Modeling Cyclical Markets – Part 3

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In Part 1, I introduced my Primary-ID model that identifies major price movements in the stock market. In Part 2, I presented Secondary-ID, a complementary model that tracks minor price movements. In this article, I combine these two rules- and evidence-based models into a composite called Cycle-ID and discuss the virtue of a single model.

I examine the efficacy of Cycle-ID from three separate but related perspectives. The first area is the utility of the composite. What are the benefits of moving from a binary scale (bullish or bearish) of Primary-ID and Secondary-ID to a ternary scale (bullish, neutral or bearish) of Cycle-ID? The second topic is synergy. Can the composite perform better than the sum of the parts? Finally, how can we use Cycle-ID to custom-design strategies similar to those of risk-parity for the purpose of matching market return and risk? Do these more complex investment strategies add value?

Cycle-ID – a composite model for cyclical markets

All investors need to achieve a dual objective. The first is capital preservation by minimizing losses in market downturns. The second is wealth accumulation by maximizing market exposure during market upturns. Not losing money should always be the main investment focus but making money is why we invest in the first place. Investors often achieve one objective at the expense of the other. For instance, many so-called secular bears avoided the 2000 dot-com crash and/or the 2008 sub-prime meltdown, but missed the 2003-2007 and the 2009-2016 bull markets. My cyclical-market models are aimed at preserving capital during stormy seasons as well as accumulating wealth in equity-friendly climates.

The signal scores of both Primary-ID and Secondary-ID are binary: +1 is bullish and -1 is bearish. Cycle-ID is the sum of the two models and therefore its scores are +2, 0 and -2. What do the three Cycle-ID scores mean? A Cycle-ID score of +2 indicates that both primary and secondary price movements are positive. In other words, the stock market is in a rally phase (a positive Secondary-ID) within a cyclical bull market (a positive Primary-ID). A Cycle-ID score of -2 indicates that both the primary and secondary price movements are negative. Put simply, the stock market is in a retracement phase (a negative Secondary-ID) within a cyclical bear market (a negative Primary-ID). When Cycle-ID is at zero, the stock market is either in a correction phase (a negative Secondary-ID) within a cyclical bull market (a positive Primary-ID), or in a rally phase (a positive Secondary-ID) within a cyclical bear market (a negative Primary-ID). Since the two cycle models are in conflict, one would naturally assume that the market is neutral. However, there is a counterintuitive interpretation of the zero Cycle-ID score that I will present later.

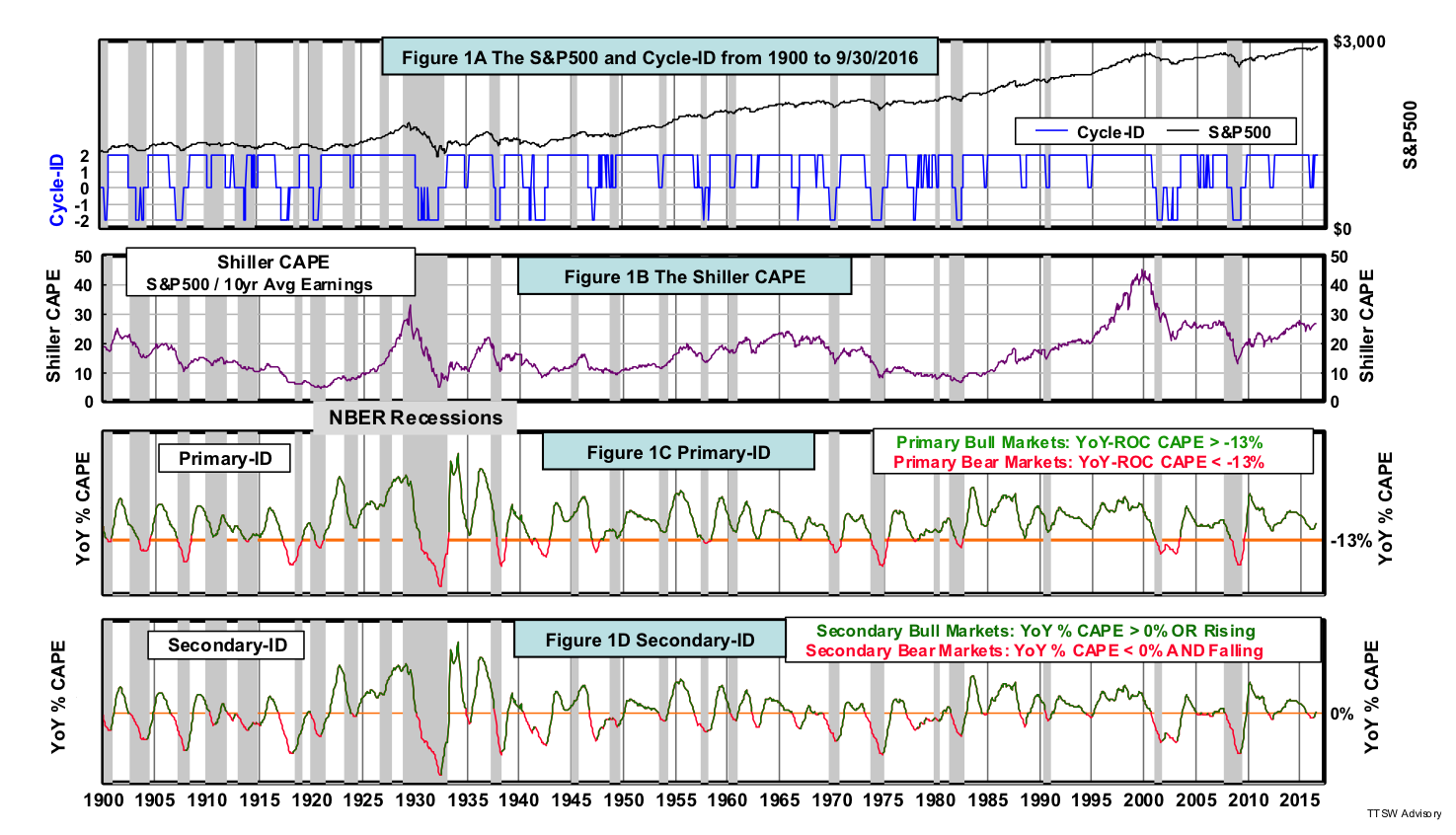

Figures 1A shows the monthly S&P 500 (in black) in logarithmic scale along with the Cycle-ID score (in blue) from 1900 to September 2016. Figure 1B is Robert Shiller's cyclically adjusted price-to-earnings ratio (CAPE) from which the vector-based indicators of Primary-ID and Secondary-ID are derived. Figure 1C is similar to Figure 5A in Part 1 and Figure 1D is the same chart as Figure 4D in Part 2 but updated to the end of September. All green segments in Figures 1C and 1D represent +1 scores and all red segments, -1. The blue Cycle-ID score in Figure 1A is the sum of the Primary-ID and Secondary-ID scores at either +2, 0 or -2.

Figures 1C and 1D show that green segments overwhelm red segments in both duration and quantity. History shows that corrections in cyclical bull markets are more prevalent than rallies in cyclical bear markets. Therefore a zero Cycle-ID score is not really neutral, but has a bullish bias. This subtle difference in the Cycle-ID score interpretation can make a huge impact on the investment outcomes over an extended time horizon.

For ease of visual inspection, the contents in Figures 1A to 1D are zoomed in for the period from 2000 to September 2016 as shown in Figures 2A to 2D, respectively. Cycle-ID score hit -2 several times during the protracted 2000-2003 dot-com meltdown. Cycle-ID also reached -2 in July 2008, months before the collapse of Lehman Brothers' and the global financial systems. During the bulk of the two cyclical bull markets from 2003 to 2007 and from 2009 to 2016, Cycle-ID was at +2 most of the time. During the last 16 years while market experts were engaging in worthless debates on whether we were in a secular bull or bear market, Cycle-ID identified all major and minor price movements objectively without any ambiguity. The rules-based clarity and the evidence-based credibility of Cycle-ID enabled investors and advisors to meet their dual objective – capital preservation in bad times and wealth accumulation in good times.

Let's examine the hypothetical performance statistics to see if Cycle-ID effectively met the dual objective in 116 years.

