In November last year, I discussed the importance of yield spreads, historically the market’s “early warning system.” To wit:“

In other words, the yield spreads reflect the perceived “risk” in the financial markets. The spread between risky corporate bonds and safer Treasury bonds remains narrow when the economy performs well. This is because investors are confident in corporate profitability and willing to accept lower yields despite higher risks. Conversely, during economic uncertainty or stress, investors demand higher yields for holding corporate debt, causing spreads to widen. This widening often signals investors are growing concerned about future corporate defaults, which could indicate broader economic trouble.

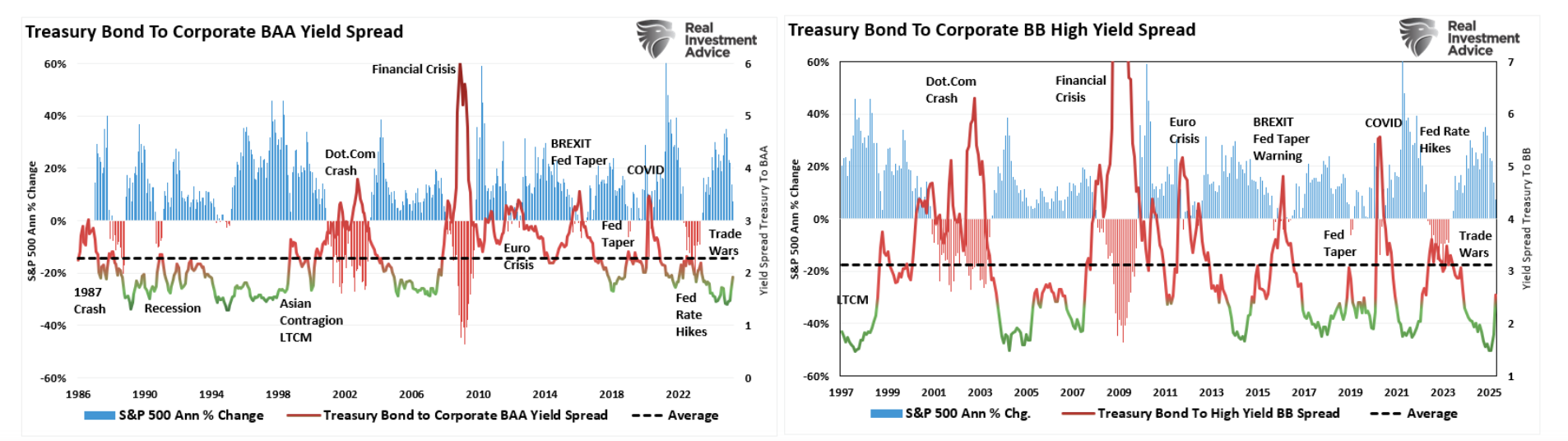

The two charts above show the importance of yield spreads, which tend to rise before financial turmoil in the stock market. When yield spreads began to widen, those increases often preceded liquidity events, reduced corporate earnings, economic contractions, and stock market downturns. In other words, the increase in yield spreads reflected increased investor risk aversion. Eventually, that risk aversion spilled over into the financial markets as investors realized the fundamental shift in the financial markets.

As we discussed in this past weekend’s #BullBearReport, yield spreads reflect the recognition of a shift in three primary areas:

- Corporate Financial Health: Credit spreads reflect investor views on corporate solvency. A rising spread suggests a growing concern over companies’ ability to service their debt. Particularly if the economy slows or interest rates rise.

- Risk Sentiment Shift: Credit markets tend to be more sensitive to economic shocks than equity markets. When credit spreads widen, it typically indicates that the fixed-income market is pricing in higher risks. This is often a leading indicator of equity market stress.

- Liquidity Events: As investors become more risk-averse, they shift capital from corporate bonds to safer assets like Treasuries. The flight to safety reduces liquidity in the corporate bond market. Less liquidity potentially leads to tighter credit conditions that affect businesses’ ability to invest and grow, weighing on stock prices.

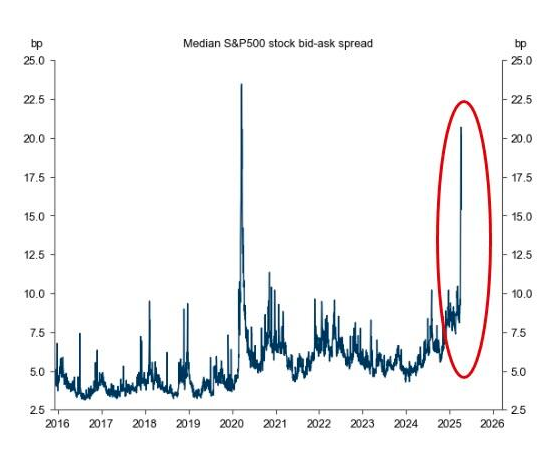

The recent market disruption caused by Trump’s trade war has undoubtedly widened spreads between “risk-free” treasury yields and corporate bonds. This is because those tariffs directly impact corporate financial health (reduced profitability), a shift in “risk sentiment” (valuations), and liquidity (potential increase in default risk). Regarding the last point, the lack of market liquidity is at levels not seen since the economic shutdown in 2020.

While yield spreads have widened, they remain well below the long-term averages. However, if recession risks increase due to tariffs, sentiment, or illiquidity, those yield spreads will widen further. The illiquidity issue is currently the most significant risk to the markets, as the sharp spike in yields this past week is warning of a more significant event brewing in the bond market. As we noted in our Daily Market Commentary this past week:

That type of sharp liquidation has historically been the issue of some liquidity events in the bond market. In this case, it appears to be the heavily leveraged arbitrage trade used by hedge funds called the “basis trade.” That trade is a little complicated but critically important to understand. The link below is a brief explanation.

However, the increase in yield spreads and the disruption in the bond and equity markets certainly raise the risk profile for investors in the near term.

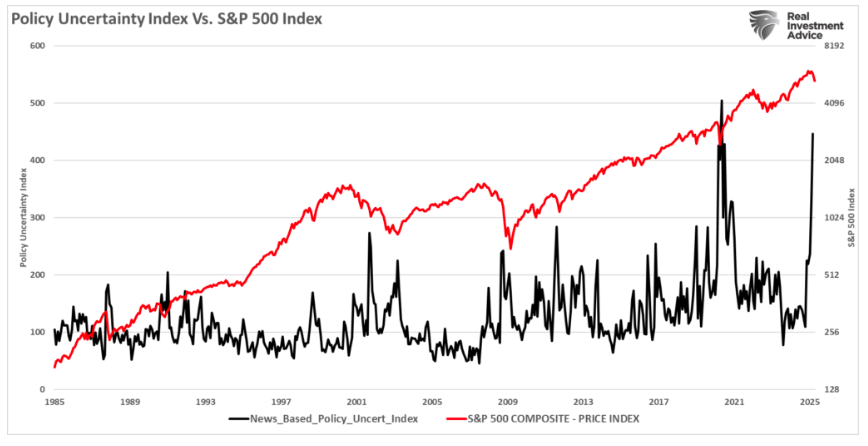

Economic Policy Uncertainty

We previously addressed the market’s selloff, primarily due to the Trump administration’s “tariff on, tariff off” policies.

As shown, those policies are creating a sharp increase in policy uncertainty. We suspect this isn’t going to change in the near term. However, it is notable that these periods are historically short-term, and such spikes are generally near market lows. In other words, the current policy uncertainty will pass, and markets can return to focusing on earnings and valuations. Until then, market rallies will likely be an opportunity to reduce risk.

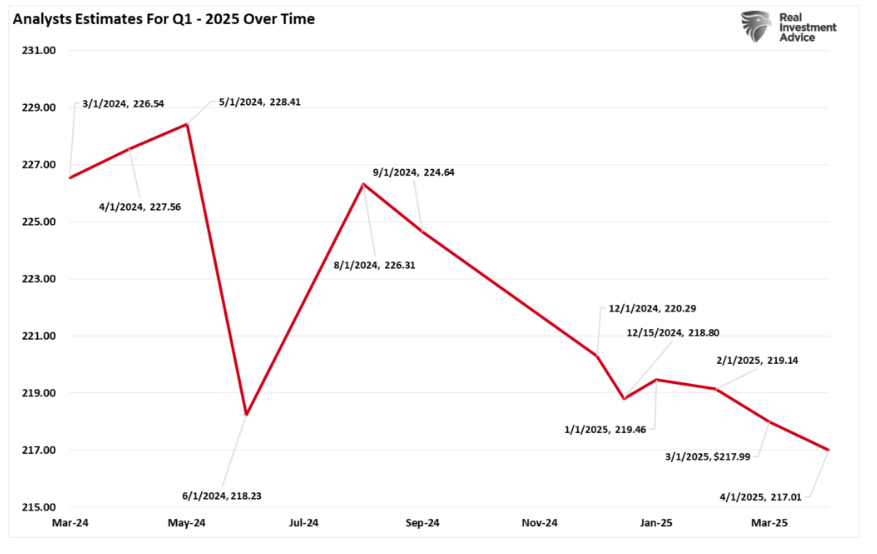

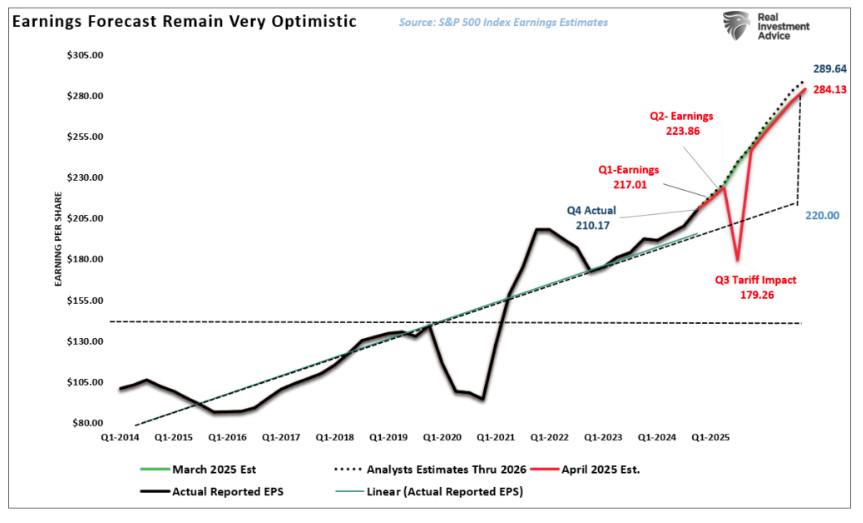

Regarding earnings and valuations, Wall Street only expects a one-quarter impact from tariffs. As shown, earnings for Q1 are currently expected to come in at $217/share, down from $226.54 one year ago. But, interestingly, Q2 earnings are expected to rise to $223.86, roughly where Q1 estimates started a year ago.

However, in Q3, earnings are expected to drop sharply to just $179/share. If realized, that 20% drop in earnings will be pretty significant. This is particularly problematic for the equity market when assigning forward valuation multiples. For example, assuming the market trades at an 18x multiple of $179 in earnings would pin the market’s fair value at 3,222. Such would be a nearly 40% decline from Friday’s close.

Following that sharp drop in earnings, analysts at S&P Global expect Q4 earnings to rebound sharply to their previous estimates. That assumption suggests they believe the tariffs to be temporary, and the Trump administration will negotiate “no tariff” deals with our trading partners. While such could be the case, I am not so optimistic.

However, whatever outcome occurs will likely lead to reduced estimates heading into 2026, closer to the long-term linear growth trend. That is what the rise in yield spreads suggests as the economy slows and inflation falls. That is barring the expansion of the current bond market crisis into a more significant credit-related event that begins to impact the major banks.

This uncertainty, in both policy and markets, is why we are cutting risk for now.

We Cut Risk For Now

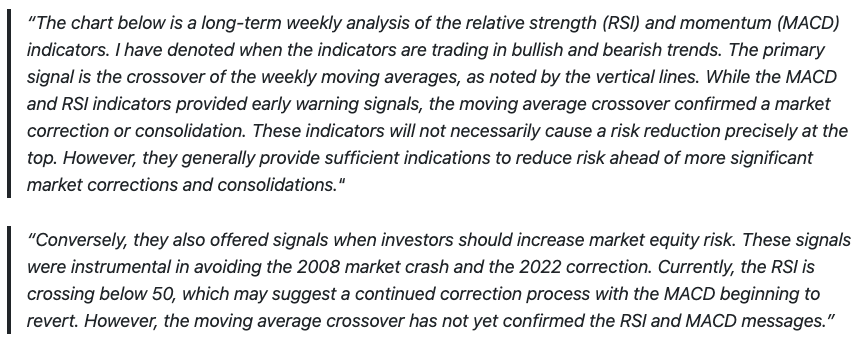

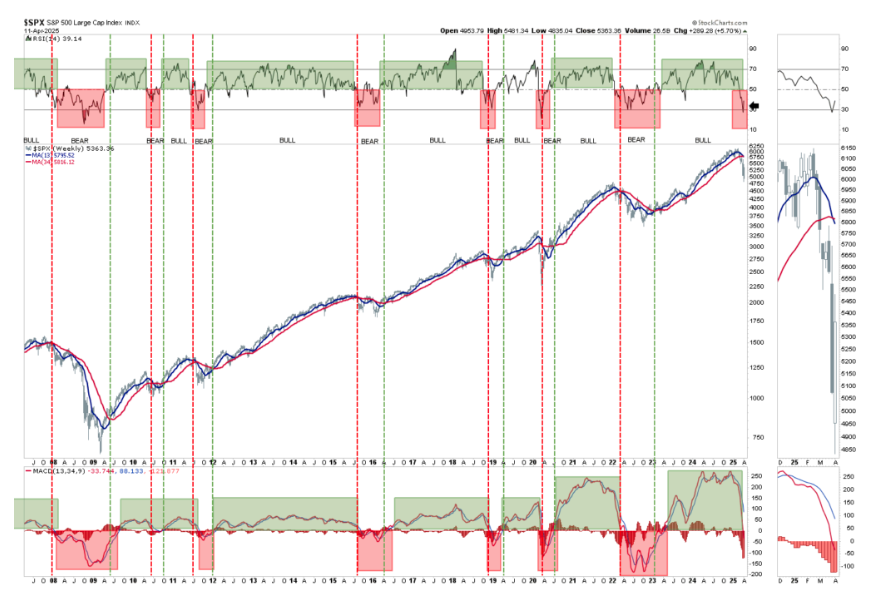

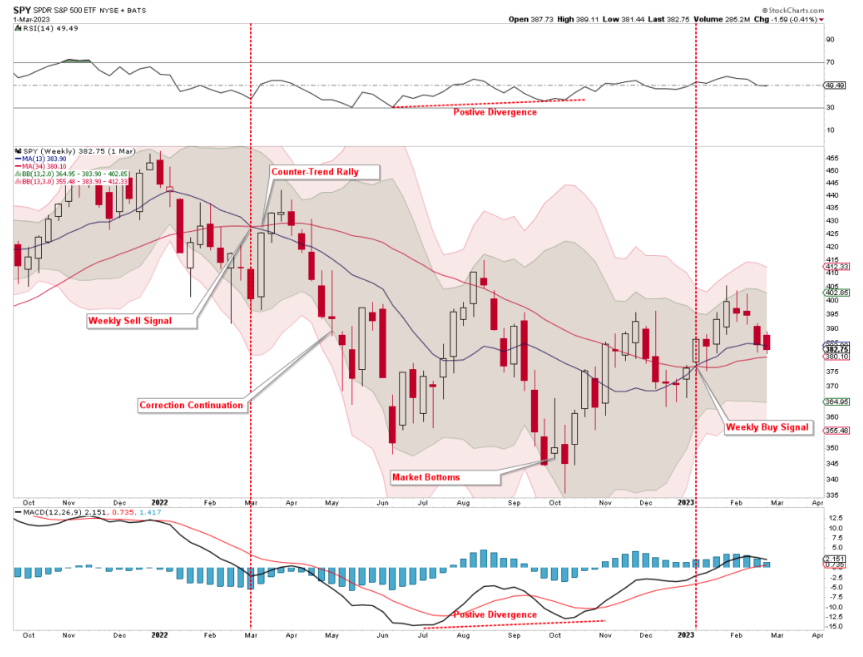

As discussed in last week’s post, “Hope In The Fear,” the weekly “sell signal” was triggered.

Currently, both the market and the increase in yield spreads warn investors of elevated market risk that could induce further market declines and increased volatility. While such does not preclude a significant counter-trend rally in the short term, the longer-term risks seem to be growing.

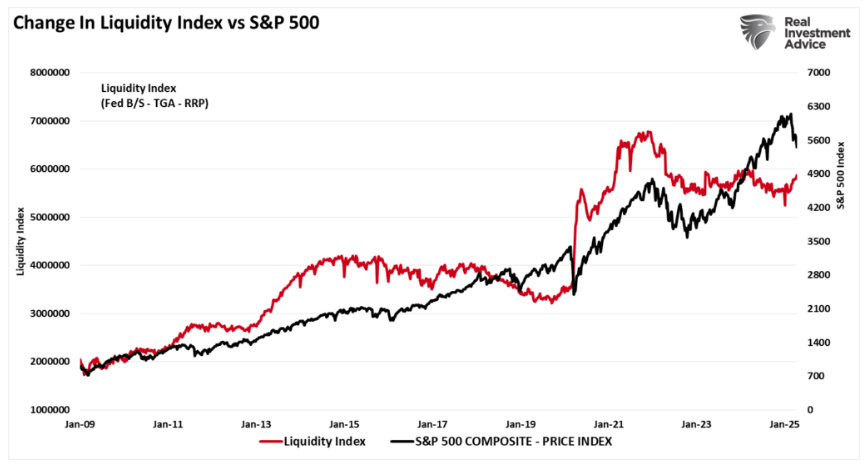

As investors, we could undoubtedly ignore the warning signs, and this could be a short-term corrective event like we saw during the 2020 pandemic or the Fed’s “taper tantrum” in 2018. The market correction was brief in those instances, and the bull market resumed. However, it is worth noting that during those periods when the “sell signals” were short, the Federal Reserve intervened by cutting rates, increasing monetary accommodation, or both. Currently, as shown in the Fed Liquidity Index, that is not the case.

For these reasons, we began cutting risk on this week’s rally. With the market still technically oversold, we will not be surprised to see a continuation of the rally this week. Such would be similar to the reflexive rally we saw immediately following the weekly “sell signal” in 2022. Today, like then, sellers emerged as market concerns remained elevated. I suspect that will be the case this time as market participants continue to reprice markets for slower economic growth and policy changes. Markets rarely bottom without retracing toward the previous lows or setting new lows. Given the technical damage to the market, we suspect we will see a pullback before this correction process is over.

From a more bullish point of view, the valuation reversion will eventually become complete. However, that is likely not in the coming weeks or even the next couple of months.

If the markets rally substantially from current levels, our risk reduction actions will drag on portfolio performance. I am okay with that until I am more confident that the corrective process is behind us and that the benefits of increased equity exposure outweigh the risks to invested capital. Given the warning signs from yield spreads, the weekly “sell signal,” and slowing economic growth and inflation, market risk seems tilted against investors temporarily.

For now, we will continue to use rallies to rebalance risk, manage asset allocations, and hold increased cash levels.

Trade accordingly.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice