Key takeaways:

-

High yield bonds show resilience. They appear more stable than direct lending and leveraged loans versus recent history – reflecting stronger underwriting discipline, a greater share of BB rated issues, lower duration, and less exposure to the software sector, where AI is raising fundamental questions.

-

Distress in direct lending and leveraged loans is likely to rise. Even if the macro backdrop remains stable, these markets face stress driven by the uneven pass-through of higher rates to floating-rate borrowers, a post-COVID fundraising cycle that weakened underwriting discipline, and heavy sponsor concentration in software.

-

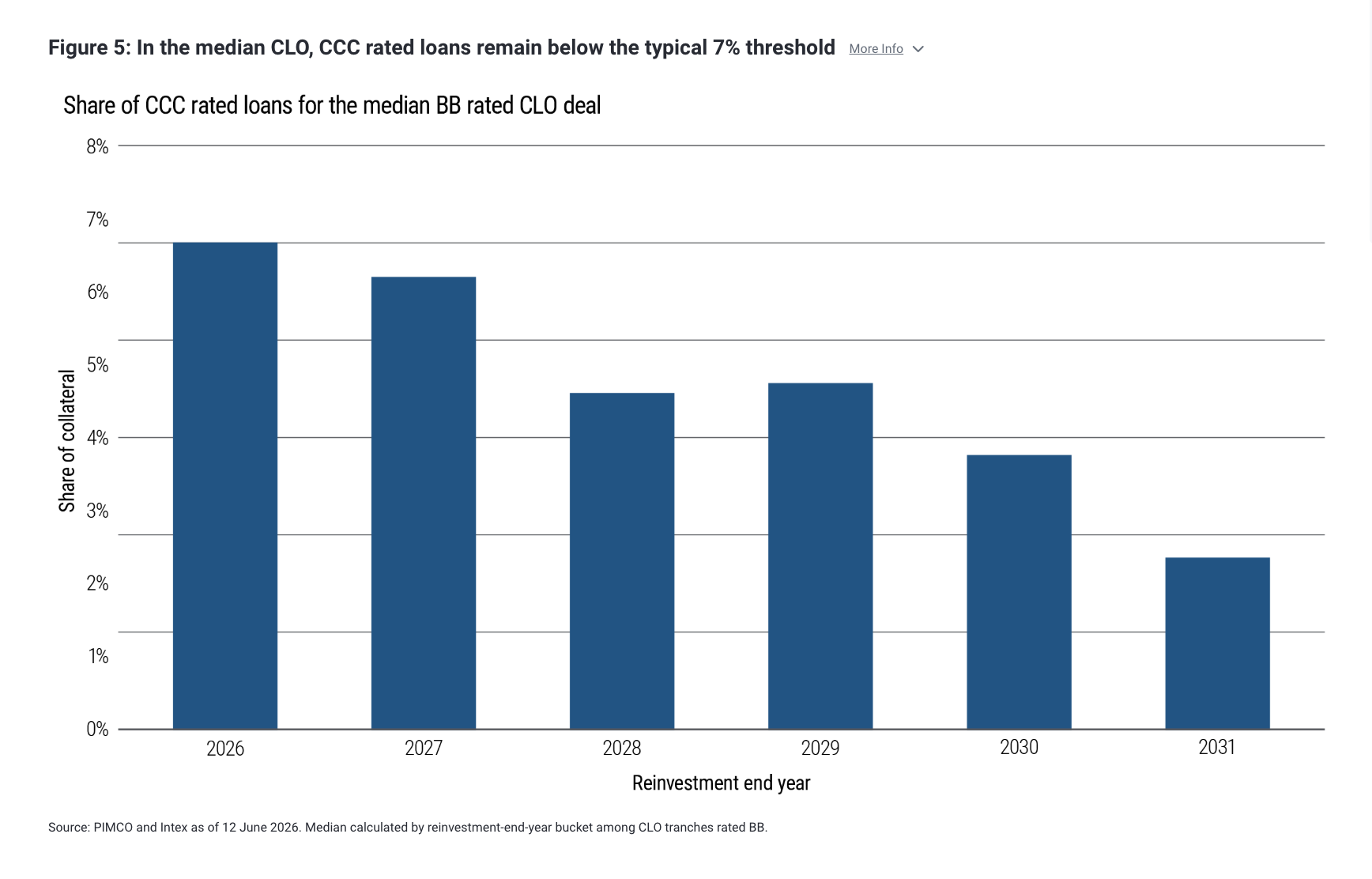

CLOs face pressures from a rising share of underlying CCC rated loans. In collateralized loan obligations (CLOs), stress is building beneath the surface - not through defaults, but through marks. For median CLOs, CCC buckets are near the 7% threshold for deals approaching the end of their reinvestment periods.

In June, a healthcare software company announced an amend-and-extend transaction to push its previously agreed 2027 loan maturity further into the future – the first leveraged loan software issuer to do so this year. The transaction is unlikely to prove idiosyncratic and may instead mark a broader shift: Financial distress is likely to rise in direct lending and leveraged loans, even if the business cycle remains resilient.

This kind of distress is usually cyclical, surfacing when earnings weaken and financial conditions tighten. As discussed in PIMCO’s Secular Outlook, “Rupture and Resilience,” the emergence of credit market stress alongside stable growth and a resilient economic environment points to internal pressures rather than macro fundamentals.

Divergent paths in leveraged finance markets: Loan markets under strain

Three forces help explain the stresses in loan markets amid a more broadly benign macro backdrop:

-

Higher rates continue to flow through unevenly across capital structures. The roughly 500 basis points (bps) of Federal Reserve rate tightening delivered between March 2022 and July 2023 has weighed heavily on direct lending and leveraged loans, where floating-rate exposure has driven a sharp increase in interest burdens. That has eroded interest coverage even without a growth slowdown. By contrast, high yield issuers – which are predominantly fixed-rate – have been partially insulated, delaying the transmission of tighter financial conditions.

-

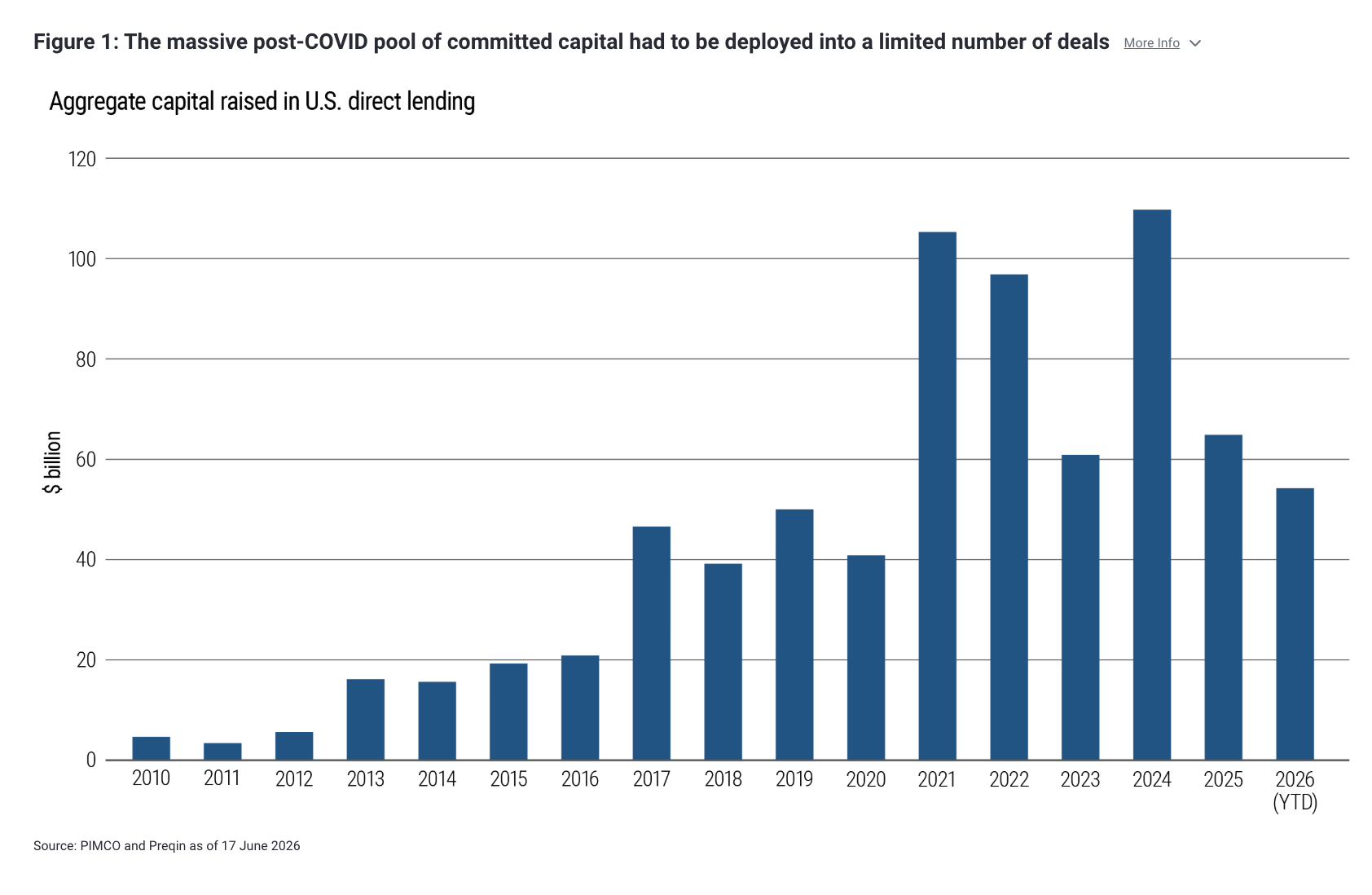

Direct lending is dealing with a growth hangover. The post-COVID fundraising cycle left a massive pool of committed capital to be deployed into a constrained opportunity set (see Figure 1). Excess capital chasing limited deals predictably weakened underwriting: looser covenants, aggressive EBITDA (earnings before interest, taxes, depreciation, and amortization) add-backs, permissive documentation, deferred coupons, larger deal sizes, and greater portfolio overlap across managers. In short, competition eroded many of the protections meant to compensate for leverage and illiquidity.

-

Software will likely amplify these vulnerabilities. Sponsor capital in direct lending and broadly syndicated loans has been heavily concentrated in the software sector for understandable reasons: recurring revenue, high margins, and predictable cash flows that supported elevated leverage and valuation multiples. But AI disruption has started to challenge the math behind many software leveraged buyouts (LBOs), raising questions about pricing power, customer retention, and margin durability. Software has therefore become not only the largest sector in both leveraged loans and direct lending (according to PitchBook), but also a key transmission channel for stress.

Read more: Muhlenkamp Quarterly Market Commentary – July 2026

Relative strength and stability in high yield bonds

If the macro cycle remains intact, the important distinction is between markets where excess capital has weakened underwriting and those where fundamentals have improved. In our view, the high yield (HY) bond market stands out: It looks stronger than its own history, stronger than leveraged loans and direct lending, and less exposed to the supply-demand imbalances that have built up elsewhere in leveraged finance.

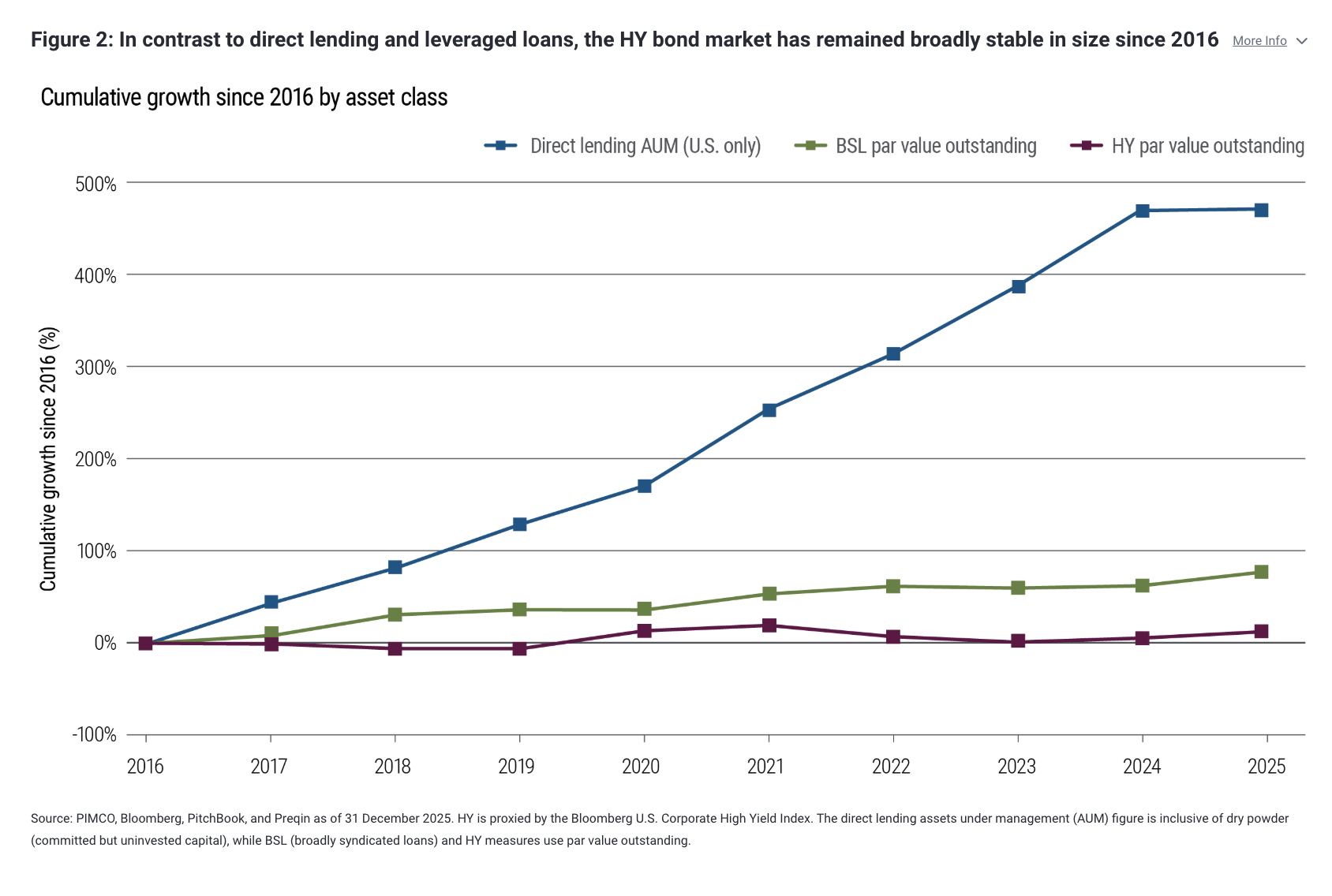

That relative strength is visible across several dimensions. The HY market has remained broadly stable in size since 2016, while leveraged loans have grown by roughly 70% and direct lending has expanded severalfold, reflecting sustained inflows into private credit (see Figure 2).

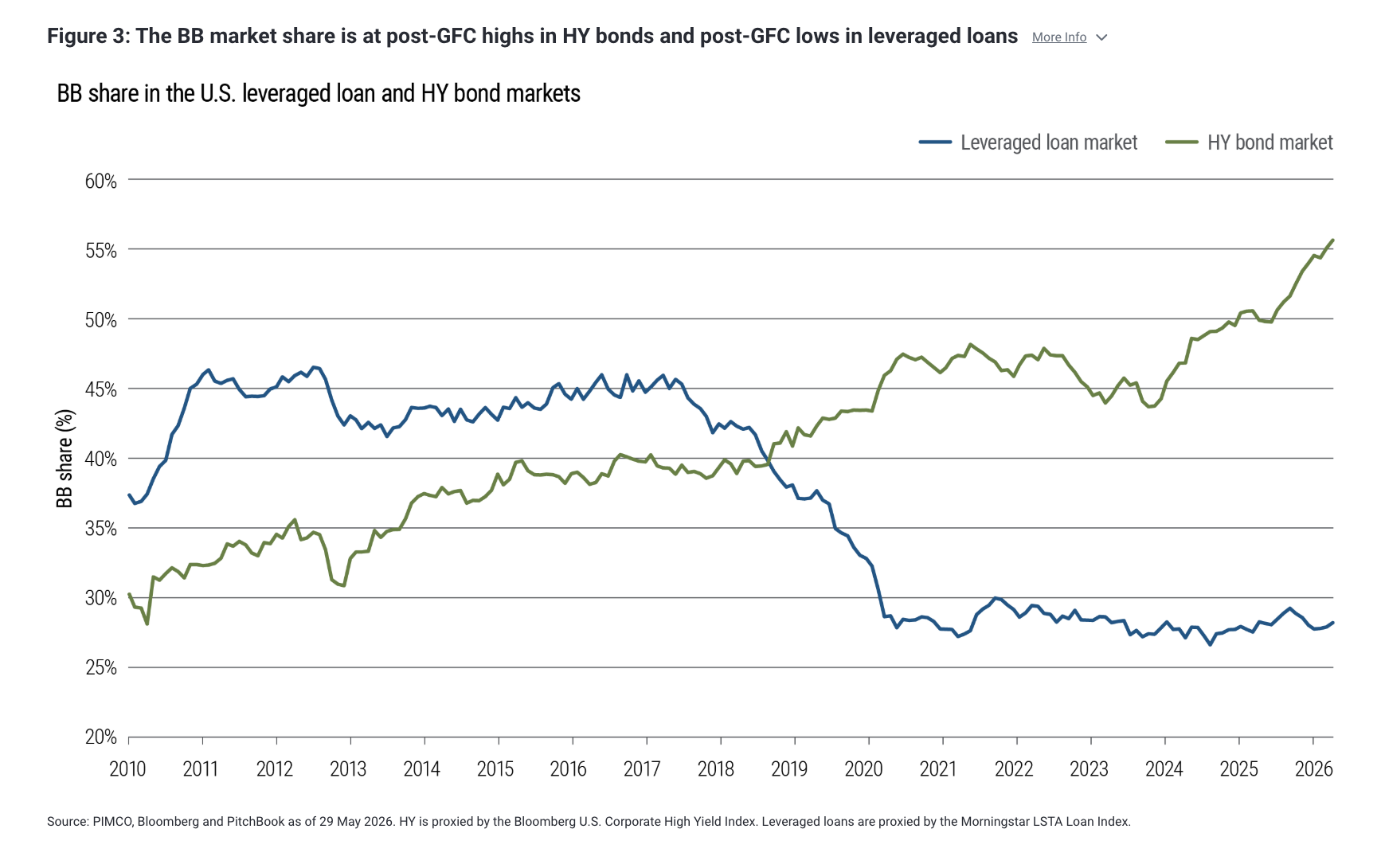

Overall HY credit quality has also improved: As shown in Figure 3, the share of BB rated bonds has risen to a record 54%, up from 30% in 2010, while the BB share in loans has fallen to 28%, down from a peak of 45% in the wake of the global financial crisis (GFC). This partly reflects issuer composition as well as the growth of secured issuance in the bond market, which now approaches 40% of the HY universe (as represented by the Bloomberg U.S. Corporate High Yield Index).

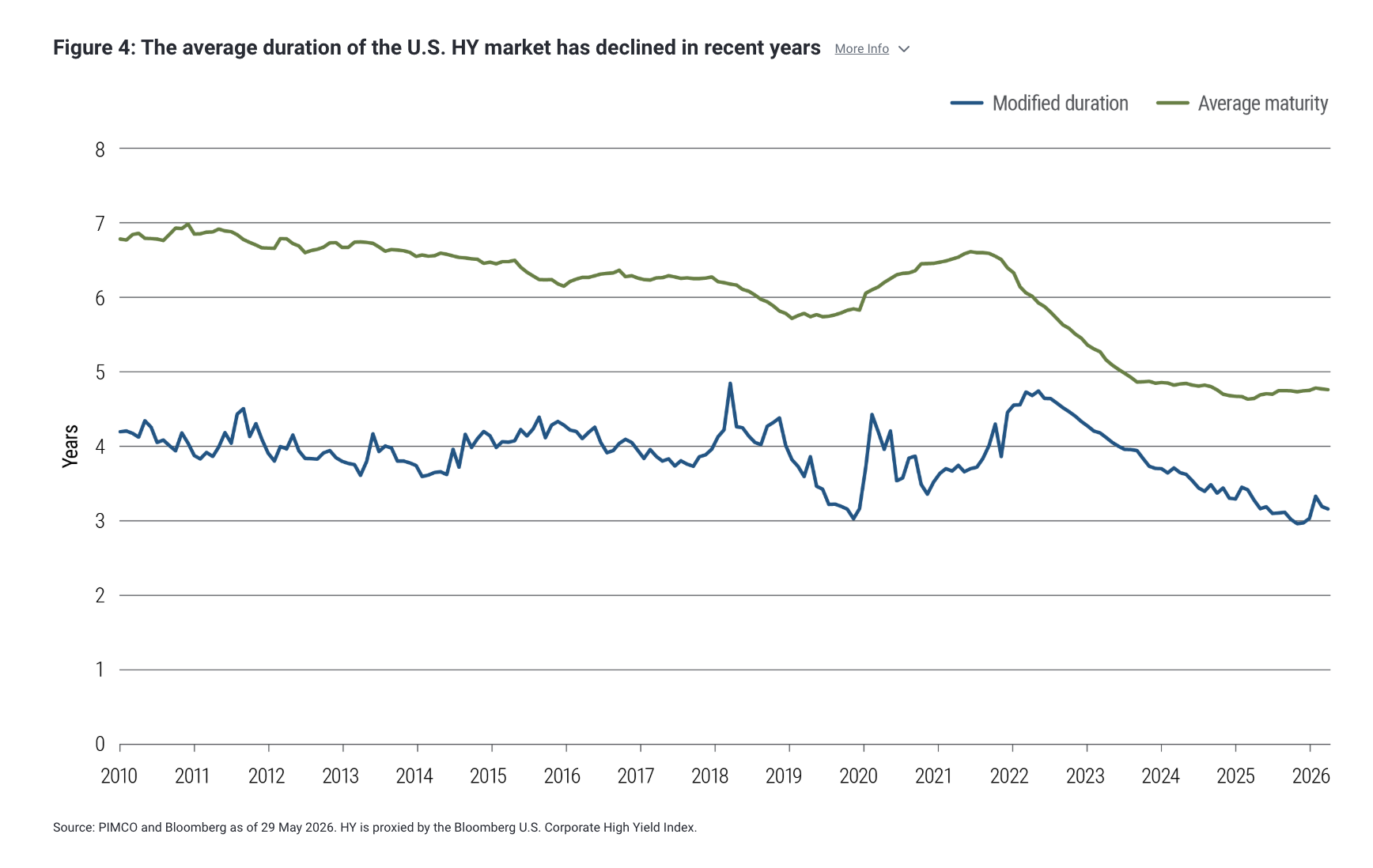

Average duration in HY markets has also declined, driven by post-2022 repricing and a shift toward shorter maturities. This helps reduce sensitivity to rate volatility and lowers overall risk (see Figure 4).

BB CLOs: Marks don’t need downgrades to hurt

The valuation reset that swept through software earlier this year remains largely unchanged, suggesting investors are still in “show me” mode and want evidence that AI will expand the industry profit pool rather than reshuffle it.

So far, the broader leveraged loan market has contained the damage despite software’s meaningful index weight. But the vulnerability lies beneath the surface. Much of the software loan universe is rated B−, leaving it exposed to downgrades if operating performance surprises materially to the downside. A migration into CCC territory would matter not only for software loans, but also for the broader collateralized loan obligation (CLO) ecosystem, where rating constraints could amplify dispersion.

The most widely watched metric – the share of CCC rated loans – remains below the typical 7% threshold in most deals, though it is close for deals nearing the end of their reinvestment periods (see Figure 5).

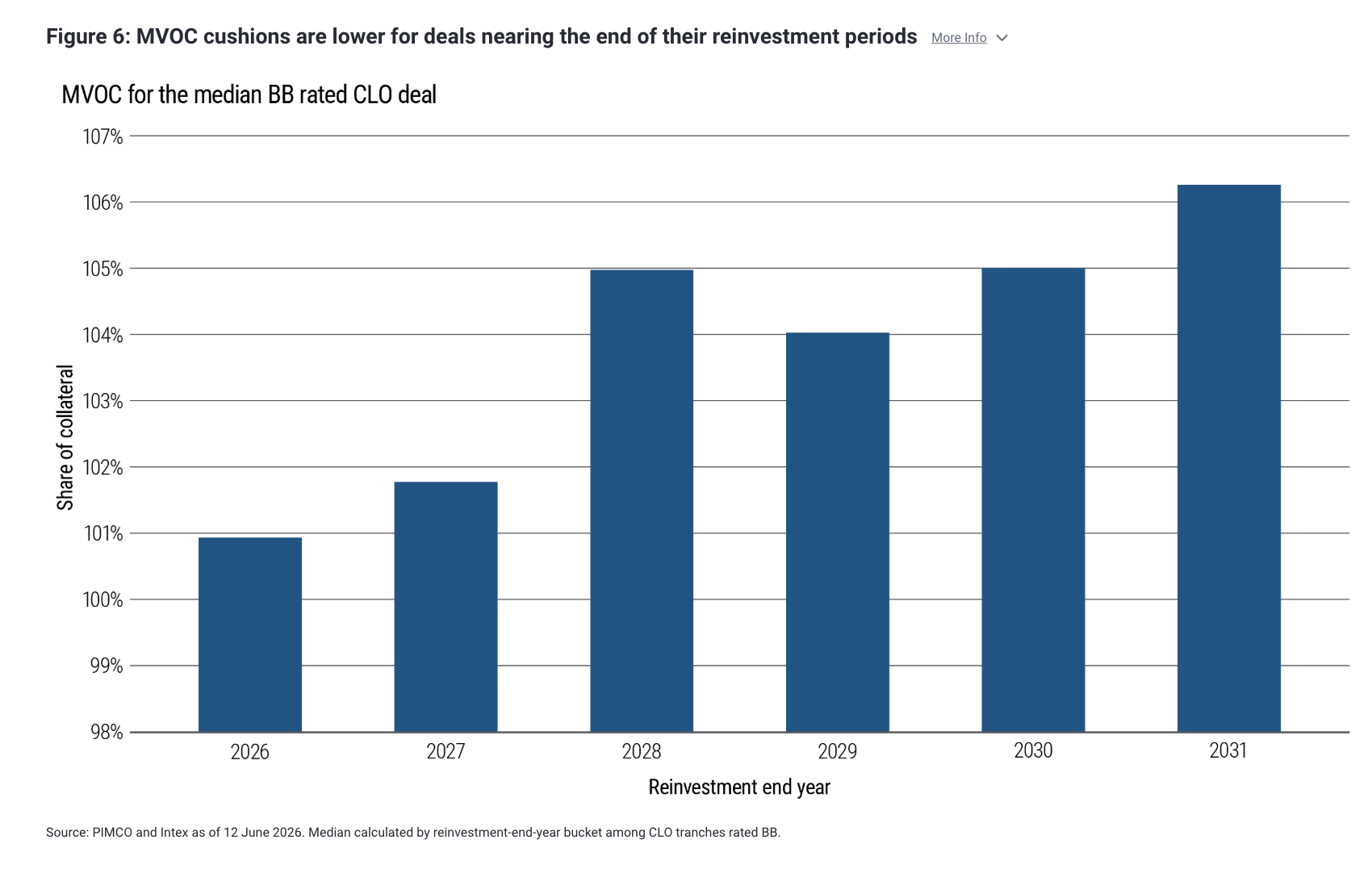

Within the CLO market, market value overcollateralization (MVOC), which measures the market value of the collateral pool relative to the par amount of a given tranche plus all tranches senior to it, is also flashing yellow for deals nearing the end of their reinvestment periods (see Figure 6).

This matters because once collateral values no longer fully cover liabilities higher up the capital structure, the system becomes more sensitive to further price declines. As reinvestment periods expire, managers also lose flexibility to rotate out of weakening credits.

A wave of software downgrades could therefore create pressure beyond the sector itself – not necessarily through realized defaults, but through weaker marks and reduced structural protection.

At the index level, this supports a continued preference for HY bonds over leveraged loans. It also means relative value between the two markets should not be framed simply as a carry-versus-duration trade-off. Duration can be hedged; structural credit deterioration is harder to offset.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

All Investments contain risk and may lose value. Investments in asset-based finance or asset-based lending is subject to a variety of risks including, but not limited to, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Investments in residential/commercial mortgage loans and commercial real estate debt are subject to risks that include prepayment, delinquency, foreclosure, risks of loss, servicing risks and adverse regulatory developments, which risks may be heightened in the case of non-performing loans. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while U.S. agency MBS are generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Collateralized Mortgage Obligations (CMOs) may involve a high degree of risk and are exposed to risks such as credit, default, market, interest rate, prepayment and extension, and certain classes or series may have more or less volatility depending upon the predictability of cash flow for such class or series. Investors may lose some or all of the investment and there may be periods where no cash flow distributions are received.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

It is not possible to invest directly in an unmanaged index.

©2026 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0702-5715562

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO