On June 23rd, voters in the U.K. shocked global markets by voting to leave the EU. In this report, we will examine the various paths the country may take in the coming months with regard to this issue, discuss the political lessons learned and the impact Brexit will have on other European nations. As always, we will conclude with the potential impact on markets.

Brexit—Now What?

In the aftermath of the Brexit vote, PM Cameron announced he would be stepping down in September and the ruling Conservatives will select a new prime minister. Over the past week, the Tories, who are members of Parliament (MPs), voted on potential replacements for Cameron. The party started with five candidates and, through party voting and resignations, that group has narrowed to Home Secretary Theresa May. Energy Minister Andrea Leadsom pulled out of the race today. May is a member of the “remain” camp but has indicated that she will respect the will of the people expressed in the referendum vote. Leadsom supported the “leave” campaign. Thus, her exit from the campaign does have an impact on whether or not Brexit actually occurs. It is unclear at this point, even though May is the only remaining candidate, whether the party will hold a membership vote in September to formally select her as the new prime minister.

The June referendum expresses the will of the people but the actual process of leaving the EU only occurs with an act of Parliament.1 If Parliament fails to approve a formal decision to exit the EU, known as invoking Article 50 of the EU charter, Brexit won’t occur.

May has already indicated that she won’t begin the process of invoking Article 50 until 2017. At some point, the next PM will present a vote to Parliament. It is quite possible an Article 50 vote will fail and Brexit, despite the referendum, won’t occur. On the other hand, if the MPs vote to exit, the U.K. government will begin formal negotiations to leave the EU.

Assuming May does win the leadership vote within the Tories, which is almost a certainty given that she faces no opposition, we would not be shocked to see her call for snap elections, especially if she intends to reverse the Brexit referendum. Although the Conservatives only hold a narrow five-seat majority in Parliament, the Labour Party is in disarray and winning an election would give May a new mandate. In effect, the new elections would probably be another referendum on Brexit, especially if May argues that a vote for her is a vote to remain. The only alternative to those supporting exit would be to vote for the U.K. Independence Party, which has just seen the resignation of its longtime leader, Nigel Farage.

Essentially, the exit voters would be left without a real choice and May would likely be able to reject the referendum. Of course, this would only work if she runs specifically on a platform to reverse the referendum, which might be difficult for her to pull off as it would divide the Conservatives and might trigger a vote of no confidence against the PM.

Another tactic would be for May to hold a snap election, campaigning for exit. It is quite possible that the Tories would fail to gain a majority (as noted above, they only hold a five-seat majority) and any of the major parties would refuse to form a government without the promise of remaining in the EU. It is doubtful that the U.K. Independence Party would gain enough seats to form a government with the Conservatives, and so a vote to invoke Article 50 might never occur.

The bottom line is that it is still quite possible that Brexit never occurs. If the U.K. stays within the EU, it would likely trigger a significant relief rally in financial markets. In fact, we saw a strong market recovery with Leadsom’s withdrawal, with U.K. equities and the pound rising.

Lessons Learned

The first lesson learned is that polling and betting pools have become less reliable. Pre-Brexit polls and the betting pools consistently showed the remain side winning. We note that the betting sites did report the amount of money being bet in favor of the remain outcome exceeded those wagering on exit, but the volume of trades favored leaving the EU. In other words, more numerous small bettors were leaning on exit while it appears that fewer wealthier bettors were wagering on remain.

This discrepancy in polls could reflect a phenomenon called “preference falsification.”2 Under conditions of preference falsification, voters may misrepresent their true desires due to social pressures. If the “proper” position is to vote for remain, voters may lie to pollsters about their actual preferences.

If preference falsification is prevalent in the U.S., Donald Trump may be doing better than current polls and betting sites indicate. Simply put, in controversial circumstances, the potential for election surprises is unusually elevated. And so, markets can be vulnerable to misreading the outcome before the vote.

The second lesson is that, even if Brexit does not occur, the referendum is a clear signal of discontent. The first risk discussed in our Mid-Year Geopolitical Outlook3 was the Rise of Populism. The U.K. vote is a clear expression of this anger.

Although there are various facets of this populist trend, perhaps the best way to understand it is based on the idea that society makes a grand tradeoff between efficiency and equality.4 Efficiency is part of creative destruction. Globalization and deregulation are the primary tools of efficiency. In the long run, society benefits from efficiency—we are able to create more goods and services with fewer resources. However, in the short run, some people will suffer dislocation from this process. Taxi drivers are facing competition from Uber; the combination of “semi-pro” drivers and technology is undermining the traditional livery model and reducing the wages of cab drivers. Online maps have put atlas publishers out of work; online applications have eliminated the need for telephone books. For those who worked for map or phone book printers, their careers have ended. For society in general, this is an improvement. Online applications can be easily updated and they are faster to search. In addition, they can link to maps that offer directions. But, for those individuals who have lost their livelihoods, it’s hard to support this development.

Economists have long recognized this issue and offer bromides about how society should compensate these short-term losses out of the broader gains to society. In real life, that rarely happens. At the same time, policymakers have, throughout history, tilted toward efficiency or equality at various times. In the U.S., efficiency triumphed into the early 20th century when Teddy Roosevelt moved to reduce the power of business. Into WWI, a host of new laws designed to improve the lot of workers, including child labor restrictions, work hour restrictions, food safety rules and anti-monopoly laws were passed. This progressive policy trend stalled during the 1920s but roared back during the Great Depression and through the 1970s.

Supporting equality requires some reduction in efficiency.5 Ideal policy deftly balances the two, allowing enough efficiency to keep inflation controlled and boosting potential long-term growth but providing enough equality to maintain political stability and promote short-term consumption. In reality, since efficiency and equality tend to develop their own constituencies, what is actually observed are cycles where either equality or efficiency is emphasized.

We are currently in an efficiency phase, which began in the late 1970s with the Reagan-Thatcher revolutions. The rise of populism suggests that this efficiency cycle may be coming to a close.

Policymakers, mostly drawn from the political establishment, could potentially extend the current cycle by dialing back some efficiency-supporting policies. Fiscal expansion would be a way to potentially contain the current populist surge. For example, allowing Italy to use public funds to recapitalize its banks would likely stall the rise of the Five Star populist party. Of course, this action would tend to reward bad banking practices and signal to creditors that their bank bonds are safe at any price. However, forcing losses on these same creditors will almost certainly promote a populist backlash that will put the Eurozone project under threat. Similarly, in the U.S., expanding public investment could produce, at a minimum, construction employment. If this investment is well-executed, it could actually increase potential growth.6

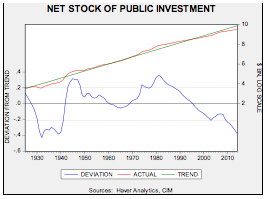

This chart shows the net stock of public investment, log scaled regressed against a time trend. The lower line in the chart shows the deviation from trend. Much of public investment is tied to military spending. Net public investment tends to decline during periods when efficiency is being emphasized because, in general, private investment is more efficient. Even during the New Deal, the decline in public investment was only arrested, and did not increase above trend. WWII clearly led to a massive lift in public investment that was maintained through the Cold War and into the Reagan-Thatcher Revolution. However, since 1980, net public investment has been steadily declining against trend. It is now at its lowest levels since the1930s. As we discuss in footnote #5, creating productive public investment in a developed economy is difficult but, given the low level of net stock to trend, we suspect that there is room for spending, even if it merely protects existing infrastructure.

If policymakers fail to address the concerns reflected in the populist surge, we may be nearing a new equality cycle. We will discuss this issue in the Ramifications section below.

Brexit and Europe

Immediately after the Brexit vote, populist parties in France and the Netherlands called for similar votes in their countries. We would not expect those votes to occur. The political establishment in Europe views Cameron’s decision to hold a referendum in order to quell backbencher unrest as a serious mistake.

However, the bigger risk for the EU is the establishment’s persistent underestimation of the risks from rising populism. The next major test will be from Italy, where a serious banking system problem is brewing.7 Estimates suggest that up to 17% of Italy’s non-performing loans will default. If this number is correct, some degree of bank recapitalization will be necessary. Under current EU rules, the first line of defense is bank creditors—bondholders and depositors. This German-inspired program is designed to protect taxpayers (read: German taxpayers) from having to bail out bad banks. The problem is that such a program is a recipe for bank runs.

