Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

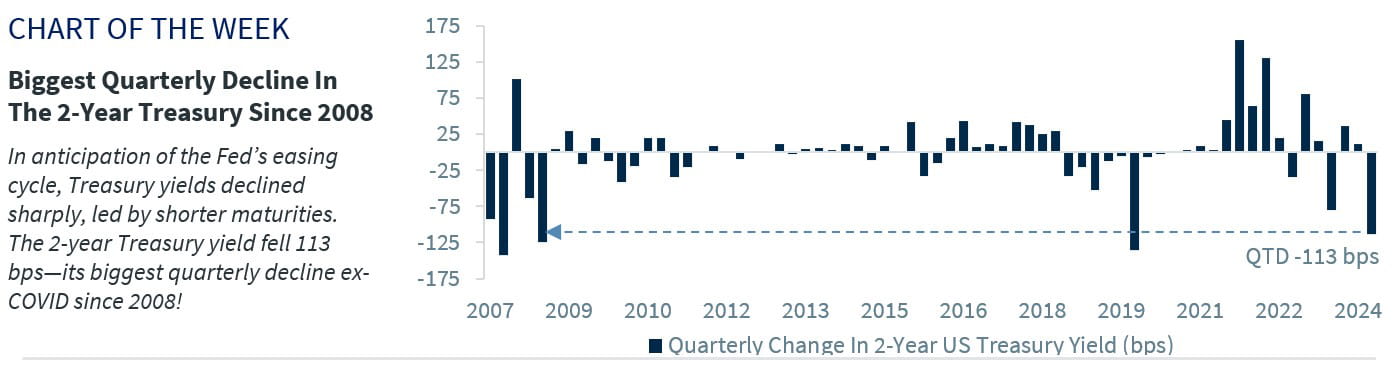

- Strong returns across all fixed income sectors in Q3

- Another solid quarter for the equity market

- Mixed commodity performance despite weaker USD

Who says nothing happens over the summer? It’s not unusual for life to slowdown in the summer as we all strive to take a break from the daily grind of going into the office and enjoy time relaxing at the beach or the mountains with family and friends. While we may be lulled into thinking that not much happens over the summer as we take a mental break, this year was more active than most. The economy reached an inflection point, with labor market conditions squarely in focus. Chair Powell laid the groundwork (in Congress and at Jackson Hole) for the Fed’s easing cycle to begin, triggering a massive rally in the bond markets. And, equity markets were jolted with a spike in volatility in early August, but swiftly recovered. Below we provide a brief recap of the major trends driving the economy and the financial markets this quarter:

- Economic momentum is downshifting | Steady progress on the inflation front, slowing payroll growth and a surprise increase in the unemployment rate convinced policymakers the time had come to take their foot off the brake pedal. While growth has remained resilient (Q3 Atlanta Fed GDPNow is still running at a 2.9% pace), anecdotal evidence from the Fed’s Beige Book (one of Powell’s favored indicators) and micro-data embedded in 2Q24’s earnings reports (highlighting softening consumer demand) suggested economic growth may be weaker than the Fed expected. Significant downward revisions to prior payroll reports, which reduced job growth by 818k for the 12 months ending March 2024, added to the picture of slowing economic momentum. While the economy may be entering a soft patch, it should be short-lived now that the Fed is using some of its firepower to provide support and keep the expansion going. Our economist expects the economy to slow to a below-trend pace in the coming quarters and reaccelerate in 2025 with few if any job losses, allowing the Fed to achieve an elusive soft landing.

- Strong returns across all fixed income sectors | Cooling inflation and softening labor market conditions sparked a sizeable decline in bond yields as the market prepared for a shift in Fed policy over the summer. The Fed delivered last week with a jumbo-sized 50 bps rate cut (something rarely seen outside recessions). As the bond market anticipated the Fed’s actions, the policy-sensitive 2-year Treasury fell 113 bps – its largest quarterly decline ex-COVID since 2008. The U.S. Aggregate Bond Index is up 5.2% QTD—on track for its best quarter since Dec 2023 and the 5th consecutive month of gains! While credit markets experienced some wobbles in early August as volatility spiked during the unwinding of the yen carry trade, investment grade, and high yield quickly recovered, delivering solid returns (IG +5.7% and HY +5.1%) as spreads modestly tightened QTD. While it’s been a strong quarter, the gains are unlikely repeatable given how much Fed easing is already expected in the months ahead. The bulk of the move lower in yields is likely behind us, barring any unforeseen weakening in the economy (not our base case).

- Another solid quarter for the equity market | Equities bucked the seasonal trend in the third quarter (3Q is typically the weakest quarter of the year), with the S&P 500 up 6% (notching four record highs during the quarter) – its fourth consecutive quarter of gains. On a YTD basis, the S&P 500 recorded 42 record highs (the eighth most to start a year) and is up 21.7%! The powerful stock market rally has been underpinned by strong earnings growth (2Q24 earnings rose at the fastest pace since 4Q21), still positive economic growth, the onset of the Fed easing cycle, and declining interest rates. Most important, the third quarter brought a change in market leadership, with a significant broadening in performance beyond the mega-cap tech leaders. In fact, Tech underperformed the S&P 500 by its widest margin since 2Q16! Instead, the more defensive sectors, such as Utilities and Real Estate (which are interest-rate sensitive) were among the best performers. In addition, the S&P 500 Equal Weight Index outperformed the S&P 500 by ~4% and small-cap equities gained 8%. As a soft landing remains our base case and with the Fed likely to deliver a series of rate cuts, we expect the broadening in performance to continue over the next 12 months.

- Despite a weaker dollar, mixed performance for commodities | Relative to its DM counterparts, the U.S. economy remained the standout on the global stage. Despite this, the U.S. dollar posted its second worst quarterly decline (-4.7%) over the last ten years, as rising expectations for future rate cuts weighed on the greenback. While a weaker dollar is usually supportive of commodities given the negative correlation between the two asset classes, commodities were slightly lower QTD, down 1.1%, with significant dispersion beneath the surface. Crude oil was particularly weak (-17%) as record production in the US, OPEC looking to roll back production cuts, and weaker demand in China (one of the largest consumers of crude oil) more than offset increased geopolitical risk in the Mideast. While the announcement of stimulus in China helped soften the blow, weakness in Chinese demand also weighed on industrial metals (-0.7% QTD). One area that did shine was gold, as the weaker dollar, slowing global economic activity, and the Fed cutting interest rates led the precious metal to rally 15% – the best quarterly return since 1Q16.