American Foreign Policy: A Review, Part II

Last week, in Part I of this study, we examined the four imperatives of American policy with an elaboration of each one. This week, we will discuss why each is important. We will examine why there has been a “drift” in American foreign policy since the end of the Cold War. This drift has now reached a critical point as the U.S. appears to be backing away from its postwar trade policies and the geopolitical imperatives that avoided WWIII. As always, we will conclude with the impact on financial and commodity markets.

The Importance of the Imperatives

To review, the U.S. had four geopolitical imperatives after WWII. They were:

1. Deal with the Soviet Union, in particular, and the threat of global communism, in general

2. Maintain peace in Europe

3. Maintain stability in the Middle East

4. Maintain peace in the Far East

All four of these imperatives were critical to maintaining global peace. Preventing the expansion of communism was “job one,” but removing the “German problem” from Europe was also very important as was keeping tensions manageable between China and Japan. Although it was difficult to justify supporting authoritarian regimes in the Middle East on moral or ethical grounds, it was necessary to maintain stability. Essentially, American foreign policy was designed to contain communism and freeze three potential conflict zones in Europe, Asia and the Middle East.

All of these imperatives require sacrifice. To bind Europe and Asia to the U.S., open (rather than free) trade was embraced; both Germany and Japan established economic policies that were the mirror image of American policy. These recovering nations suppressed consumption and maintained undervalued exchange rates in order to create trade surpluses that the U.S. absorbed. It allowed both nations to recover from the devastation of WWII, remain in the free world and become economic powers in their own right. Other nations followed this policy mix with positive results. A series of nations around the world adopted similar policies that allowed them to develop using the reliable demand from the American consumer.

Until the 1970s, the U.S. economy was proportionally large enough to absorb these imports with little impact on employment. However, as the size of the U.S. economy has shrunk relative to the rest of the free world, employment began to be adversely affected. To some extent, the U.S. was a victim of its own success.

The supply-side policies of the Thatcher/Reagan revolution led to increased globalization, outsourcing and the rapid introduction of disruptive technology. These policies were remarkably successful in reducing inflation from 1965 through the 1980s. However, this drop in inflation came at the cost of increasing U.S. income inequality. In order to maintain enough spending to fulfill the reserve currency role in the face of falling incomes, the U.S. deregulated its financial system and supported debt accumulation.

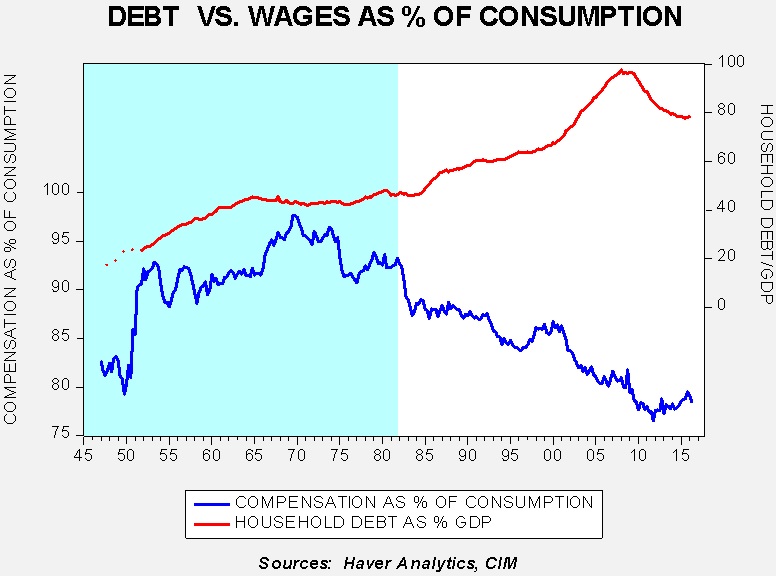

This chart shows the level of consumption that could be funded by worker compensation (lower line) and the household debt/GDP ratio. Until the early 1980s, compensation would fund 90% to 95% of household consumption. Since then, the ratio has steadily declined, now only funding about 78% of consumption. The rest is funded by transfer payments and debt (the debt statistic shown on the upper line). Household debt to GDP almost reached 100% at its peak; deleveraging since the financial crisis has reduced this ratio to 78.4%. Although there is no “magic ratio” of debt/GDP that completely signals sustainability, we estimate that a ratio around 60% is probably maintainable at normal interest rates.

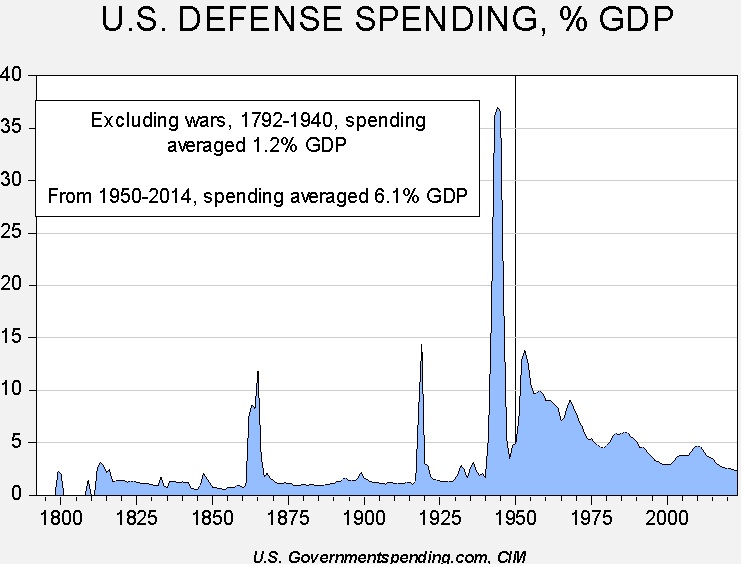

The security requirements of the four imperatives were also costly. The next chart shows U.S. defense spending as a percentage of GDP. Prior to the Cold War, defense spending tended to track wars; during wars, the U.S. would mobilize its military and demobilize once the conflict ended. During the Cold War, spending remained permanently elevated to meet the aforementioned imperatives.

The reserve currency role and military spending represented global public goods supplied by the U.S. economy. There are benefits Americans receive from these factors, such as the fact that the U.S. can run trade deficits with little fear of currency problems due to the natural demand for dollars that comes from the reserve currency role. However, it does endanger industries that compete globally and leads to higher U.S. unemployment as industries find themselves facing withering foreign competition.

The Populist Reaction & the Costs

This election cycle, we are seeing a populist reaction against what are essentially superpower policies. Both Donald Trump and Bernie Sanders have called for reducing America’s foreign policy commitments. The fact that Trump won the Republican Party’s nomination and Sanders came close to winning the Democratic Party’s nomination shows the power of these ideas. Yes, they both had other positions but, for the most part, implementing their policy platforms would, at best, require a major adjustment in America’s superpower role and could very well lead to an outright rejection of the role. Overall, it appears that Americans are tiring of the costs of hegemony.

However, before one accepts the populist position of hegemonic rejection, at least as it was practiced for most of the past seven decades, we should understand the costs. Let’s examine the potential outcomes of rejecting the four imperatives:

Containing communism and Soviet expansionism: At first glance, this imperative appears to have been met. America and the free world did win the Cold War. However, as Kennan noted, Russia’s expansionist behavior wasn’t because it was communist; instead, communism became expansionist because it originated in Russia. Russian expansionism is rooted in its geopolitics. It has historically defended itself by creating large buffer zones and taking advantage of brutal Russian winters, which forced invaders to traverse long distances and dangerously extend supply lines. Both Napoleon and Hitler fell victim to Russia’s time-honored defense methods. Russia’s expansionism has been historically constrained by its poverty; it eventually can’t afford to dominate its “near abroad.” Although it does occasionally lose control of this region, it always works to retake the near abroad over time.

The West’s mistake after the Cold War was to assume that Russia would become a Western nation once communism was abandoned. Instead, it reverted to its earlier form of Russian nationalism. It views buffer zones as key to its survival and is willing to go to great lengths to establish these areas. Thus, its belligerence in Ukraine should not surprise anyone who understands Russian history. In other words, although the U.S. won the Cold War, all we did was defeat communism. However, Russia remains a threat.

Maintain Peace in Europe: The key to maintaining peace in Europe is to resolve the German problem. The division of Germany into East and West Germany and its demilitarization mostly ended this threat. However, post-unification, Germany’s economy again dominates Europe and it has unexpectedly used the creation of the Eurozone to expand its influence. Brexit will further concentrate power in Germany’s hands.

There is nothing to suggest that Germany is striving to regain military superiority. It seems it would prefer to remain an American client state. However, the foreign policy proposals of Trump and Sanders suggest the U.S. wants NATO members to spend more on their own defense. Although this is a worthwhile goal, the problem that follows is if the EU develops a formidable military then it may decide to follow a foreign policy independent of U.S. goals. There is no guarantee, in fact it would be naïve to expect, that if European taxpayers devote more of their fiscal spending to defense that they would still follow American foreign policy aims. A remilitarization of Europe would likely bring a return of the German problem and create conditions that might foster war.

Maintain stability in the Middle East: It is notable that President George H.W. Bush commanded a war that removed Iraqi forces from Kuwait but went no further, while his son removed Hussein from power, leading to the eventual destruction of Iraq’s borders. The first Bush’s policies were designed to protect the status quo in the region. The second Bush’s policies ended the status quo and created conditions for wider turmoil. The latter Bush’s plan was to remove Saddam Hussein from power and instill democracy. Unfortunately, George W. Bush apparently didn’t understand the colonial structure of Iraq. Democracy meant the majority Shiites would control the government, a prospect that terrified the minority Sunnis who had dominated the Iraqi government from the days of British rule. Iraq has devolved into civil conflict that has developed sectarian and ethnic overtones. At present, the colonial borders of Iraq have disappeared in the west and the north as the Kurds and Islamic State dominate much of what was Iraq. Syria has also collapsed into civil war.

At this juncture, it appears that stability is probably lost. Perhaps the only power in the region that could establish stability is Turkey, but that would require the Turks to occupy large portions of what was Iraq and Syria. The U.S. has essentially allowed the status quo to end and may have created conditions of near constant warfare. The region is riven by religious and ethnic divisions, creating conditions similar to the European 30-Years War. These wars could create training grounds for a generation of terrorists. There is no easy solution to the failure of this imperative; allowing the “nations” in the region to form organically likely leads to continued conflict for the foreseeable future.

Maintain Peace in the Far East: America’s decision to guarantee Japan’s security has maintained stability in Asia for decades. Donald Trump’s offhand comments suggesting that Japan and South Korea should defend themselves opens the possibility that Japan would become an offensive military power. With China attempting to gain control of the seas surrounding it through island building, the chances of a conflict are rising. American presence in the region has maintained peace since WWII. Reducing our influence raises the likelihood of regional conflict.

The Crux of the Problem

Perhaps the best way to view America’s foreign policy is that we reluctantly accepted the superpower role in order to avoid fighting WWIII. We did it by (a) containing the Soviets (Russians), (b) solving the German problem by demilitarizing Europe, © maintaining the status quo in the Middle East, and (d) demilitarizing Japan. Essentially, America contained the Russians and froze three potential conflicts in Europe, the Far East and the Middle East. It makes sense to assume that if we abandon these policies, the frozen conflicts will thaw (it’s likely that the Middle East conflict has already defrosted) and regional wars will become much more common. The Obama administration’s “pivot to Asia” is, in a sense, a recognition of weakening American bandwidth. Essentially, the administration wanted to reduce its interest and influence in the Middle East to focus more resources on the Far East. The outcome wasn’t optimal—we got the Arab Spring and the collapses of Iraq and Syria.

Most Americans were on board for meeting the first imperative. It was almost universally held that communism was a major threat and the Soviets needed to be contained. However, the other three imperatives were either not recognized or were considered part of the first imperative and no longer necessary after the Soviet Union devolved.

Consequently, when the Berlin Wall fell and the Soviet Union dissolved two years later, most Americans believed that they had “won the war” and the need for hegemonic sacrifices was no longer necessary. In fact, the four imperatives still remain and still include the financial role of providing the reserve currency. If the hegemonic role is abandoned, history suggests a world of great tumult. Regional wars will proliferate and global trade will decline.

The Elections

It would be simple to suggest that Clinton, running as the establishment candidate, would not endorse a wholesale rejection of the four imperatives, whereas a Trump presidency would lead to their rejection. The problem is more complex; the populist arguments have a degree of legitimacy. The costs and benefits of American foreign policies are not equally distributed; for the most part, the establishment has generally benefited from America’s superpower status as they are more employable in a globalized world.1 Without equalizing burden sharing, it makes sense for the populists to argue for a rejection of the four imperatives and the superpower role.

At the same time, one has to be aware that rejecting the four imperatives and the superpower role will lead to a less stable world, one that is more likely to see regional wars. The U.S. will likely remain safe—Canada and Mexico are no military threat—but, at some point, these regional conflicts could involve the U.S.

Ramifications

So, if the U.S. abandons the superpower role, or begins to scale it back significantly, what happens to markets? We expect at least five significant trends to develop.

1. Foreign investing becomes problematic. Everything we know about foreign investing has occurred in an environment where the world had a hegemon providing the global public goods of a reserve currency and geopolitical security. Foreign investing takes on additional risk factors for which we have little history to use as an analog.

2. U.S. investing becomes much more attractive. Not only is it likely that North America becomes an oasis of stability in an uncertain world, but the U.S. is the strongest nation on the North American continent. Global capital will be seeking safety and the U.S. will probably become the target for capital flight. Thus, U.S. financial and real estate assets will be especially attractive. The dollar should also benefit.

3. Outsourcing will become less attractive due to the lack of geopolitical stability. Large cap stocks will suffer as their supply chains shrink, giving small and mid-caps an edge until these supply chains are adjusted.

4. Although the stronger dollar will act as a damper on commodity prices, we do expect rising precautionary demand for raw materials as companies, governments and households shift from “just in time” inventory management to “just in case” methods. The uncertain supply, caused by the instability of the reserve currency and regional conflicts, will make key commodities attractive.

5. Fixed income outside the U.S. will become quite risky as inflation will likely rise due to the steady erosion of globalization. U.S. rates will likely rise as well but at a slower pace because of capital flight.

Thus, U.S. investors will likely position their portfolios domestically, with a bias toward small and mid-caps in equities and an allocation in real estate and commodities. Duration in fixed income will be shortened and foreign bonds will likely be avoided.

It is still possible that the U.S. can build a political consensus to allow for the superpower role to continue. Policies that allow for greater burden sharing, both at home and abroad, would allow American hegemony to continue. Framing the geopolitical case for American hegemony, which requires great political skill, is probably necessary as well. Given the current state of politics in America, we are pessimistic this favorable set of policies will emerge. And so, we are closely monitoring the steady decline of American influence in the world and preparing for a geopolitical vacuum of a G-0 situation.2

Bill O’Grady

October 10, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 A common charge is that the volunteer military is populated with the poor. A series of studies suggests that the upper income brackets are also well represented in the volunteer military. In part, this is because the educational requirements of the modern U.S. military is high enough to exclude many of the underprivileged. See: http://www.heritage.org/research/reports/2008/08/who-serves-in-the-us-military-the-demographics-of-enlisted-troops-and-officers.

We note that this report is somewhat dated and may not reflect the current situation. In addition, in the state by state data, there is a heavy overrepresentation in the military from the South, mountain West and the “rust belt” states, and lower representation fromthe proverbial “establishment” states, California and New York (see Map 2 of the linked report). The perception that the offspring of the establishment are underrepresented in the Armed Forces is difficult to prove conclusively from income data alone. However, the geographic distribution of enlistment does suggest that establishment underrepresentation is plausible.

2 Bremmer, I. (2013). Every Nation for Itself: Winners and Losers in a G-0 World. New York, NY: Penguin Group.