policy increases the potential for regional conflict. Raising barriers to trade may simply lead to global mercantilism and weaker global growth. The combination of falling economic growth, reduced trade and “thawing” conflict zones is a recipe for conflict.

Again, it’s early in the process but one of Trump’s campaign slogans was “America First.” That doesn’t necessarily mean isolationism, but it does suggest the U.S. won’t be the generous hegemon of the past.

Issue #2: European Elections

The past year delivered two electoral jolts from Europe, Brexit and the Italian referendum. The coming year promises similar uncertainty. There are three potentially important national elections in 2017.

Netherlands: The first election occurs in the Netherlands in March. Current polls put the Party for Freedom in the lead with a projected 34 seats out of 150. This is a right-wing populist, Euroskeptic, anti-immigrant party led by Geert Wilders. It isn’t clear whether he can form a government. Nearly all the other parties in the country dislike Wilders and he seems to prefer being in the opposition. However, if his party wins the largest share of seats, it will be difficult to create a government of minority parties. Thus, the Netherlands could face a situation of political instability even after the election.

France: The first round of elections will be held in late April. Assuming no candidate gains an outright majority (and that outcome isn’t expected), a runoff will be held in early May. Current opinion polls suggest that the center-right Republican candidate, François Fillon, is leading, with the National Front candidate, Marine Le Pen, in second. Both candidates are controversial. Fillon was PM in the Sarkozy administration. Politically, he is similar to supply-side American Republicans. He supports balanced budgets, tax cuts and fiscal restraint. Le Pen is a right-wing populist, Euroskeptic and anti-immigrant. In the past, when the National Front emerged from the first round to compete in the runoff, the rest of the establishment parties would unite around whatever establishment candidate was competing for the presidency. However, Fillon is considered radical by French standards and Le Pen could be considered more acceptable to left-wing voters. Although we would not expect a National Front victory, a Fillon-Le Pen election could lead to a populist government in France.

Germany: Although Chancellor Merkel has seen her popularity fall due to her support of immigration, her coalition of the center-left SDP and center-right CDU are currently polling with support of 44.5%. With Germany’s mixed proportional voting system, we would expect Merkel’s coalition to prevail, although with less power than the current arrangement. However, it should be noted that support for the mainstream parties has been declining. If France or the Netherlands produce populist outcomes, we could see a threat from The Left or Alternative for Germany, which are left-wing populist and right-wing populist parties, respectively.

Italy: Although the country doesn’t have scheduled elections in 2017, the recent failure of PM Renzi’s referendum on government restructuring has led to his resignation. If a new government cannot be formed, a no-confidence vote and snap elections are possible. There is a good chance populist parties will win and, if they do, the odds will increase significantly that Italy holds a referendum on exiting the Eurozone.

Even if the establishment parties maintain control, populist movements are forcing change. For example, Chancellor Merkel has recently called for bans on full-face veils usually worn by some Islamic women.3 In France, the most likely runoff will occur between non-traditional candidates. Mainstream parties are in retreat and thus policies that are less supportive of European unification should be expected. Combined with our expectations from President-elect Trump, Europe could face increasing turmoil next year.

Issue #3: The Fall of Islamic State

Islamic State (IS) is in clear retreat. It is facing a steady loss of territory in what was Syria and Iraq. Recently, IS admitted it had been ousted from Libya. The collapse of the proto-state in the Middle East is on the horizon.

This is good news but also an outcome with consequences—who will fill the power vacuum this creates? The Kurds will try to expand their territory already held in Iraq to parts of Syria. Shiite Iraqis will probably oppose this expansion. Turkey will also strongly oppose any expansion of Kurdish-controlled territory, fearful that this group will try to create a separate state in the region.

Although there has been a focus on IS due to its claim of creating a caliphate and its documented brutality, the fact of the matter is that Iraq and Syria are disintegrating and some other power is going to fill the vacuum. Unfortunately, the region will probably face further war after IS is removed from power. It is unclear how Western powers will handle wider conflict. History suggests that sides will be chosen and the region could devolve into a proxy conflict. Thus, even though defeating IS is a worthy cause, it won’t end conflict in the region.