If Germany maintains its stance on the Italian banking system and does not allow a government bailout, the Five Star movement could take power and it would likely want to not only leave the Eurozone, but the EU as well. Italy leaving is a much more serious threat to both organizations than Britain’s potential exit. After all, a major nation exiting the Eurozone will not only disrupt that system (imagine how investors in Italian sovereigns will react to accepting payment in the new lira rather than euros), but might encourage other nations to leave as well.

German policymakers seem to misunderstand that the Eurozone has become something of a German colony. The German economy has become very dependent on exports; if nations leave the Eurozone and can depreciate their currencies against the euro or the new Deutsche mark, the German economy will likely suffer a significant shock.

Note that at the onset of the euro, in 2000, exports represented about 32% of German GDP; they now represent 46% of GDP. Germany should, at all reasonable costs, do everything it can to maintain the integrity of the Eurozone, even if that means bending the banking rules to allow the Italian government to support its banking system. At this point, there is little evidence to suggest any flexibility in Berlin. That rigidity could pave the way for another EU crisis this fall.

Ramifications

Since the late 1970s, we have been living in a policy environment designed to quell inflation. The policies in place have tended to support efficiency over equality. The rise of Trump and Sanders, the Brexit vote and populism in Europe all suggest that those who feel the benefits they derive from efficiency are less than the costs they bear are rebelling.

As noted above, policymakers could bend a bit toward equality and still maintain much of the efficiency policy program. This would involve lifting transfer payments, perhaps tying these to work,8 and expanding public investment.

The risk is that a bigger rebellion takes place which would deglobalize and re-regulate the economy. Both Sanders and Trump strongly support trade barriers and discourage foreign investment. Sen. Warren recently criticized the technology sector for its growing concentration,9 which is a significant change from her usual criticism of the financial services industry.

If we see a full swing toward equality policies, the investing trends of the past 35 years will likely be reversed. Bond yields will rise, equity markets will face headwinds in the form of contracting P/E multiples and inflation will rise over time. It is not out of the question that central bank independence could be curbed. This shift is something we monitor very closely because it would engender a fundamental change in the underlying conditions that would require investors to reevaluate their positions, especially in fixed income.

In terms of the U.K., if Theresa May becomes PM, the financial markets may begin to re-price British financial assets if the odds of Brexit decline. This situation may provide a short-term opportunity for investors. For now, efficiency policies remain in place; thus, major allocation shifts are not presently necessary.

Bill O’Grady

July 11, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

|

1 This is the position of the U.K. Constitutional Law Association. Although this position is not universally held, the general consensus is that an act of Parliament is necessary to invoke an Article 50 declaration. This stance was reiterated by over 1k lawyers in Britain in a letter to PM Cameron. http://uk.reuters.com/article/uk-britain-eu-lawyers-idUKKCN0ZR0K2

2 Kuran, T. (1997). Private Truths, Public Lies: The Social Consequences of Preference Falsification. Cambridge, MA: Harvard University Press.

3 See WGR, 6/27/16, The 2016 Mid-Year Geopolitical Outlook.

4 The seminal work on this topic comes from Arthur Okun. Okun, A. M. (1975). Equality and Efficiency: The Big Tradeoff. Washington, D.C.: Brookings Institution Press.

5 It can be argued that, at extreme levels of inequality, some loss of efficiency might still improve the public welfare.

6 Determining the level and type of public investment is very difficult in a developed economy. Clearly, the interstate highway system was a public investment that boosted the growth potential for the overall economy. At the same time, one cannot get the same boost by building it again. What sort of investment might make sense? The government fostered universal telephone service by allowing AT&T to have near-monopoly status in return for providing national phone coverage. The firm did so by subsidizing local residential calling by overcharging on long-distance calling, which was mostly done by businesses. In many respects, our modern cell phone system probably could not have developed under the AT&T monopoly. At the same time, it is doubtful the private sector would have provided universal phone service either. The government could support universal high speed internet coverage by granting Alphabet (GOOG, 700.13) monopoly status to provide it at a low cost. Creating new regulations that support entrepreneurship and the “gig” economy via portable health care and pensions might also be wise public investments. On the other hand, investing in new roads or airports might make travel somewhat easier, but the return on investment would likely be miniscule.

7 See WGR, 1/25/16, Italy’s Banking Crisis.

8 The Earned Income Tax Credit could be expanded to include single workers and made more generous.

9 http://money.cnn.com/2016/06/30/technology/elizabeth-warren-google-apple-amazon/

© Confluence Investment Management