SUMMARY

- In the aftermath of the financial crisis, there had been widespread hope that the 20% fall in sterling would mean that this UK recovery would be export led. However, this recovery has followed a familiar path of falling mortgage rates, rising consumer confidence and rising house prices, with rises in house prices comfortably outstripping wage increases.

- For the UK recovery to be sustainable over the medium term, further progress on wages, and ideally productivity, is required.

- In our view, there is little urgency to raise interest rates as inflation remains comfortably below target, consumer spending has been outstripping spending and the savings rate is at an historic low. That should change with better wage growth through 2016, but even then the path of rate hikes is likely to be very benign.

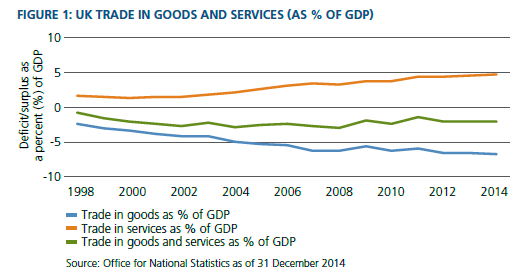

In the immediate aftermath of the global financial crisis, there was widespread hope that the 20%–25% fall in the trade-weighted value of the British pound would rotate the UK economy away from its reliance on domestic demand and toward the export sector. After a decade before the crisis, in which the UK trade deficit had averaged 2.2% of gross domestic product (GDP), a more competitive manufacturing sector was expected to stabilise the traded-goods deficit, while a large and potentially rising surplus in the service sector would bring the deficit back into balance.

Unfortunately, this is not how things have played out (see Figure 1). The overall trade deficit has been stuck at 2%, with the actual cash deficit staying unchanged and a rising GDP playing its part in reducing the deficit as a percentage of the overall UK economy. Meanwhile, the diverging fortunes of the goods and services sectors have continued unabated.

The current state of the UK recovery

Thankfully, that has not prevented the UK recovery from gaining traction, with total output now 5.9% higher than the prior peak in mid-2008. UK employment is at a record high, for both total and full-time employees, real wages are rising and the UK government deficit is now coming back under control. So should we be worried about another domestically based recovery, and are there troubling aspects to this recovery that increasingly mirrors those prior to the global financial crisis?

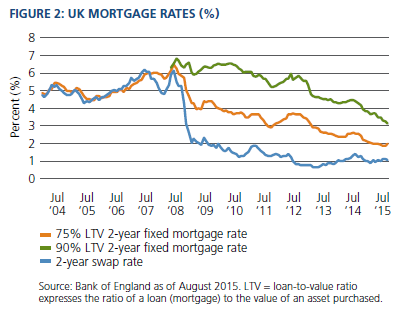

To answer this question, it is useful to put the current UK recovery into perspective. While the Bank of England (BOE) has left monetary policy unchanged for the last three years, private sector interest rates have continued to fall. This can be most clearly seen in domestic mortgage rates, which have fallen by 1.75% to 1.9% on the most commonly sourced two-year, fixed-rate loan with a value of 75% of the underlying property. Higher loan-to-value (LTV) mortgage rates have fallen by even more, from 5.9% down to 3.1% (according to the BOE, 30 September 2015). This fall in mortgage rates has not been as a result of lower wholesale interest rates, but rather due to the recapitalisation of the banking industry and banks’ increasing willingness to provide mortgage financing to new home buyers (see Figure 2). Alongside the benefits of a more resilient banking system, banks’ recapitalisation is providing a real and quantifiable benefit to the broader economy.

A note of caution

Given this improvement in financing conditions for households, UK consumer confidence has been rising steadily to a 15-year high and housing activity is improving, as are house prices. This favourable backdrop for the consumer has certainly played its part in the broader UK recovery, but it would be unfair not to note the contribution from higher investment spending. As consumers have gained confidence, UK businesses have felt more able to expand, such that – alongside the well-publicised rise in employment – investment spending has also played its part. Indeed, if we look at UK growth since the start of 2013, the average growth in GDP of 2.7% can be more than explained by household consumption, which has averaged 2.6% annually, and investment spending, which has averaged 6.6% (these two sectors make up almost 80% of GDP). Indeed, there are also signs that labour productivity may finally be starting to pick up, with average hourly output rising by an annual 1.3% over the last 12 months; however, the picture since 2013 remains a little more mixed, with average annual growth of just 0.2%.

Among all this good news, what are the risks to this domestically led UK recovery? And how much will this influence the actions of the BOE’s Monetary Policy Committee (MPC)? The first point to note is that, with house prices rising annually at 5%–7% and average earnings growth running at 3% a year, there is clearly a risk that the UK housing market ultimately proves destabilising for the broader economy. At present, house prices represent 5.26 times the average of household incomes, which remain some way above the 10-year average of 4.9 times average earnings, although below the 2007 peak of 5.86 (according to data from Lloyds/HBOS). Also, there appears to be an increase in the more speculative element of the UK housing market, as the Financial Policy Committee noted in its 25 September 2015 press release. Since 2008, the number of buy-to-let mortgages has risen by 40%, compared to a rise of 2% in owner-occupied mortgages, such that buy-to-let mortgages now constitute 16% of the total book of outstanding mortgages (according to the BOE, 25 September 2015), up from 12% in 2008. That is the bad news. The good news is that 2014’s tightening of mortgage lending criteria and stress tests on new mortgages would suggest less vulnerability to forced selling in the event of a market downturn; but clearly, this bears monitoring.

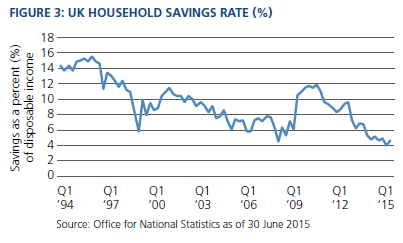

In a similar vein, household consumption has been steadily outpacing household income, as is most clearly seen in the household savings rate, defined as the proportion of household income that is saved (see Figure 3). Here again, the data suggest a note of caution to the UK outlook. At present, the proportion of household income that is saved is just 4.7%, a level which is in line with previous cyclical lows. This further reinforces the need for the nascent recovery in productivity to gain traction, which would in turn facilitate higher wages for UK workers. As with the productivity data, recent wage data from the Office of National Statistics (as of 30 September 2015) do suggest some upward drift in average earnings, which, excluding the more volatile bonus-payment component, has risen at 2.9% over the last 12 months, its highest level in five years. However, it is clear that for the UK recovery to be sustainable over the medium term, further progress on productivity and wages will be needed.

Sharper focus

So what does this mean for monetary policy given BOE Governor Mark Carney’s July 2015 comments that the decision on when to raise official interest rates would “come into sharper focus” around the turn of the year? As we rapidly approach the end of 2015, the prospects for an interest rate hike look fairly low. At present, it is not clear that the UK consumer would be able to withstand a monetary tightening cycle, and with inflation still stuck around zero, there seems little urgency to raise interest rates.

That said, as we move through 2016, assuming the U.S. Federal Reserve successfully navigates a rise in the federal funds rate, the decision may well “come into sharper focus.” Recall the MPC has a target of achieving 2% inflation over the medium term, typically regarded as in two to three years’ time. Part of the recent low level of headline inflation relates to low import prices, notably food and energy, which should fall out of the annual comparison in early 2016. Thereafter, PIMCO forecasts the UK Consumer Price Index (CPI) will likely rise gently to 1.5% by this time next year, while UK growth continues at an above-trend 2.25% to 2.75% level. With the unemployment rate already at 5.5%, employment growth slowing and vacancies still very close to the highs, it seems likely that we are getting closer to full employment, and so wage growth will improve further. This in turn, we believe, will put upward pressure on domestically generated inflation (more from higher demand than higher unit labour costs, assuming the nascent improvement in productivity continues).

So if the decision on monetary policy will be under the microscope by mid-2016, what does this mean for investors? At the time of writing, pricing at the front end of the yield curve means that the market expects the first rate hike to come in the fourth quarter of 2016, and that the total UK rate cycle will likely see the MPC hike from 0.50% to 1.75% by the end of 2018. Given our expectations for the monetary tightening cycle to start in mid-2016 and our New Neutral forecast for the BOE’s rate to settle at 2% or slightly higher, front end valuations look a little rich.

Similarly, the persistent long-end demand for UK defined benefit pension funds suggests long-dated bonds at 2.5% offer little yield protection in the event of a domestic rate hiking cycle. Where investors can, we would suggest they seek the greater income in the corporate bond market in the knowledge that, even when the BOE tightening cycle comes, the pace of rate hiking will be slow and the economy will be allowed to continue to perform. Indeed, a cumulative hiking cycle of around 150 basis points (bps) is very consistent with prior BOE hiking cycles, which have ranged from 100 bps to 175 bps.

Whichever way you look at it, this looks like a very British-type of recovery.