In February, we presented an analysis of Brexit, which is shorthand for Britain’s potential departure from the European Union (EU). The referendum is slated for June 23.[1] In general, the points discussed in the aforementioned report on the economy, trade, regulatory policy, immigration and the U.K.’s geopolitical “footprint” all still hold. There are potential risks to the U.K. political system and economy from leaving the EU. However, there is also, in my opinion, an underappreciated risk to the EU as well.

The problem can be summed up in this question—what if the U.K. leaves the EU and prospers? This has the potential to be a major problem for the postwar European political environment. In this report, we will discuss the role of the EU in shaping the postwar geopolitical environment in Europe and the multiple threats Britain’s exit presents for the EU. As always, we will conclude with the impact on financial and commodity markets.

The EU Response to World Wars

Following two world wars, most of Europe lay in ruins. Both wars failed to address the “German Problem,” the problem of an economic powerhouse situated in a region of Europe that was completely indefensible. Germany’s rising economic prowess after its unification in 1871 became a growing threat to the established order of Russia, France and Britain. Germany was well aware of its precarious geopolitical position and, in response, built a formidable military. Its defense doctrine was based on the Schlieffen Plan, which called for a massive attack on northern France by crossing through neutral Belgium and the Netherlands to knock Paris out of any war and then shift to attacking Russia on the Eastern Front. The goal was to avoid the dreaded two-front war.

In WWI, the plan failed. The French military managed to prevent the German Army from capturing Paris and controlling the country. WWI soon devolved into a war of attrition characterized by trench warfare. After more than four years, the war ended with the Treaty of Versailles. The treaty was deeply flawed—harsh enough to hurt the German economy and breed resentment but not so draconian as to prevent Germany from rearming and threatening the European continent again. In addition, mostly due to the work of President Woodrow Wilson, the concept of self-determination was unleashed on Europe, which led to rising nationalism. In less than two decades, the German Problem resurfaced through the rise of Adolph Hitler and the Nazi Party. The continent was soon plunged into WWII.

European leaders had two goals in the aftermath of WWII. First, they wanted to foster the economic recovery of the devastated continent. Second, they wanted to prevent the conditions that led to two world wars being fought on their soil from occurring again. This included addressing the German Problem.

Economic recovery came by tying the European economy to the United States economy. Bretton Woods, which established the dollar as the free world’s reserve currency, and the Marshall Plan both supported European rebuilding. The latter gave direct aid to Europe to boost its recovery, and the former gave European firms a ready market for exports. These two policies supported the European postwar recovery.

The second goal was ultimately met by a series of steps whose objective was to weaken nationalism within European states. Nationalism is a strong force everywhere, and in Europe, the notion of the nation and the “people” can be very close. As we have noted on numerous occasions, if one comes to the U.S., takes the citizenship test and passes it, one becomes an “American.” But, in Europe, this is less common. Yes, one can move to France, learn the language and pass the citizenship test to become a citizen of France, but one will never truly be “French.”

To overcome the pernicious effects of nationalism, the leadership of Europe tried to foster an allegiance to the continent rather than to the individual states. This began with the European Coal and Steel Community that was established in 1951 with six nations, then evolved into the European Economic Community with a dozen members, and finally became the current European Union consisting of 28 members. The political elites of Europe knew that overcoming nationalism would be very difficult. The goal of the EU was to expand economic prosperity, making economic growth a replacement for national identity. The crowning achievement of this movement was the creation of the Eurozone, where 19 European nations use a single currency, the euro, and effectively relinquish control of their monetary policy to the European Central Bank (ECB).

At its most basic level, the supra-nationalist movement succeeded. No third world war has been fought in Europe. The German problem was generally managed, at first by dividing the country and, after unification, by Germany joining the Eurozone and giving up the Deutsche mark. Of course, a key reason for the European project’s success was that the continent outsourced its defense to the U.S. As the Western European militaries atrophied, their ability to wage war on each other (or anyone else, for that matter) waned.

Although the EU and its predecessor organizations have managed to prevent WWIII, it has come at the cost of reduced national sovereignty. Within the Eurozone, it has become evident that Germany dominates the single-currency bloc. Greece discovered that it is completely beholden to the German government for debt relief. In addition, EU bureaucrats have extended their reach into other areas of European life, overruling local governments on environmental and agricultural policies. The national central banks have become nothing more than arms of the ECB.

One of the other major achievements of the EU is the Schengen Area, which allows for nearly free travel for EU member citizens across European borders. Although this did make the European continent more economically efficient, nations within the EU also discovered that they had lost control of their national borders. This issue became controversial with the recent surge of refugees from the Middle East and North Africa. Once these refugees made it into the Schengen Area, they were able to travel almost unimpeded until states reestablished “temporary” border controls.

The EU project has been essentially a trade—nations give up some degree of sovereignty in exchange for economic prosperity and peace. On a purely intellectual level, this tradeoff seems reasonable. However, sovereignty, like nationalism, isn’t just an intellectual issue. It’s emotional as well. No amount of prosperity can replace the emotional feeling of hearing one’s national anthem. The EU political leaders have tried to weaken nationalism; the fact that the pictures on euro paper currency represent no specific place was intentional.

The refugee flow, the debt crisis that weakened growth across southern Europe, continued sluggish economic growth and a seemingly irresponsive political class have fostered populist movements across Europe. That populism has, in many cases, evolved into Euroskepticism, exhibited by the Brexit referendum.

The Real Risk of Brexit

The “remain” campaign has argued that Brexit would be an economic disaster. Trade deals would have to be renegotiated, the financial center status of London would be at risk and isolating the island nation from Europe would reduce the U.K.’s political influence. All this might be true.

Or, it might not. The U.K. is a significant economy. EU nations would probably want to retain relations with Britain. Although Scotland has suggested it might leave the U.K. to rejoin the EU, it isn’t obvious that the latter would be open to accepting another small nation into its ranks. After all, the U.K. puts more into the EU coffers than it draws. Scotland would likely be a drain on EU resources.

The key problem for the EU is its promise to members of prosperity by relinquishing part of each nation’s sovereignty. If a major nation were to leave and maintain its economy, it would severely undermine the basic rationale for joining the EU. If the U.K. leaves the EU and an economic collapse is avoided, other nations within the EU will surely be tempted to follow the U.K. out of the EU.

In addition, an EU without the U.K. would remove a significant counterweight to Germany and make it much easier for Germany to dominate Europe. Already, it is clear that Germany dominates the Eurozone. Germany’s weight in the EU will be higher if the U.K. is unaffiliated with the EU.

Essentially, European political leaders took a calculated risk that they could entice nations to swap sovereignty for economic growth. If it turns out that being a member of the EU isn’t necessary for economic prosperity, or at least leaving doesn’t hurt the economy significantly, it will become more difficult to keep nations within the grouping.

Unfortunately, the U.K.’s consideration of Brexit is coming at a time when there is a growing isolationist sentiment in the U.S. Although Sen. Clinton has a foreign policy stance that isn’t much different from many neoconservatives, both Donald Trump and Sen. Sanders are running on primarily isolationist platforms. Trump’s foreign policy is Jacksonian while Sanders’s policy is Jeffersonian.[2] If Brexit occurs as the U.S. security guarantee is eroding, the EU will be vulnerable to losing a major military ally such as the U.K. Of course, the EU will likely try to maintain NATO relations and keep the U.K. in the security arrangement. In fact, the EU would probably want to strengthen its security relations with the U.K. and the latter could use that leverage in trade negotiations.

The EU leadership, for the most part, has a great incentive to take measures to undermine the U.K. economy if the Brexit vote passes. Otherwise, the entire EU project could come under pressure from other defectors.

If the EU begins to unravel, the longer term risk is that conditions that existed prior to the creation of the union which led to two world wars would return. In other words, we know, for a fact, that Europe has not spawned a third world war. However, we don’t know the reason behind this fact. If this terrible event hasn’t occurred because of the steady economic unification of Europe, then Brexit is a profoundly dangerous idea. On the other hand, it is quite possible that war has been avoided simply because the U.S. disarmed the region. If that is the case, Brexit probably isn’t all that dangerous and the real key to European security rests on the decision American voters will make in November.

In general, it is almost an article of faith that trade and economic interdependence reduce the odds of war. Although these factors do increase the costs of war, WWI proved that trade didn’t prevent war in Europe. The steady economic integration did help solve the German Problem in that it helped relieve the German fear of invasion by creating a collegial atmosphere in Europe. However, none of that would have occurred without the U.S. security blanket. If the U.S. decides that it will no longer provide nearly free security to the continent and the Europeans are forced to rearm, it is highly unlikely that the EU structure alone will be enough to prevent future wars.

Ramifications

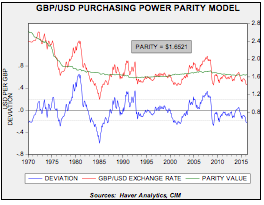

In the short run, the most sensitive financial relationship to Brexit is the GBP/USD exchange rate. The pound has declined due to worries about Brexit. Even if the vote to leave occurs, we suspect the worries over the U.K. economy are overblown and an appreciating pound would offer some support for British financial assets.

Based on purchasing power parity, the pound is undervalued. Since 2000, based on the levels of valuation, it has been favorable to own the pound. Obviously, if the EU decides to undermine the U.K. economy in response to leaving the union, the prior relationship may not hold. However, we doubt that the EU will act harshly toward the U.K. because it simply isn’t in Europe’s interest to punish a large economy that might trigger economic “blowback” if the EU acts in a punitive fashion.

Longer term, Brexit could undermine the entire EU project. Although we doubt the current generation will have to deal with European rearmament and a return of the German Problem, the next generation will likely see elements of these issues and the third generation will almost certainly see it and perhaps wonder why seven decades of peace were squandered.

Most likely, the lack of confidence in America’s ability to manage the superpower role has fostered a rise in nationalism globally, but especially in Europe. It is possible that new leadership in the White House might change that trend but, at this juncture, hopes for such an outcome are facing long odds. Brexit, then, may simply be a reflection of global insecurity. In other words, if international organizations fail to offer protection, going on one’s own may be an attractive alternative.

Bill O’Grady

June 20, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

|

1 See WGR, 2/29/2016, Brexit.

2 Using Walter Russell Mead’s archetypes. See WGR, 4/4/2016, The Archetypes of American Foreign Policy: A Reprise.

© Confluence Investment Management