Employment Data Confirms Economy is Slowing

Membership required

Membership is now required to use this feature. To learn more:

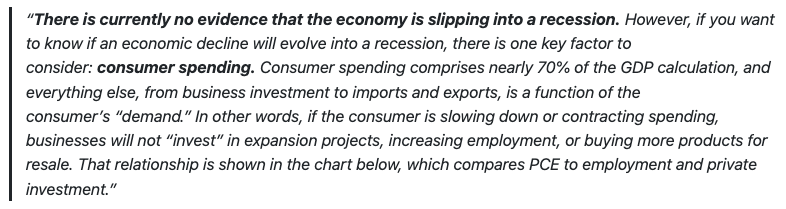

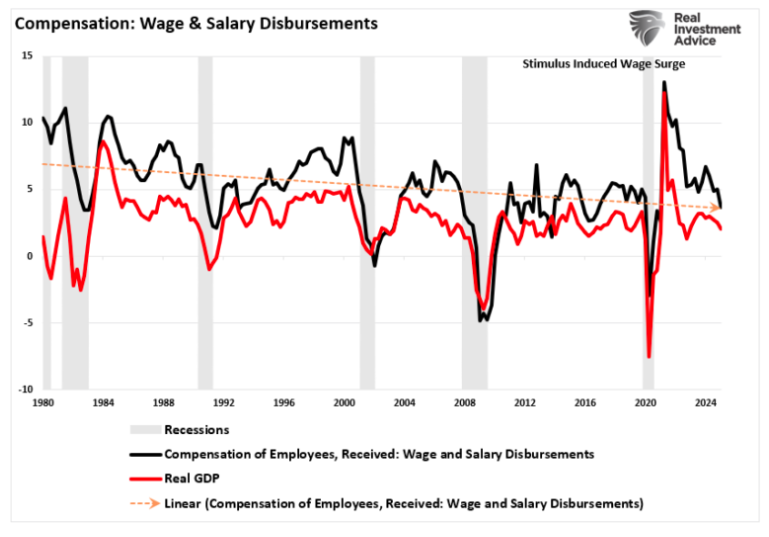

View Membership BenefitsWhile coming in much stronger than expected, the latest employment data confirmed what we already suspected: the economy is slowing. The reason the employment data is so important is that without employment growth, the economy stalls. It takes, on average, about 200,000 jobs each month to keep up with population growth, which ultimately keeps the economy growing. That is because, as discussed in last week’s #BullBearReport, the consumer comprises about 70% of economic growth. To wit:

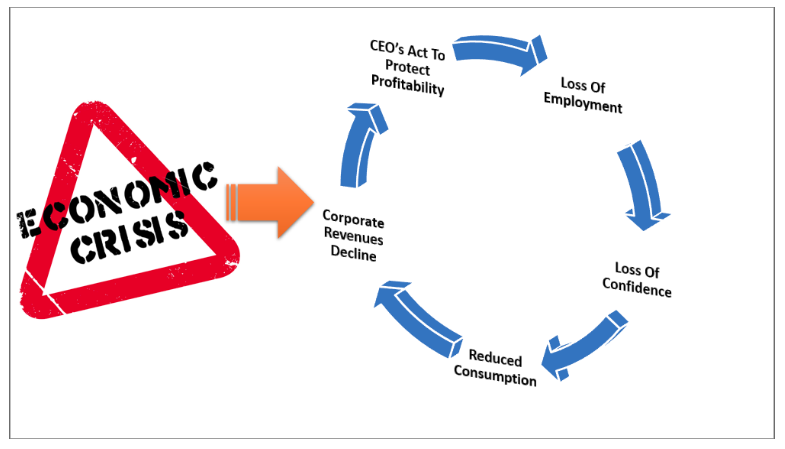

However, most crucially, consumers can not consume without producing something first. Production must come first to generate the income needed for that consumption. The cycle is displayed below.

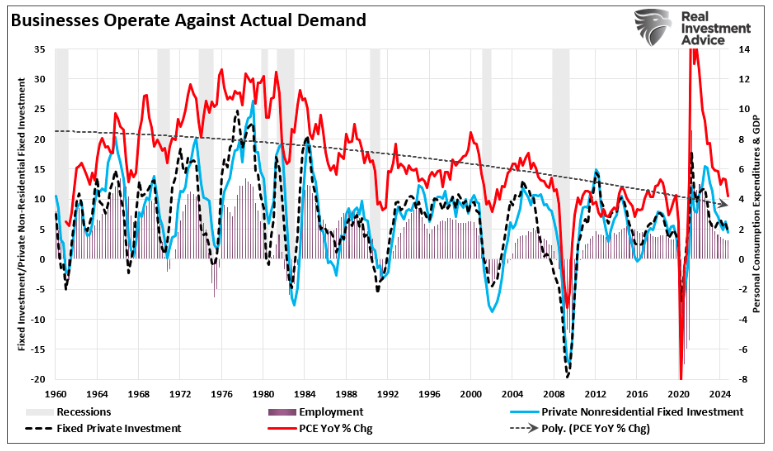

Here is the most critical point. Not all jobs are equal.

While the media touts the ‘strong employment reports,’ such is mostly the recovery of jobs lost during the economic shutdown. However, the reality is that the full-time employment rate is falling sharply. Historically, when the rate of change in full-time employment dropped below zero, the economy entered a recession.

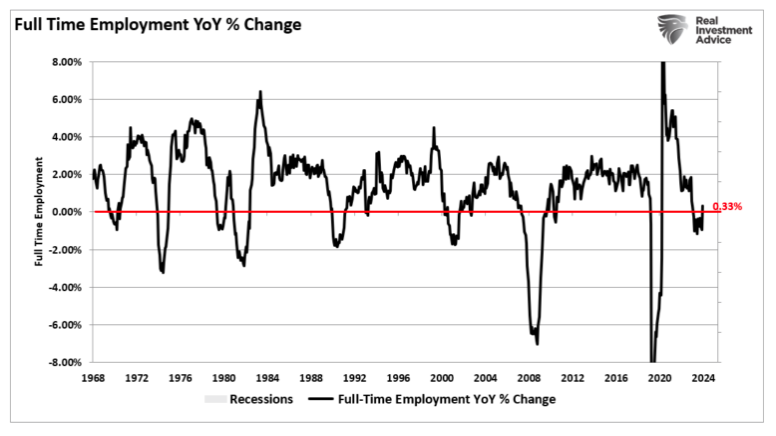

Notably, given the surge in immigration into the U.S. over the last few years, the all-important ratio of those employed full-time relative to the population has dropped sharply. As noted, given that full-time employment provides the resources for excess consumption, that ratio should increase for the economy to continue growing strongly. However, full-time employment has decreased since the turn of the century as automation, technology, and offshoring have risen. While President Biden recently touted strong employment growth in his SOTU address, full-time employment as a percentage of the working-age population failed to recover to pre-pandemic levels.

Notably, sharp downturns in full-time employment have been coincident with recessionary onsets.

No Recession, But Slower Growth Coming

The latest employment data put to rest recession concerns, at least for now. Employment growth remains strong enough to support economic growth and quell concerns that CEOs are withdrawing from the job creation process. However, compensation continues to decline as economic demand slows.

As is always the case, as the economy slows down, employers begin to change the most costly aspect of any business – employment. Cutting full-time jobs is the most efficient way to protect earnings and profitability. However, employers tend to hang on to employees as long as possible, as good employees are expensive to train and hard to replace. Eventually, if the demand falls too much, full-time employees are sacrificed to protect profits. As such, a reasonably predictable cycle continues until exhaustion is reached.

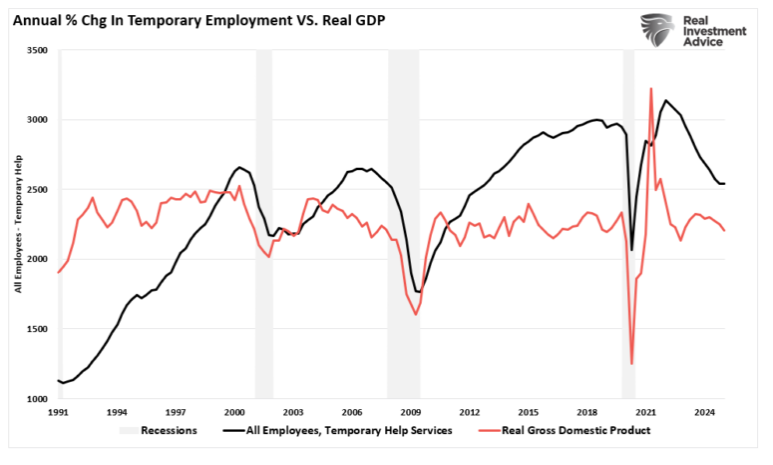

While we are seeing declines in full-time employment as the economy slows, we are now also seeing cuts in temporary help, which, as shown, is consistent with slowing growth. The reason is that cutting temporary employment is the first step by business owners to reduce employment costs while hanging on to full-time, and mostly crucial, employees. However, as noted above, once temporary workers are exhausted, the next step will ultimately be full-time employees.

The latest employment data did not provide much support for the “recession” crowd in 2025. As such, Wall Street analysts are quickly reversing their recession calls for this year, and are becoming more focused on slowing economic growth. However, that assessment can certainly change promptly if personal consumption expenditures take a turn for the worse. As noted above, nearly 70% of economic growth is derived from consumption; therefore, if consumption declines, employment falls, reducing consumption and further employment declines. When it accelerates, that cycle is the foundation for recession outcomes.

Indicators We Are Watching

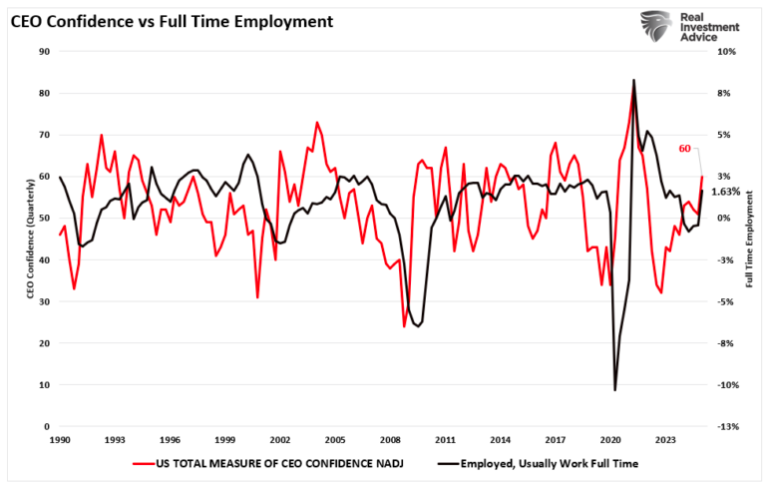

As noted, while the employment data is weak, there are certainly indicators we are watching closely to confirm whether “job loss” is accelerating. First, we pay attention to the Conference Board’s measure of CEO confidence. Since the October 2022 lows, CEO confidence has continued to improve, and as of Q1, it rose to 60 from 51 in Q4 of 2024. That confidence increased full-time employment as the outlook for economic growth was improving heading into 2025. However, this is a lagging indicator, and the results of the Q1 survey were taken in February before the market decline and tariff announcements. Later this month, we will get an update to see if sentiment has changed, which could give us clues about future employment reports.

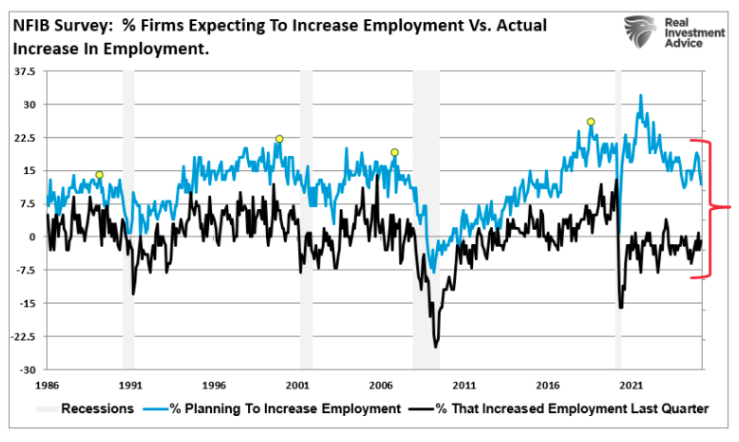

The second indicator we are watching is the NFIB small business confidence index. Specically,.it is their “plans” to increase employment versus what they do. Notably, employment by small businesses, roughly 50% of the total employment in the U.S., has remained stagnant since the pandemic. However, small business owners were very optimistic about hiring post-pandemic, expecting sharp improvements in sales. However, that optimism is fading quickly.

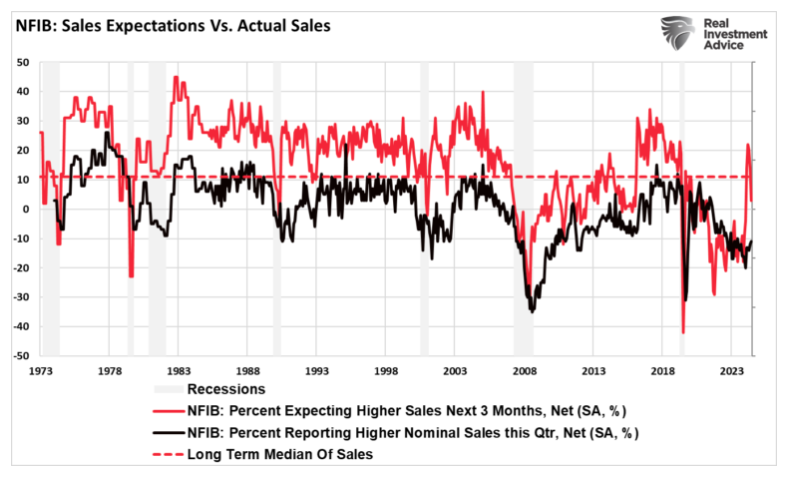

The reason is that, as discussed at the opening of this discussion, employment is a function of the demand for goods and services that businesses supply. As shown, expectations for sales surged following President Trump’s election, but given that actual sales have failed to materialize, that optimism is fading rather quickly. Expectations for business owners are one thing, but without actual increases in sales, which drive revenue, there is little reason to increase full-time employment, which is why it has remained stuck at lower levels since 2020.

Conclusion

Given the importance of consumption in the economy and that employment (production) must come first in the cycle, attention to employment data, particularly full-time employment, is crucial to determining economic risk. The risk of a recession remains very low; however, that can change if something causes consumption to contract quickly. Aside from an unexpected, exogenous impact, investors should expect economic growth to continue to slowly weaken to a longer-term trend slightly less than 2% annually. Unfortunately, while not recessionary, that growth rate will make it hard for corporate profitability to remain at record levels.

Eventually, a valuation adjustment in the financial markets will reflect the reality of a slow-growth economy. However, that isn’t today. However, the risk of a decade of low returns as markets normalize for a slow-growth economy is steadily increasing.

Just something to consider.

For more in-depth analysis and actionable investment strategies, visit RealInvestmentAdvice.com. Stay ahead of the markets with expert insights tailored to help you achieve your financial goals.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All