- The UK remains in a “stable disequilibrium”, one that needs to either transform into growing economy with narrowing income differentials or risk a more aggressive policy response.

- Financial repression, protection of real purchasing power, tail risks of accelerated currency weakness and price sensitivity will likely dominate UK markets over the secular horizon.

- Investors may consider progressively reducing exposure to assets susceptible to tail risks. Higher quality short-dated income-generating, inflation-hedging and non-sterling assets remain attractive.

Each May, PIMCO professionals gather for three days in our Newport Beach office to assess the three- to five-year secular outlook for global markets. As Mohamed A. El-Erian has written in the

2013 Secular Outlook, “

New Normal … Morphing”, amongst the key questions addressed this year was whether the global economy would exhibit signs of genuine, inclusive and sustainable growth or continue to exhibit multi-speed characteristics, with the various economic regions continuing to focus on domestic agendas.

Our core conclusion is that the world economic outlook has morphed to include “stable disequilibrium” dynamics that depend significantly on growth. Over the next three to five years, we believe the greater likelihood is that growth will remain dependent on central bank assistance, asset prices could risk outrunning economic reality, growth differentials will remain and possible “T-junctions” await key economies.

How is the UK positioned within this world outlook?

Many of the themes we identified globally resonate strongly with the UK: Disappointing growth, in turn reliant upon central bank activism; persistent income inequality; dysfunctional politics and the challenge of unlocking better (corporate) balance sheets. Indeed, at the broad level, the concept of a stable disequilibrium describes the current UK economy well: Employment levels are high, but real income growth remains negative; the export sector remains too focussed on Europe and thus unable to provide meaningful stimulus; and the government remains committed to the medium-term fiscal plan. Overall, growth remains flat to moderately positive, sufficient to maintain a degree of social tolerance for the necessary economic restructuring, albeit at a painfully slow pace.

In turn, this leads us to raise several critical questions: Can UK prospects improve meaningfully over the secular horizon and will voter tolerance continue? Will the UK risk its own T-junction? Will a new Bank of England (BoE) governor or the 2015 election introduce any unexpected twists and turns? And how do we, as investors, position for these risks and opportunities?

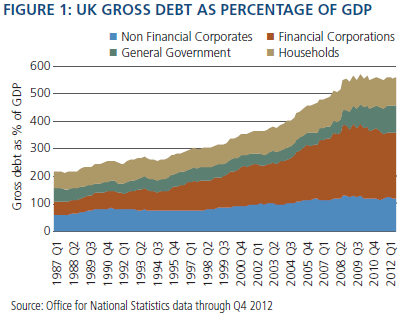

Taking the economy first, there have been a number of disappointments over recent years which in combination leave us a lot earlier in the necessary deleveraging process than many would have hoped. In aggregate, gross debt as a percentage of GDP is little changed as the marginal reduction in private sector leverage has been balanced by the expansion of the government balance sheet (see Figure 1). When we look at the economy as a whole, there looks to be much work left to do.

That said, the news is not unequivocally grim. The banking sector has shrunk based on the amount of loans outstanding while the capital ratios for major banks have improved materially. However, the UK banking industry is not as far through the balance sheet recovery process as the U.S. banking industry, and regulatory efforts remain heavily focussed on reining in aggressive risk-taking by UK banks. For the early part of the next three to five years, we expect commercial banks will remain a drag on growth as they further shrink their balance sheets. Yet, for the period as a whole, it is likely their capital raised and asset sales will be less than the previous three- to five-year period.

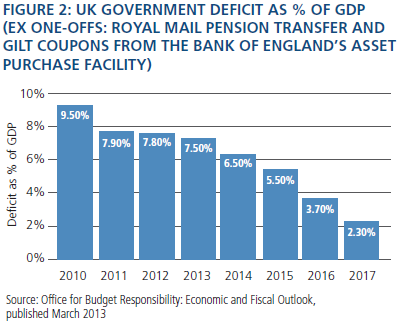

Sadly, the same cannot be said for the government sector, which (looking at the underlying deficit – see Figure 2) is still stubbornly high. The debate over how much of this is self-imposed (excessive austerity) rather than an unfortunate confluence of circumstance (high spot inflation, weak eurozone) will no doubt continue. Looking ahead, the most important aspect is that the government sector will likely remain a secular drag on growth.

This suggests that unlocking those corporate balance sheets may well prove elusive. Domestic demand will be hampered by weak real income growth and fiscal drag – hardly the backdrop for a rapid recovery in investment spending. This is particularly the case if the eurozone, the UK’s single largest trading partner with just under 50% of exports, remains a secularly weak growth area. Net exports have persistently disappointed since sterling’s fall in 2008 and 2009 and, as discussed in the March 2013 issue of

UK Perspectives, “

What happened to that export-led recovery?”, will be unlikely to provide a robust contribution to UK GDP for much of the secular horizon.

So how do policymakers react to this tepid growth environment? Three areas of interest immediately strike us:

Fiscal policy, voter fatigue and the rise of the protest party

The UK, like many eurozone countries, has seen the rapid rise of a new political party. However, unlike many of the other protest parties across Europe, the UK Independence Party (UKIP) has a clear focus: The UK leaving the European Union (EU). Already, this has elicited responses from the Conservative Party. It seems likely the disruptive new fourth party will remain a part of the political scene, but does it mean a UK exit is likely over the secular horizon? We doubt it, but it does serve as a useful reminder that, while the UK is likely to be mired in its own stable disequilibrium, there are potentially disruptive elements out there.

The politics of UKIP also have important implications for UK fiscal policy over the secular horizon. Not because UKIP has a strong stance on the austerity versus spending debate, but a possible split in the Conservative vote does raise the prospect of a change of government in two years. While there is much political rhetoric in the current debate between the ruling Conservative coalition and the opposition Labour Party, as Figure 2 amply demonstrates, any actual shift will likely be a reduction in the pace of austerity rather than a policy reversal and higher government spending (as is happening in Japan).

Monetary policy – further hyperactivity?

With fiscal policy likely to remain constrained, it appears highly likely that the onus of responsibility for growth will remain with the BoE. Somewhat conveniently, the three- to five-year secular horizon coincides with soon to be incumbent BoE Governor Mark Carney’s five-year term (he starts 1 July 2013). Should we expect a reinvigorated and augmented array of stimulus tools? Forward guidance linking the policy outlook with prospects for growth or (more likely) the labour market does seem likely. Similarly, we should expect further attempts to direct lending to the capital-constrained small- and medium-sized enterprises (SME) sector.

However, there are two potential elephants in the room: The scope for the BoE to buy private sector assets and the scope for sterling to fall further. Each remains plausible over the secular horizon, and we will be monitoring Governor Carney’s early exchanges for signals on timing. Either taking sterling down or conducting more quantitative easing (QE) would be easier to implement; these are the most likely initial forms of aggressive monetary policy (once the well-flagged forward guidance has been implemented). Given the stickiness of UK inflation, and its sensitivity to higher import prices, UK investors should stay alert to the risk of higher-than-expected inflation.

Investment implications

A world of weak growth, further monetary stimulus and weaker currency points to an economy unlikely to escape what Mohamed A. El-Erian has coined “assisted growth”. Look for asset prices to continue to front-run the real economy; investors should remain wary of buying risk assets purely on the premise of a “Carney put”. Financial repression, protection of real purchasing power and tail risks of accelerated currency weakness will likely dominate UK markets. Gradually reducing exposure to risk assets is likely to be a dominant secular theme – with risk defined by both duration and exposure to the lower parts of capital structures. Short-dated income-generating products backed by high quality collateral, non-sterling assets in markets offering positive real yields and, if you have to “stay local”, shorter-dated nominal and longer-dated inflation-linked products remain attractive.

Risk management should also continue to evolve to recognise the low probability, high impact events that may intermittently beset investment markets. In the last few years, the dominant risk for UK markets has been European problems within the eurozone; however, now that risk seems more balanced against risk from without in the form of a “Brexit”. This is certainly not our central expectation, but the fact that there is such disillusionment with the existing political arrangements is a reminder that the UK remains in a stable disequilibrium, one that in time needs to either transform into growing economy with narrowing income differentials or risk a more aggressive policy response. The latter would likely involve an explicit reversal of fiscal policy, a semi-open recognition that sterling needs to go lower and a much lower degree of policy control over the ultimate outcome. Over to you, Dr. Carney.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world. © 2013, PIMCO.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO