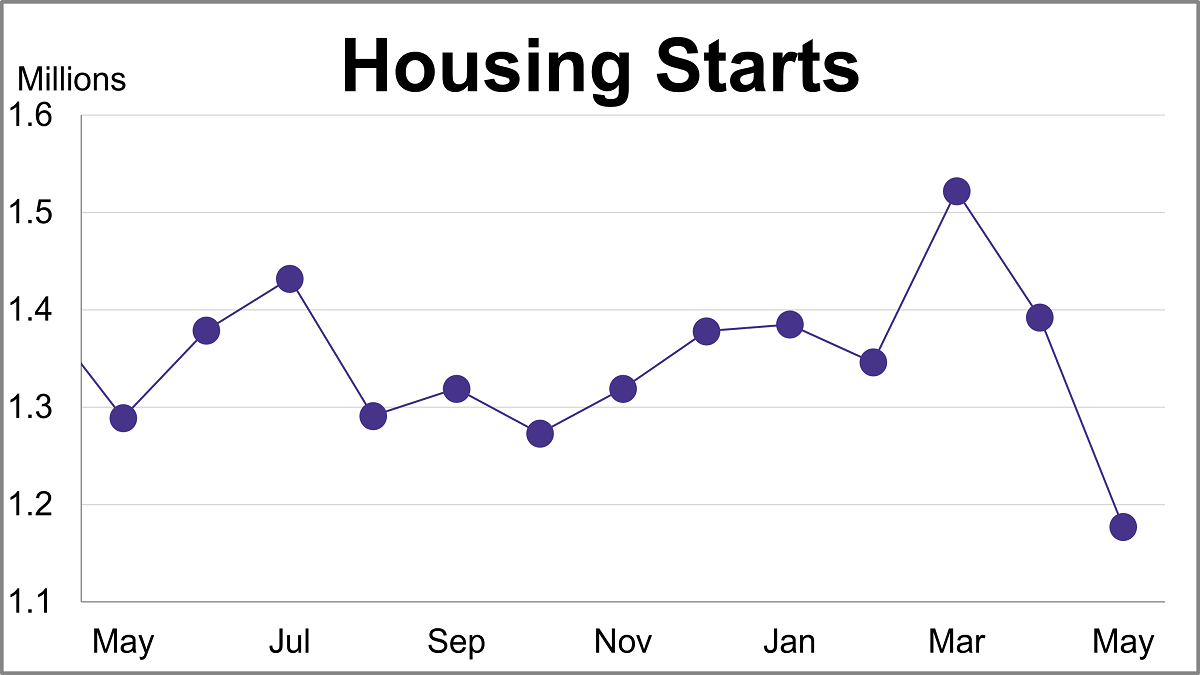

Housing starts sank 15.4% in May to a seasonally adjusted annual rate of 1.177 million, the lowest level in six years. The latest reading was significantly lower than the projected 1.430 million.

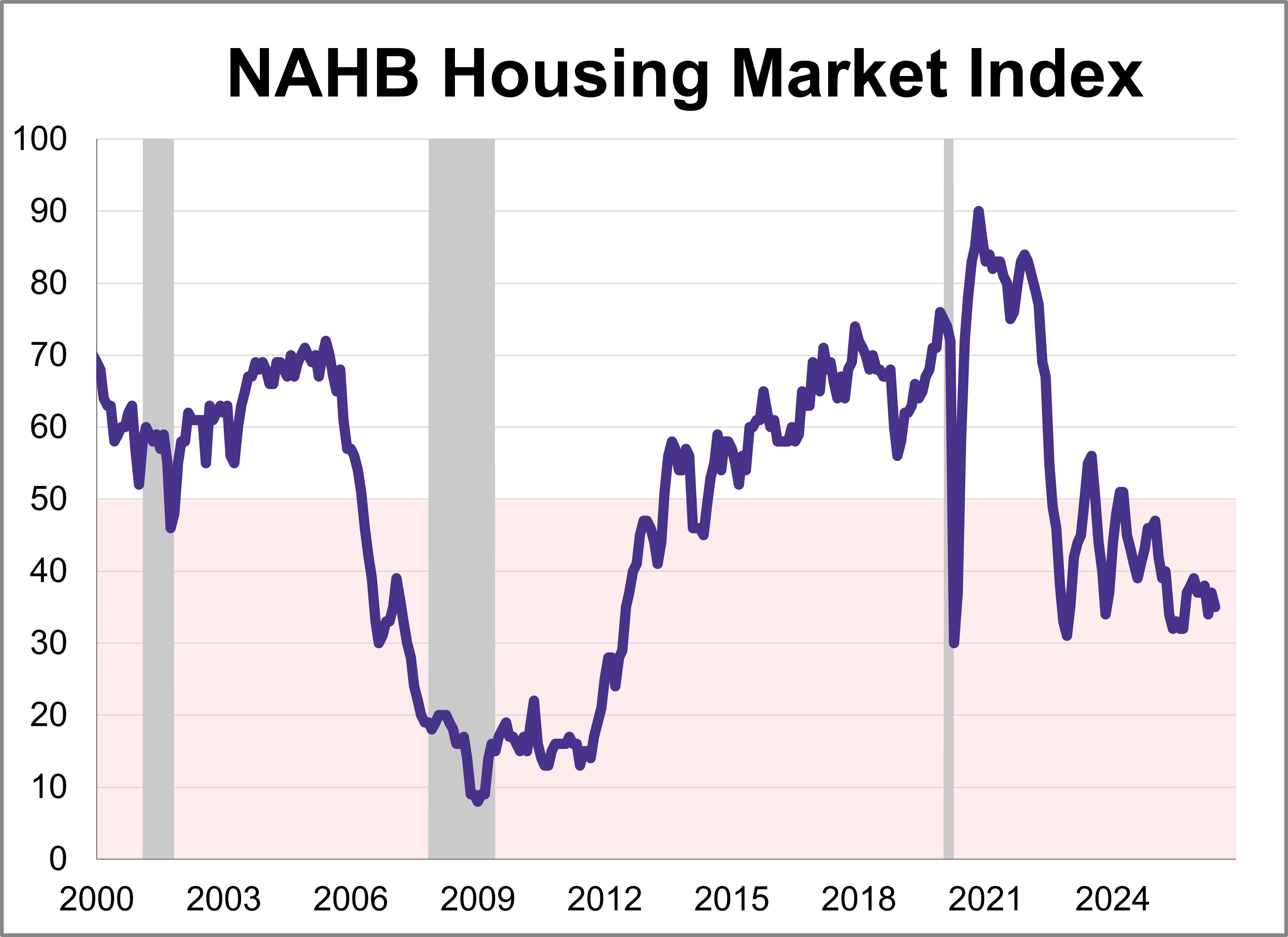

Builder confidence edged lower in June as ongoing affordability challenges continue to affect the housing market. The National Association of Home Builders (NAHB) Housing Market Index (HMI) fell 2 points from May to 35 this month, marking the 26th consecutive negative reading.

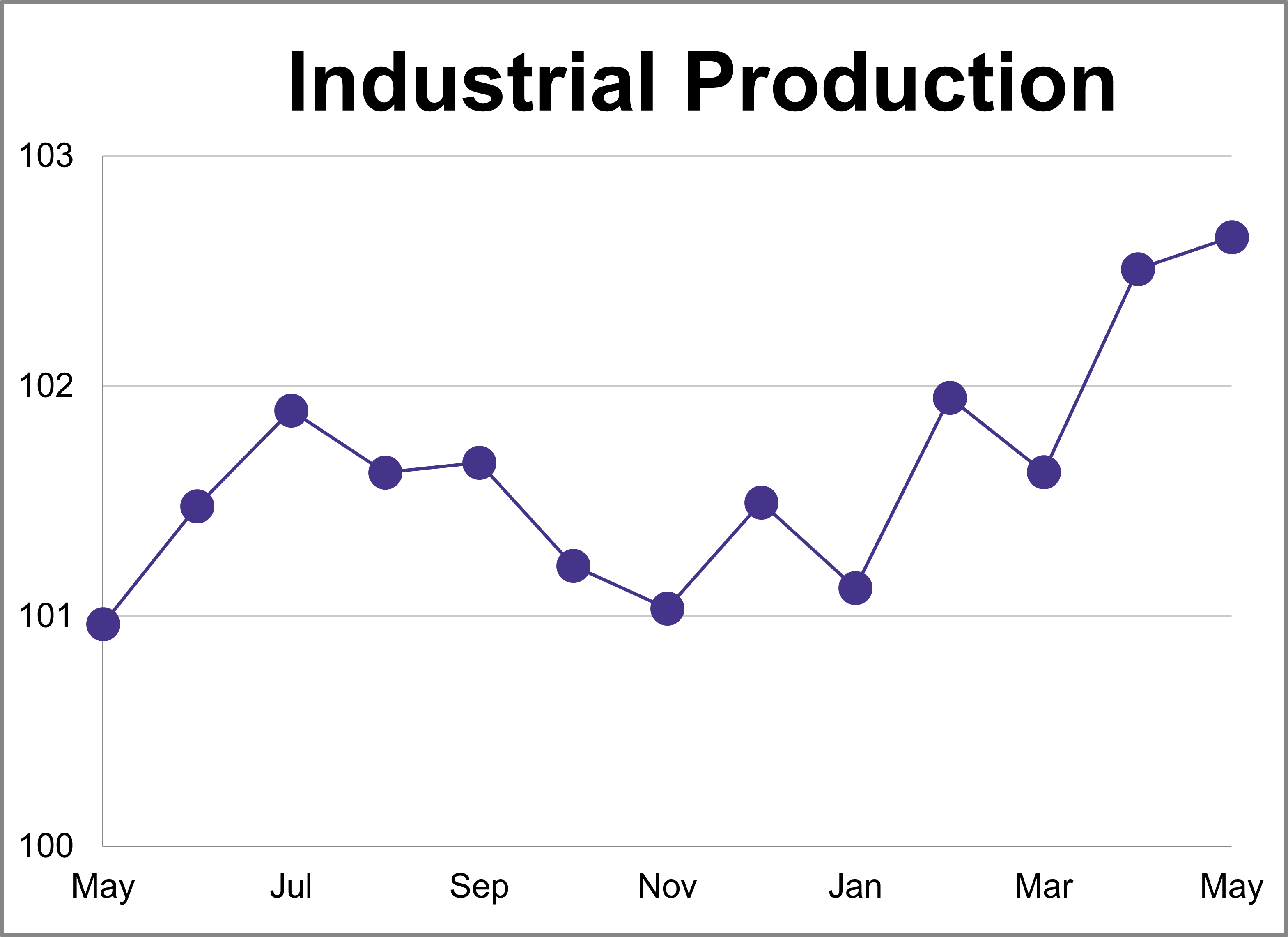

Industrial production rose less than expected in May, increasing 0.1% after a 0.9% jump in April. This was lower than the expected 0.3% growth and marks a 1.7% increase compared to one year ago.

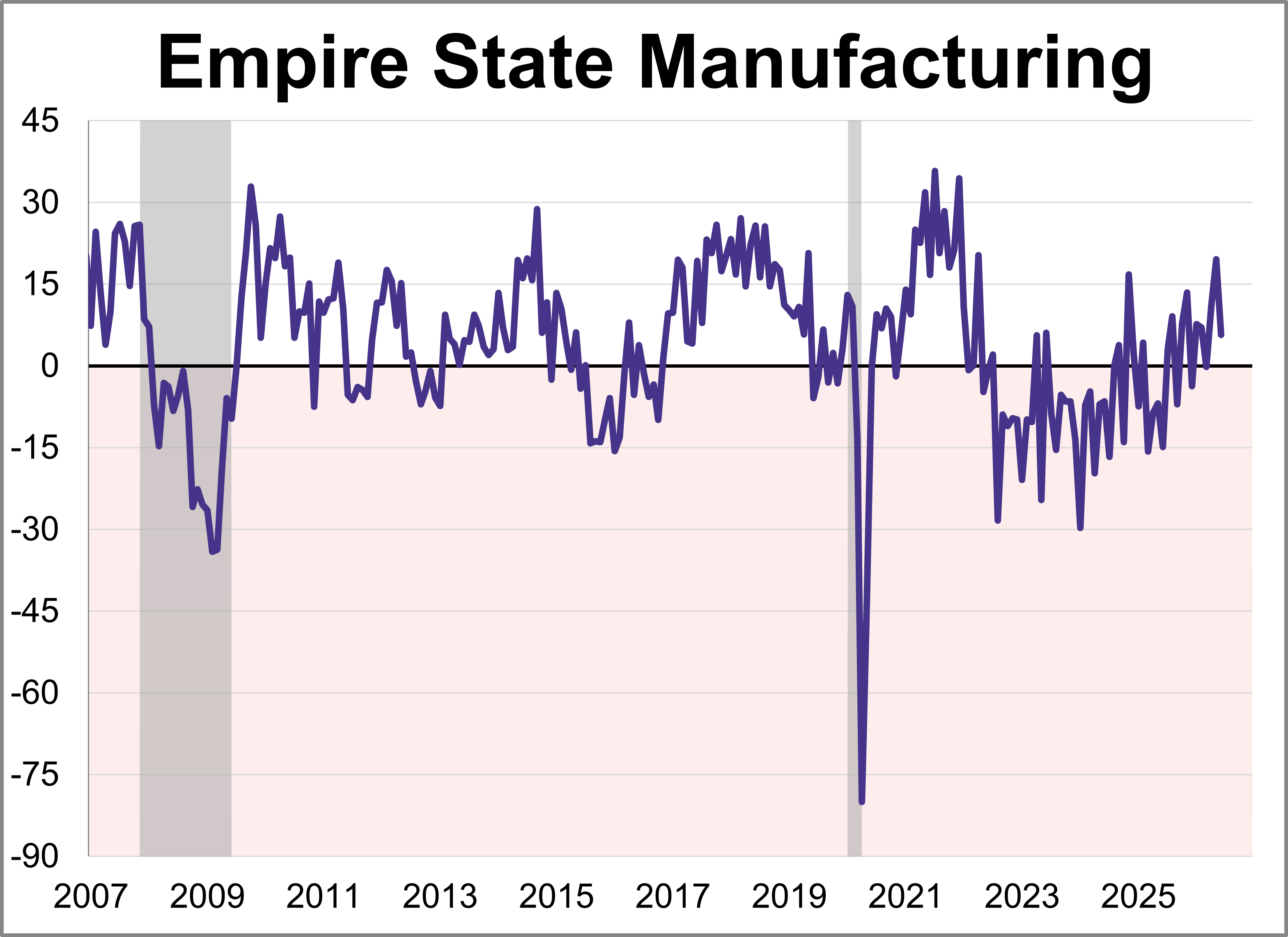

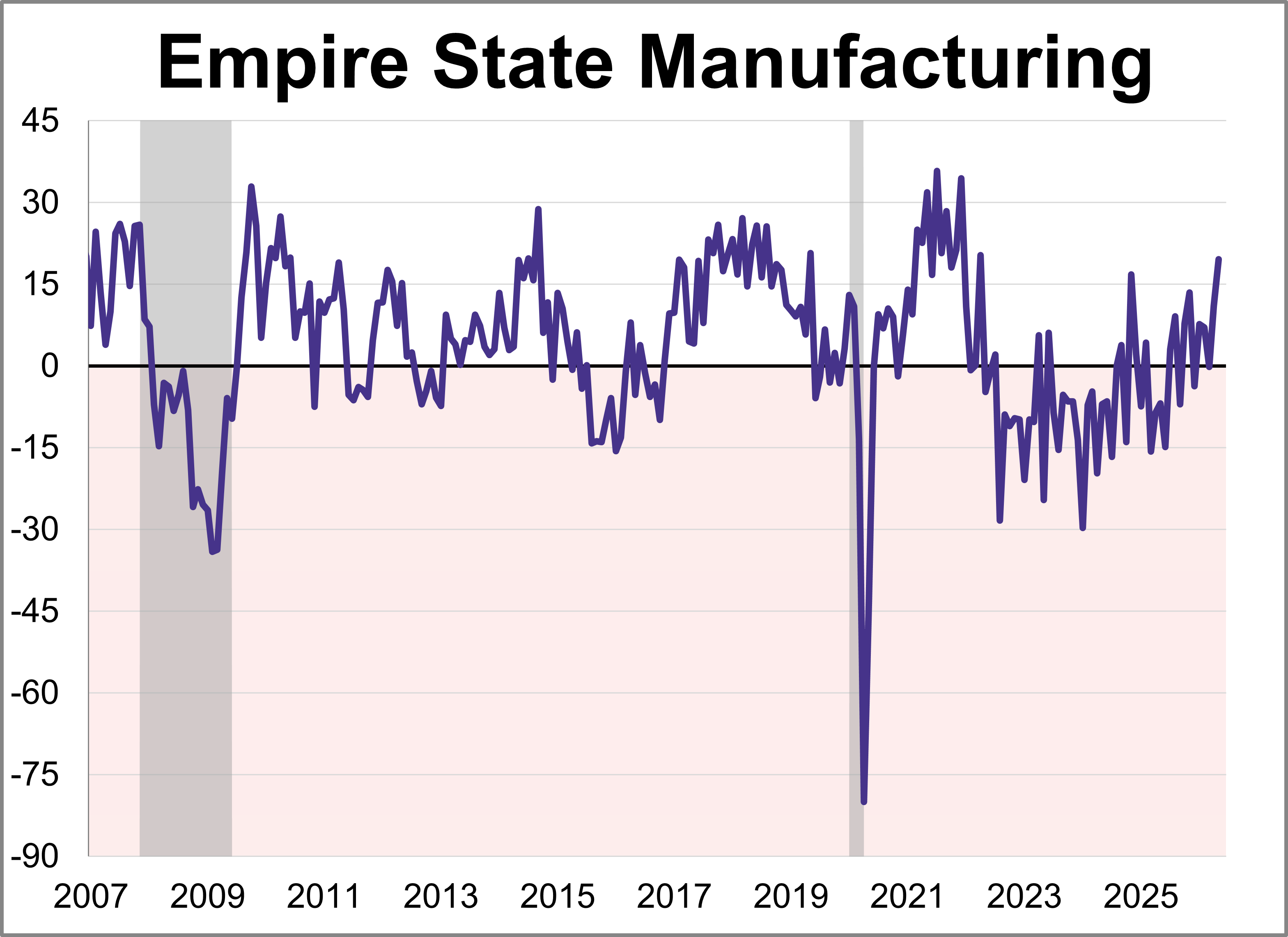

Manufacturing activity rose modestly in New York State, according to the Empire State Manufacturing June survey. The diffusion index for General Business Conditions remained positive but dropped 13.9 points to 5.7, falling short of the 13.2 forecast.

