Inflation Risk Is Subsiding Rapidly

Membership required

Membership is now required to use this feature. To learn more:

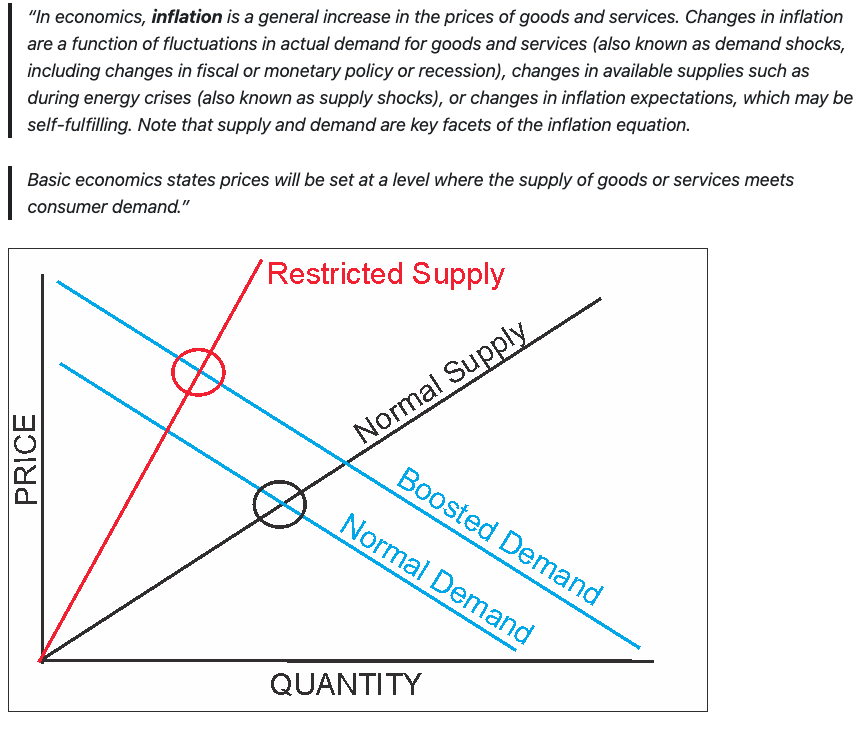

View Membership BenefitsInflation risk has been a significant topic of discussion in the mainstream media for the last few years. Such is unsurprising given that inflation spiked following the pandemic in 2020 as consumer spending (demand) was shot into overdrive from stimulus payments and production (supply) was shuttered. To understand why that occurred, we need to revisit “Economics 101.”

The economic illustration shows this basic principle taught in every “Econ 101” class. As noted, in 2020, inflation was the consequence of restricting supply and massively increasing demand.

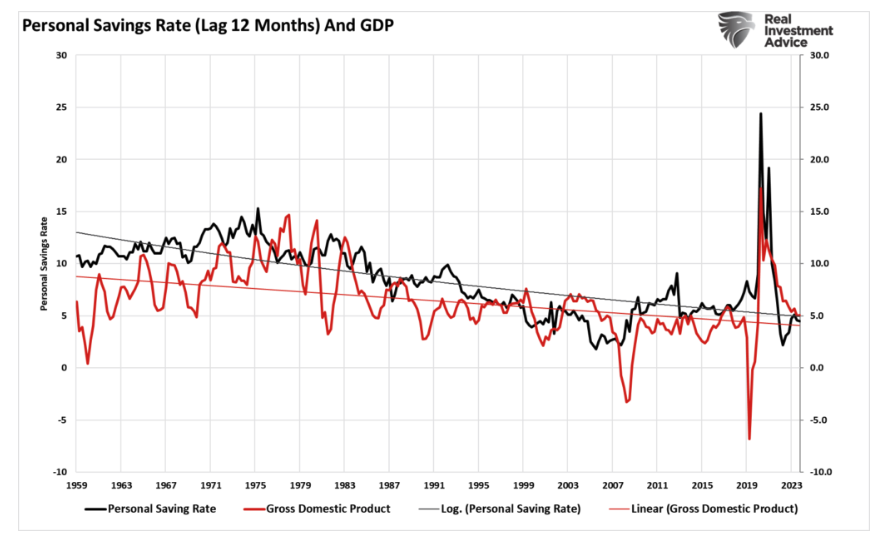

That massive surge in stimulus sent directly to households resulted in an unprecedented spike in “savings,” creating artificial demand. As shown, the “pig in the python” effect is evident. Over the next two years, that “bulge” of excess liquidity has reverted to the previous growth trend. Given that economic growth lags behind the reversion in savings by about 12 months, we should continue to see economic growth slow into 2025. Notably, the “lag effect” is critical to the “inflation risk” thesis.

Understanding that inflation is solely a function of supply and demand, the ongoing reversal of monetary liquidity is continuing to erode economic activity. Notably, what caused the inflation spike post-2020 was not an increase in the debt or the Federal Reserve but rather the temporary increase in the money supply caused by sending checks to households. Therefore, the inflation risk will continue to subside unless the government passes a new infrastructure spending bill of massive proportions or sends another stimulus to households.![]()

They aren’t for two reasons, and it all starts with consumer confidence.

Consumer Is The Key To Inflation Risk

I understand the basic assumption that if you impose a tax on a product, good, or service, then the “cost” of that product, good, or service will increase, hence the inflation risk. While that is perfectly logical, it excludes two crucial factors: 1) Only producers pay the “tax” from tariffs, and 2) we measure inflation (in terms of CPI) from the consumer side of the equation.

In “Tariffs Aren’t An Inflation Risk,” we discussed tariffs’ impact on the production side of the equation.

Read that bolded sentence again.

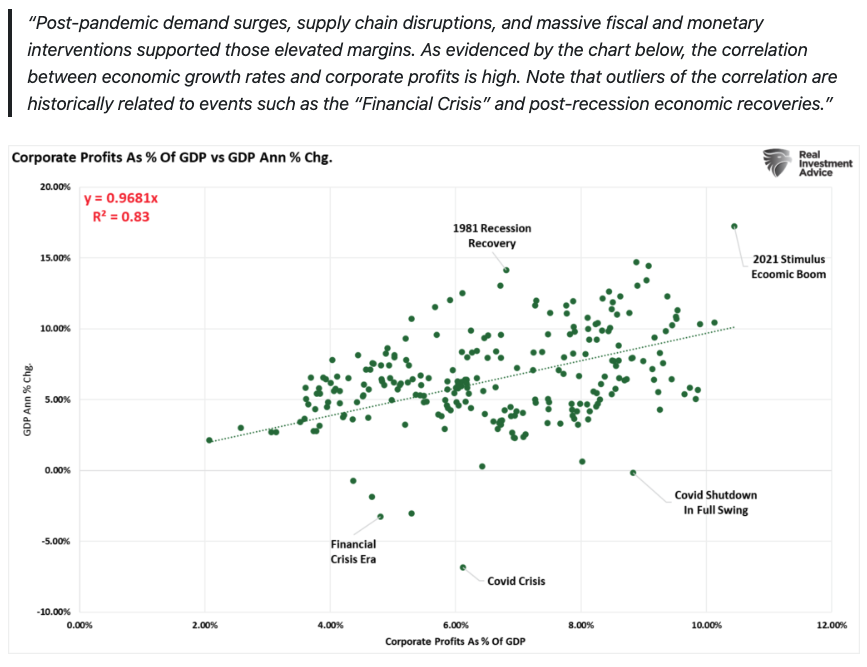

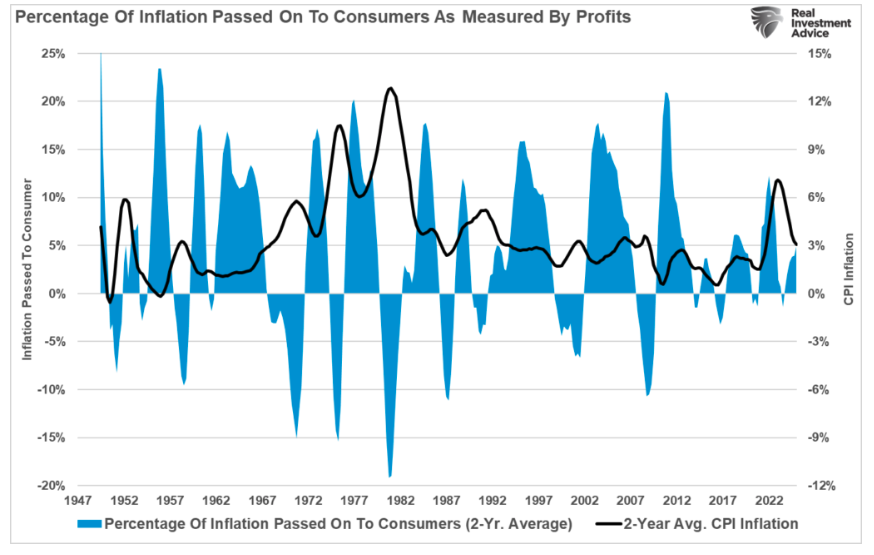

When discussing inflation risk, consumer activity drives inflationary pulses in the economy. If we use a two-year average of corporate profits minus inflation, we can visualize that impact. As shown, inflationary increases, like tariffs, are only inflationary in the economy if they can be passed onto the consumer. Inflation surged in 2020 as corporations could pass on the bulk of the cost increases to consumers flush with cash. Today, to consumers. Today, inflation is declining due to declining demand. As such, the percentage of cost increases corporations must absorb is increasing, which reduces corporate profitability but shows up in the economy as slowing inflation.

Here is the crucial point:

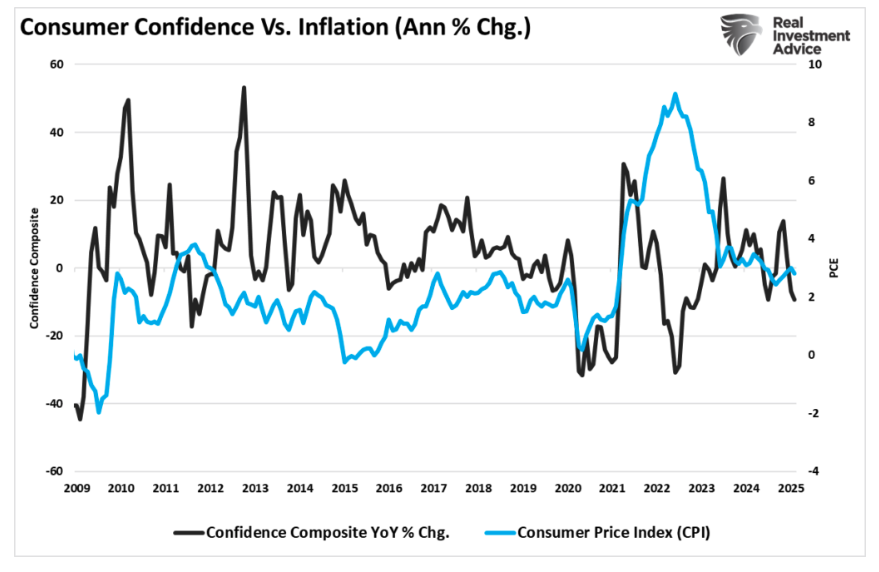

As we should expect, consumer actions, which is how we measure inflation through the consumer price index (CPI), drive inflation risk. Consumer confidence is the key to understanding whether inflation risk is present in the economy.

Consumers Lack Confidence

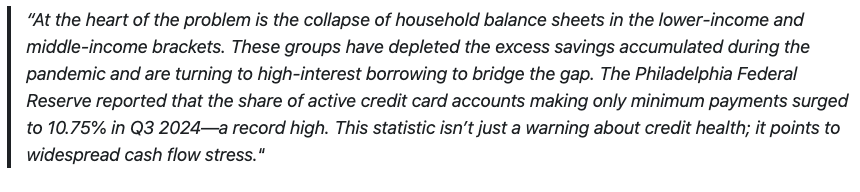

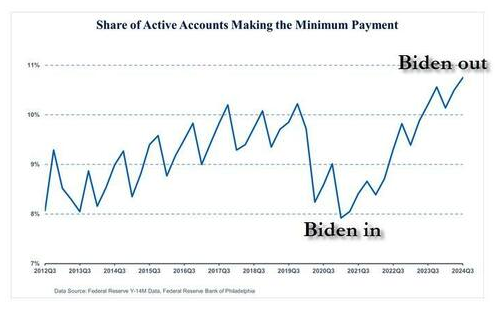

Despite all the commentary about tariff-related inflation risk, inflation is hard to achieve if consumers are unwilling or, more importantly, unable to pay higher prices. As noted in this past week’s commentary, “Consumers Are Tapping Out,” consumers show signs of deep financial stress.

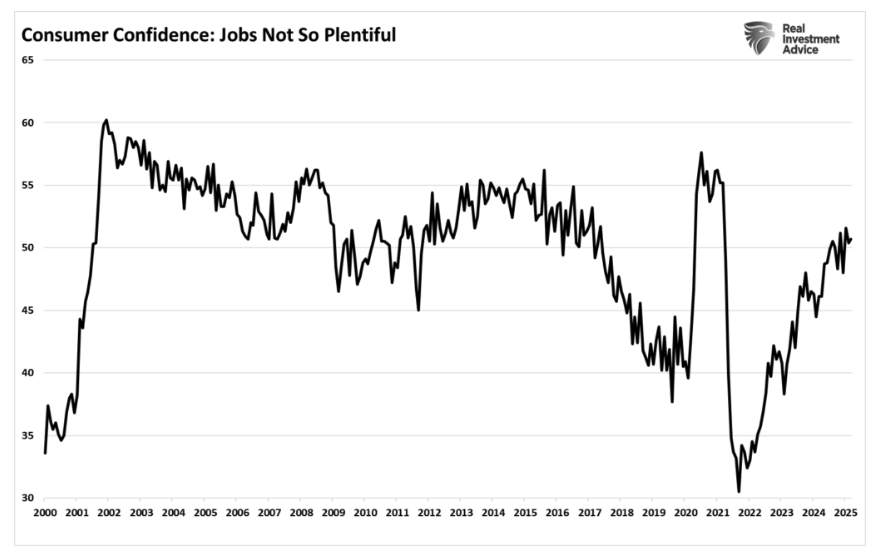

Furthermore, consumer confidence in finding employment continues to erode as the economy slows. Given that employment creates income for consumption, it is difficult to expand consumption (demand) if consumers do not have a job, fear losing their jobs, or wage growth stagnates.

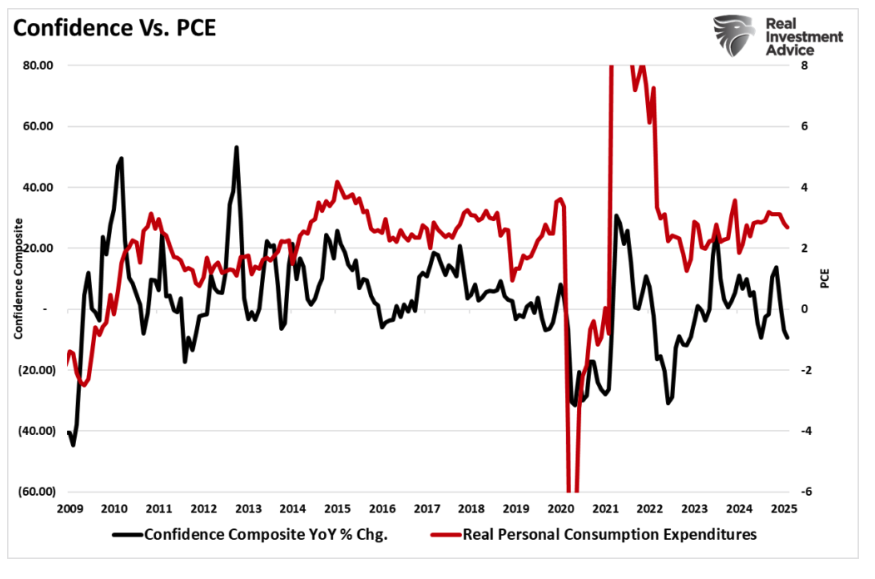

We can investigate this further by examining Personal Consumption Expenditures (PCE), which comprise nearly 70% of the economic equation. Historically, when consumer confidence is declining, consumption also slows.

As such, it is unsurprising that inflation is tied to consumer confidence. As consumer confidence declines, the demand for goods and services also declines. The reduction in economic activity shows up in the current inflation risks.

Conclusion

Lastly, Consumer stress isn’t limited to anecdotal indicators—it shows up in corporate earnings and executive commentary. During the company’s earnings call, Doug McMillon, CEO of Walmart, stated that many customers are under “budget pressure.” They also exhibit “stressed behaviors,” including spending reductions across general merchandise. Specifically, he warned that “For many customers, the money runs out before the month does.”

Similarly, Dollar General CEO Todd Vasos painted an equally concerning picture. He described his customers as “struggling more than ever before.” Todd added that some are now forgoing non-discretionary items, like medication or hygiene products, to afford groceries and fuel. He said, “These customers are making trade-offs we haven’t seen in years.” Concurring with that warning was Jane Fraser, CEO of Citigroup. She observed that consumers are “becoming more cautious” and focusing spending on smaller, lower-cost purchases. While this signals a growing defensive posture, often associated with recessionary conditions, they are also deflationary. When consumer behavior shifts en masse from aspirational to survival-based, the ripple effects are inevitable.

The bottom line is that inflation risks are extremely muted given the rapidly slowing economic backdrop and disruption in the stock and bond markets, which also impact consumer confidence. Could that change? Yes, but such a change would require a reinstatement of stimulus checks, a surge in Government spending, and the Federal Reserve increasing monetary policy. For now, none of those are available.

The most significant risk to the economy is not the return of inflation risks but rather the collapse in consumer confidence that leads to a recession.

We may have that data showing up sooner than later.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All