Issue #4: China’s Financial Situation

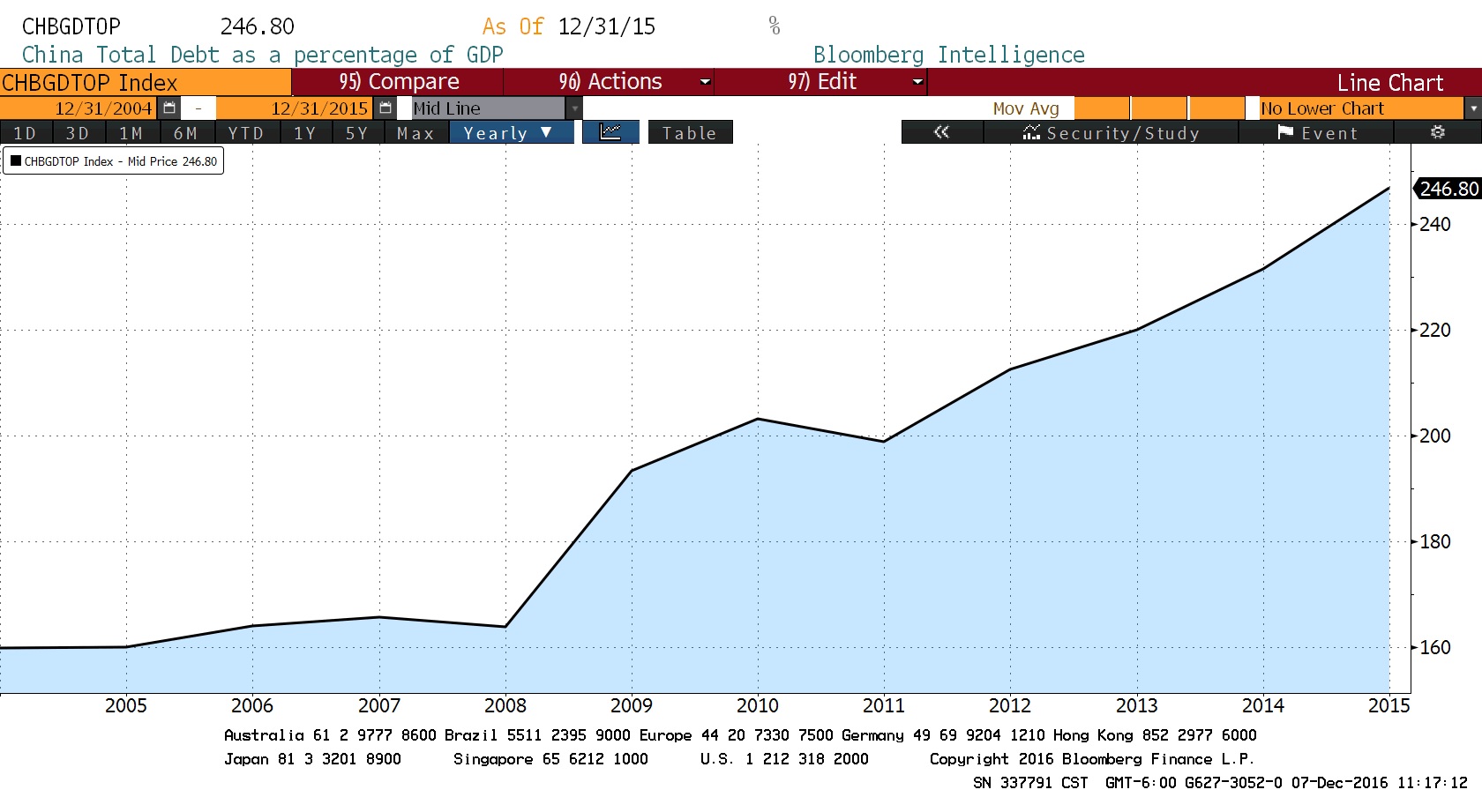

China’s debt has been growing at a furious pace. As the chart below shows, since the financial crisis, China has been taking on debt rapidly in order to maintain economic growth.

(Source: Bloomberg)

Rapid debt growth has been associated with economic crises in other nations. China does have high savings rates that should protect it from triggering a problem. We doubt China can avoid a rise in non-performing loans. The key issue is how the losses are allocated. In the past, China has allocated loan losses to the household sector. We suspect that will happen again.