The U.S. economy faced intensifying headwinds in May as both consumer and wholesale inflation metrics surged to multi-year highs.

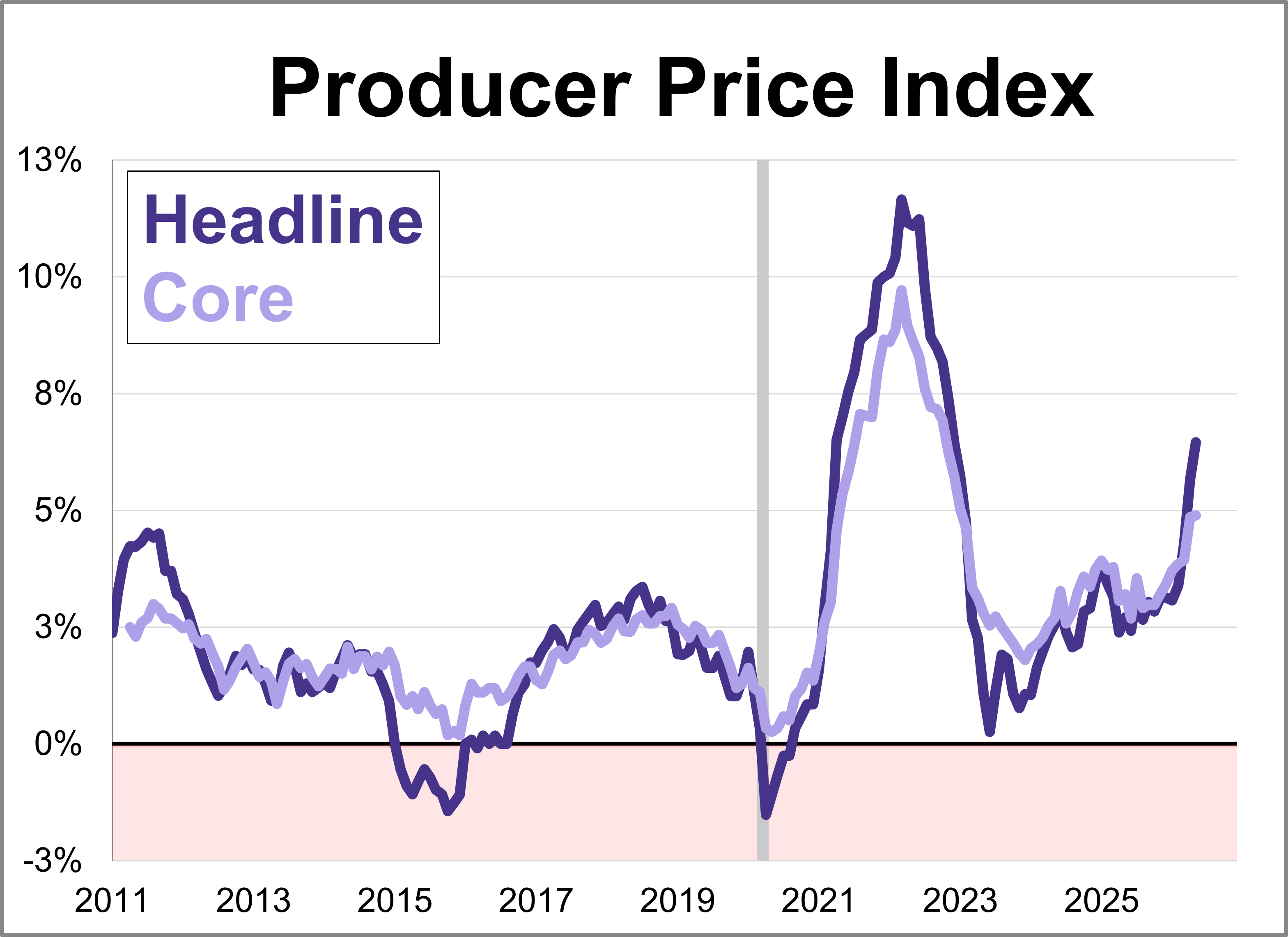

May's Producer Price Index (PPI) data delivered another blow to inflation watchers, as wholesale price growth came in hotter than expected.

With the latest CPI report showing that inflation is likely here to stay, it could be time to pivot towards ETFs with downside protection.

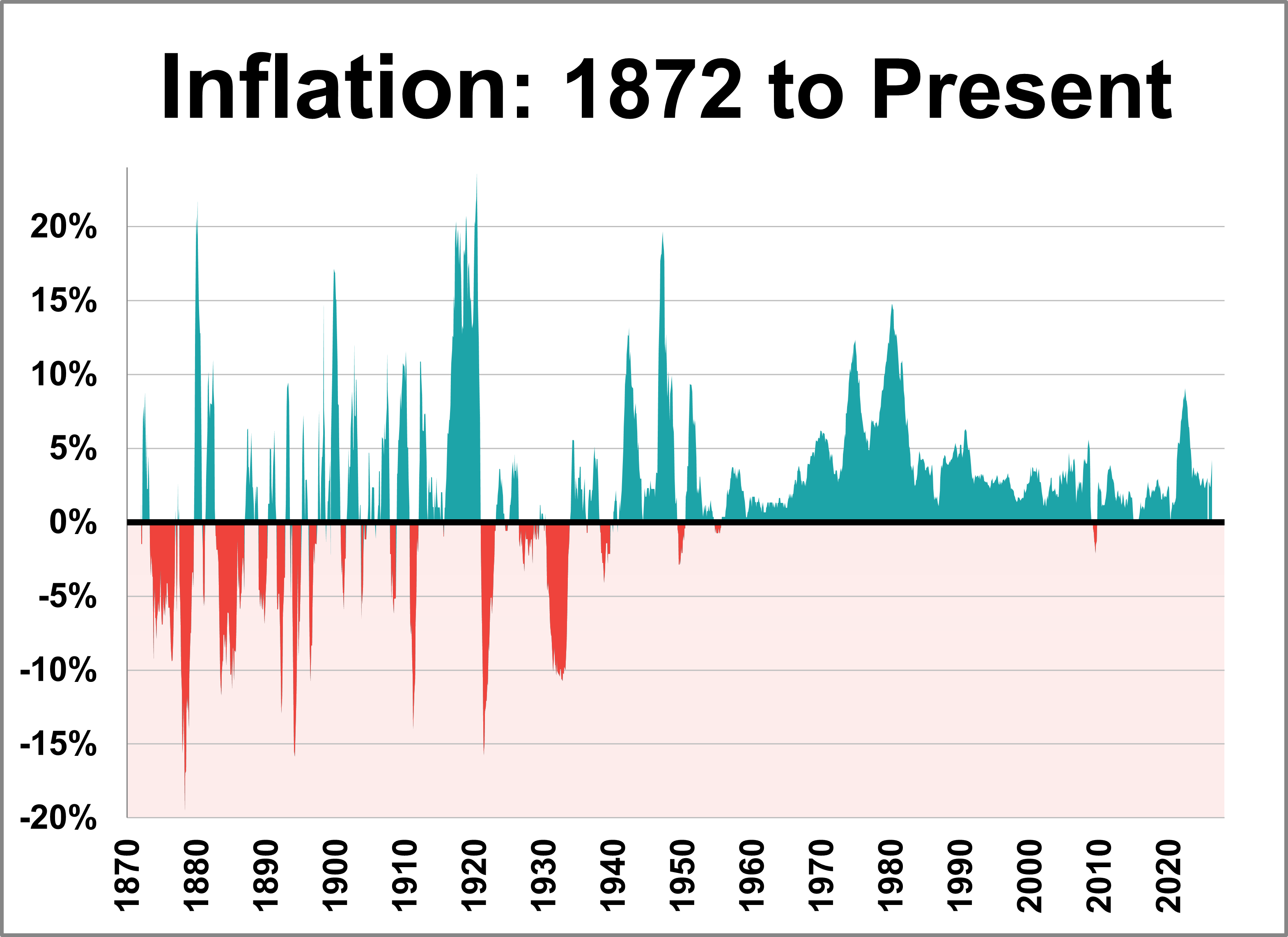

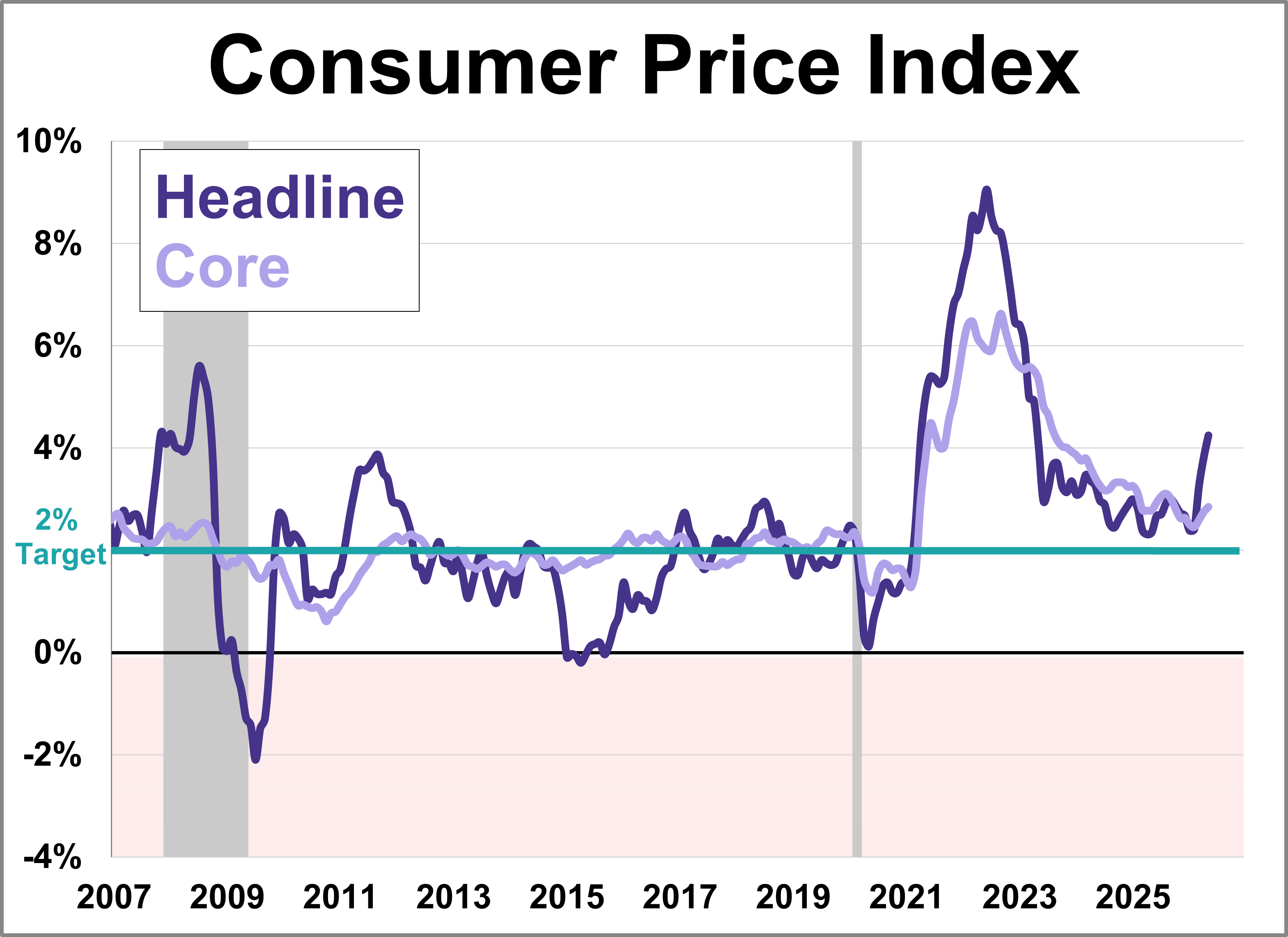

The May release of the Consumer Price Index for Urban Consumers (CPI-U) places the year-over-year inflation rate at 4.25%, its highest level in over three years. This keeps inflation above the post-WWII average of 3.72% for a second straight month and marks the third consecutive month that the current rate is above the 10-year moving average, which currently sits at 3.27%.

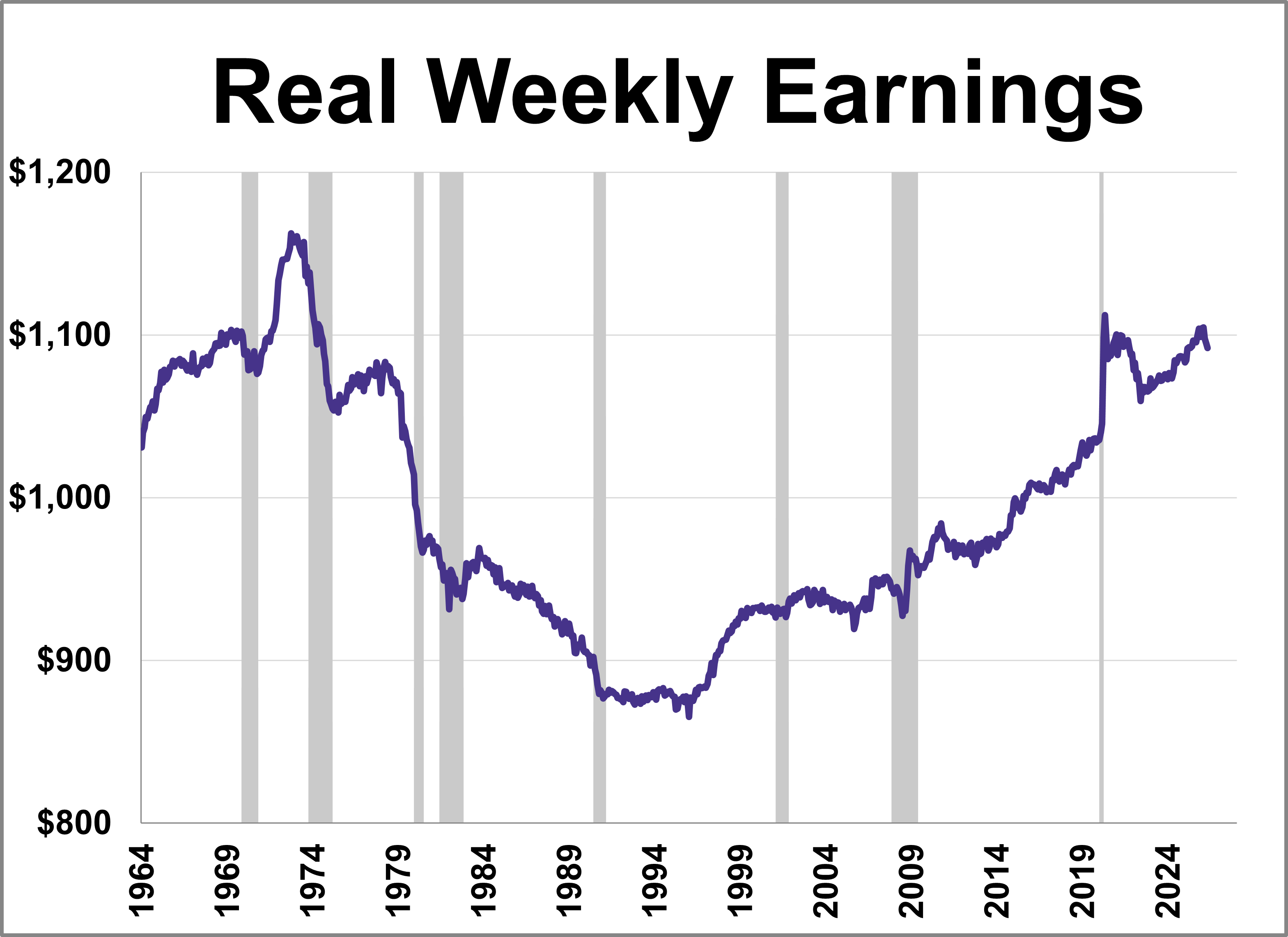

This series has been updated to include the May release of the consumer price index as the deflator and the monthly employment update. The latest hypothetical real (inflation-adjusted) annual earnings are at $54,604, down 6.1% from over 50 years ago.

