- In light of the generally buoyant economy, we may start to see more normal conditions returning to the UK labour market and, importantly, upward movement in wage growth over the cyclical horizon.

- In turn, these developments are critical for the conduct and timing of monetary policy and the behaviour of the Bank of England’s (BOE) Monetary Policy Committee.

- We believe investors may want to treat the BOE’s interest rate cycle with caution in shorter-maturity bonds, while valuations offer more protection in intermediate bonds given PIMCO’s New Neutral thesis of secularly low real interest rates.

Over recent months, a combination of geopolitics, weak inflation and most recently the Scottish referendum have all raised genuine questions over when, and by how much, UK interest rates will rise. In particular, very benign wage growth, below-target inflation and questions over the economic outlook for the eurozone have pushed expectations of the start of the UK hiking cycle to Q2 2015. In the knowledge that the UK will not be going through a challenging period of separation from Scotland, and while issues remain in the Middle East and Ukraine, this appears a good time to take stock and revisit the underlying performance of the economy and in turn the outlook for interest rates.

Before turning to the economic outlook for the UK, it is worth noting that one of the most interesting aspects of the market is the implied pricing of the Bank of England’s (BOE) first rate hike by Q2 2015, which to my mind is the least likely date for the start of any monetary cycle. This in large part relates to the cycle of meetings of the BOE’s Monetary Policy Committee (MPC), and their coincidence with the May 2015 general election. It seems highly likely that, when the MPC do get round to the first hike, BOE Governor Mark Carney will want to explain the MPC’s thinking in some detail. After all, the last UK rate hike was in July 2007, some seven years ago. Not a single current member of the MPC has raised interest rates in the UK. That suggests that the first rate hike will come alongside the quarterly forecasting round at the BOE, which results in the publication of the quarterly inflation report and accompanying press conference. The quarterly cycle runs in February, May, August and November each year. Thus the timing is such that the May decision and inflation report will be within days of the 2015 general election.

While we fully accept the MPC rhetoric that the political cycle will not weigh on its decisions, we think it is hard for the MPC to say anything else and equally hard to actually make the first move at such a politically charged moment. That brings us back to the question: Will the recovery be sufficiently well-entrenched to allow the MPC to start the hiking cycle ahead of the general election, or will we find that MPC guidance persistently indicates that rates are going up, but not yet?

Staying the courseA look at the underlying dynamics indicates the economy retains good momentum. GDP data has exhibited more volatility than the monthly purchasing manager index (PMI) over the last decade (see Figure 1), and there is a long-standing debate about which provides the higher-quality real-time information on the state of the economy. However, the striking aspect of these series is how they both have been strong for the last two years, and there is little in these series to suggest an imminent slowdown in activity. Most recently, some of the forward‒looking components, such as the new orders series, have come off their peak ‒ but levels remain strong. In short, the domestic tailwinds to growth appear to remain.

We can also see that the economy is holding up well by looking at a range of other business surveys, where investment intentions remain strong, as do the all-important surveys of employment intentions. Employment growth has been remarkably strong in this recovery (see Figure 2), currently running at levels not seen since the late 1980s.

While this all speaks to economic momentum being maintained, it does not answer the key question of why wage growth has remained so weak, and whether it will remain so. Given that inflation appears stable at 1.5%, as long as wages remain so weak, there will be little appetite for the MPC to raise interest rates (indeed, there would be no good reason to hike rates).

About that raise …To answer the puzzle of low wage growth, we should look at not just the rate of improvement in the demand for labour, but also the level of demand relative to the level of supply. Indeed, if the level of supply still overwhelms the absolute amount of demand, it would be no great surprise that wage growth is so weak, particularly with the dark days of 2008 and 2009 so fresh in many people’s minds.

This indeed does appear to provide one potential answer to the puzzle of weak wage growth. Job centre vacancies in the UK have been rising strongly since mid-2012, rising from 450,000 to 650,000 at the most recent reading in July this year. These levels of vacancies are very similar to the average level of vacancies in the 10 years prior to the collapse of Lehman Brothers in 2008 (the average number of vacancies was 610,000). However, the number of unemployed is still materially higher than the decade prior to the collapse of Lehman Brothers, with a current number of 2.02 million compared with an average of 1.575 million in the decade prior to September 2008, according to the Office for National Statistics. So, putting the demand for labour in the context of the supply of labour, it should not be a big surprise that wage growth is weak. At present, average hourly earnings are growing at 0.6%, compared with the 4%–5% prior to September 2008.

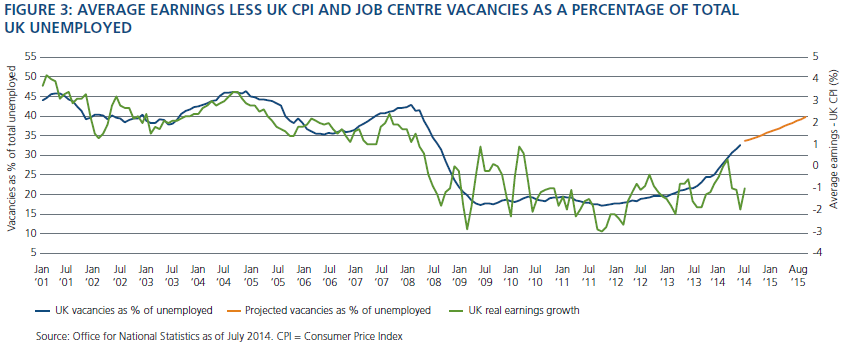

That raises the obvious question: How long will it take the UK to use up that spare labour market capacity, and in turn see wages start to rise? While there are many caveats to any forecast, there are ways in which we can start to answer this question. One way is to look at the ratio of job centre vacancies to the total number of unemployed, and see how that compares to real wage growth (defined as average hourly earnings less CPI). Looking at Figure 3, the ratio of vacancies-to-unemployment remains below even the cyclical lows prior to the financial crisis, and in turn real wages are very weak. However, looking forward, if we were to assume that vacancies remain unchanged but that the unemployment rate continues to fall by 0.75% per annum, we could get an estimate as to how quickly the economy will reach the point of traction in wage growth.

Given current economic momentum, this is a pretty conservative set of assumptions for unemployment, which has fallen by 1.5% in the last 12 months. Under these assumptions, we should start to see upwards momentum in wage growth over the next six months.

Looking at market timing in a little more detail, the above projections suggest that the October 2014 data set will show vacancies as a percentage of the unemployed reaching the prior cycle lows, when we should start to see more normal conditions returning to the labour market. We believe that it is unlikely that real wage growth will return to 2% above inflation in the next 12 months, given the other factors pressing down on wages such as tighter controls on benefits, increasing numbers of over-65-year-olds remaining in the labour market and immigration.

However, we should be able to see real wages finally get back towards a positive number after six years of real wage contraction. This is critical for the conduct of monetary policy and the behaviour of the MPC. As the MPC members have been keen to make everyone aware, monetary policy works with a lag. Thus, they need not wait to see the actual rise in wages, but just to be confident that the rise in wages is coming, and that it will more than offset any productivity improvements. If that is the case, we should still expect to see the first rate hike this side of the general election, with the February 2015 MPC meeting and inflation report the most likely period.

Are we there yet?If that is the case, then shorter-dated UK bonds will be vulnerable over the next six months, and are likely to be the focal point for any market weakness. Further out on the curve, PIMCO’s New Neutral base rate of 2%–2.5% implicit in the structure of the gilt curve suggests fairer valuations.

The UK remains a highly levered economy sensitive to changes in asset prices, especially housing. As such, treat the interest cycle with caution in shorter-maturity bonds, but remember the economic healing has a long way to go. That will temper this rate cycle (and probably the one after that).

© PIMCO

© PIMCO