Charting the Business Cycle

Membership required

Membership is now required to use this feature. To learn more:

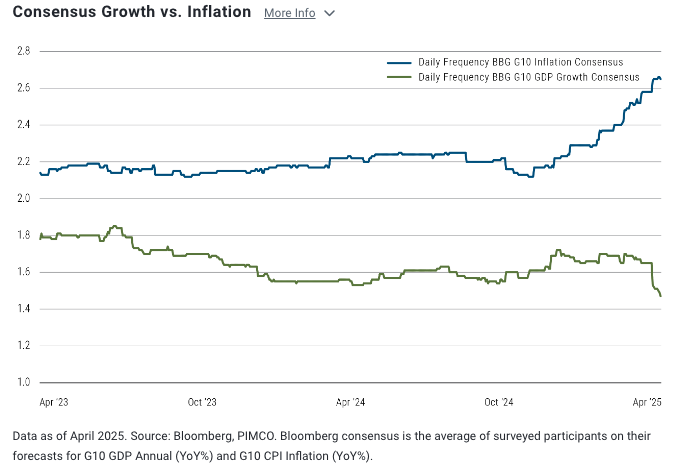

View Membership BenefitsMacro instability drives consensus views on weaker growth, higher inflation

Policy choices are roiling markets and shaking confidence among consumers and businesses.

The consensus outlook for G-10 developed economies has shifted sharply toward lower growth—or even contraction—amid significant inflationary pressure.

Is a widespread bout of stagflation on the horizon? And how can central banks manage the competing risks to growth, employment, and price stability?

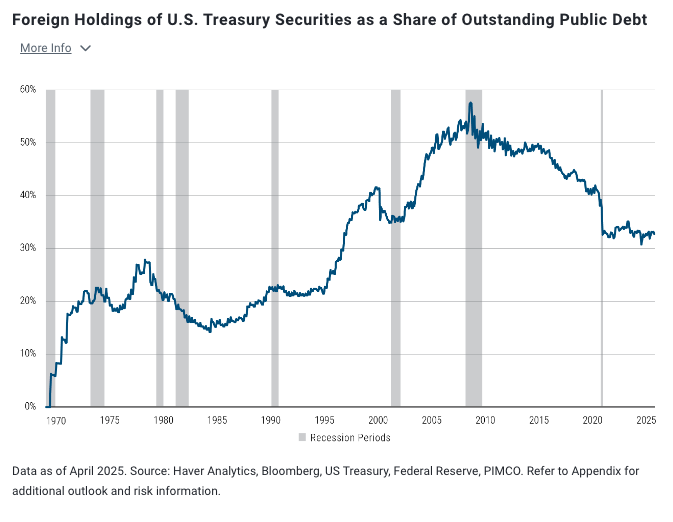

Foreign investors’ share of U.S. debt could decline further

To compound stagflation concerns, U.S. Treasury issues have not been absorbed at the same pace by foreign investors since 2014.

This long-term trend could be further exacerbated by countries that face recent tariff announcements while holding large amounts of Treasuries—uncertainty could subject foreign investors to further slow or cease buying Treasuries.

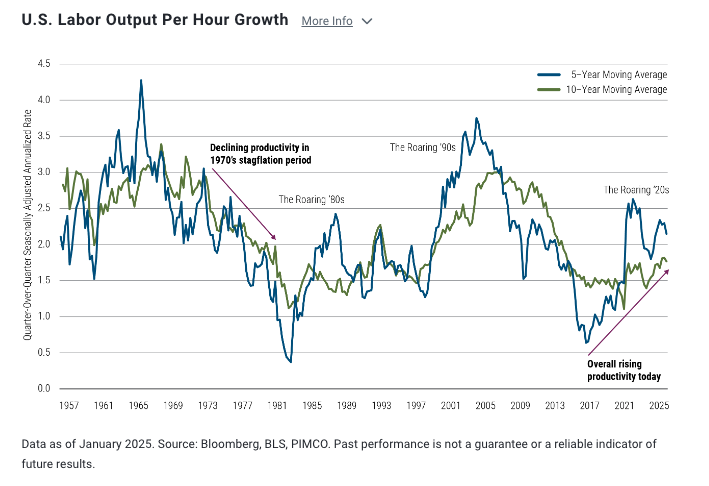

U.S. labor productivity appears resilient amid stagflationary pressure

Even so, unlike the stagflation period of the 1970s that saw a large drop in U.S. labor productivity partly attributed to the energy crisis, U.S. labor productivity has held up fairly well.

Looking ahead, productive labor markets could help balance—to some degree—the inflationary pressures and trade-related uncertainty likely to hinder U.S. economic growth and activity.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results.

It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of manager] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2025-0415-4412074

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All