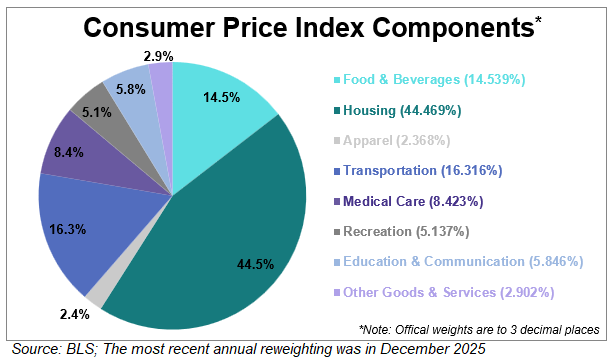

Inflation affects everything from grocery bills to rent, making the Consumer Price Index (CPI) one of the most closely watched economic indicators. The Bureau of Labor Statistics (BLS) tracks this by categorizing spending into eight categories, each weighted by its relative importance.

Inflation surged to 4.2% year-over-year in May, hitting its highest level in over three years. The headline figure for the Consumer Price Index (CPI) was consistent with the forecast, driven primarily by cost increases in energy, shelter, and food.

Several articles enjoyed strong performance during the month of May, though there does not seem to have been a unifying theme, unless it is pointing out mistaken beliefs or unexamined conventions.

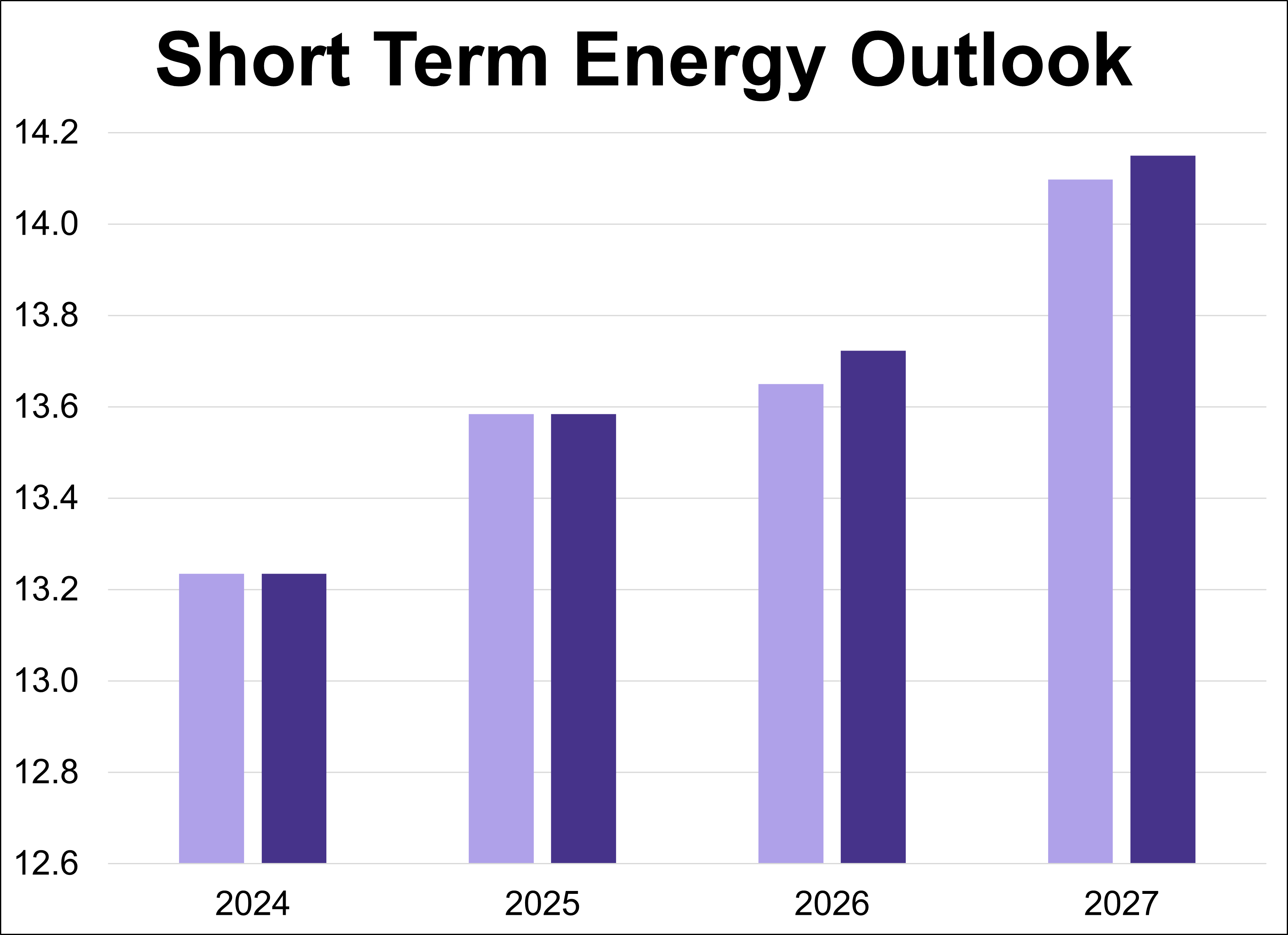

The U.S. Energy Information Administration (EIA) has released its latest Short-Term Energy Outlook (STEO), providing forecasts for energy markets. This article presents the annual production outlooks for crude oil, natural gas, and natural gas liquids (NGLs), comparing the June 2026 projections against the previous month's estimates.

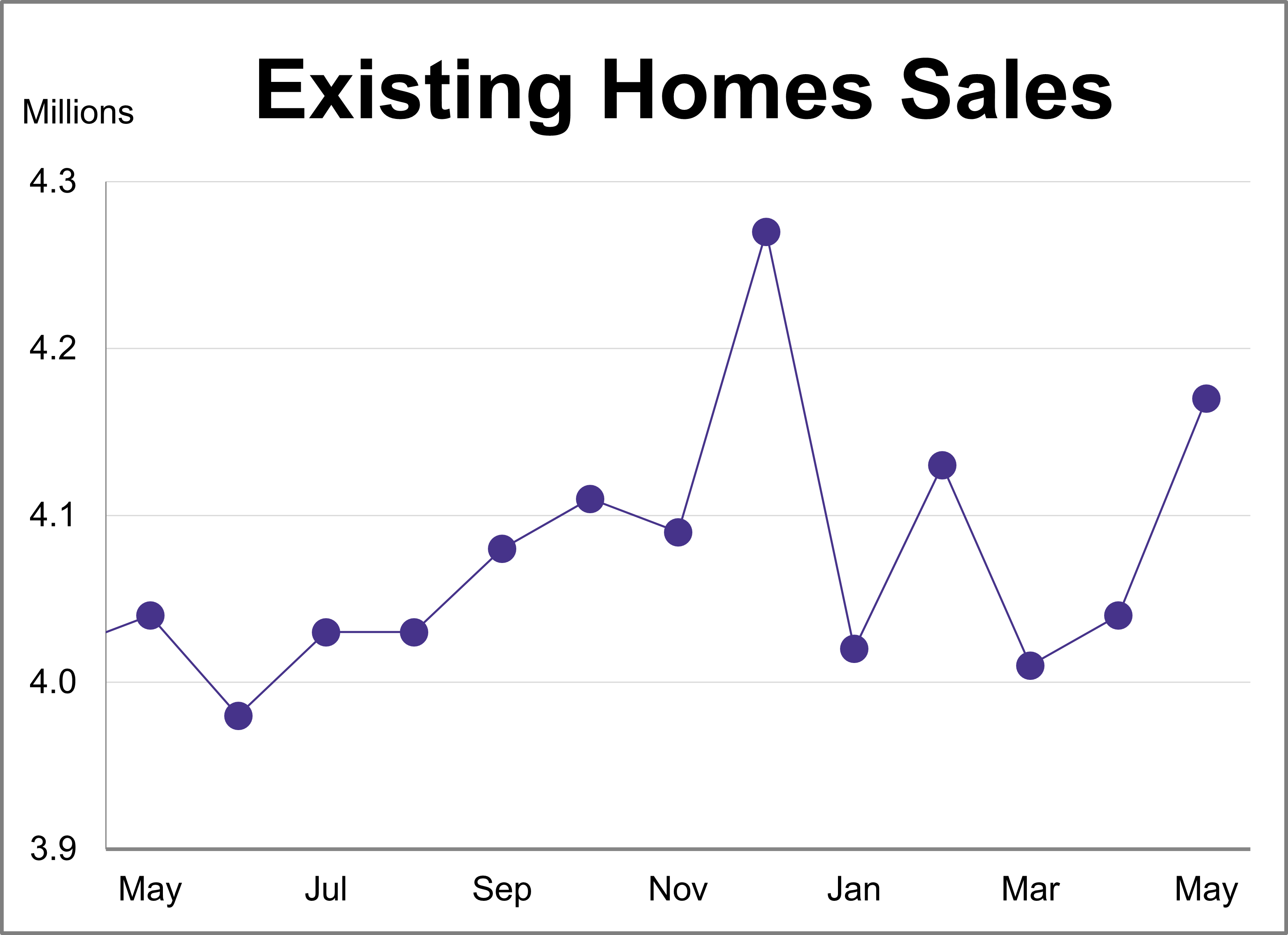

Existing home sales reached their highest level of the year in May, rising 3.2% after a 0.7% increase in April. According to the National Association of Realtors (NAR), sales reached a seasonally adjusted annual rate of 4.17 million units, surpassing the projected 4.07 million.

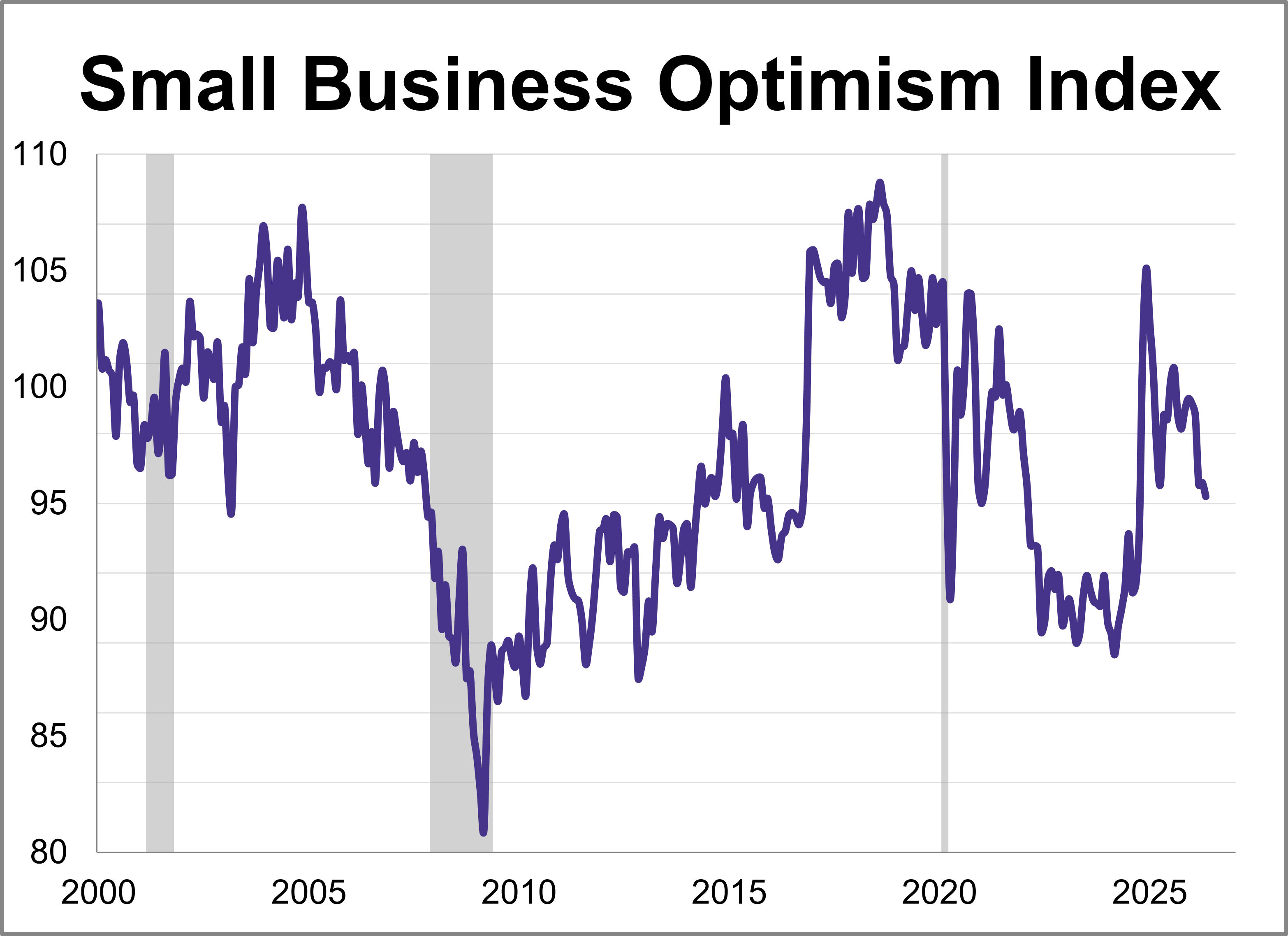

The NFIB Small Business Optimism Index dropped 0.6 points to 95.3, reaching its lowest level since October 2024. The index remains below its historical average for a third straight month.

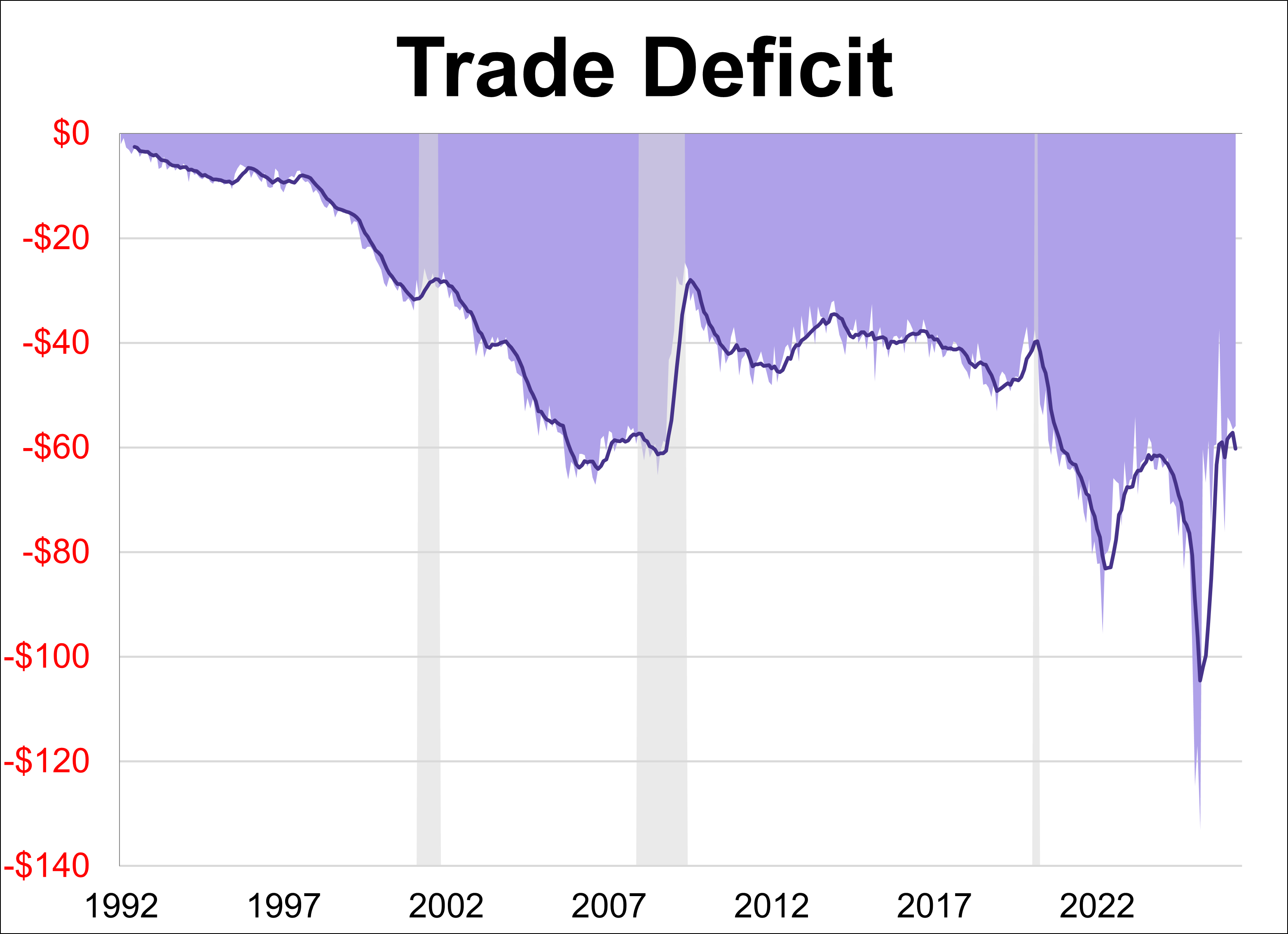

The U.S. trade deficit shrunk just over 1% in April to $55.88B after expanding nearly 3% the previous month. The latest reading barely missed the forecast of -$56.20B.

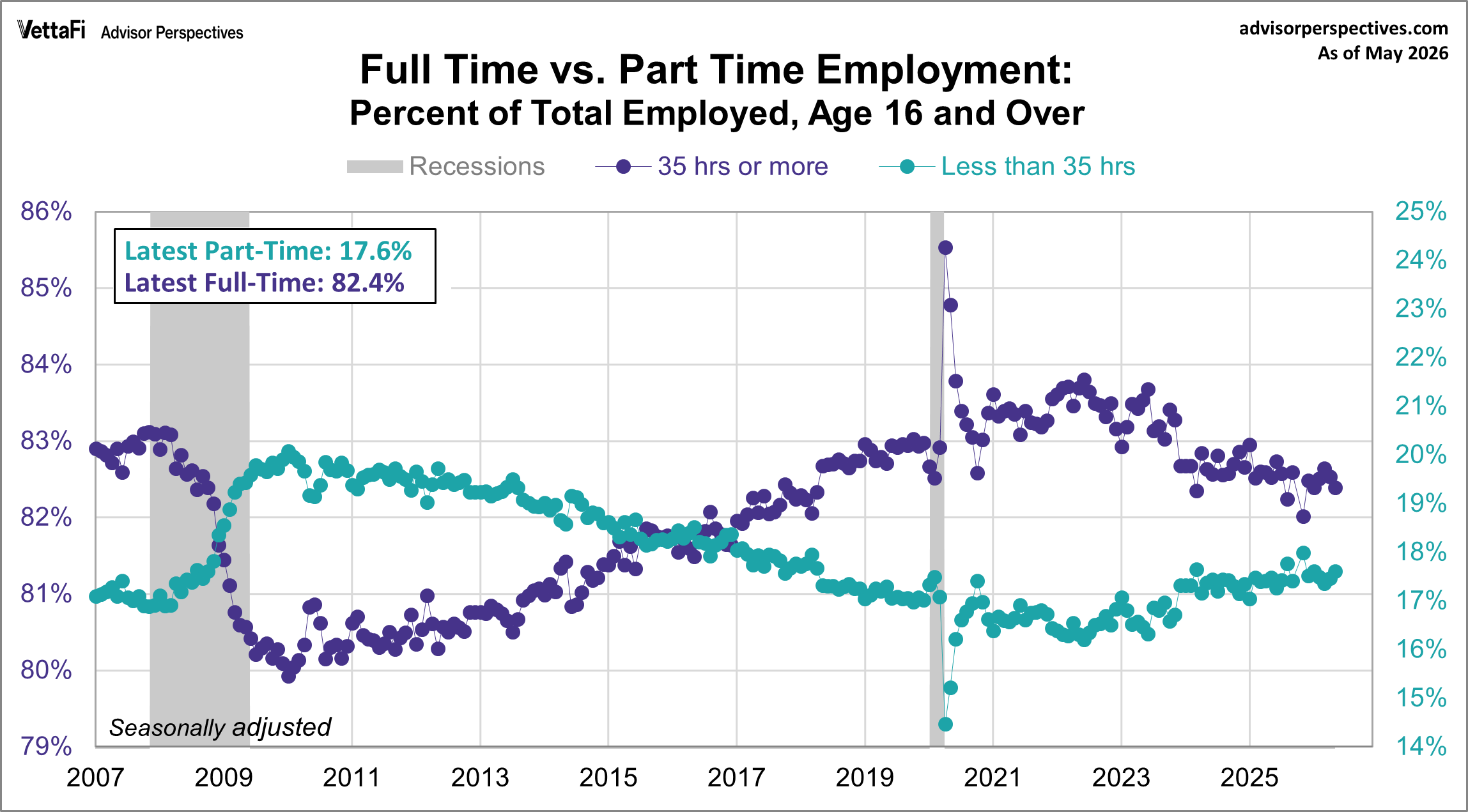

May's employment report showed that 17.6% of total employed workers were part time and 82.4% of total employed workers were full-time.

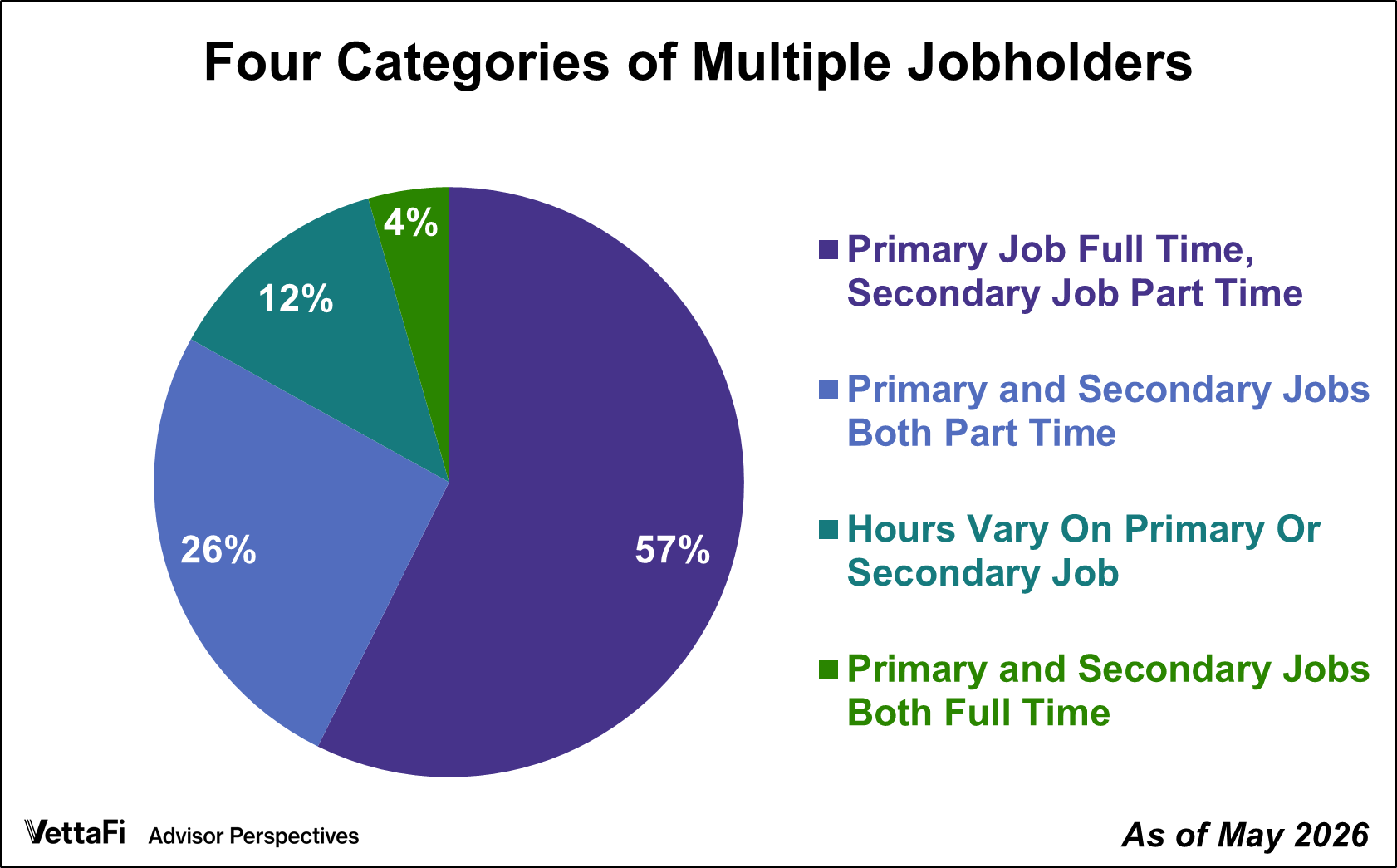

Multiple jobholders accounted for 5.1% of civilian employment in May, the lowest level in ten months.

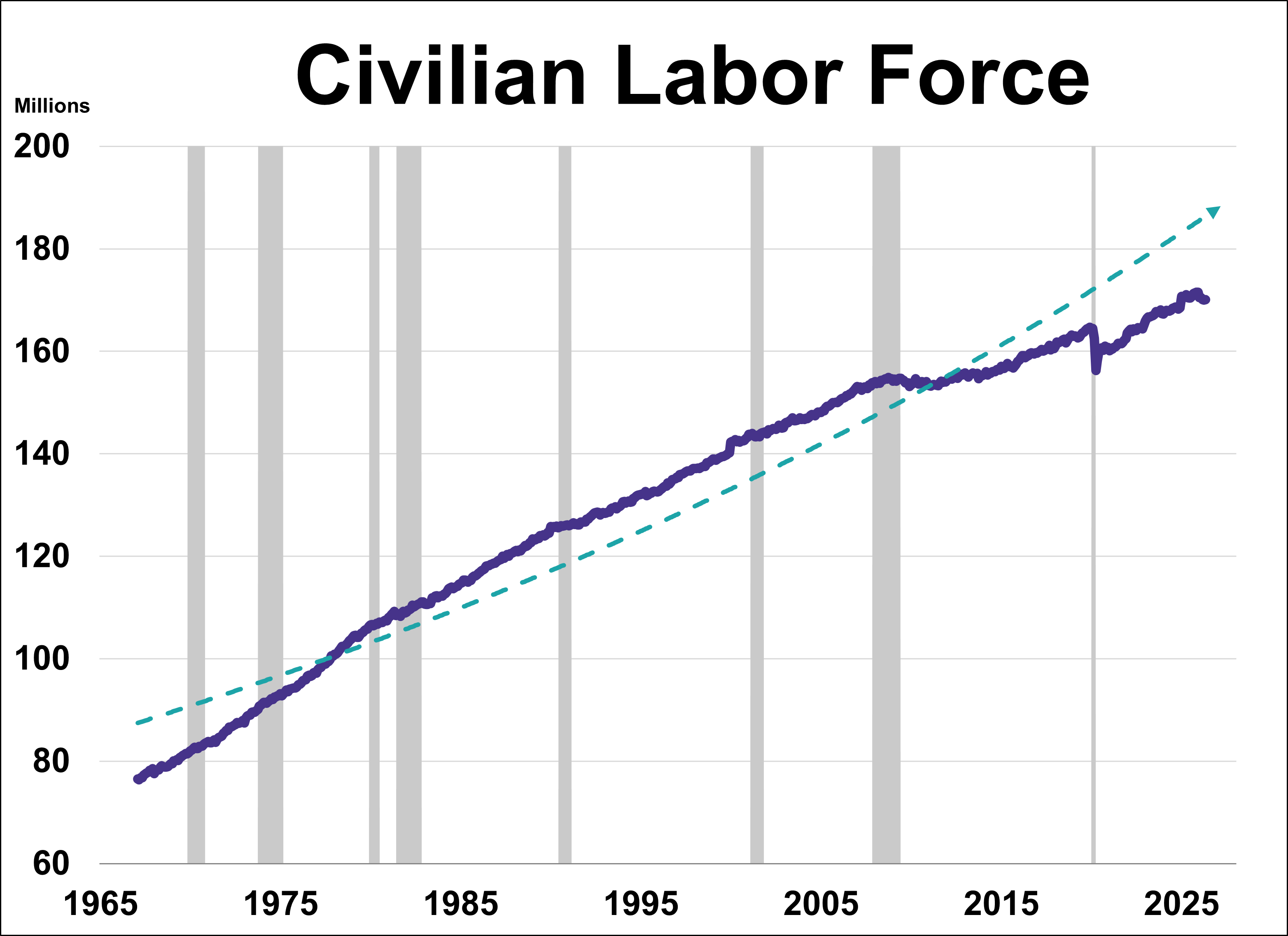

What does the ratio of unemployment claims to the civilian labor force tell us about where we are in the business cycle and recession risk?

The U.S. labor market took center stage last week as three major labor market indicators outperformed forecasts. Robust payroll additions in both the public and private sectors, paired with a massive surge in job openings, point to a workforce on solid footing.

Ride the momentum wave. Discover how tech-fueled factors propelled momentum and high-beta ETFs to historic, benchmark-crushing gains.

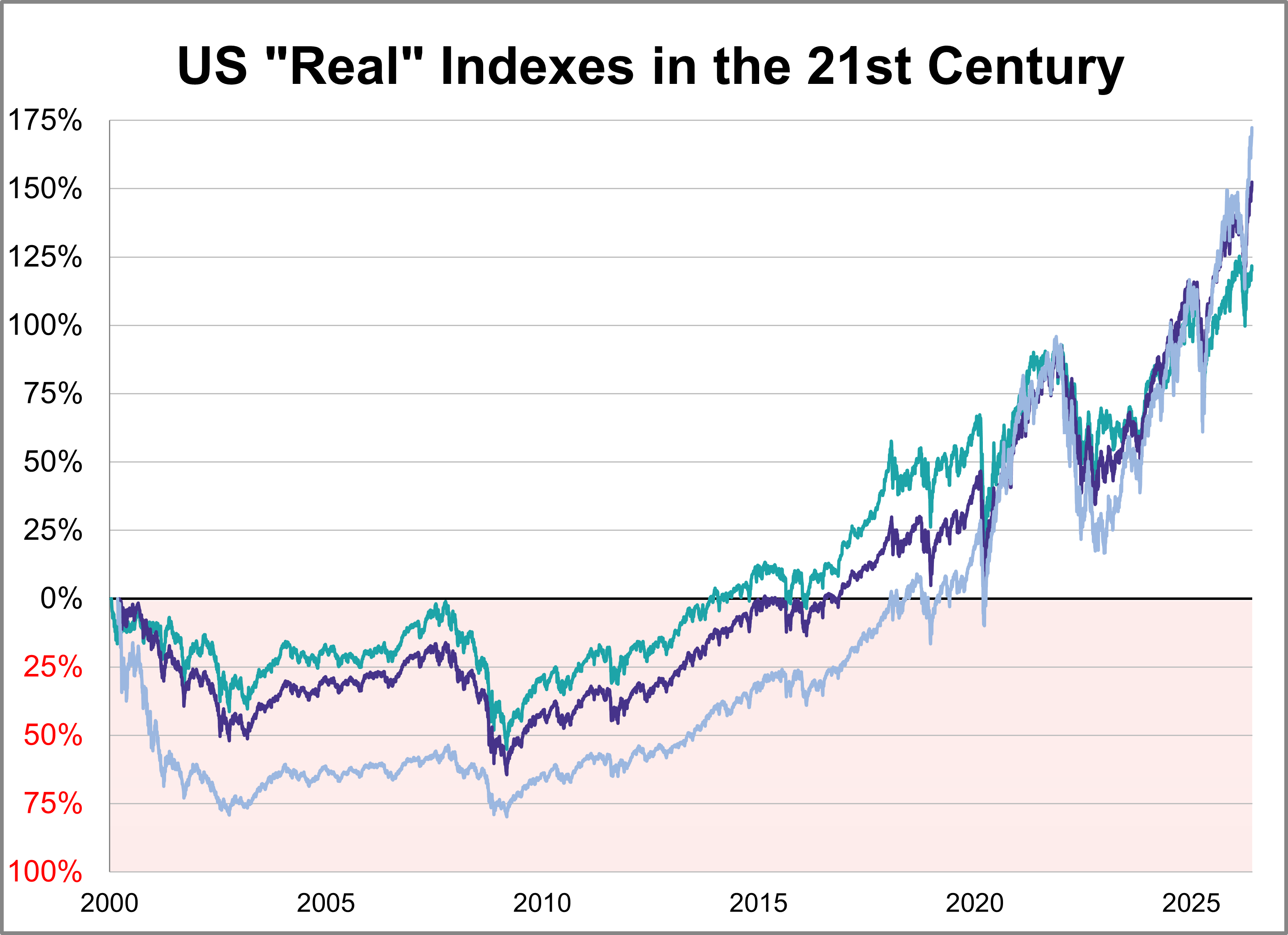

Here is a look at real (inflation-adjusted) charts of the S&P 500, Dow 30, and Nasdaq composite since their 2000 highs. We've updated this through the May 2026 close.

Here's an interesting set of charts that will especially resonate with those of us who follow economic and market cycles. Imagine that five years ago you invested $10,000 in the S&P 500. How much would it be worth today, with dividends reinvested but adjusted for inflation?

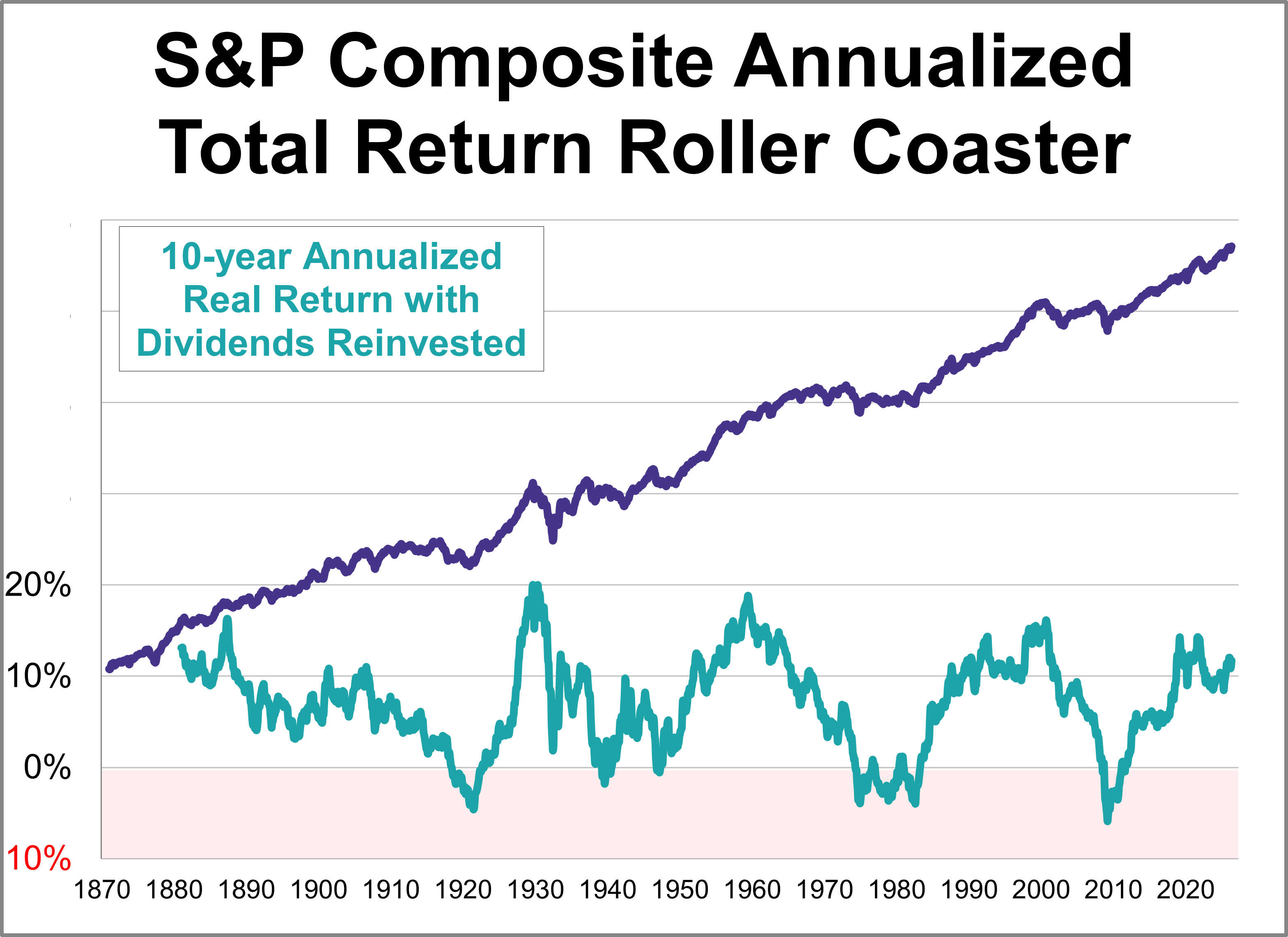

The S&P 500 real monthly averages of daily closes reached a its all-time high in May 2026. Let's examine the past to broaden our understanding of the range of historical bull and bear market trends in market performance.

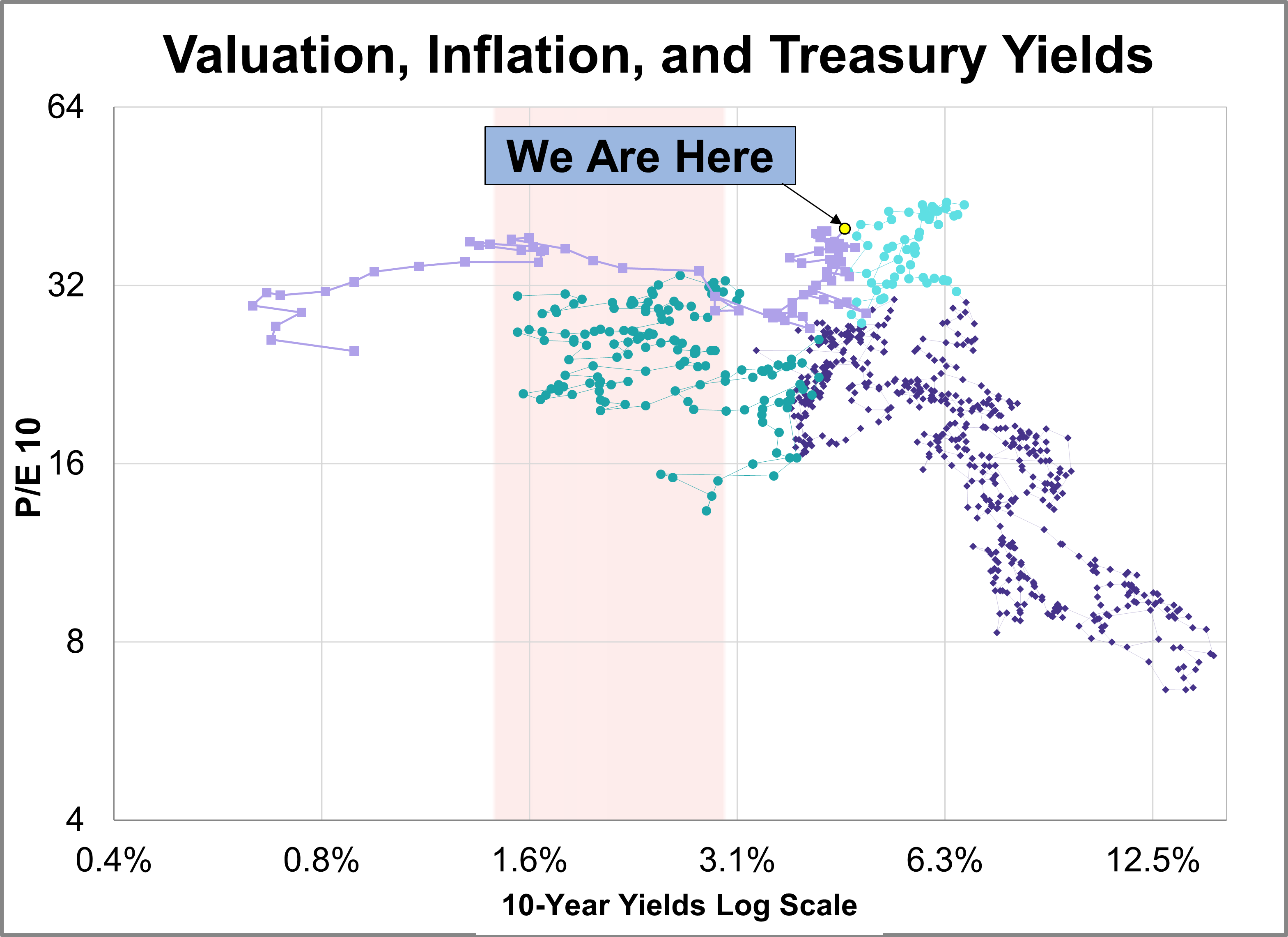

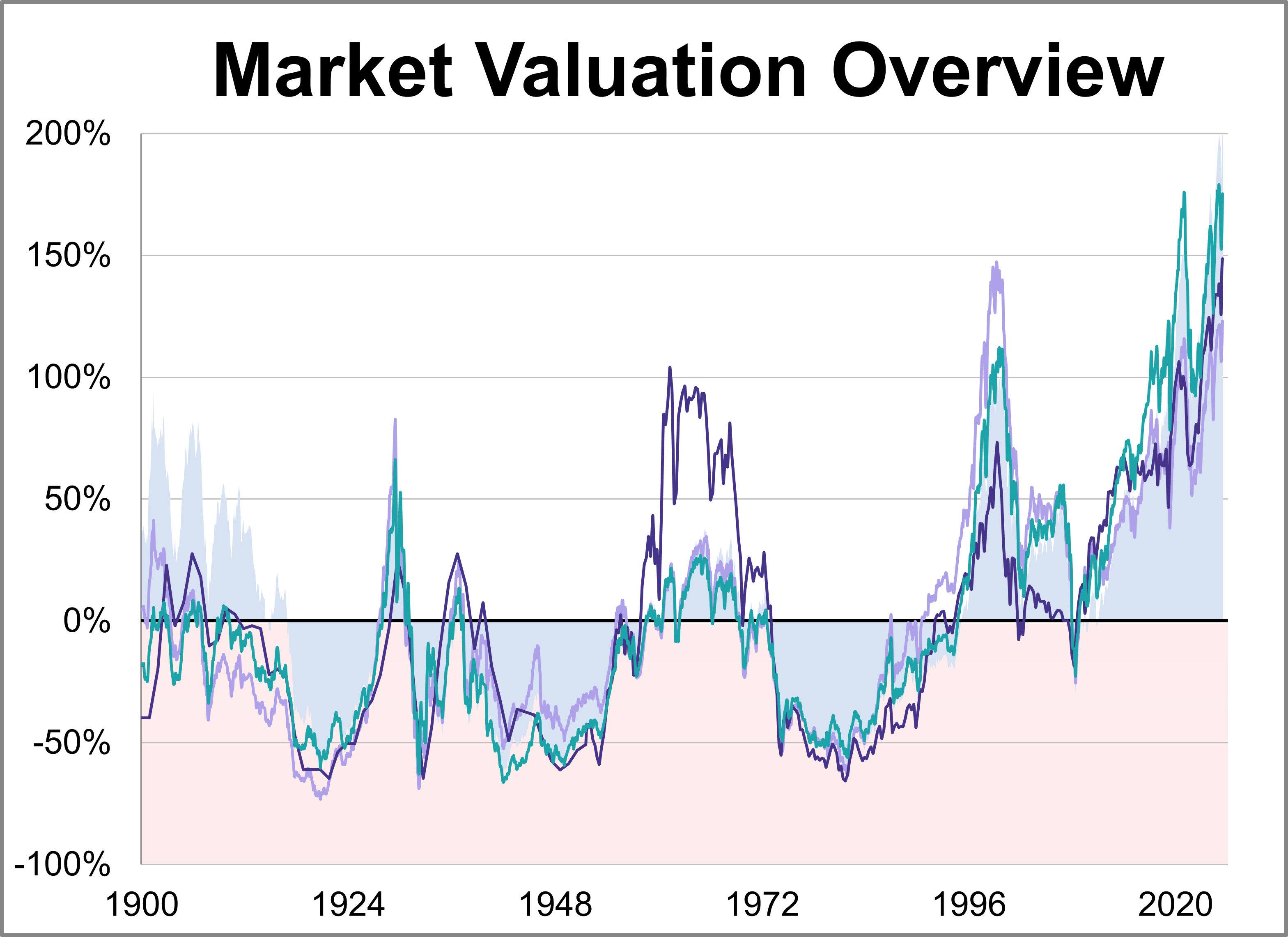

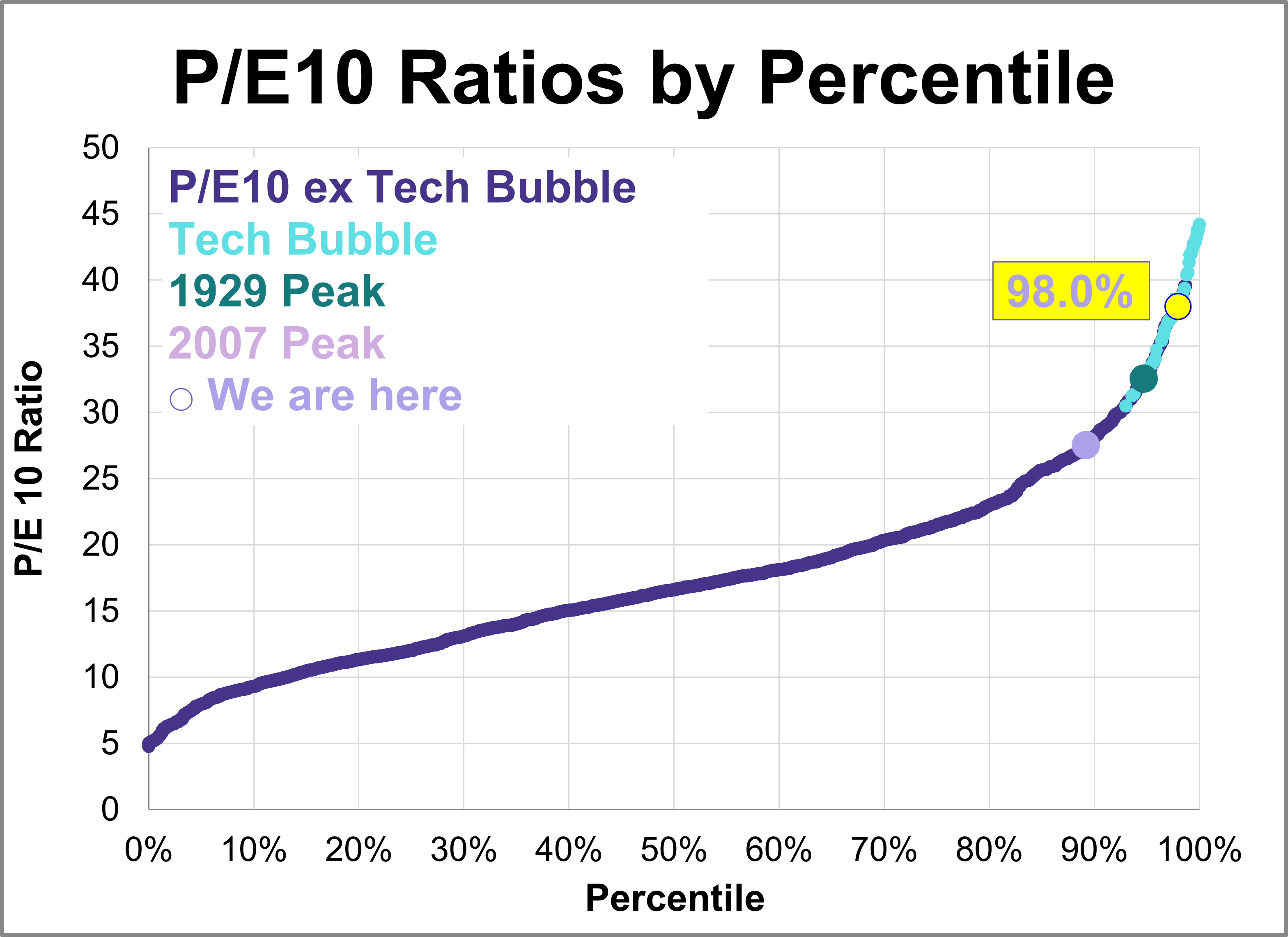

Our monthly market valuation updates have long had the same conclusion: US stock indexes are significantly overvalued, which suggests cautious expectations for investment returns. This analysis focuses on the P/E10 ratio, key indicator of market valuation, and its correlation with inflation and the 10-year Treasury yield.

