Last week’s data can be summarized by a volatile market reacting to tariff news, a backwards-looking inflation reprieve, and deteriorating sentiment across consumers and small businesses.

The stock market experienced dramatic swings. These were fueled by President Trump's partial reversal of his recently announced tariff policies. That move is reportedly triggered by a rapid rise in the 10-year Treasury yield. This reversal led to the S&P 500's best single-day performance since October 2008.

Meanwhile, prices fell for the first time in nearly five years. That's due to inflation cooling to its lowest level in over four years. However, this encouraging report preceded the implementation of the new tariff policies. That suggests the current price relief may be short-lived. Adding to the cautious outlook, consumer sentiment continued its steep decline. it reached near-record lows as concerns about trade wars, inflation, and the labor market intensified, while small business optimism also waned.

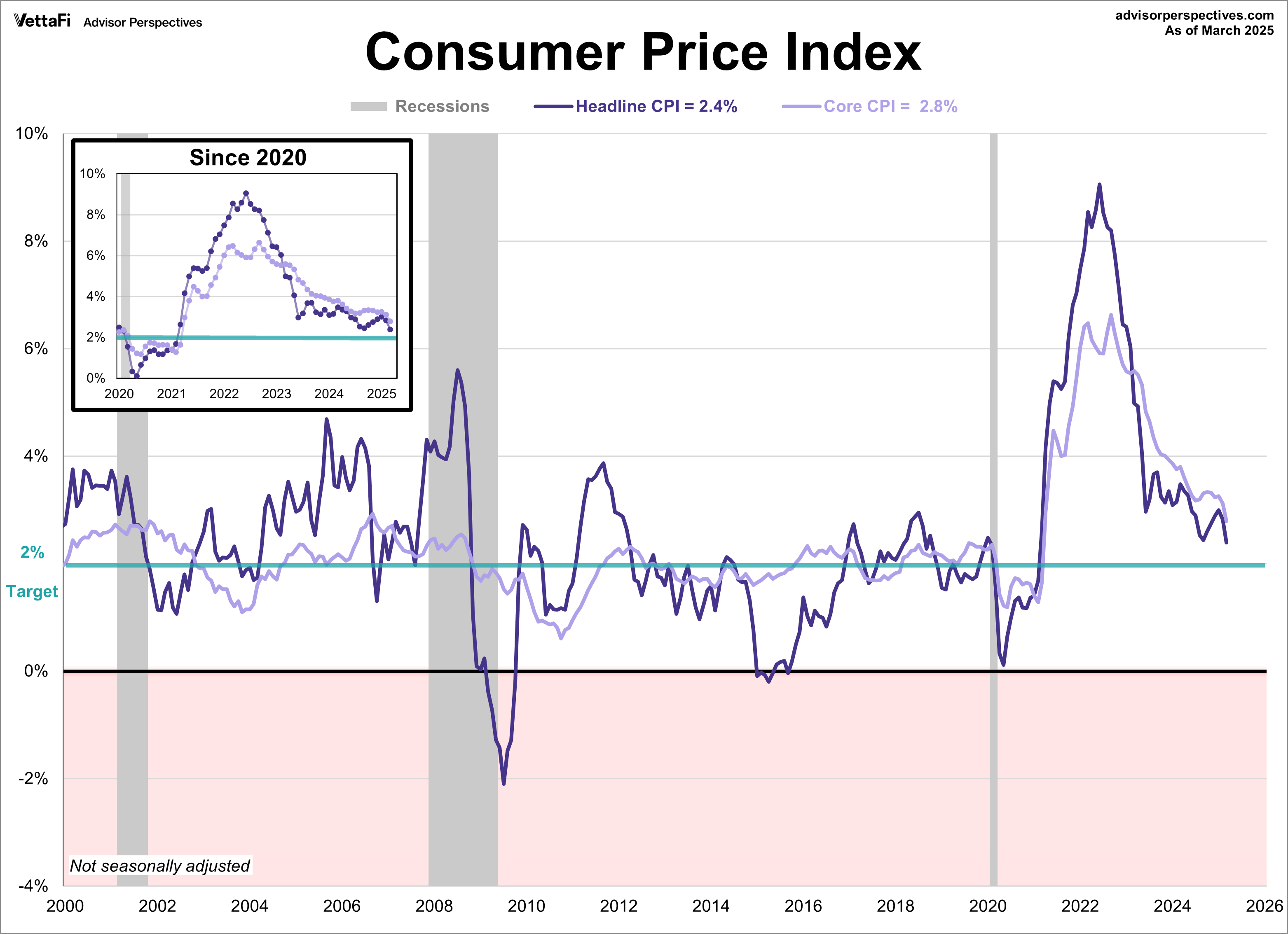

Consumer Price Index

Inflation cooled for a second straight month in March. It fell to its lowest level in over four years. However, the price pressure relief may be short-lived. That's because President Trump’s tariffs will likely lead to price increases in the coming months.

The Consumer Price Index (CPI) rose 2.4% last month, down from 2.8% in February and lower than the expected 2.5% growth. On a monthly basis, prices fell 0.1% after a 0.2% rise in February. This was the first monthly decline since May 2020. The decline was driven by lower costs for energy, airline fares, motor vehicle insurance, used cars and trucks, and recreation. These were offset by increases in the food index, personal care, medical care, education, apparel, and new vehicles.

Core inflation, which is more closely watched since it excludes volatile items like food and energy, fell to 2.8% last month, its lowest level since 2021. Core prices were up 0.1% from the previous month following a 0.2% increase in February. Both readings were lower than expected.

While the latest data offered some relief from price pressure, the Fed will most likely continue with its “wait-and-see” approach to evaluate the impact that current tariffs, potential future tariffs, and other policies may have.

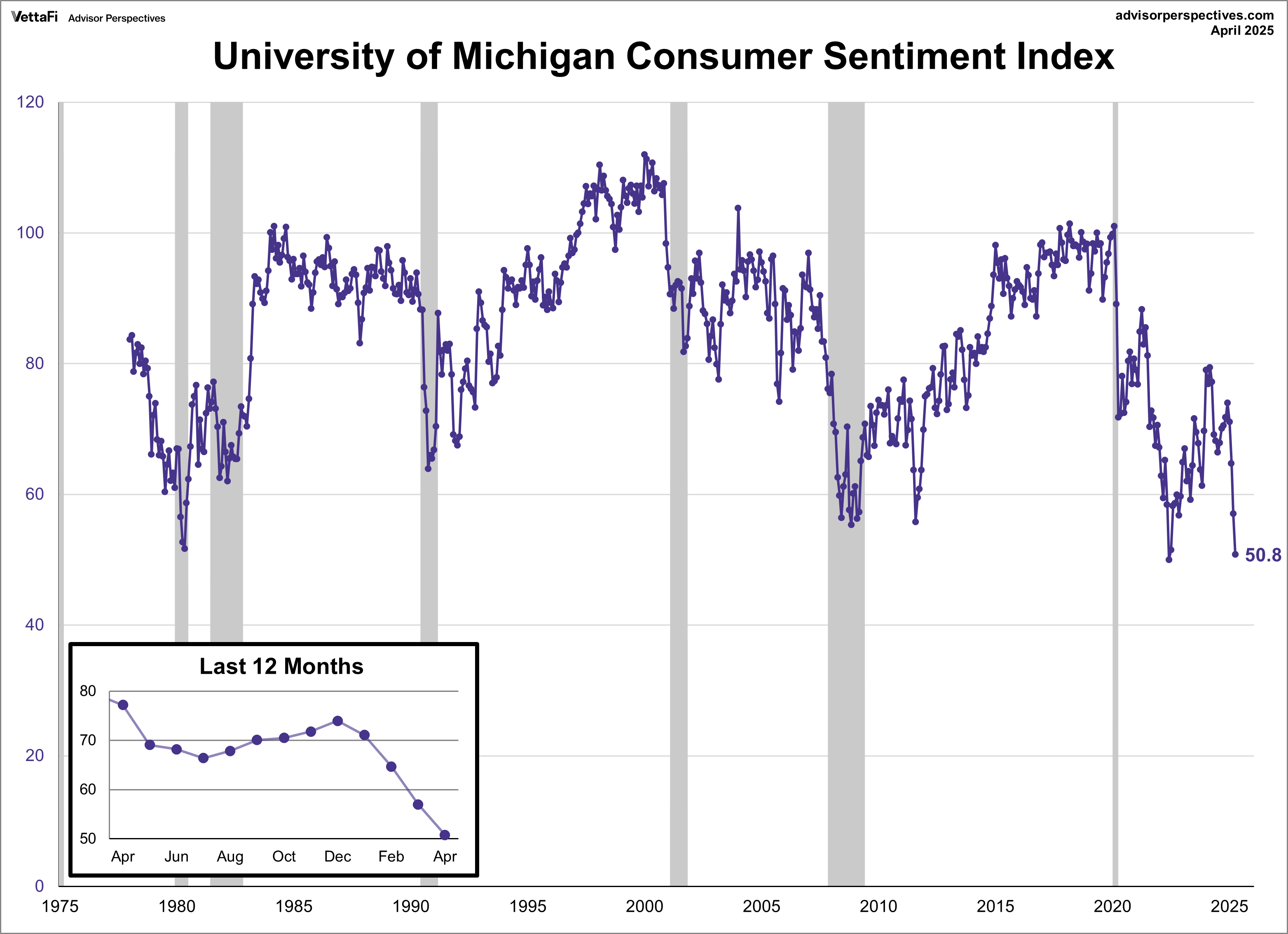

Michigan Consumer Sentiment

Consumer sentiment fell further this month as consumers reported growing concerns around trade wars, inflation, and the labor market. The Michigan Consumer Sentiment Index fell 6.2 points to 50.8 this month, its second-lowest reading on record. This represents a 10.9% decline from March’s final reading and a 34.2% drop from one year ago, the largest annual decline since July 2022.

The significant downturn in consumer sentiment this month has triggered recession alarms. The current conditions index dropped to its lowest level since 2022 while the expectations index sank to a 45-year low. Consumers expressed mounting fears regarding trade tensions and a worsening economic outlook across key areas, particularly the labor market, signaling heightened recession risk.

Inflation expectations continued to rise for both the near and long term. Year ahead expectations rose for a fifth straight month to 6.7%. That is the highest level since November 1981. Five-year expectations jumped to 4.4%, the highest since 1991.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

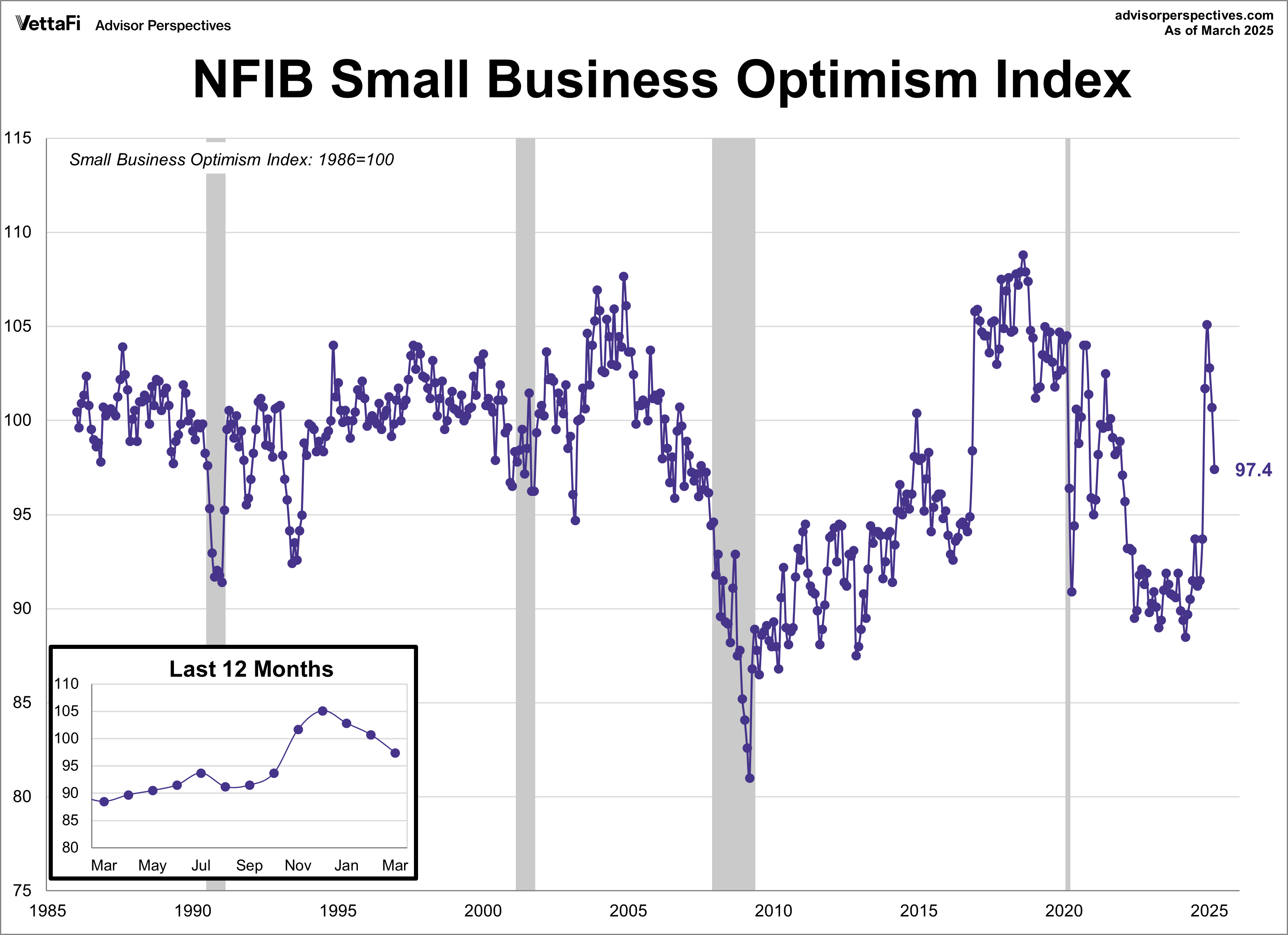

NFIB Small Business Survey

Optimism among small business owners continued to worsen last month. The NFIB Small Business Optimism Index declined for a third consecutive month, falling 3.3 points to 97.4 in March — below the 98.9 forecast. The latest reading pushed the index back below its historical average for the first time since October.

Small business owners cited labor quality, taxes, and inflation as their top concerns, with many scaling back sales growth expectations. Furthermore, there was a decline in the number of owners who believe business conditions will improve over the next six months. And there was a higher number who reported difficulty in obtaining a loan. The survey results highlight the significant impact that the small business sector can have on the overall economy. That's because small businesses employ roughly 50% of the U.S. workforce.

Market Reactions

Following its worst week in over five years, the S&P 500 staged a significant recovery, posting its best week since November 2023 with a 5.7% gain. This rebound was largely fueled by Wednesday's dramatic 9.5% surge, its biggest single-day increase since 2008. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 5.6% last week. Meanwhile, the S&P Equal Weight Index was up 3.2% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 3.1%.

The yield on the 10-year note ended April 11, 2025 at 4.48%, its highest level since mid-February. Meanwhile, the 2-year note ended at 3.96%.

The CME FedWatch Tool currently shows an 80% likelihood that the Fed will hold rates steady at their meeting next month. Markets are pricing in three 25 basis point cuts for later this year coming at the June, July, and October meetings with one additional 25 basis point cut in 2026.

Economic Data in the Week Ahead

This week's economic data will provide updates on consumer spending, housing, and the broader industrial sector. On Wednesday, retail sales data for March will reveal if consumers remained cautious with their spending amid heightened economic uncertainty. Housing indicators released throughout the week will show how tariffs, elevated mortgage rates and affordability challenges are shaping the real estate market. Additionally, the Empire State and Philadelphia Fed manufacturing surveys, along with March’s data on national industrial production, will highlight both regional and national trends in the manufacturing and industrial sectors.

For more news, information, and strategy, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more commentaries by VettaFi