Originally published February 14, 2025

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Tariffs could reduce economic growth by up to 0.60% over the next year

- Tariffs' impact on inflation could be mitigated by a variety of factors

- Fed policy will likely remain on hold until there is more clarity

Happy Valentine’s Day to all our friends, family, and co-workers. With this special day falling on a Friday and leading into a long weekend, retailers and restaurants are optimistic that consumers will spend generously this year. The National Retail Federation’s annual survey predicts a record $27.5 billion in Valentine’s Day spending. Popular splurges include chocolates, roses, extravagant evenings out, and my wife’s favorite – jewelry. However, those planning to gift chocolates will face higher costs, as cocoa prices have doubled over the past year, even before considering tariffs. Speaking of tariffs, financial markets are becoming uneasy as President Trump follows through on his campaign promises to impose or threaten new tariffs to improve trade imbalances or achieve some of his policy priorities (e.g., border protection and drug trafficking). Below, we detail how these tariffs could impact the economy, inflation, the Fed's outlook, and the equity markets.

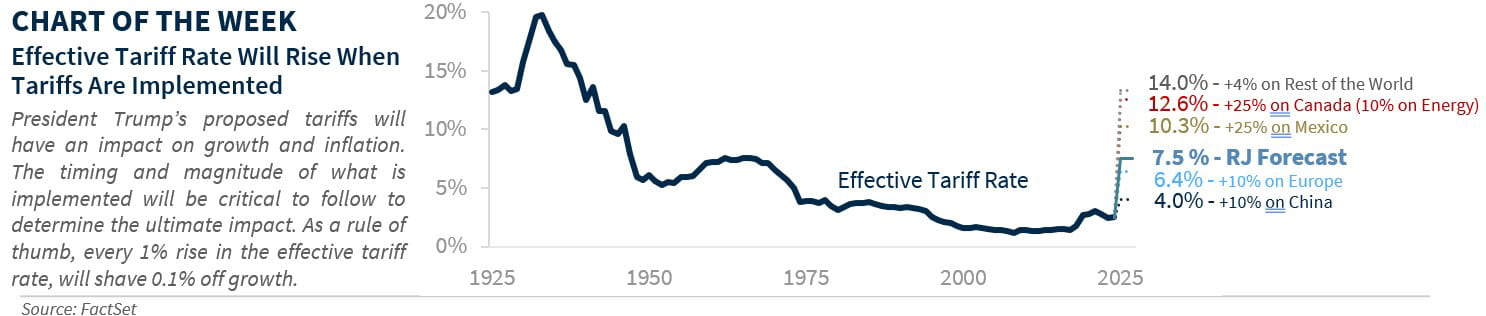

- The Economy | The US economy continues to progress steadily, with the Atlanta Fed GDPNow estimate for Q1 2025 tracking at around 2.3%. However, heightened trade uncertainty and President Trump’s early (and potentially more aggressive) use of tariffs could pose risks to growth while we await the offsetting effects of other policy measures, such as tax cuts and deregulation. Although we have maintained our 2.4% GDP forecast for 2025, we have examined the potential economic impacts of tariffs. Our economists estimate that for every 1% increase in the effective tariff rate, there will be a ~0.1% drag on growth. While we assume the threatened tariffs on Canada and Mexico will not be implemented (or at least not be long-lasting), Trump will likely increase tariffs further on China and impose tariffs on Europe and other parts of the world. As a result, our base case is that the effective tariff rate could rise from 2.5% to 7.5%, potentially reducing growth by up to 0.60% in the first year. This would be a significant, but still manageable headwind. However, a more extensive use of tariffs, including those on Canada and Mexico, could result in a growth drag of up to 1.2%. This estimate does not account for retaliatory tariffs, which could lead to a more substantial negative growth influence that we will monitor closely. The timing of these tariffs will be critical as well.

- Inflation | Tariffs enacted during Trump’s first term did not have a lasting impact on inflation. However, today's situation differs significantly from 2018. Currently, inflation remains well above the Fed’s 2.0% target, and Trump’s proposed tariffs are broader in scope. These tariffs come at a time when consumers are more sensitive to inflationary pressures because of recent experiences after COVID. This sensitivity is evident in the sharp rise in inflation expectations as consumers grow increasingly concerned about the upcoming tariffs. Our economists estimate that every 1% increase in the effective tariff rate adds approximately 0.1% to overall inflation. Therefore, a 5% increase in the effective tariff rate could raise annual inflation by 0.5%. However, several mitigating factors could lessen this impact. First, with consumers now more price-sensitive due to online shopping, there will likely be an increased substitution effect as they shift to cheaper, alternative goods. Second, a demand hit could ultimately put downward pressure on prices. Third, other macro factors, such as easing shelter and energy costs, could slow the increase in inflation. And finally, a stronger US dollar could offset some of the rising costs of tariffs. Ultimately, we expect the potential rise in inflation above our core PCE estimate (2.6%) could be as much as 0.3-0.4%—not ideal, but not catastrophic.