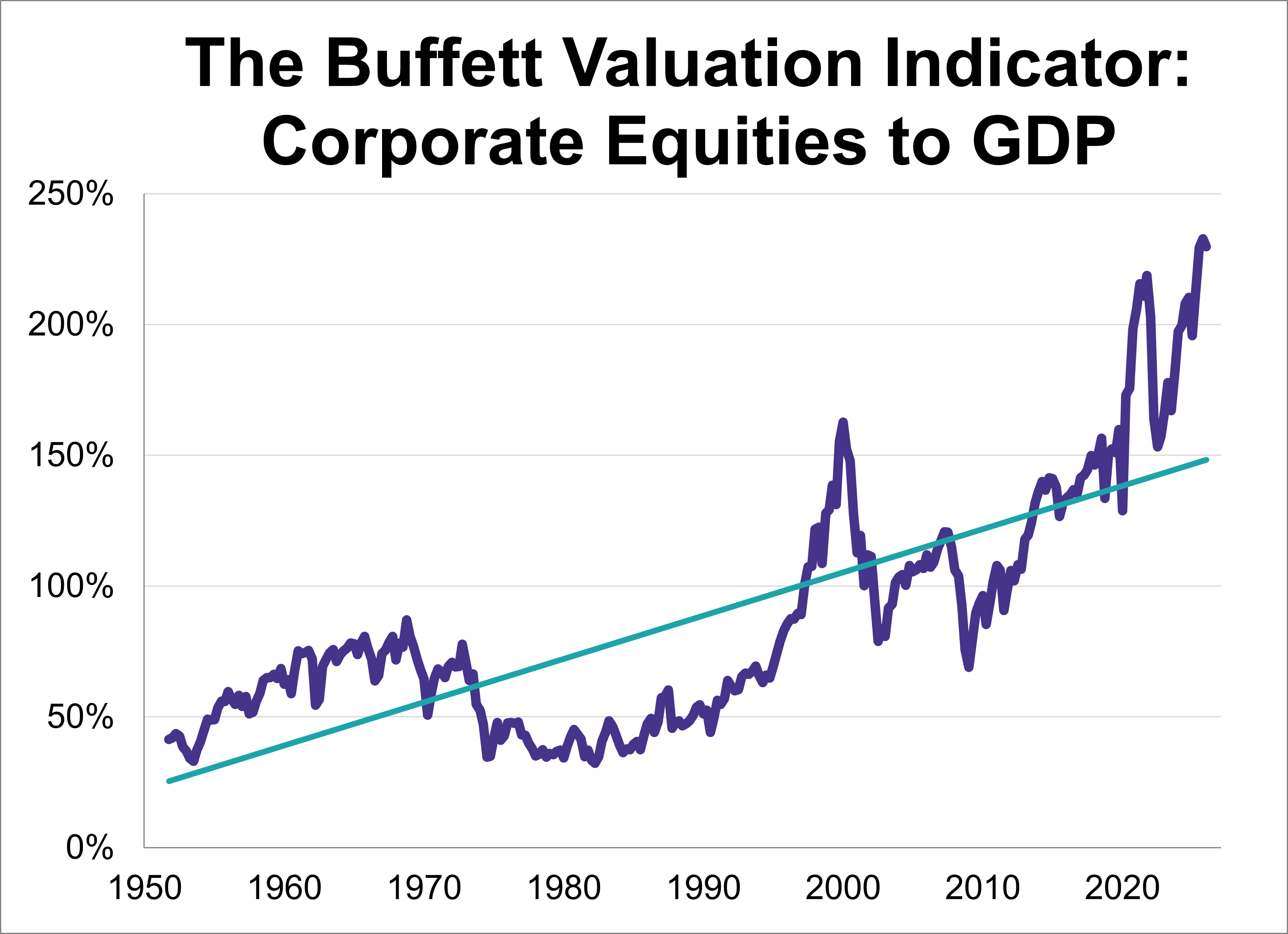

Following the Q1 GDP second estimate, the 'Buffett Indicator'—the ratio of corporate equities to GDP—now stands at 229.7%. This marks the second-highest reading in history, eclipsed only by the previous quarter.

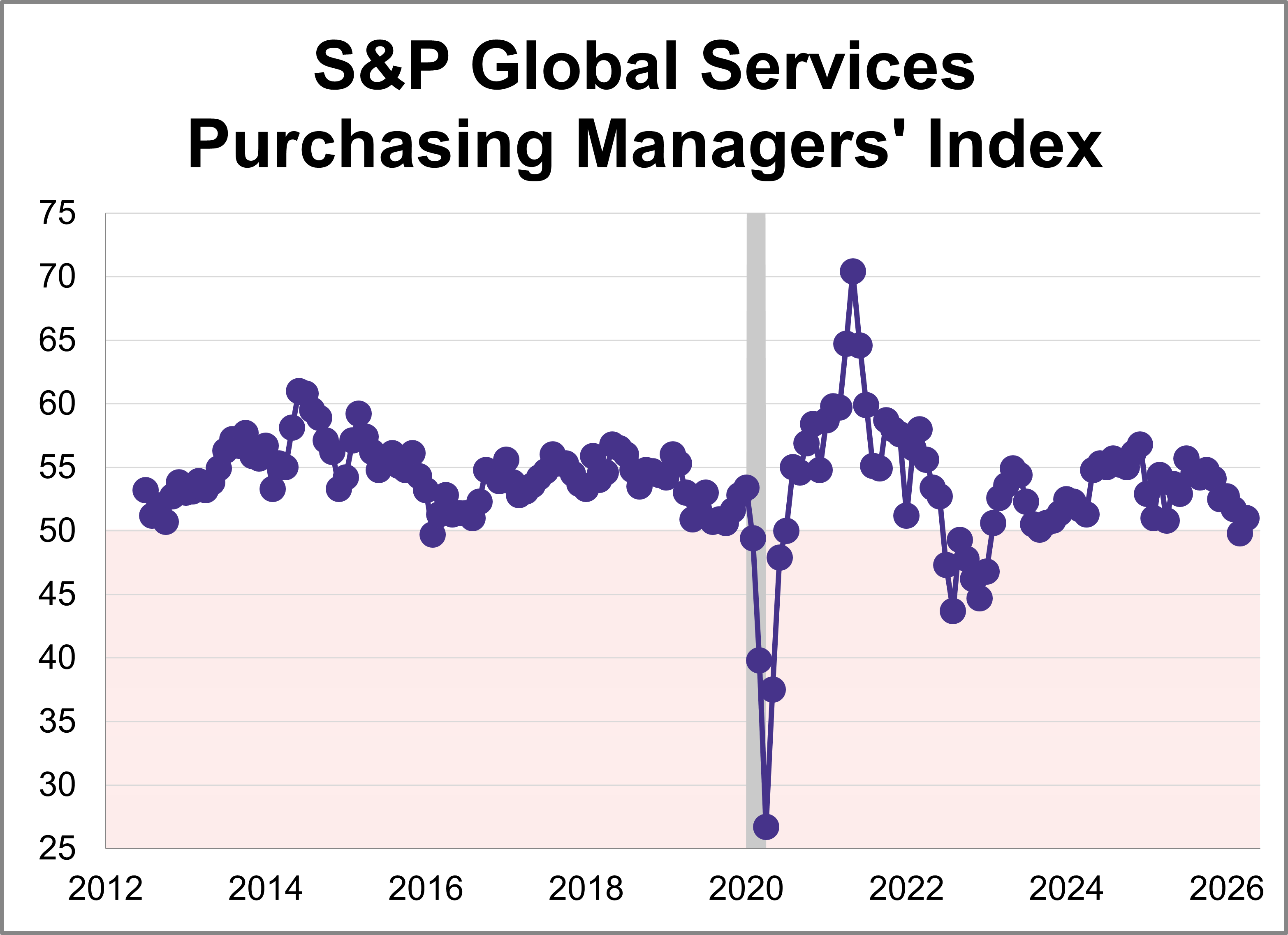

The May U.S. Services Purchasing Managers' Index (PMI) from S&P Global inched down 0.3 points to 50.7, indicating slower expansion in the services sector. The latest reading was lower than the forecast of 50.9 and was among the weakest months of expansion in the past 2.5 years.

Here is a summary of the four market valuation indicators we update on a monthly basis.

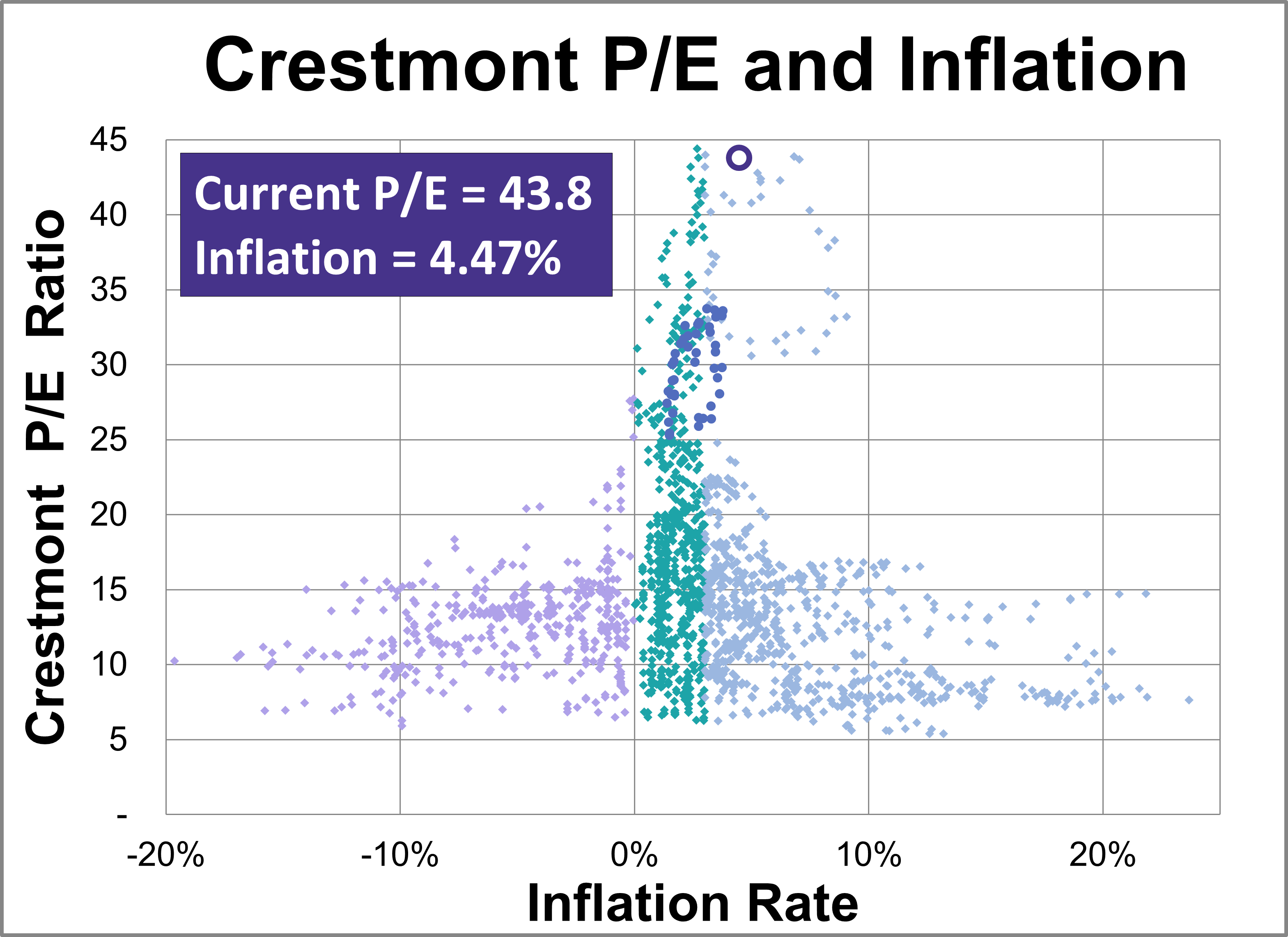

Based on May's S&P 500 average of daily closes, the Crestmont P/E of 43.8 is 185% above its arithmetic mean, 213% above its geometric mean, and is in the 100th percentile of this 14-plus-decade series.

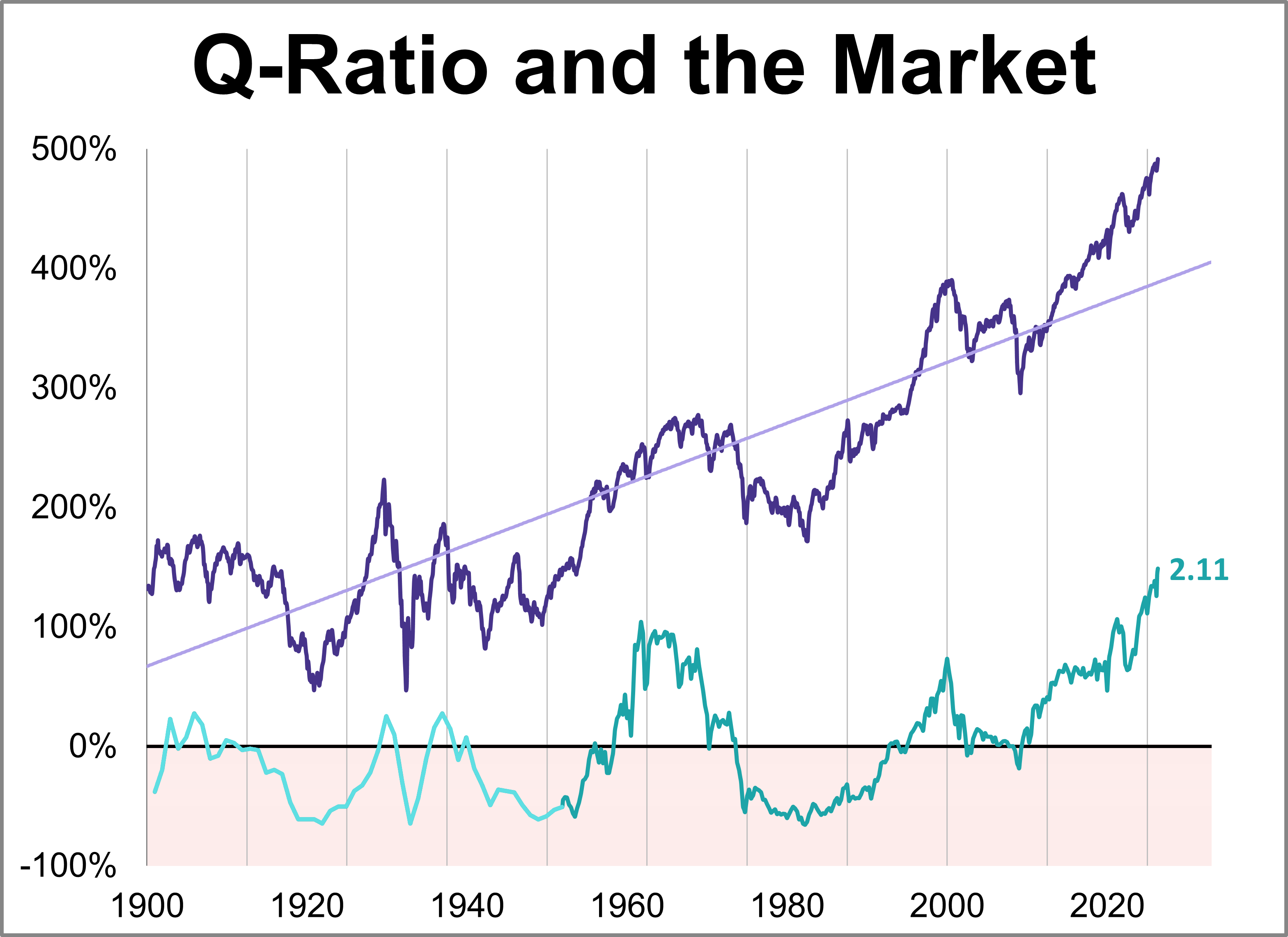

The Q Ratio is the total price of the market divided by the replacement cost of all its companies. As of May 2026, the latest Q-ratio is at 2.11, the highest level in history.

Here is the latest update of a popular market valuation method, Price-to-Earnings (P/E) ratio, using the most recent Standard & Poor's "as reported" earnings and earnings estimates, and the index monthly average of daily closes for the past month. The latest trailing twelve months (TTM) P/E ratio is 25.9 and the latest P/E10 ratio is 39.9, the highest level since 2000.

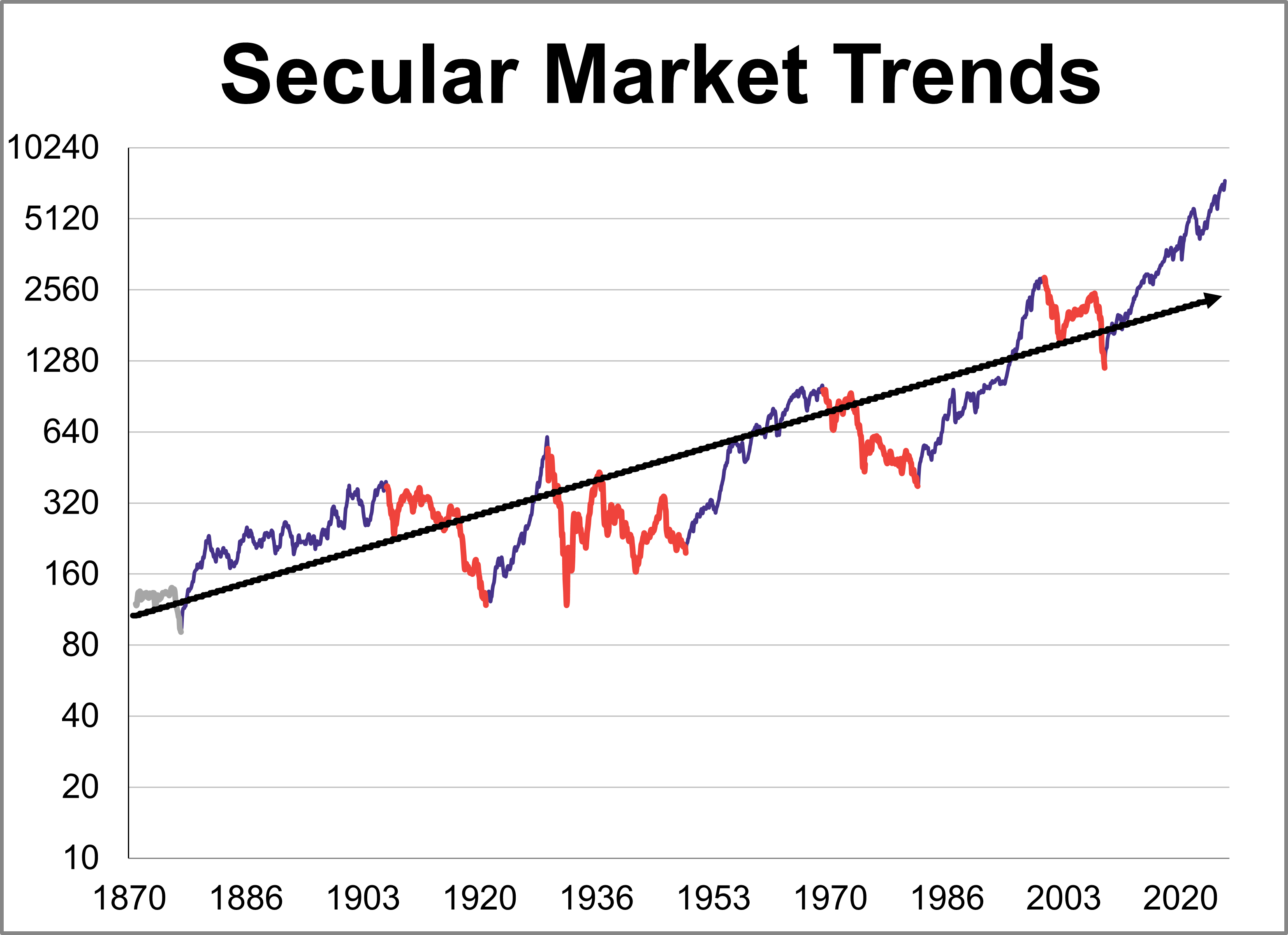

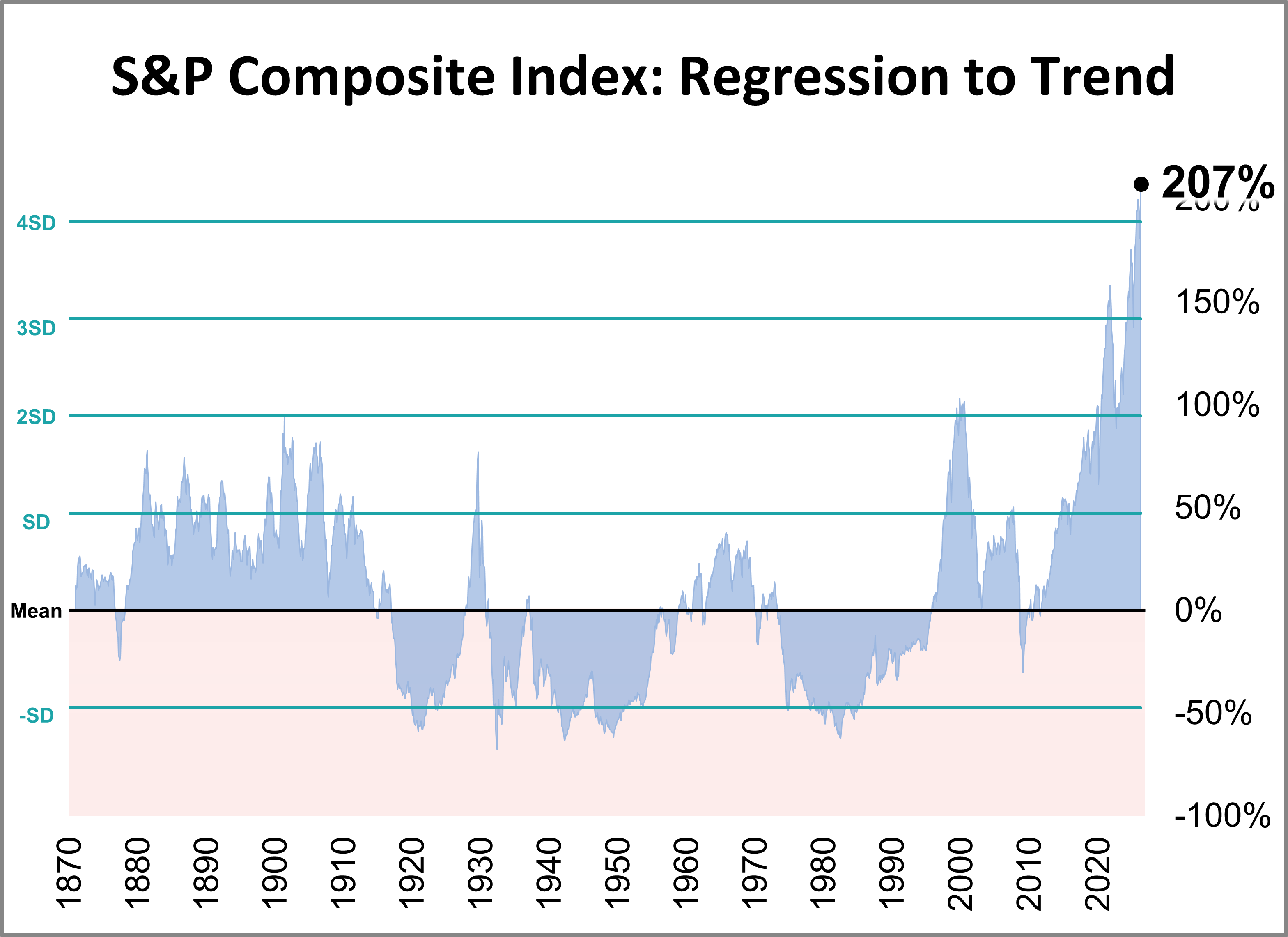

The inflation-adjusted S&P Composite Index was 207% above its long-term trend at the end of May.

Closed-end funds may not be a hot topic right now, but they offer a highly compelling means to solve today's macroeconomic woes.

Last week’s data tracked a shifting economic trajectory over the last several months. While the latest reading on first-quarter GDP confirms the economy started the year with steady growth, subsequent inflation metrics moved higher and ultimately weighed on consumer confidence.

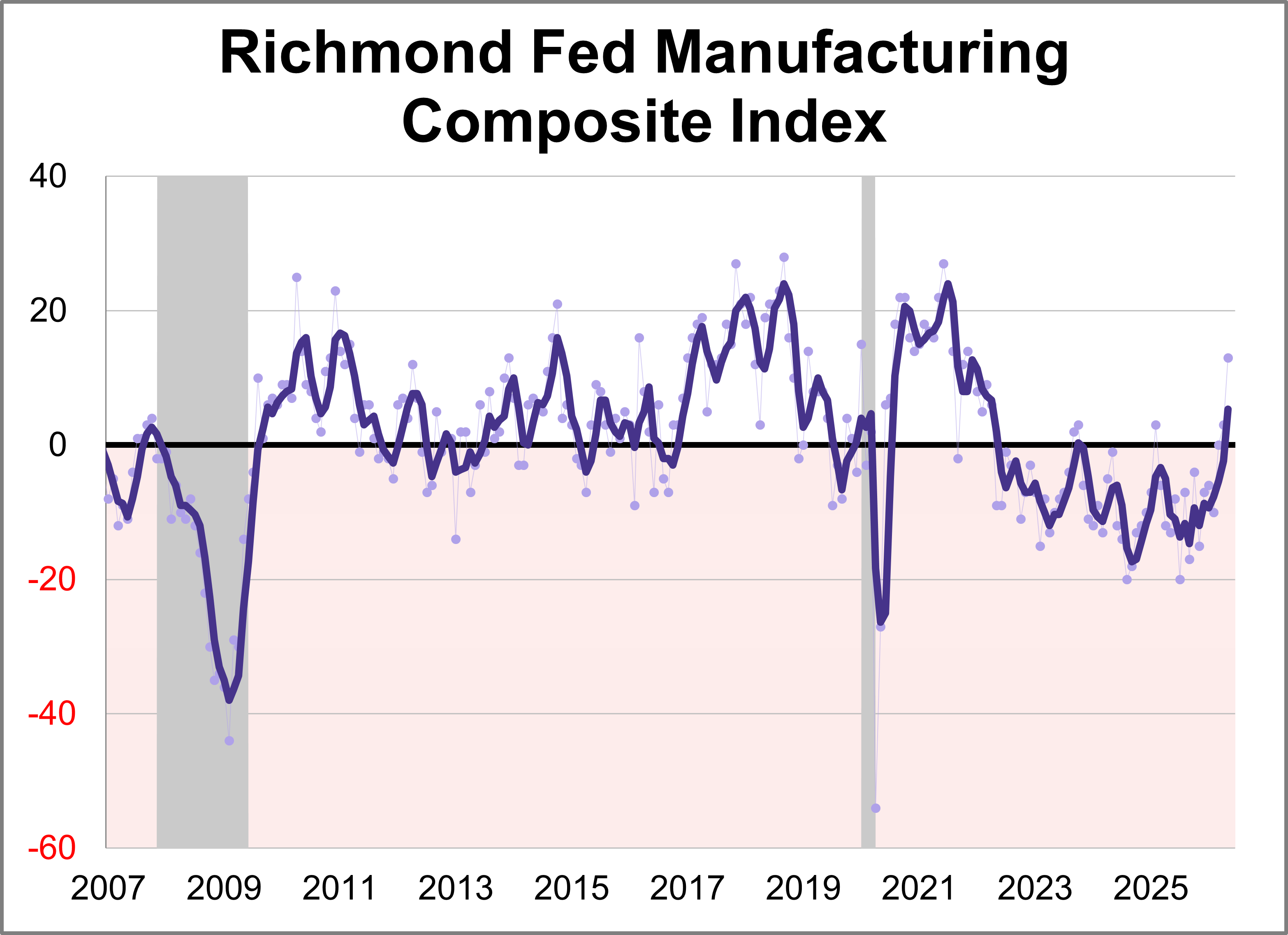

Fifth district manufacturing activity increased in May according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose ten points points to 13, marking the highest level in nearly five years. This month's reading was above the forecast of 4.

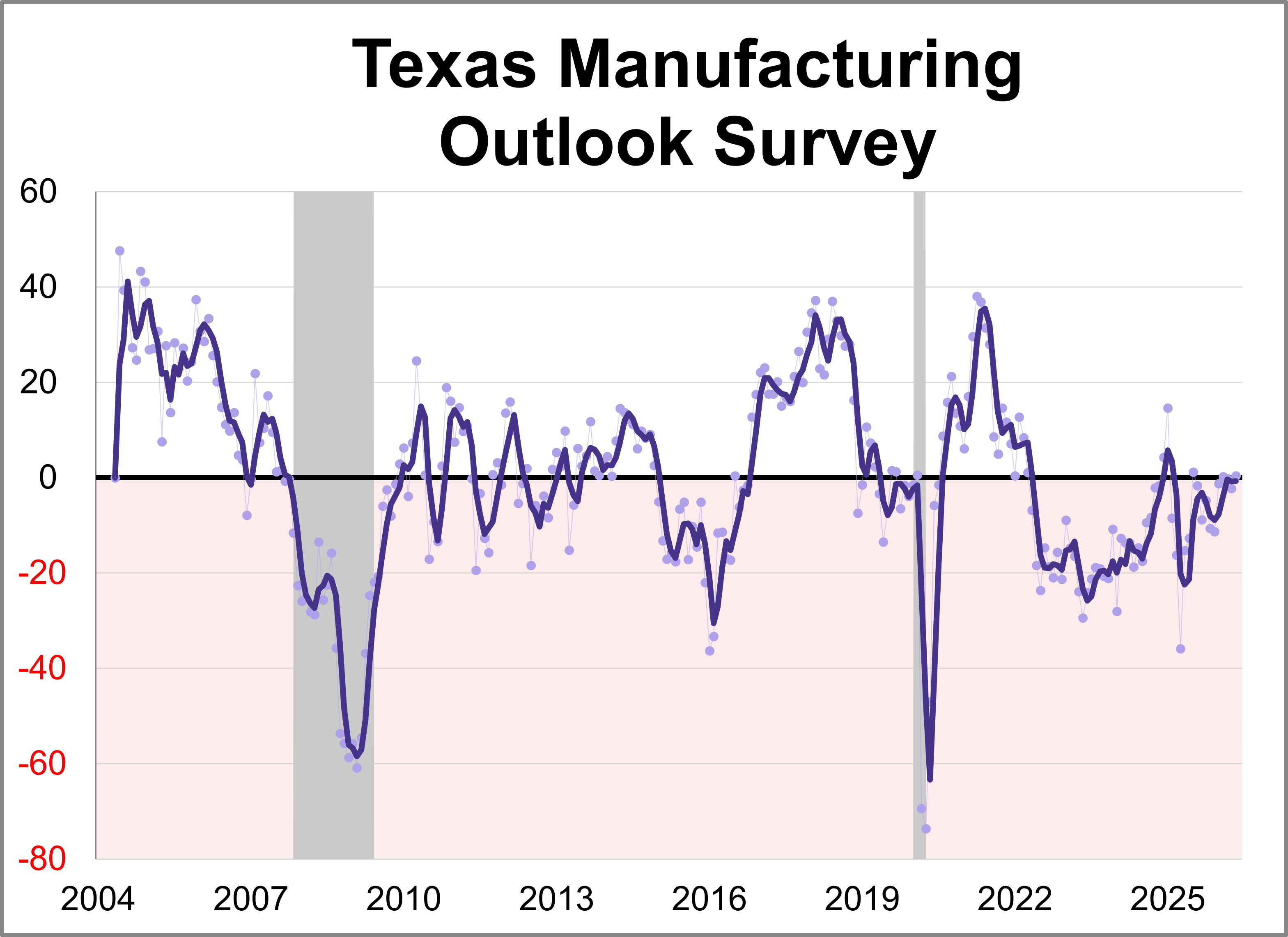

The Dallas Fed released its Texas Manufacturing Outlook Survey (TMOS) for May. The general business activity index rose 2.7 points to 0.4, indicating slower growth of manufacturing activity and stable business conditions perceptions.

There is currently a stark contrast between everyday consumer confidence and financial market behavior. On one hand, persistent inflation and elevated living costs have driven consumer sentiment to historic lows. On the other hand, financial market participants are exhibiting aggressive risk appetite, with margin debt surging to an all-time high record on the heels of major equity market gains.

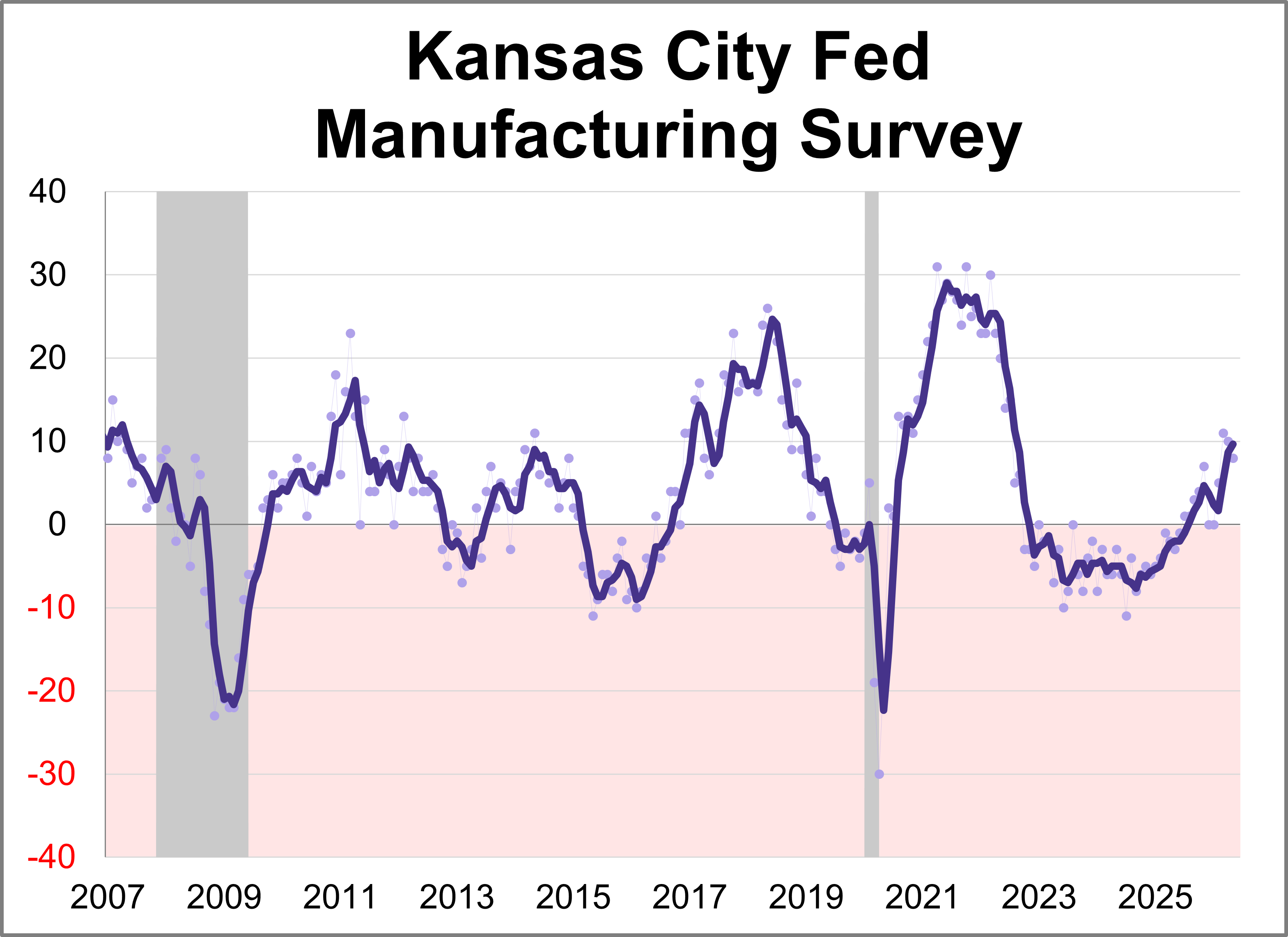

The Kansas City Fed Manufacturing Survey revealed regional activity continued to increase in May. The composite index came in at 8 this month, down slightly from 10 in April but still indicating continued expansion.

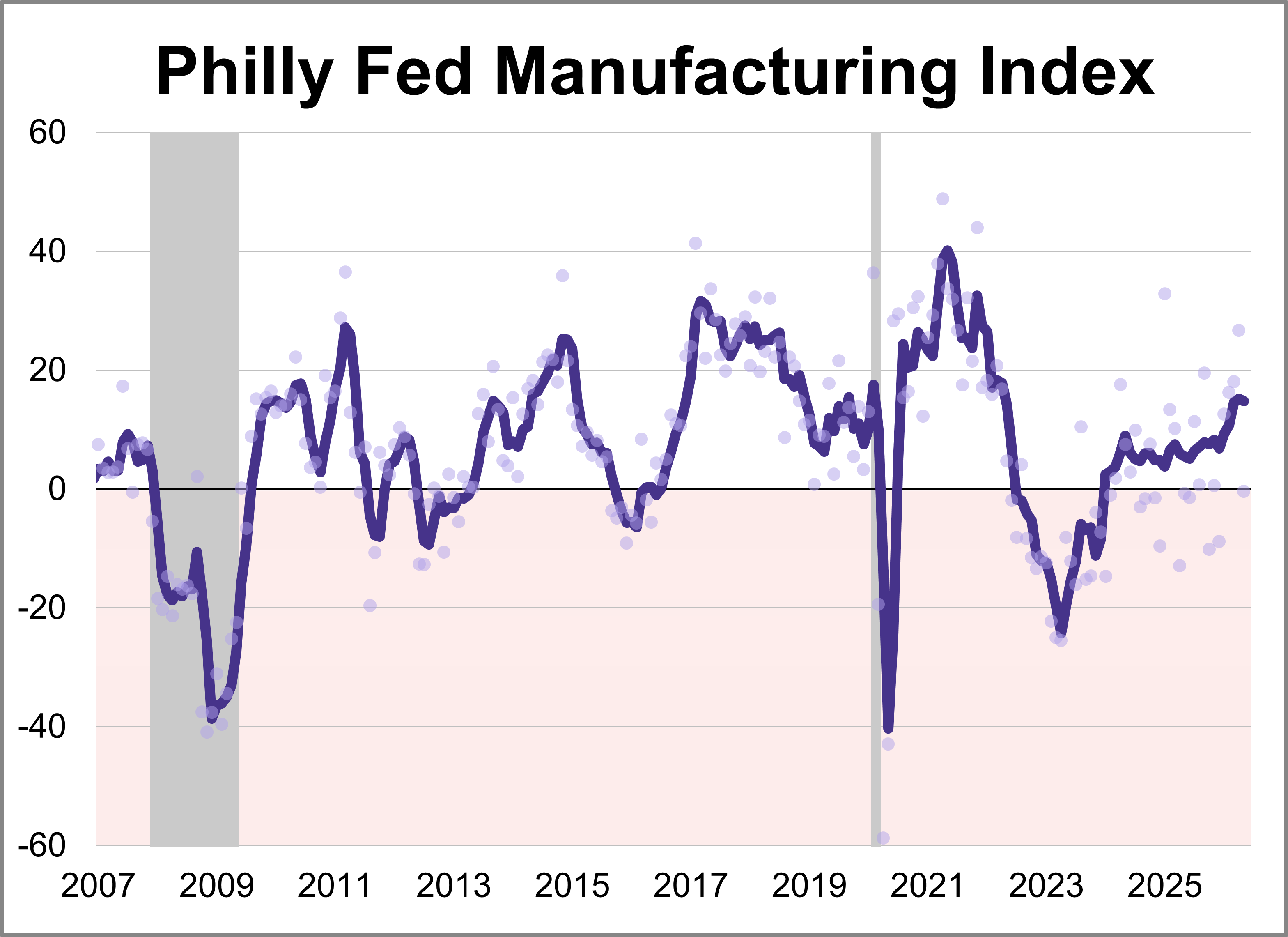

The latest Philadelphia Fed manufacturing index showed activity weakened in May, with the index sinking 27.1 points to -0.4. The latest reading marked the lowest level for the index this year and was worse than the forecast of 17.6.

As inflation lingers and market dynamics shift, advisors are rethinking the 60/40 portfolio with managed futures and options income ETFs.

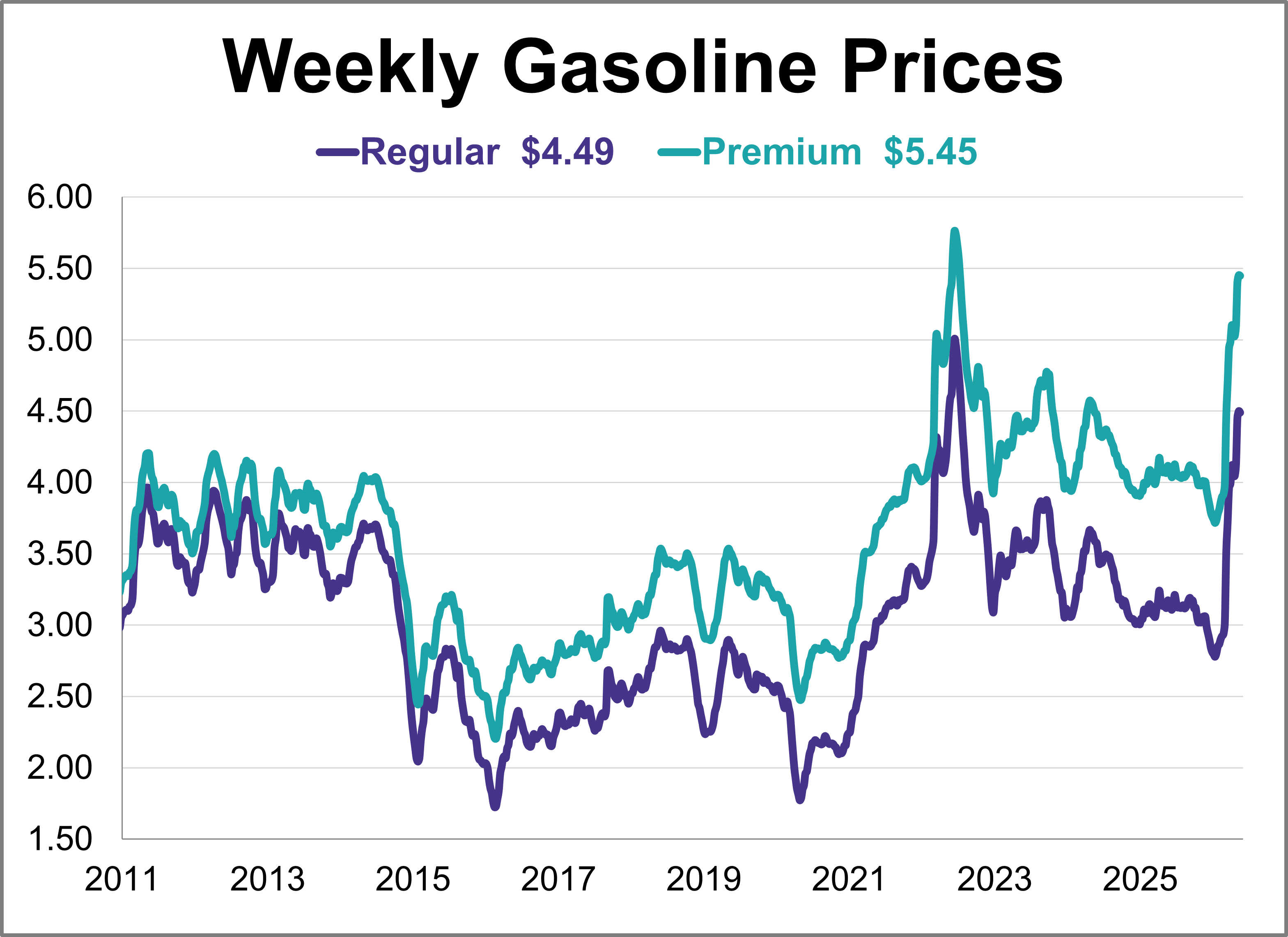

Gas prices were relatively flat this week, remaining at their highest level in nearly four years. As of May 18th, weekly prices were down 1 cent for regular and were unchanged for premium.

The U.S. economic landscape in April was defined by a significant rebound in inflation across both consumer and wholesale sectors, complicating the path for future monetary policy.

Explore how Women in ETFs & CFAOC experts believe AI will supplement, not replace, financial professionals.

Manufacturing activity grew strongly in New York State, according to the Empire State Manufacturing May survey. The diffusion index for General Business Conditions rose 8.6 points to 19.6, its highest level in over four years.

Investors and advisors often seek private equity, but they are frequently thwarted by liquidity and other issues.

Addressing common 529 Savings Plan concerns and how recent legislative updates have broadened the 529 scope.

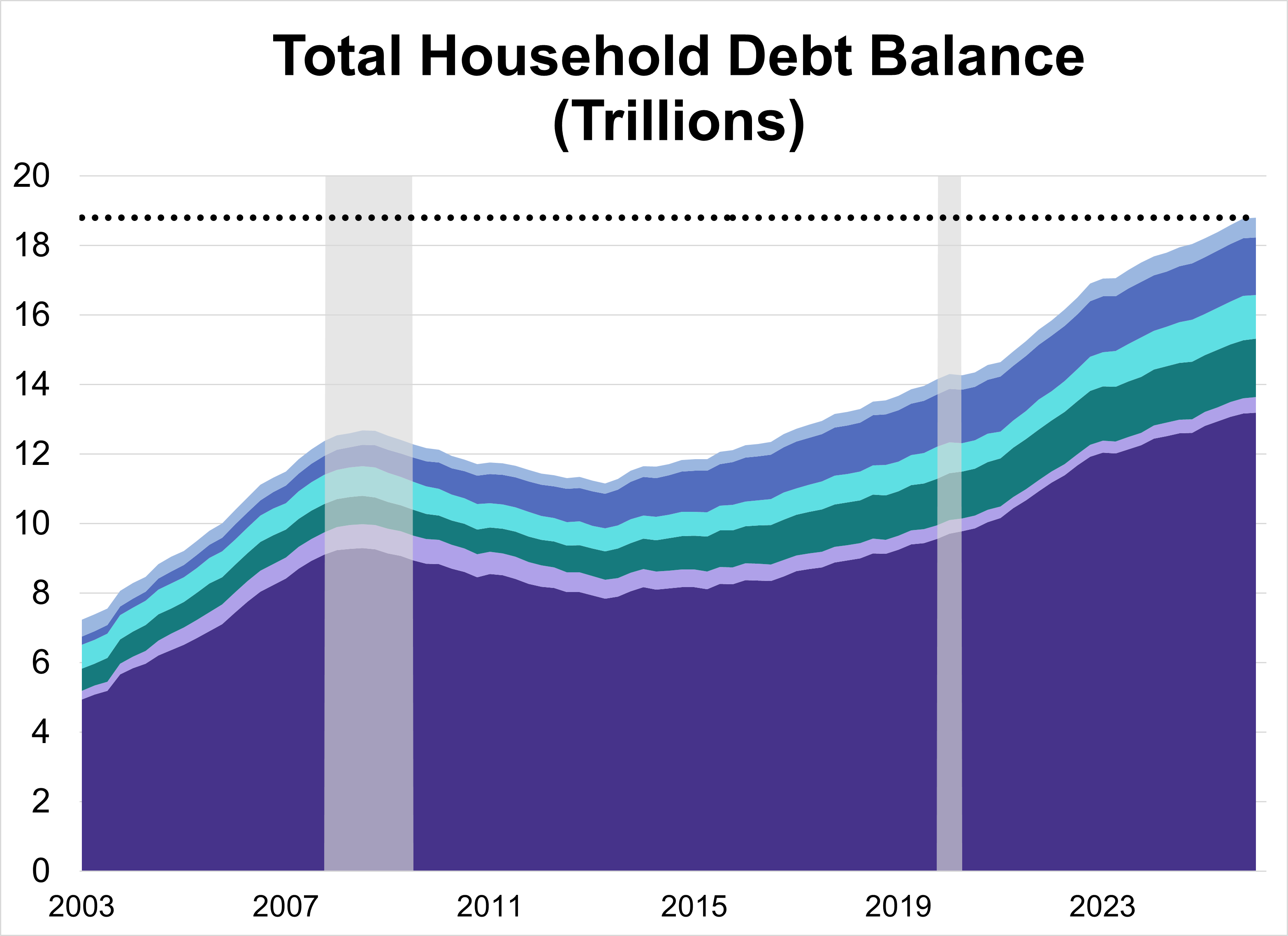

Total U.S. household debt climbed to a record $18.79 trillion in Q1 2026, a modest 0.1% ($18 billion) increase from the previous quarter. The overall rise was driven by increases across a handful of categories, specifically mortgage and auto loan balances.

Munis may have struggled a bit in March, but the long-term environment for these bonds remains full of potential.

Explore the new 529 rules, including Roth IRA rollovers, the grandparent loophole, and higher K-12 limits.

The U.S. labor market demonstrated remarkable endurance in April, with job gains outpacing expectations and private sector expansion reaching its strongest point in over a year. As the Federal Reserve maintains a steady interest rate policy, the focus now turns to upcoming inflation and retail data to gauge the sustainability of this momentum.