China has founded an infrastructure bank, the Asian Infrastructure Investment Bank (AIIB), to compete with the World Bank (WB) and the Asian Development Bank (ADB). The U.S. has opposed the creation of this bank but, despite administration opposition, 57 nations have joined it, including 14 members of the G-20. A chorus of commentators have suggested that the founding of this bank may mark the end of U.S. hegemony.

In this report, we will describe the AIIB, including its members and capitalization. Next, we will cover the conventional wisdom surrounding the bank, and follow up with our analysis of the real impact of the bank. We will conclude with potential market ramifications of this framework.

The AIIB

In October 2013, China proposed a new infrastructure bank. Initially, with the exception of India, China was only able to attract small Asian nations. However, over U.S. objections, the U.K. Chancellor of the Exchequer, George Osborne, announced that his nation would join the AIIB. This announcement led to a plethora of developed nations signing on to the new bank. After Britain’s announcement, numerous other European countries announced their membership in the new bank. Perhaps the biggest snub to the U.S. was Israel’s decision to join the bank. Even Taiwan tried to become a charter member, but China rejected the application because the mainland views Taiwan as a province of China.

The AIIB will be capitalized at $100 bn, of which China will contribute $50 bn, making it smaller than the WB, capitalized at $223 bn, and the ADB, at $163 bn. Still, the ADB estimates that the region needs $8.0 trillion in infrastructure development, so the additional funds should be welcome.

The U.S. opposes the creation of the AIIB because it competes with existing development banks. The administration fears the new bank will lack proper controls to prevent corruption and protect the environment. China was frustrated with its small representation in Bretton Woods-era bodies like the IMF and the WB. China’s voting power at the former is a mere 6.068% and 4.42% at the latter. Given that China is the second largest economy on the planet, it feels it should have greater power in these organizations. This position led China to found the AIIB.

The Conventional Wisdom

According to the pundit class, the founding of the AIIB is “kind of a big deal.” 1 China believed that the U.S. had a stranglehold on the Bretton Woods-era institutions and was using them to project power. The U.S. has been considering reforms for the WB and IMF that would give China greater representation. However, no U.S. administration has actually pushed for these changes in Congress and there is a perception that the U.S. wanted to keep the preponderance of power among itself and its close allies, Japan and Western Europe. In effect, the lack of reform is a way for the U.S. to effectively contain China and prevent it from reaching its true potential. There is some truth to this allegation. The left in Congress loathes to give power to China and the right doesn’t really like multilateral institutions. Thus, legislation to make changes tends to fall low on any president’s priority list.

When China proposed the AIIB, the Obama administration leaned on developed nation allies to avoid joining the bank. The administration had been reasonably successful at this effort until Britain decided to break ranks.

The British decision to join the AIIB was driven by the hope that London will be a major clearing market for the Chinese yuan (CNY) once that currency becomes freely convertible. The U.K. was worried that if it stayed out of the AIIB then other financial centers might win out. Once the U.K. made its decision, several other European nations moved to join as well, worried they would miss out on whatever benefits might accrue.

The British decision opened the floodgates of membership. In fact, according to reports, even the Chinese were stunned by the scramble to become members.2 Conspicuous in their absence, only Japan and the U.S. have declined to join.

There is no doubt the Obama administration handled the AIIB situation poorly. Its ham-fisted response to China’s decision to create the bank has turned into a major diplomatic embarrassment. To have major allies like Germany, Britain, Australia and South Korea join over American objections makes the U.S. look weak. Although we don’t usually engage in “oughts,” it would have been much simpler for the U.S. to join the bank. If the administration was really concerned about oversight, it will have more by being a member than not being a member.

The huge response to the AIIB has led to a number of commentators projecting that this event may mark the beginning of China’s ascendency and America’s decline. Some have speculated that this bank will dramatically expand China’s influence in Asia as it uses its growing financial clout to tie the region more closely to its economy.

The Reality

These projections are probably overblown. As Ho-Fung Hung noted recently in the New York Times,3 the AIIB actually represents a retreat of sorts. China has tended to avoid multilateral agreements in favor of bilateral arrangements. In one-on-one situations, given China’s size, it can more easily dominate the relationship. However, over the past few years, China has managed to botch many of these situations. From 2001to 2011, the RAND Corporation estimated that China had lent $671 bn to developing nations, an amount that dwarfs the capital of the AIIB. However, China put conditions on this lending that forced nations to use Chinese contractors and products. These stipulations have led to deep resentment in many nations, mostly notably in Africa. For example, in Zambia’s 2011 election, voters elected a candidate on an anti-China platform. Lamido Sanusi, the former governor of the Central Bank of Nigeria, suggested that China’s activities in Africa were merely a “new form of imperialism.” Africa isn’t the only region to take umbrage with China. Myanmar has tried to improve relations with the U.S. to overcome its dependence on Chinese investment. It also suspended Chinese-funded dam projects in the country due to local opposition.

In addition to these problems, China’s aggressive actions taken in its coastal waters have further damaged its reputation. Activities such as putting an oil rig in disputed waters around Vietnam, creating islands in the South China Sea to expand its reach, and the nearly constant incursions into Japan’s airspace have raised serious concerns about China’s belligerence. Tensions have increased to the point where former U.S. adversaries, like Vietnam, are welcoming U.S. Navy visits to its harbors.

Ho-Fung argues that the creation of the AIIB is really a form of retreat. The backlash that China is experiencing in its foreign investment and regional security policy is driving it toward the use of soft power. Soft power, using culture, trade and aid to improve a nation’s standing and help in projecting power through cooperation, is partly why the U.S. established the IMF and the WB in the first place. Japan’s establishment of the ADB in the mid-1960s was done for similar reasons. China likely intends to use the AIIB to promote itself less aggressively. It is always important to remember that bilateral or unilateral arrangements are more efficient and, at least in the short run, more effective. The decision to move in a multilateral direction is giving ground to a less efficient foreign policy.4

The other major misunderstanding that the AIIB has created is in terms of the reserve currency issue. Mostly this is because of a general lack of understanding about how the reserve currency works. Essentially, if a nation wants to provide the reserve currency, it must be willing to provide the following:

- The reserve currency nation must have a nearly completely open capital account. In other words, this nation must allow nearly all countries the ability to purchase financial and other assets with little restriction. This is because, if nations are going to hold the reserve currency as a form of ultimate savings, they must have the ability to hold those savings in the financial assets of the reserve currency nation.

- As a consequence of an open capital account, the reserve currency nation must generally support free trade. If nations are going to use the reserve currency, they must have access to it, and the most efficient way to accomplish this is by running trade surpluses with the reserve currency nation. In effect, the reserve currency nation becomes the global importer of last resort and the locomotive of global growth.

In providing the reserve currency, the reserve currency nation must be willing to have an economy skewed toward consumption, see its domestic industries face burdensome foreign competition that will persistently threaten unemployment, especially for lower skilled workers, and have a very large financial services industry to manage that open capital account. These accommodations will have economic and political consequences for the reserve currency nation.

Although having a large economy is helpful in providing this role, having the largest economy in the world doesn’t necessarily lead to that nation being the reserve currency nation.

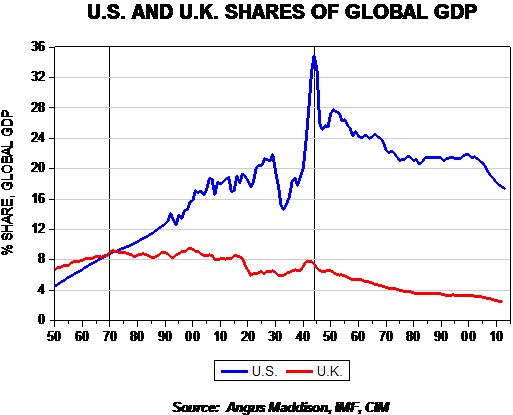

This chart shows the relative share of GDP for the U.S. and the U.K. from 1850 to the present. We have drawn two vertical lines on the chart, one at 1870, when the U.S. economy became the world’s largest, and one at 1944, when the dollar became the reserve currency at the Bretton Woods conference. Despite the fact that the U.S. economy was the largest in the world from 1870, it took nearly 75 years before the U.S. accepted the role as superpower, including the provision of the reserve currency. We believe China may become the world’s largest economy at some point in the future. However, that does not mean the CNY will become the reserve currency unless China is willing to accept a fully open capital account and allow for persistent trade deficits. There is little evidence that China is prepared to take that step.

Ramifications

In terms of market effects, China’s founding of the AIIB won’t have much impact. The world is awash in liquidity; if it wasn’t, we wouldn’t be seeing negative nominal yields in so many places. The lack of investment in Asian infrastructure isn’t because there isn’t money to borrow; it’s because the credits are dodgy. We seriously doubt the AIIB will have any special ability to get these less than creditworthy nations and projects to suddenly become better credits. Simply put, the reason these projects are not getting funded isn’t because the ADB or WB don’t have the cash, it’s because these projects are risky.

The most important ramification from the AIIB is how the Obama administration “scored an own goal” in its aggressive opposition to the bank. Instead of simply letting China start its bank and dealing with the issues that come from it, U.S. actions confirmed Chinese suspicions that America really just wants to contain and isolate China. While that is likely the U.S. policy, unveiling it over this project shows a serious lack of perspective on the administration’s part. To some extent, situations like this happen in second terms. The “first string” has usually moved on by this stage of the second term and less experienced hands are in charge. This condition isn’t unique to the Obama administration; after all, Reagan had Iran-Contra and Clinton had the Lewinsky scandal, both during their second terms.

Perhaps the best way to think about these multilateral organizations is in terms of cause and effect. Analysts who believe the AIIB is a watershed event seem to be thinking that the U.S. formations of the IMF, U.N. and WB were the causes of American hegemony. In fact, they were effects. The U.S. decision to adopt the superpower role came first; these multinational organizations were a way of promoting soft power, but were not the reason the U.S. became a hegemon. Instead, they were a consequence of American power.

Fortunately, the administration can recover from this mistake. It can ignore the AIIB and let it struggle to get started. It appears that a political deal for “fast-track” trade approval may be in place that will facilitate the Trans-Pacific Partnership, which is a keystone of the president’s trade policy.

So, in conclusion, we don’t expect the AIIB to amount to much, the mistakes the administration has made in its policy toward it are not fatal and getting the TPP passed will become the focus of events in terms of Asia. In terms of markets, the AIIB won’t make China significantly stronger or threaten the dollar’s reserve currency status. Although the media firestorm has been furious, in a few months, it likely won’t matter much.

1 With all due respect to Ron Burgundy.

2 Perlez, J. (2015, April 2). Stampede to Join China’s Development Bank Stuns Even its Founder. New York Times.

3 Hung, H. (2015, April 5). China Steps Back. New York Times.

4 It is important to remember that one of the policy changes implemented by the George W. Bush administration was the decision to avoid many of the multilateral organizations (IMF, UN) that the U.S. had created after WWII. This move infuriated a large number of nations, both allies and others, who feared that the decision to avoid these organizations reduced their influence on American policy. In fact, that was the point; the Bush government concluded that going through these organizations limited American power, which it did. However, by not using these organizations, the Bush administration discovered over time that it was difficult to gain support and assistance when it needed it, e.g., when the U.S. could have used help in quelling the Iraqi insurgency. At the same time, these multilateral organizations are slow to make decisions and require nearly constant diplomacy to accomplish anything.

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication

© Confluence Investment Management