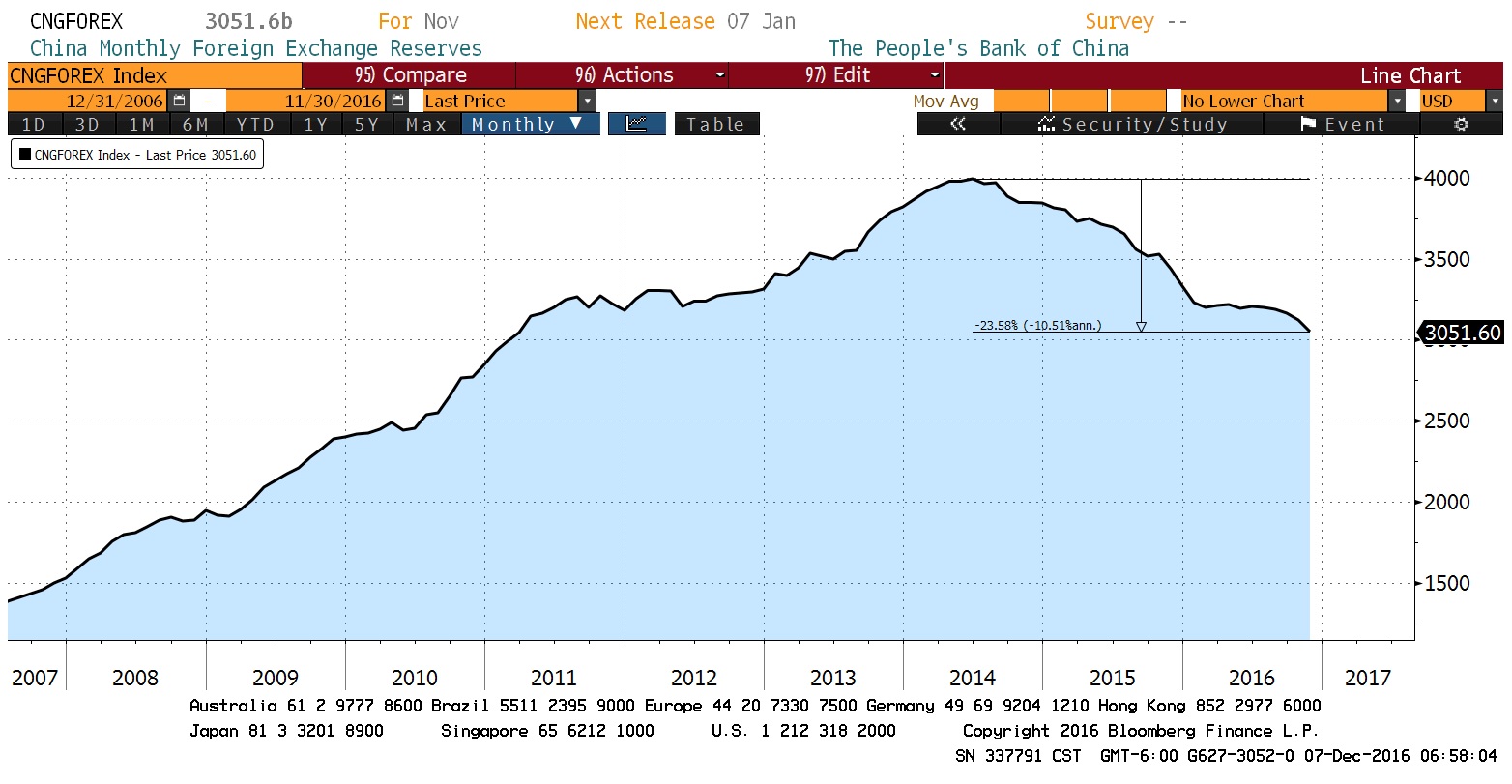

However, there is a concern that households and others may be worried about the assignment of losses or worse. Foreign reserves have been falling steadily for two years.

(Source: Bloomberg)

Foreign reserves peaked in mid-2014 and have declined nearly 24% since then. We suspect this drop is due to capital flight. At the end of November, the Chinese government implemented more stringent rules to prevent money from leaving China. This has caused great concern among Western firms who are finding it difficult to repatriate funds as part of their normal business operations.

Some of China’s capital flight is coming to the U.S. Local West Coast real estate markets have become targets of Chinese investors.4 Although capital flight is a benefit for the foreign nations who receive the flows, it could destabilize China’s economy. This could become an issue in 2017.

Ramifications

In our opinion, these four issues are the most geopolitically important for the upcoming year. Usually, geopolitical events tend to be bearish for risk assets. However, these particular issues could cause specific concerns. For example, a malevolent hegemon could be quite bullish for the U.S. but bearish for foreign markets. A strong dollar that comes from rising global instability could weaken emerging markets. Usually, a stronger dollar is bearish for commodities as well, but if the dollar strength is due to international instability then commodities will probably benefit. If European elections lead to an increase in populism, U.S. financial and real estate will look attractive as well.

President-elect Trump presents a unique set of risks that are not completely definable; in fact, unpredictability is seen as a virtue by the incoming president. At present, it is unclear if Trump will side with traditional supply-side Republicans or with right-wing populists. We expect him to attempt to placate both. But, in the end, rising populism will need to be addressed and this factor will need to be monitored in the coming year.

Bill O’Grady

December 12, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

© Confluence Investment Management

Read more commentaries by Confluence Investment Management