In February, we reported on the situation in Greece.1 Over the past few months, there has been no resolution to Greece’s debt problem, despite numerous deadlines and meetings. In our earlier report, we framed the conflict between Greece and the EU in terms of game theory.

In this report, we will begin by recapping our earlier analysis. Using this framework, we will discuss how a third option has evolved which will likely force PM Tsipras to acquiesce to the EU. As always, we will conclude with potential market ramifications.

The Game of Chicken2

The classic game of chicken holds that the most likely outcome for both parties is to concede to the other, usually simultaneously. Any one participant does better by maintaining the course, but if both do so, the outcome is catastrophic.

|

VEER |

HOLD |

|

|

VEER |

-5,-5 |

-5,+10 |

|

HOLD |

+10,-5 |

-100,-100 |

If both veer, both suffer some loss of face. If one veers and the other doesn’t, the holding player wins. If both hold, they suffer severe damage.

This game assumes that the losses are symmetric. During the Cold War, the nuclear standoff evolved into a situation of mutually assured destruction, or MAD. The MAD concept assumes a game of chicken, in which Veer becomes No Attack and Hold becomes Attack. If both attack, the world ends. If the losses become asymmetric, one of the players may perceive that his relative loss may be less than catastrophic and may reconsider his hold position. That is why, in MAD, treaties were put in place to prevent the creation of missile defense systems for fear it would make one of the parties believe that their losses in an Attack/Attack outcome would be survivable and thus encourage war. As long as both parties believe that complete destruction is the most likely result, neither would attack. In effect, if both players can create practices that minimize the costs of “loss of face,” a chicken game can be repeated.

Greece, the EU/Germany/ECB and Chicken

We believe that Greece and the Eurozone are effectively engaged in a game of chicken. However, Alexis Tsipras and his Syriza Party have concluded that the payoffs are more favorable to Greece than those of his predecessors, and so he is willing to risk a financial crisis to get the troika to Veer. The establishment is equally worried that Tsipras has underestimated the dire straits his nation is in and is at risk of triggering a crisis that may lead to Greece’s exit from the Eurozone.

Syriza’s Positions:

- The Tsipras government believes that the German economy is so dependent upon the Eurozone for its export-driven economy that it cannot risk anything that would lead to a breakup of the single-currency bloc.

- It also believes that the exit of Greece from the Eurozone would set off the exodus of other nations and bring into question the entire European unification project that began in the 1950s. A breakdown of this order would trigger fears that Europe is heading into a period of rising nationalism, which was responsible for two world wars in the last century.

- Syriza believes that an ECB cutoff of liquidity to Greece’s banking system would trigger bank runs in the periphery nations and trigger a broad banking crisis in the Eurozone. The inability to contain bank runs may have led Chancellor Merkel to bail out Greece in 2012.

- It also believes that the ECB will not take steps which would force Greece out of the Eurozone. To have a non-elected central bank essentially make a major political decision of this magnitude would undermine the concept of a democratic Europe.

EU/Germany/ECB Positions:

- The EU leadership has concluded that Greece could exit and contagion would be limited. Thus far, while Greek sovereign yields have increased with Syriza’s election, the yields of other periphery nations have not. This was not the case in 2012.

- Germany especially fears that its vision of reform (called austerity elsewhere) would be irreparably harmed if Greece were to receive significant debt relief. The mainstream parties that have embraced reform, like those in Spain, would be seriously hurt if Syriza were successful. Simply put, if Merkel doesn’t stop Syriza, the German view of reform will be undermined throughout the Eurozone.

What Has Changed?

In our earlier report, we concluded that both sides were overestimating the strength of their positions and underestimating the powers of the other. The Syriza coalition had a democratic mandate from its voters. The Greek government was running a primary fiscal surplus and if it defaulted, it would use that surplus to fund its economy. If the Greeks left the Eurozone and prospered, it would become very difficult for other struggling nations to stay with the single currency.

Such an outcome would be a nightmare for Germany and the EU establishment. If the periphery nations began to exit the Eurozone, the euro would likely strengthen to excessive levels, leaving German exports uncompetitive. At the same time, without the Eurozone, Germany could lose its free trade access to these countries, meaning they could erect trade barriers and prevent Germany from exporting to them. Likewise, by returning to their legacy currencies, the exiting nations could engineer a major currency depreciation that would undermine the competitiveness of German exports.

PM Tsipras and his finance minister, Yanis Varoufakis, thought they had a winning situation. The EU would either give Greece unlimited debt relief or face the prospect that the country would leave the Eurozone and unwind the EU.

On the other hand, the EU leadership noted that public opinion polls had consistently shown that Greek citizens not only wanted an end to austerity, which was reflected in the Syriza victory, but also had no interest in giving up the single currency. For Greeks, the euro represented currency stability and low inflation, which was absent under the drachma. No one knows for sure which desire is dominant; in other words, will Greek voters live with austerity to keep the euro or bid farewell to the single currency to escape austerity?

However, PM Tsipras misplayed his position. First, when it became apparent that Syriza was going to win the election, there was a sharp decline in tax compliance. Government revenues began to fall rapidly. Second, the new government decided to increase spending as part of the anti-austerity promises made during the campaign. Rapidly, the estimated primary surplus that may have been as high as 4% of GDP rapidly became a deficit of 1% of GDP.

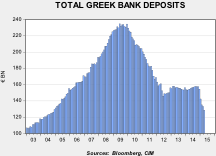

Whether it was by luck or foresight, the EU has found itself with a third outcome. With the primary surplus squandered, Syriza no longer has the funds to pay for its proposed anti-austerity measures even if it defaults on its external ones. To function within the Eurozone, Tsipras would be forced to implement austerity himself. If he leaves the Eurozone, the government could print drachmas but, as the aforementioned polling suggests, that would not be a popular outcome. Older Greeks have memories of holding a weak currency. This concern is reflected in Greek bank deposits.

As the chart indicates, deposit outflows have increased; even though Syriza won elections in late January, deposits in that month fell by over €12 bn from December, and through March, the latest official data available, deposits are down nearly €26 bn since the beginning of the year. Perhaps even more unsettling is that retail deposits, which represented 80.5% of total deposits in July 2007, just before the first inkling of the Great Financial Crisis, now represent 89.2% of the total and are up from 86.3% since September 2014. It would appear that there has been a steady drain of commercial deposits from Greece since the financial crisis, meaning that if capital controls are implemented, they will hurt households as the wealthy and well-connected have probably already moved their money out of Greece.

If, on the other hand, Tsipras tries to create a new Greek economy by defaulting and reverting back to the drachma, EU regulations would force him to exit not just the Eurozone but the EU as well. This would create chaotic financial and fiscal situations for Greece.

Now, as long as the EU keeps Greece in the Eurozone then the Tsipras administration will find itself forced to either exit the Eurozone or apply the austerity it promised to end. Not only would such an outcome send a clear signal to other Eurozone nations that exiting was foolhardy, it would also indicate that radical, nationalist, anti-establishment and anti-austerity parties cannot deliver on their promises.

The EU won’t force Greece to exit the Eurozone but it won’t offer anything to keep Syriza in power, either. The EU simply needs to keep negotiating without offering anything but strict compliance with what was already agreed upon, which is continued austerity in return for loans. In effect, to use a sports analogy, the EU just needs to “run out the clock.” In the end, it appears that Tsipras will either be forced out of office or forced to break up his coalition and form a new government with the mainstream parties, the outcome that EU and Germany have been angling for all along.

Greece’s Last Card

As PM Tsipras realizes his fate, we would expect him to make one last stab at leverage by cozying up to Russia. We would look for a flurry of meetings and Kremlin offers of support. This probably won’t matter very much as Russia really doesn’t have the financial means to offer Greece significant support. Still, a hostile Greece does complicate European geopolitics and could be a factor in negotiations. This is why the EU will likely offer significant support for an establishment government in Greece; in other words, once Syriza is out, Greece will receive more assistance.

Ramifications

The most critical concern about a Greek financial crisis is that it will likely trigger bank runs that extend into other parts of the Eurozone. Keeping Greece in the Eurozone and forcing Syriza out of power would certainly mitigate this risk. However, there is still a chance that Tsipras will conclude that a “suicide” strategy of taking Greece out of the EU and the Eurozone is a better alternative than continued austerity. Thus, there is still a chance that Greece triggers a broader financial crisis. However, at this juncture, it appears Syriza has misplayed its position and that the EU has the upper hand. Overall, we expect tensions to remain high but the EU establishment to win in the end. This means that European equities should remain supported. The euro may initially rally, but since the monetary policy of the ECB is designed to weaken the currency over time, we would expect any rallies in the euro from an establishment win to eventually subside.

Bill O’Grady

June 1, 2015

1 See WGR, 2/9/2015, Greek Games.

2 In the usual narrative, two participants drive their cars toward each other onto a single-lane bridge. If neither veers off at the entrance, both suffer certain destruction in a head-on collision. If one veers and the other doesn’t, that participant is “chicken.”

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

|

© Confluence Investment Management