Cycle-ID performance stats

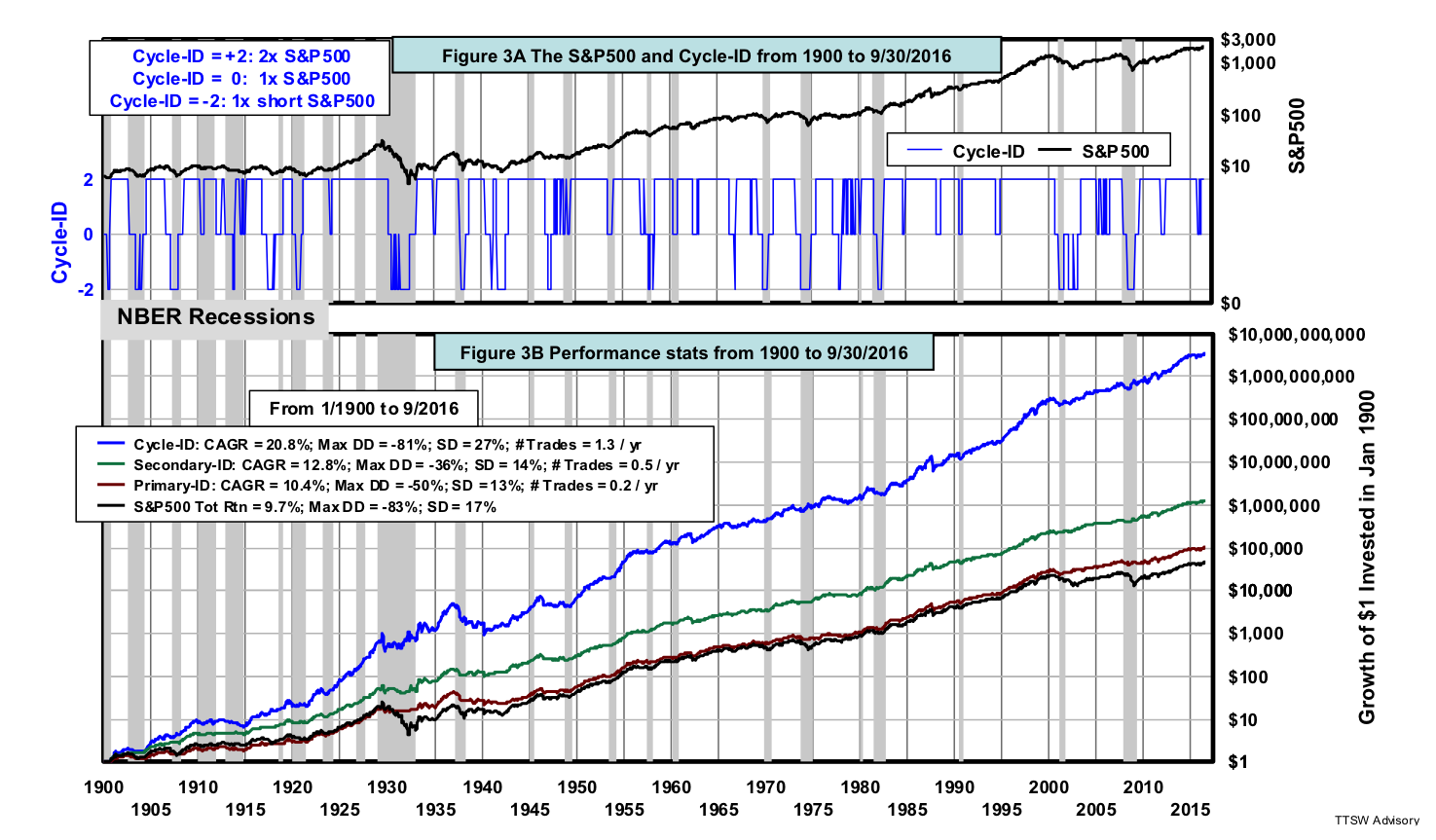

The ternary scale of Cycle-ID allows for many different combinations of investment strategies including the use of leverages and shorts. I intentionally selected a set of fairly aggressive strategies for the purpose of stress-testing Cycle-ID. This aggressive strategy set is used to demonstrate Cycle-ID's potential efficacy and is not an investment strategy recommendation.

The aggressive strategies are translated to execution rules as follows. When the Cycle-ID score is at +2 (the market is in a rally mode within a bull market), exit the previous position and buy an S&P 500 ETF with 2x leverage (e.g. SSO) at the close in the following month. When the score is at -2 (the market is in a retracement phase within a bear market), exit the previous position and buy an inversed unleveraged S&P 500 ETF (e.g. SH) at the close in the following month. When Cycle-ID is at zero, close the previous position (either leveraged long or unleveraged short) and buy an unleveraged long S&P 500 ETF (e.g. SPY) at the close in the following month. This mildly bullish interpretation of the zero score is based on the evidence that in over 100 years cyclical bull markets significantly outnumber their cyclical bear counterparts as shown in Figure 1C. Bull market corrections also outnumber bear market rallies as shown in Figures 1C and 1D. As a result, I consider a zero Cycle-ID rating a bullish call rather than a neutral market stance in the stress test.

Figure 3A is the same as Figure 1A with the aggressive set of strategies specified in blue on the upper left. Figure 3B shows that the cumulative return of Cycle-ID is 20.8% compounded over 116 years, far and above the compound annual growth rate (CAGR) of Secondary-ID at 12.8% and Primary-ID at 10.4%. The equity curves of Primary-ID and Secondary-ID are those presented in Parts 1 and 2, respectively. They are updated to the end of September and shown here as references. The S&P 500 compounded total return is at 9.4%, the performance benchmark for comparison.

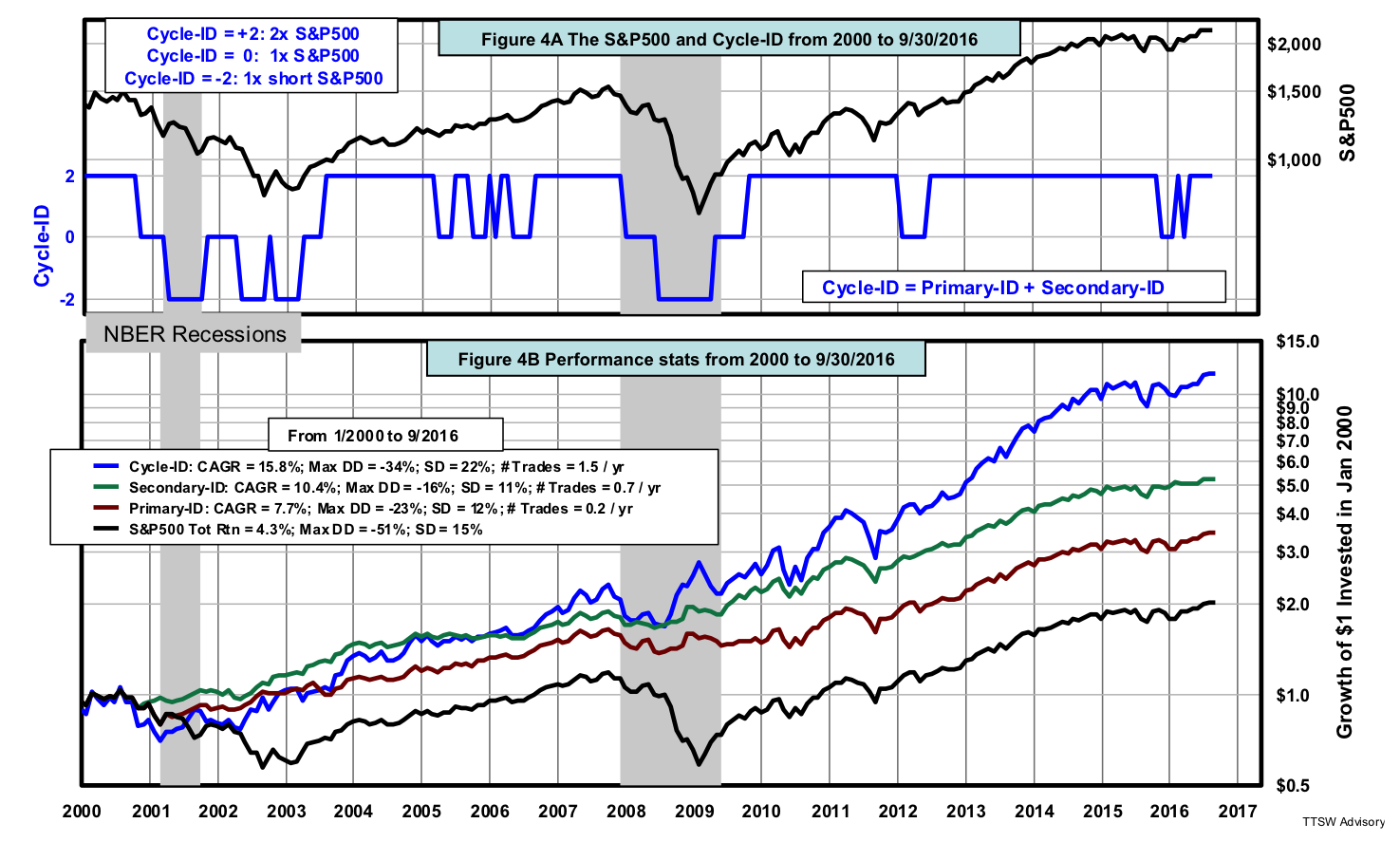

Figures 4A and 4B display contents similar to those shown in Figures 3A and 3B except the base year for the equity curves is changed from 1900 to 2000. Despite two drastically different timeframes, 116 years in Figure 3 and 16 years in Figure 4, the relative CAGR gaps between Cycle-ID and the S&P 500 total return are nearly identical, roughly 1100 bps in both periods. Risk characteristics are also similar in the two periods. Cycle-ID has a lower maximum drawdown, but shows a 1.5x higher volatility (annualized standard deviation) than that of the S&P 500. The consistency in both CAGR edge and risk gap suggests that Cycle-ID has had a relatively stable value-adding ability for over a century.

Simulating leveraged and inverse indices

I now digress to describe briefly the methodology for computing both the leveraged and the inverse-proxy indices used in the stress test presented above. The traditional ways for setting up such positions are by borrowing capital from a margin account and by selling borrowed equities. Leveraged and inverse ETF financial products did not exist in 1900 but are readily available today. To simulate a leveraged and an inverse time series from an underlying index, Marco Avellaneda and Stanley Zhang developed the appropriate formulae. Their algorithms can be used to compute the leveraged and inverse S&P 500 proxies as follows: A 2x leveraged S&P 500 index is computed by multiplying each month's ending value of the index by the quantity one plus twice the month-to-month percentage change of the S&P 500. An inversed S&P 500 index is computed by multiplying each month's ending value of the index by the quantity one minus the month-to-month percentage change of the S&P 500. In my back tests, both time series are assumed to be rebalanced monthly.

To check the accuracy of the Avellaneda and Zhang algorithms, I simulated two ETF proxies and compared them to the closing prices of two widely held ETFs: a 2x leveraged S&P 500 ETF (ticker: SSO) and an inversed S&P 500 ETF (ticker: SH). All time series are rebalanced daily. The results are shown in Figures 5A and 5B. The tracking errors averaged over 10 years are found to be 0.2% and 0.1%, respectively. These errors may be small, but they could diverge over a longer time period. On the other hand, the two divergences have run in opposite directions and the errors tend to cancel each other. Nevertheless, the algorithms appear adequate in testing Cycle-ID for illustration purposes.

Back to Cycle-ID, my intent is not to boast about the spectacular Cycle-ID CAGR of 20.8% shown in Figure 3B or to recommend a particular aggressive investment strategy. In fact, the high CAGR must be viewed with caution because both fund costs/fees and tracking error could potentially lower the hypothetical return. In addition, Figure 3B also shows that the higher hypothetical CAGR comes with higher risks. Cycle-ID has a maximum drawdown almost as high as that of the S&P 500 total return index and the annualized standard deviation (SD) is 1.6x higher than the market benchmark. Nevertheless, this simple exercise does underscore the alpha generating potential of Cycle-ID.

Return and risk tradeoffs

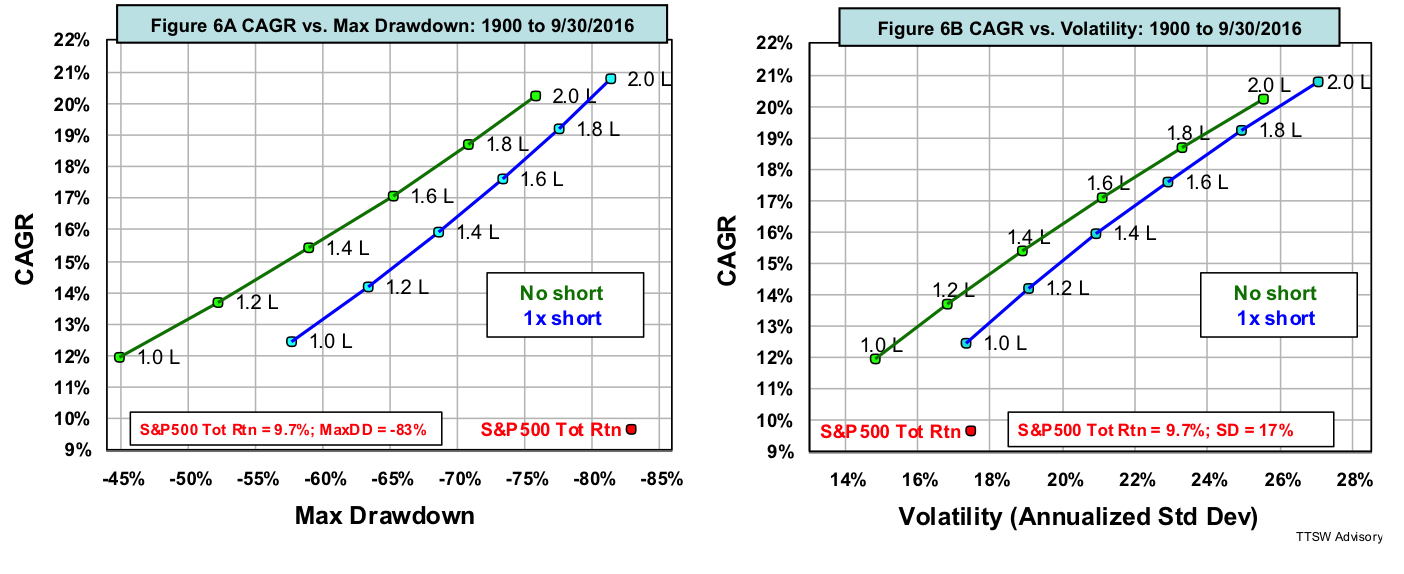

Besides the aggressive set of strategies of 2x long and 1x short, I also tested various combinations of leveraged and short positions. The best way to visualize absolute and risk-adjusted returns among different strategies is to plot CAGR against two risk measures –maximum drawdown (Figure 6A) and volatility (Figure 6B). In Figures 6A and 6B, the green curves represent long-only strategies (no shorts) with different leverage levels ranging from unleveraged (1.0 L) to 2x leveraged (2.0 L). The blue curves show the effects of adding a short strategy (1x short) into the mix while varying the degree of long leverage. The preferred corner is at the top-left showing the highest return with the lowest risk. The red dots represent the S&P 500, which is located far away from the preferred corner.

When short strategy is added (the blue lines), the rules are as follows. When Cycle-ID score is zero, exit the previous position and buy the S&P 500 (e.g. SPY) at next month's close. When Cycle-ID is at +2, exit previous position and buy the S&P 500 with various leverages (from 1.0 L to 2.0 L) at next month's close. When Cycle-ID is at -2, exit previous position and buy an inverse S&P 500 (e.g. SH) at next month's close.When no short is used (the green lines), the rules are as follows. When Cycle-ID score is zero, buy the unleveraged S&P 500 (e.g. SPY) at next month's close. When Cycle-ID is at +2, exit the previous position and buy the S&P 500 at various leverages (from 1.0 L to 2.0 L) at next month's close. When Cycle-ID score is -2, exit the previous position and buy the 10-year U.S. Treasury bond (e.g. TLT) at next month's close. The return while holding long positions is the total return with dividends reinvested. The return while holding the bond is the sum of both bond coupon and bond price changes caused by interest rate movements.

Several observations from Figures 6A and 6B are noteworthy. These characteristics are probably germane to leveraged long and short strategies in general and not specific to Cycle-ID.

- First, when no leverage and no shorts are used (the bottom-left green dots in Figures 6A and 6B), the performance of Cycle-ID is between that of Primary-ID and Secondary-ID. Hence, no synergy is expected when the performances of two models are averaged.

- Second, the blue curves are to the right of the green curves indicating that adding short strategies increases risk more than return. It's inherently more challenging to profit from short positions because down markets are brief and volatile.

- Third, the curves in Figure 6A are convex (higher marginal return with each added unit of drawdown) but the curves in Figure 6B are concave (lower marginal return with each added unit of volatility). The curvature disparity reflects the basic difference between these two types of risk. Volatility measures the uncertainty in the outcome of a bet. Maximum drawdown depicts the bloodiest outcome of a wrong bet.

- With Cycle-ID, one can tailor strategies to either match market risk or gain. For instance, if one can endure an S&P 500 drawdown of -83%, one can supercharge CAGR from 9.7% to over 21% by using the 2L/1S strategy shown in Figure 6A. If one can tolerate a 17% market volatility, one can boost CAGR to over 14% by using the 2L/0S strategy in Figure 6B. Conversely, if one just wants to earn a market return of 9.7%, by extrapolating the green lines in Figures 6A and 6B to intercept a horizontal line at 9.7%, one can reduce drawdown from -83% to below -30% or to calm volatility from 17% to less than 12%.

- A widely known approach for engineering a portfolio with either market-matching return or market-matching volatility is risk parity. It budgets allocation weights by the inverse variances of all the assets in a portfolio. Cycle-ID achieves the same mission by using a single index – the S&P 500. No risk budgeting algorithm is needed. Looking for a robust risk management tool in a chaotic, nonlinear and dynamic investment world, I would pick simplicity over complexity every-time.

Concluding remarks

My cyclical-market models are relevant to both Modern Portfolio Theory (MPT) and Efficient Market Hypothesis (EMH) – the two pillars in the temple of modern finance.

Harry Markowitz in 1952 introduced MPT – the use of mutual cancellations in the uncorrelated variance-covariance matrixes across asset classes to minimize portfolio risk. Jack Treynor was the first to note in 1962 that the risk premium (the spread between risky and risk-free returns) of a stock is proportional to the covariance between that stock and the overall market. William Sharpe in 1964 simplified Markowitz's complex matrixes into a single-index model – the Capital Asset Pricing Model (CAPM) that uses beta to represent stock or portfolio risk (price fluctuations relative to those of the market). The type of risk both MPT and CAPM focus on is volatility –uncertainties in the potential (expected) returns of one's bets. Neither MPT nor CAPM tackles the types of risk investors dread the most – temporary equity drawdowns and permanent capital losses from making the wrong bets. Volatility and beta are the types of risk financial theorists deliberate about in scholastic faculty lounges. Drawdowns and permanent losses are the types of risk that drain investors' wealth and prey on their emotions.

Furthermore, variance-covariance matrixes and betas calculated from historical data could lose their anti-correlation magic or regression line linearity when the next crisis hits. In 2008, for instance, the effectiveness in risk reduction by either EMH's diversification or CAPM's beta diminished when capital protection was needed the most. Most importantly, even when MPT and CAPM work, they can only diversify away specific risk. Both models offer no solution in managing systematic or systemic risk. Company specific risk is minuscule when compared to the risk from the overall stock market or from the collapse of the global financial systems. There were hardly any diversified portfolios that could shelter one's wealth during cyclical bear markets in the financial meltdowns in 1929 and 2008. MPT and CAPM are ill-equipped in mitigating these titanic financial shockwaves with tsunami-scale impacts that affect all asset classes around the globe.

Cycle-ID is a positive alternative to the traditional risk hedging concepts. First, Cycle-ID eliminates company-specific risks by investing only in a broad market index – the S&P 500. There's no need to optimize an "efficient portfolio" of asset classes and hope that their anti-correlation attributes would remain unchanged going forward. More importantly, Cycle-ID reduces both systematic (i.e., interest rate, inflation, currency or recession) and systemic risk (global financial systems, interlinked liquidity freeze, or geopolitical instability) by exposing one's capital only in fertile seasons with the appropriate market exposure levels. Market exposure level is objectively matched with the perennially changing market environment. This is accomplished by closely tracking the first and second derivative of the Shiller CAPE – the aggregate market appraisal by all market participants.

Both the traditional risk hedging approaches (i.e., MPT and CAPM) and Cycle-ID employ the long-standing wisdom of diversification to manage risks. The difference is that the traditional approaches diversify in assets with uncorrelated covariances to hedge against company-specific risk. My model diversifies in market exposure in harmony with the investment climate to achieve a dual investment goal: (1) to minimize systematic and systemic risks in bad times; and (2) to increase market exposure in good times. The Chinese character for risk has an insightful duality – one pictogram for danger and the other for opportunity. While risk can harm us when we are exposed to it, risk is also a driver for higher returns if we exploit it to our advantage.

Let's turn to the Efficient Market Hypothesis which was postulated by Eugene Fama in 1965. According to Richard Thaler, EMH has two separate but related theses. The first thesis is that the stock market is always right and the second, the market is difficult to beat in the long run. Behavioral economists argue that the market is not always right because its pricing mechanism does not always function perfectly. Humans are not always rational beings and financial bubbles are the proofs of market mispricing. Both traditional and behavioral economists, however, agree on the second thesis that the market is hard to beat in the long run. The market is hard to beat because it's quite efficient (discounting all known information that could affect market prices) most of the time. But the market is not totally efficient all the time. Market prices often diverge from the market's intrinsic values – an observation first articulated in 1938 by John Burr Williams before the inception of behavioral economics. Hence, it's difficult but not impossible to beat the S&P 500 in a long run.

Primary-ID, Secondary-ID, and Cycle-ID along with a handful of legendary investors and some previously published models of mine (Holy Grail, Super Macro, and TR-Osc) demonstrate that it's possible to outperform the S&P 500 total return. They do so not by predicting the future. Price prediction is futile because both the amplitude of impact and the frequency of occurrence of the various price drivers are totally random. So what are the secret ingredients for a market-beating model?

To outperform the S&P 500, following my five criteria alone is not enough. The five criteria (simplicity, sound rationale, rule-based clarity, sufficient sample size, and relevant data) would only increase the odds of model robustness, they do not offer an outperformance edge over the S&P 500. To beat the market, a model must also exhibit a quality of originality with a counterintuitive flavor. If a model is too intuitively obvious, many will have already discovered it and its edge will disappear. More importantly, to beat the market, a model must be relatively unknown so that it's not widely followed. If you can find the model in the Bloomberg terminal, it is already part of the market. The market cannot outperform itself.

My cyclical-market models are simple (a single metric – the CAPE), focused (one index – the S&P 500), logical (vectors over scalar) and above all, transparent (all rules are disclosed). Should you be worried that after publishing my models, their future efficacy will diminish? I would argue that such concern is unwarranted. First, only a fraction of the total investor universe will read my articles. Even if some have read them, only a fraction will believe in the models. Even if those who have read the articles are swayed by the rationale of the models, only a tiny fraction could internalize their conviction and have the discipline to follow-through over time. These probabilities are multiplicative and protect the models from being homogenized by the masses.

Theodore Wong graduated from MIT with a BSEE and MSEE degree and earned an MBA degree from Temple University. He served as general manager in several Fortune-500 companies that produced infrared sensors for satellite and military applications. After selling the hi-tech company that he started with a private equity firm, he launched TTSW Advisory, a consulting firm offering clients investment research services. For almost four decades, Ted has developed a true passion for studying the financial markets. He applies engineering design principles and statistical tools to achieve absolute investment returns by actively managing risk in both up and down markets. He can be reached at mailto:[email protected].

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits