Key takeaways

-

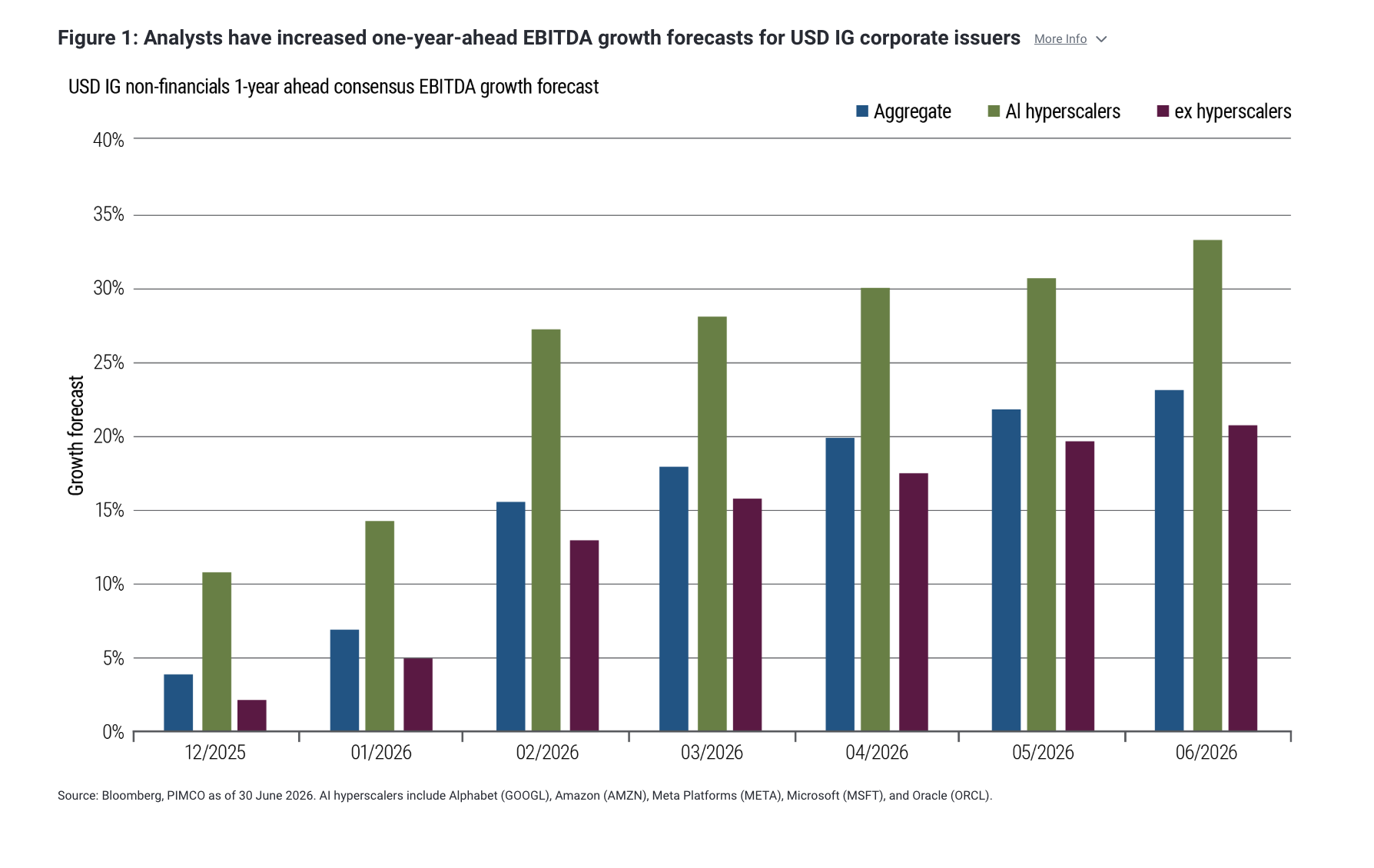

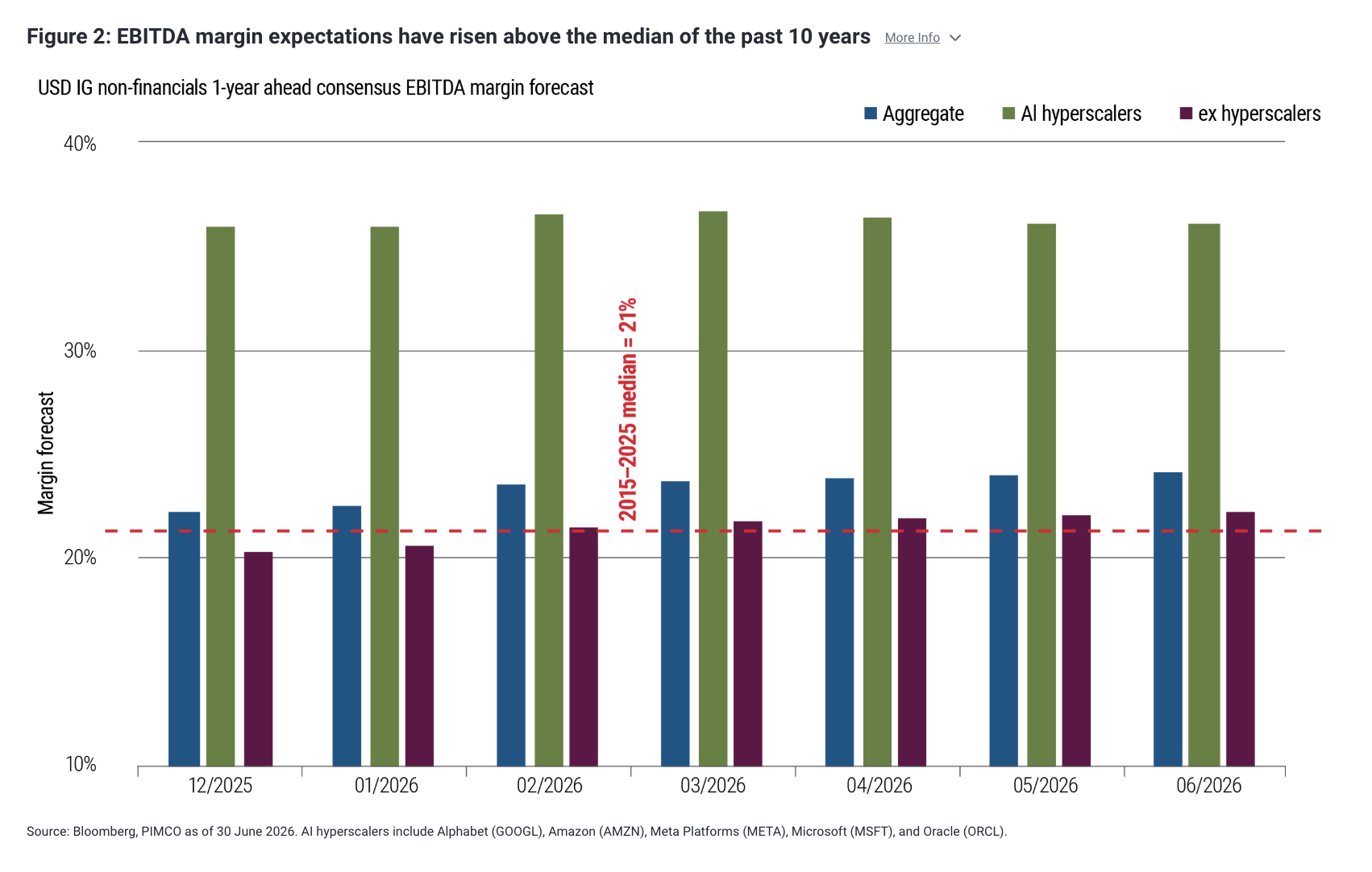

The bar has moved higher into earnings season. Since late January, analysts have quadrupled their one-year earnings growth forecasts for non-financial bond issuers in the U.S. dollar (USD) investment grade (IG) market, while margin expectations have climbed above the 2015–2025 median of 21%.

-

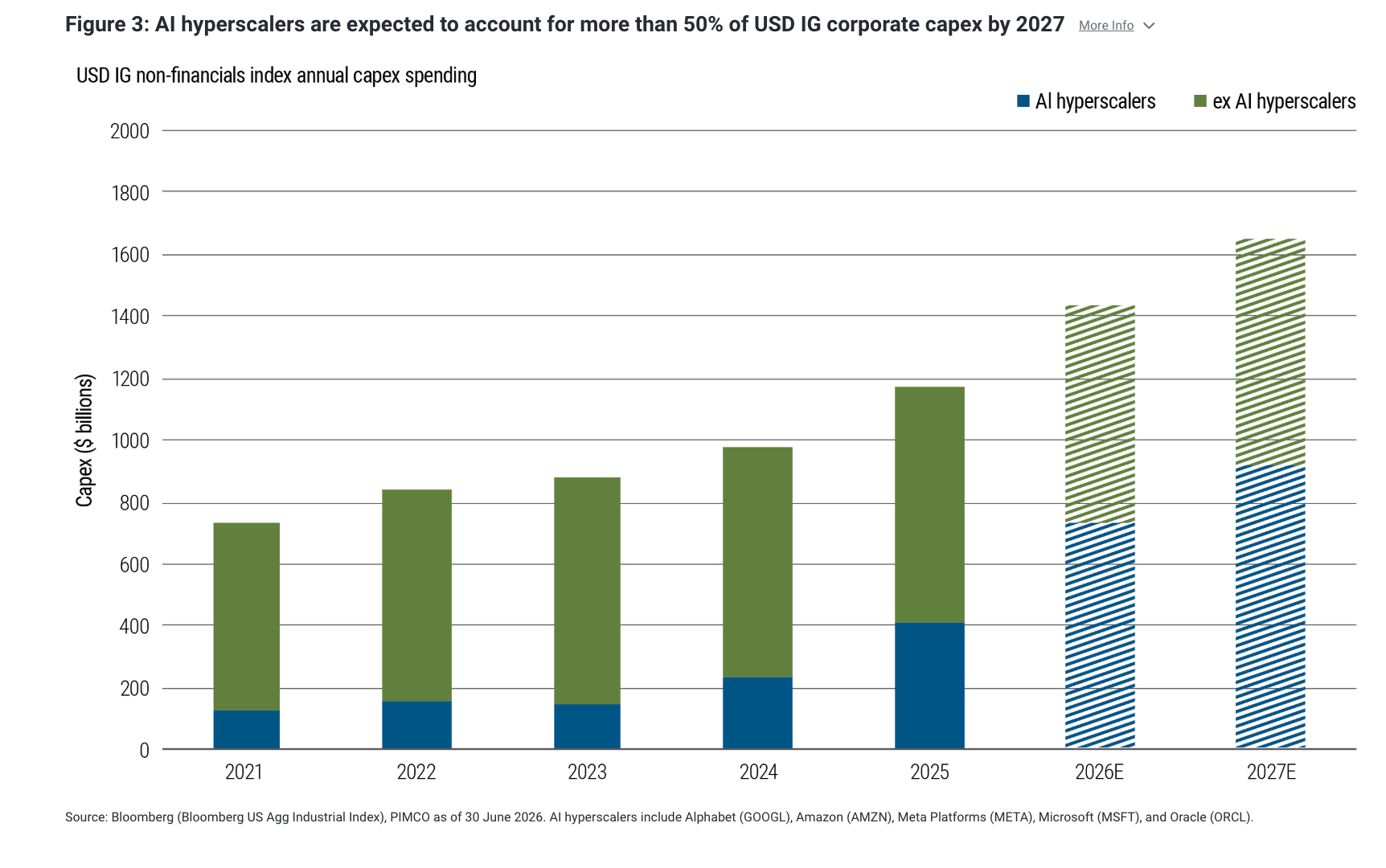

AI hyperscalers are the swing factor. Alphabet, Amazon, Meta, Microsoft, and Oracle also made up roughly one-third of capital expenditure in 2025 and are expected to reach 54% by 2027 – driving the entirety of expected capex growth in that time and making forward capex guidance the key signal to watch.

-

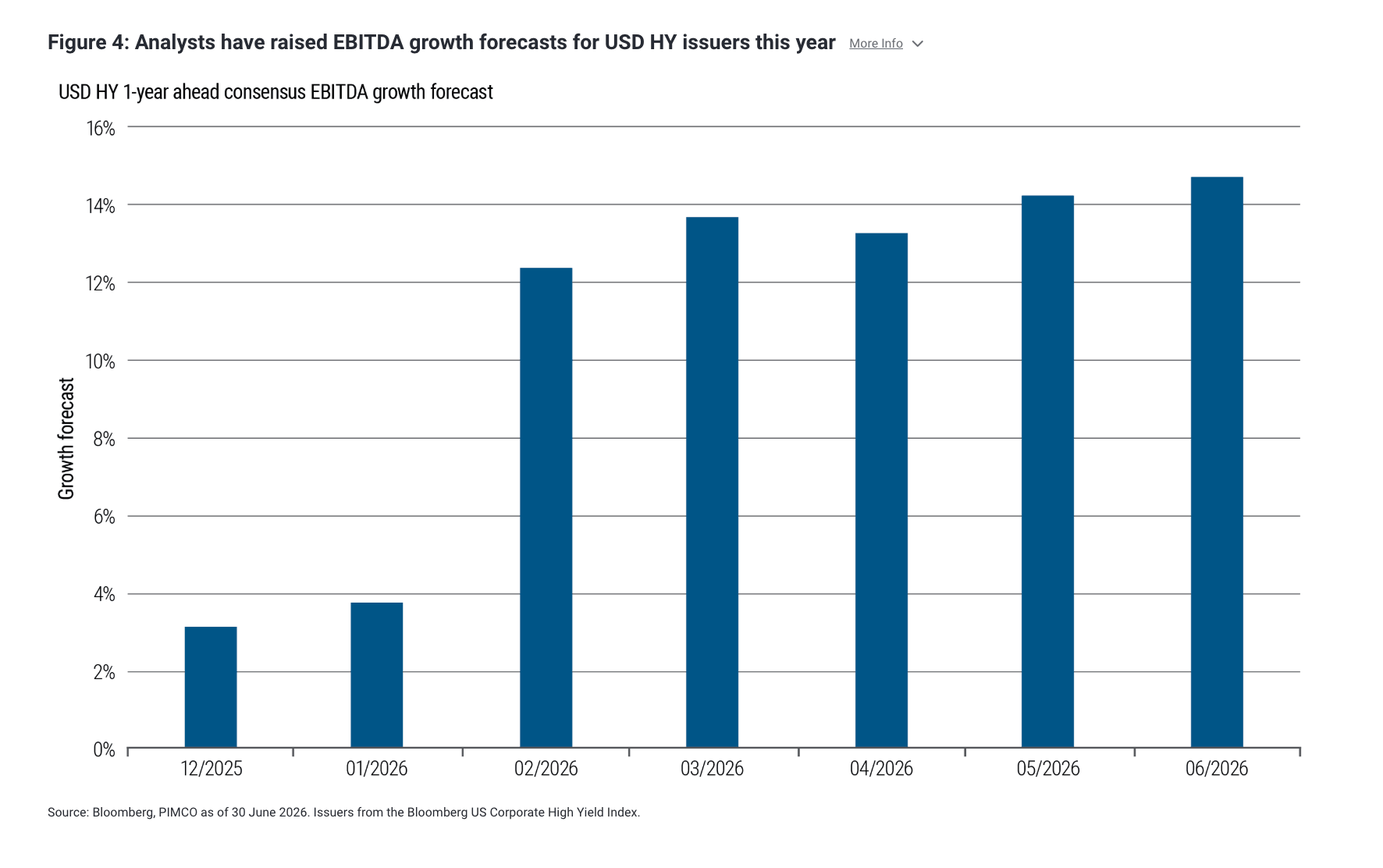

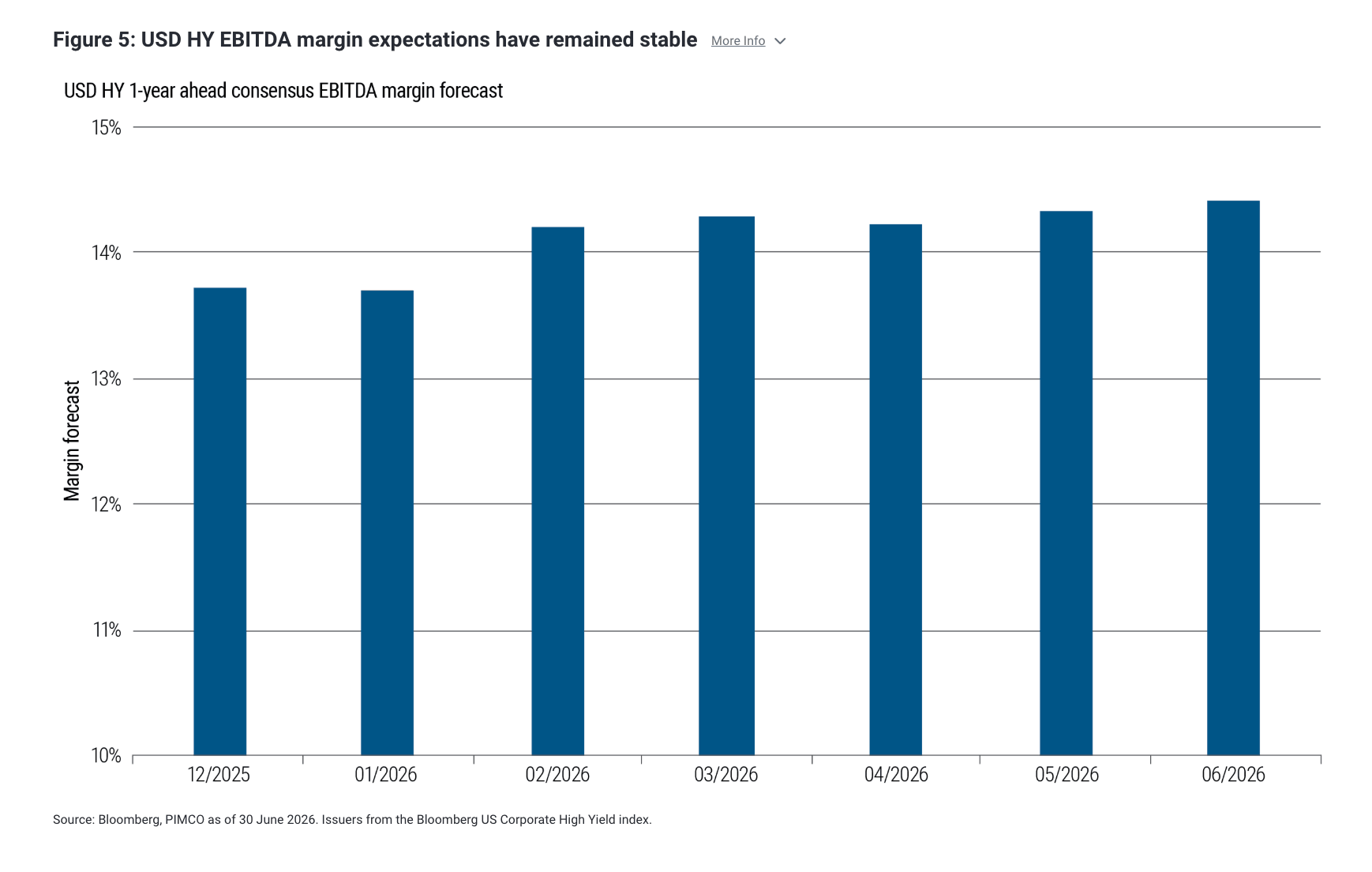

High yield is being re-rated higher too, but with little cushion. Consensus one-year EBITDA growth forecasts for borrowers in the USD high yield market have also risen from under 4% in January to more than 14% by end-June, with margins stable – a nod to U.S. economic resilience so far, but a setup that leaves little room for disappointment.

Since the start of the year, the market has become more optimistic on the earnings outlook for U.S. dollar (USD) investment grade (IG) corporate issuers, shrugging off the Iran conflict and consistently revising earnings forecasts higher (see Figure 1). The first wave of upgrades came after the AI hyperscalers reported, by and large, strong earnings. But most of the improvement has stemmed from the rest of the non-financials index, with analysts quadrupling their one-year aggregate EBITDA (earnings before interest, taxes, depreciation, and amortization) growth expectations, from 5% at the end of January to more than 20% as of 30 June.

And despite modest fears of an inflationary shock that would eat away at margins, the market has so far believed these fears to be unwarranted; aggregate margin expectations for USD IG corporates have improved from 20% to 24% since the start of year, above the 2015-2025 median of 21% (see Figure 2).

Aside from earnings, company forward guidance vis-à-vis capital expenditure plans will remain a key focus, particularly for the hyperscalers. As of 2025, these five firms accounted for around one-third of aggregate USD IG corporate capex. Although current-year capital plans are already largely set, the focus will be on additional insight into 2027 and beyond, with current forecasts for hyperscalers to account for 54% of total capex by 2027, or $915 billion (see Figure 3). In fact, relative to 2025 levels, the entirety of the expected expansion in USD IG corporate capex has been driven solely by the five hyperscalers.

See more: Wars, Markets and Economic Growth

A second-order effect related to capex is that it directly feeds into future earnings expectations; the underlying revenues are recognized as they arise by the “pick and shovel” parts of the AI ecosystem, while the expenses are capitalized for the hyperscalers, thus won’t ultimately be included in EBITDA figures.

The same earnings optimism can be seen across USD high yield (HY) issuers as well. Figure 4 shows that since the end of January, analyst expectations for aggregate EBITDA growth have climbed from just under 4% to more than 14% as of the end of June, with expected EBITDA margins relatively stable (see Figure 5).

To be clear, this universe of index firms is held constant, as of December 2025, and thus isn’t driven by any compositional effects year-to-date, such as fallen angels (IG issuers downgraded to HY), which would typically have higher EBITDA than the average HY firm given their size. Thus, it is more of a reminder of the resiliency of the U.S. economy so far, despite signs of a deeper K-shaped economic divide (for more, see the 13 April “The Credit Market Lens: Oil Supply Shocks Don’t Age Well”).

Of course, as we enter earnings season in earnest over the coming weeks, time will tell whether the optimism reflected in analyst expectations is warranted for these USD IG and HY issuers.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Past performance is not a guarantee or a reliable indicator of future results. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice. There is no guarantee that results will be achieved.

All Investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0710-5738390

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO